Cost of capital is a top priority in any discussion on infrastructure financing. Where renewable energy (RE) is involved, it assumes even greater importance. Among the various electricity generation types, RE stands out for its high degree of standardisation in technology and fixed costs, its zero feedstock cost, and its almost negligible (but not quite absent) operations and maintenance (O&M) cost structure. This leaves the power purchase agreement (PPA) tariff as just about the only feature that distinguishes one RE project from another. So, given this uniformity, how can developers differentiate themselves and outbid their competition? The answer is simple – raise funding from an investor with a relatively low cost of capital and one will have created the ability to bid relatively lower tariffs. Or so a popular line of thinking goes.

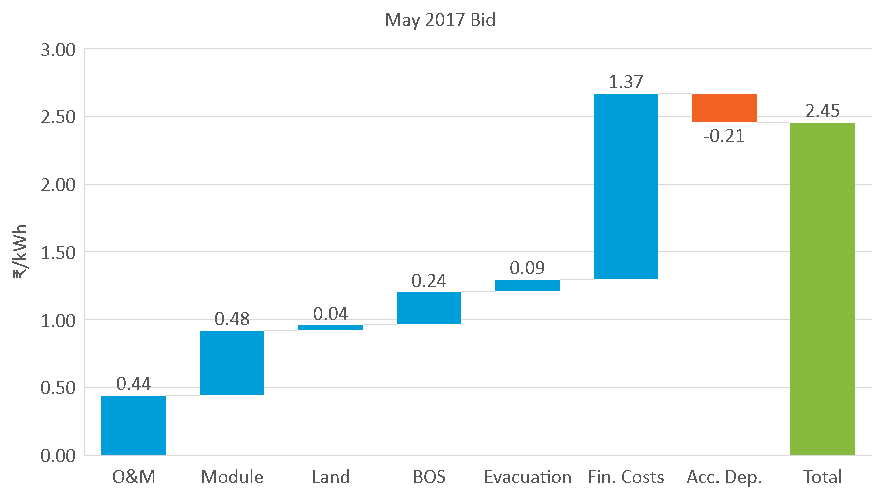

This line of thinking does have a certain appeal. It proposes a simple solution to what many RE developers believe is their principal challenge. Raising capital cheaply should certainly be a principal objective for any chief financial officer, particularly as financing costs are the single largest component in any RE tariff. This is apparent from the build up of the record-setting solar PV bids in India in May 2017.

Figure 1: Anatomy of solar tariff

Source: Chawla, Kanika and Manu Aggarwal. 2016. Anatomy of a Solar Tariff: Understanding the Decline in Solar Bids Globally. New Delhi: Council on Energy, Environment and Water.

However, raising capital on inexpensive terms requires a far more nuanced appreciation of the investor’s cost of capital, which is itself a function of past capital allocation decisions. This means investors do not usually price prospective investment opportunities using such a retrospectively derived yardstick. On the rare occasion that they do, it is only if a proposed investment mimics the capital structure and risk profile of their existing business portfolio. In other words, an investor with a low effective cost of capital does not necessarily represent an investor willing to part with capital on equally low terms.

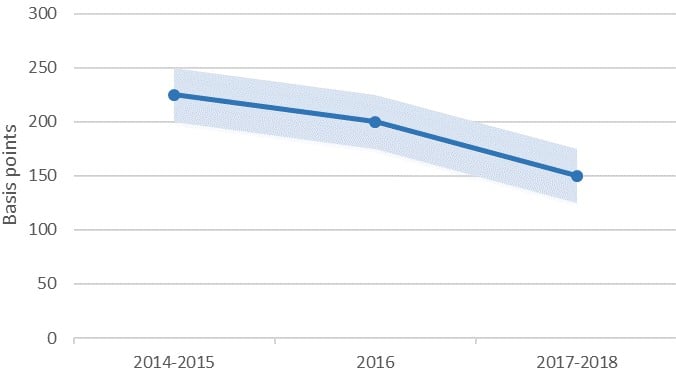

As such, developer interests would be much better served in constructing robust narratives around capital raises rather than searching for the elusive investor willing to extend capital on more favourable terms than what the broader market demands for comparable risk. This holds increasingly true as markets for various asset or risk classes mature and progressively deepen. And this is precisely where the global market for RE capital finds itself today. Evident to grow immensely in terms of absolute size, but also much more sophisticated in its ability to evaluate risks and returns compared to even just a few years ago. This reality is apparent from the way interest rate spreads for both solar and wind have progressively narrowed over recent years.

Figure 2: Interest rate spreads for solar PV and wind

Source: 2019. Clean Energy Investment Trends: Evolving Risk Perceptions for India’s Grid-Connected Renewable Energy Projects. New Delhi: CEEW & IEA.

What do robust narratives achieve?

Most importantly, robust narratives can greatly expand the pool of funding sources that developers target. India’s energy transition requires the mobilisation of a massive amount of capital. Global markets for capital and funding will have to play a vital role if the country’s energy ambitions are to be realised. Other developing countries will have similar requirements while pursuing their respective RE goals. Limiting the search to only investors with a “low cost of capital” is not just flawed for the reasons described above, but it also shuts the door on alternative sources. Investors will eventually extend capital on attractive terms not because their cost for it is low, but if they are convinced that the risk associated with a prospective investment is low. This means that if well constructed, such narratives have the potential to convert almost any investor to a provider of low-cost capital.

What should a robust narrative look like?

Project risk typically falls into three main categories. With very minor execution and O&M risks, the bulk of RE project risk falls in the offtake risk category. This last category must be addressed explicitly in any capital raising narrative. Drawing on correlations between the constituent elements of offtake risk and variables such as the offtaker’s identity, the contracted sale price for the power, the geographical location of power plants, and the share of intermittent RE in the transmission and distribution (T&D) infrastructure into which the power is being injected are just some critical building blocks of the narrative. In the Indian case, this assumes even greater importance. An increasing tendency among a section of market observers to label RE projects as risky, drawing from the unfortunate experiences of a subset of projects, threatens to cast a shadow over the Indian RE sector as a whole.

Who is best placed to construct such narratives?

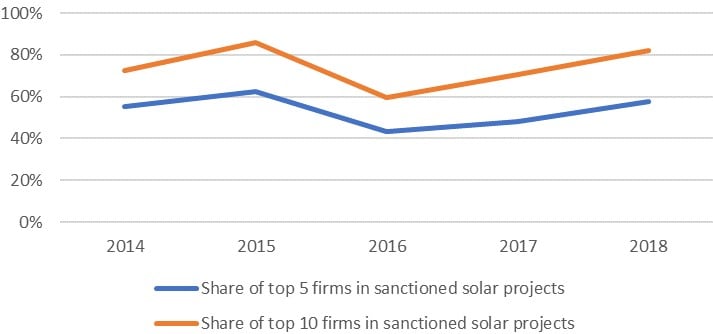

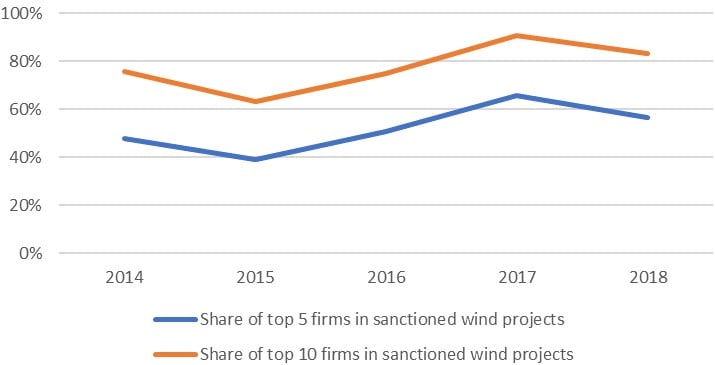

At present, large developers with scores of RE projects scattered around India hold a distinct advantage on this front. Empirical evidence supports this view, with market concentration (share of top 5 and 10 firms in sanctioned projects) remaining high in both solar PV and wind.

Figure 3: Market concentration in solar PV

Source: 2019. Clean Energy Investment Trends: Evolving Risk Perceptions for India’s Grid-Connected Renewable Energy Projects. New Delhi: CEEW & IEA.

Figure 4: Market concentration in wind

Source: 2019. Clean Energy Investment Trends: Evolving Risk Perceptions for India’s Grid-Connected Renewable Energy Projects. New Delhi: CEEW & IEA.

Some market observers cite the economies of scale advantages that such large development platforms enjoy. Scale certainly has its merits. As discussed in a previous CEF analysis piece, it sometimes manifests itself in a broadly fixed development overhead cost base, generating ever increasing cash flow streams. At a less appreciated level, scale allows these platforms to harvest invaluable proprietary datapoints, which are continuously churned out by their numerous projects. The extent to which these platforms are able to convert this information into a measurable capital pricing advantage depends, of course, entirely on the quality of the narratives they are able to construct around their proprietary datasets.

In conclusion, until such time as publicly available datasets are improved – or better yet, replaced by fit for purpose RE-specific databases – large entrenched developers will remain in an advantageous position to source capital at relatively more attractive terms. This is not because of some general size advantage, but because of their information advantage. However, meeting India’s RE targets requires far greater momentum than what exists in the status quo. Increased democratisation of data, available freely to all, can help put the entire range of developers – big, small, and even those sitting on the side-lines – on equal footing. And the greatest number of participants in RE, each equally well placed to access capital on the best possible terms, is precisely what India needs.

Do you believe accessing capital for RE on attractive terms is only about finding an investor with a low cost of capital or is there more to it? Share your views and comments on the above CEF analysis at [email protected]