Overview

This report provides context, and investigates the reasons for the higher cost of Indian solar modules. Further, it recommends key interventions needed to scale up domestic manufacturing of crystalline solar photovoltaic (PV) modules in India. The domestic manufacture of solar PV cells and modules has not kept pace with India’s rapid advances in the energy transition in recent years. China still accounts for a majority of India’s solar PV imports. Indian PV module manufacturers lack competitiveness because of higher prices and lower capacity utilisation compared to China. The report assesses the competitive advantage that China has over India, and presents a suite of short-term and long-term interventions required for a vibrant and globally competitive solar manufacturing sector in India.

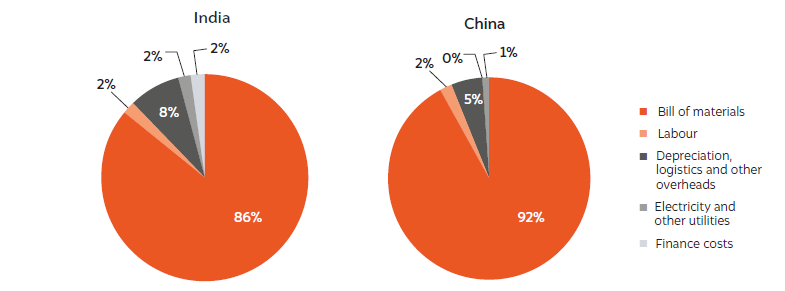

The difference in the contribution of bill of materials to module selling prices is the highest between India and China

Source: CEEW-CEF analysis*

* based on a primary survey conducted with key manufacturers in May 2020.

Key findings

- Indian solar modules are nearly 33 per cent more expensive than Chinese modules

- Around 56 per cent of this difference in selling prices(INR 3.32/Wp) is due to differences in the bill of materials (BOM) costs

- In India, BOM costs account for nearly 86 per cent of the selling price, while labour, electricity, utilities, land, logistics, and finance costs make up the remaining 14 per cent.

- In China, 92 per cent of the module selling price is based on BOM costs, while other costs account for 8 per cent of the price.

- Large-scale and automated manufacturing lowers labour and overhead costs in China, which also has better financing options.

- Indian solar manufacturers import most components and raw materials

- Up to 20 per cent basic customs duty (BCD) on solar cells and modules would be required until 2027 to ramp up India’s domestic solar manufacturing

- At current levels of tariff and module prices, it is expected that with 10 and 20 per cent increase in module prices, the tariff may increase by 5 and 10 per cent, respectively. So a 20 per cent BCD may lead to an increased tariff of INR 0.20 to 0.25 per unit of electricity.

- India should start the manufacturing process from processing of quartz and also scale up manufacturing capabilities to produce solar glass, EVA, backsheet, junction box and other components.

- Reduced reliance on imported products will make the sector self-sufficient, competitive, and resilient to supply chain disruptions.

- Apart from increasing India’s energy security, the domestic solar manufacturing industry would also help in the creation of jobs and growth of the economy.

- An integrated cell and module manufacturing would generate around 2.6 full-time equivalent jobs per MW of output.

Key recommendations

Short-term interventions

- Provide visibility of a demand pipeline and develop eco-system by providing policy stability and continuity, quality infrastructure, and a mature banking system

- Levy a BCD of 10 per cent on modules till March 2021 and 20 percent from April 2021 to March 2027.

- Introduce a short-term production subsidy at INR 1.5/watt till March 2021. An additional support of INR 1/watt may be provided to module manufacturers using domestic cells.

- Limit the production subsidy support to 250 MW per manufacturer to ensure that small players can run at full capacity, and larger companies can increase their CUF.

- Provide clear information on the implementation timelines and tenure of the proposed BCD

- Levy higher duty on modules and lower duty on cells to ensure that module facilities can increase their capacity utilisation factor (CUF), and new cell manufacturing facilities can be commissioned.

- Introduce new domestic procurement programmes such as the Central Public Sector Undertaking Scheme (CPSU)

- Record data in both capacity terms (kW units) and monetary value (INR) to accurately estimate imports, and design policy interventions accordingly.

- Set a national target of installing at least 50 GW of manufacturing capacity by 2030

- Incorporate solar manufacturing as a focus industry in foreign policy and collaborate with governments and private parties in Europe, Japan, and the United States of America.

Medium to long-term interventions

- Levy BCD on solar wafers from 2027 to 2030 in line with BCD on solar cells and modules. The process to manufacture modules from quartz could be planned to begin by the same year.

- Encourage public sector undertakings (PSUs) such as Bharat Heavy Electricals Limited (BHEL) and Bharat Electronics Limited (BEL) to lead solar manufacturing indigenisation effort.

- Consider materials that can be sourced within the country. Engage micro, small, and medium enterprises (MSMEs) to source these materials,

- Incentivise domestic manufacturers to develop, commercialise, and produce manufacturing equipment indigenously with cash prizes

- Set up 10 GW solar equipment manufacturing parks near ports in Maharashtra, West Bengal, Andhra Pradesh, and Tamil Nadu

- Rope in technology institutions like Indian Institute of Technology (IIT) Bombay, IIT Delhi, IIT Madras, and the Indian Institute of Science (IISc) Bangalore to develop novel solar technologies and commercialise them

- Provide access to low-cost capital to scale up their polysilicon and wafer manufacturing facilities.

- Set up an inter-ministerial body for ministries with overlapping mandates to work in tandem.