In early July 2019 the Government of Andhra Pradesh signalled its intention to make regulatory changes that would impact ongoing power purchase agreements with solar and wind developers. This move to retrospectively cancel or renegotiate signed and ongoing renewable energy contracts puts 7.4 GW of installed solar and wind power capacity in jeopardy.[1] The notification identifies areas of concern posed by renewable energy power but does not present any evidence on the nature or the quantum of losses due to backing down of thermal power. Nor does it furnish any data on the difference in the variable costs of thermal and solar and wind plants, which could help estimate the additional burden on the utilities by the allegedly expensive renewable energy sources.

The order directs tariffs to be revised downwards to INR 2.44/unit and INR 2.25/unit respectively for solar and wind power, from date of commissioning of projects, or termination of PPAs with the discoms. Further, the must run status granted to solar and wind power plants in their PPAs is also being contested. While several of the concerns raised by the AP government will be critical in assessing the scaling up of renewable power and could be factors to assess before future commissioning, the move towards cancelling, suspending, and renegotiating contracts sends a very poor signal to investors and developers, both in India and around the world. It raises concerns over the rule of law and the sanctity of contracts, in turn significantly hampering investor confidence in India’s clean energy market.

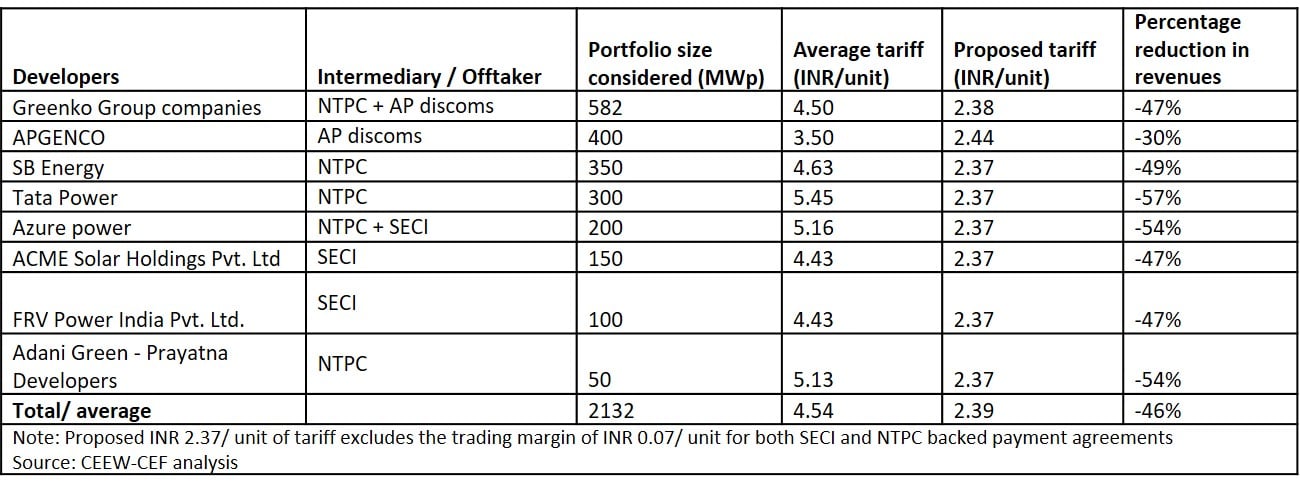

To understand the impact of the above, CEEW’s Centre for Energy Finance, analysed 23 affected solar projects by 9 power producers/developers. The projects considered for analysis, have a cumulative capacity of 2,132 MW and make up for 65 per cent of the total installed solar capacity of 3,307 MW in the state.[2] The total investment for these projects is estimated to be INR 10,000 crore (~USD 1.3 billion), with over INR 7,500 crore (~USD 1.07 billion) of debt outstanding.[3]

Table 1: List of projects reviewed and the impact on the revenue generation capacities

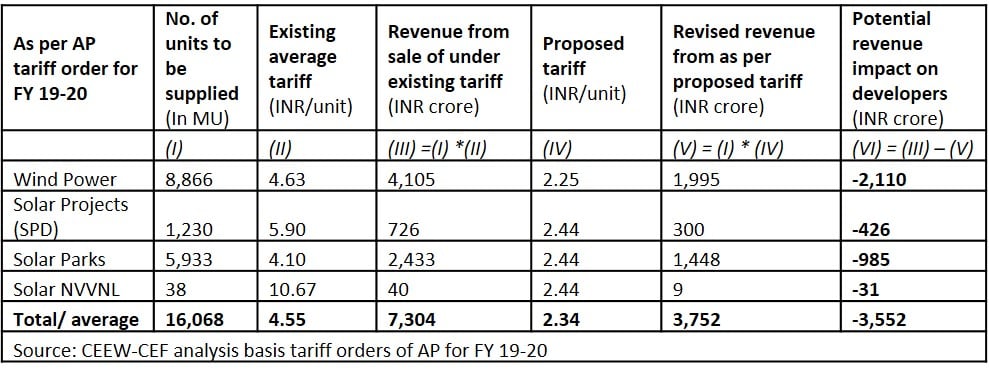

This proposed change in tariffs, of solar and wind power to INR 2.44/unit and INR 2.25/ unit respectively, if applied across to all the wind and solar power suppliers in state, will result in an adverse impact on revenues by over INR 3,550 crore every year for these projects (as per the tariff order of 2019-20). Individually, these wind power producers will see a revenue erosion of INR 2,100 crores of as against a sale of 8,866 million units of electricity during the year 2019-20.[4] Similarly, solar power developers would lose about INR 1,440 crore in revenues, against a supply of 7,200 million units of electricity to the distribution utilities in the state. As shown in table 2, the average tariff from both the wind and solar sources on average will be reduced by 48 per cent to INR 2.34 against the average tariff of INR 4.55 per unit of electricity.

Table 2: Impact on the revenue streams of wind and solar power suppliers to the state of AP

Historically courts have upheld contracts barring cases of corruption. The AP High Court stay order on the renegotiation and cancellation of PPAs has helped alleviate some of the immediate stress on the power developers but the market continues to reel under the stress of renegotiation not just in Andhra Pradesh, but also in other states if this were to go unchecked. Further, despite the stay order, there has been rampant curtailment of renewable power, which has a similar impact on developer revenues.

In the past, Change in Law clauses in PPAs have being invoked to seek reimbursements for developers for GST charges or pass through of safeguard duties. Renewable energy stakeholders have shown the necessary patience and trust in the legal process. However, in a rare instance if the Andhra Pradesh government is successful in this misadventure, we would begin to see DSCR of projects falling to 0.6x (i.e. inability of a project to meet the due debt repayments from the cash flows), leading to default or delay in debt repayments. Equity investors for these projects will also be staring at a reduced or negative equity returns. This may lead to termination of PPAs forcing developers to sell power in the open market.

This ad-hoc policy decision is particularly harsh on developers for whom investments in Andhra Pradesh form a sizeable part of their portfolio. This will place a stress not only at the project but also at holding company level resulting in a capital crunch and huge losses due to the underlying guarantees (associated with the project/ SPV financing in India). In order to continue India’s rapid acceleration along the energy transition pathway, it will be essential to control the damage caused by this notification on industry and investor sentiment across the country and limit its adverse impact to Andhra Pradesh.

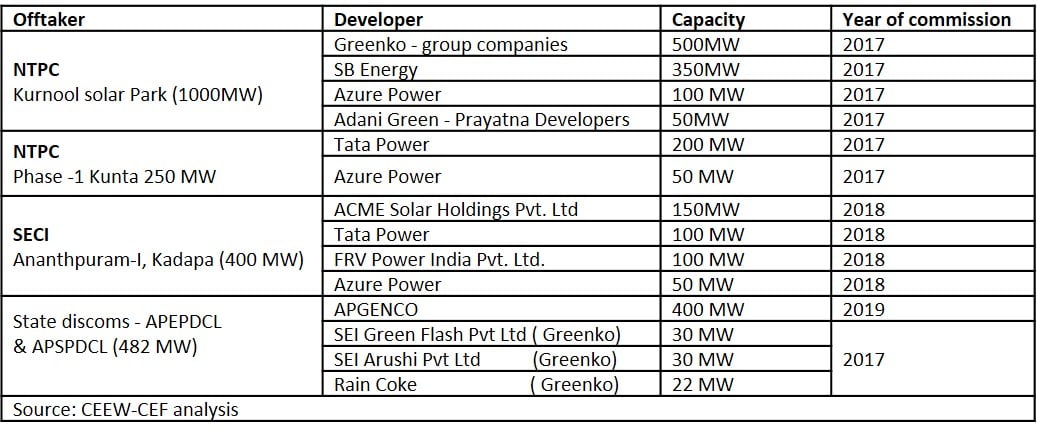

Annexure 1: List of projects, offtaker, capacity and year of commissioning of projects considered for analysis

References

- [1] MNRE (2019) “Physical progress (achievements),” available at https://mnre.gov.in/physical-progress-achievements, accessed on 30 July 2019.

- [2] MNRE (2019) “Physical progress (achievements),” available at https://mnre.gov.in/physical-progress-achievements, accessed on 30 July 2019.

- [3] Assuming a per MW cost of INR 4.5 crore on an average, with a debt to equity of 80/20 and loan tenure of 12 years and average loan repayment being 1.5 years across.

- [4] APERC (2019) “Tariff Orders / Current year orders,” available at http://aperc.gov.in/page/Tariff_Orders/Current_year_orders, accessed on 30 July 2019.