Since the tabling of the Union Budget on 1 February 2020, the solar industry has witnessed a lot of uncertainty and confusion. In the Finance Bill, 2020, the customs duty rate of solar cells and modules has been amended. The complexity of the applicable taxation structure on imported solar cells and modules has also increased.

Applicable customs duty before the amendment

The basic customs duty (BCD) for any good mentioned in the First Schedule to the Customs Tariff Act, 1975. Any amendment to the First Schedule can only be made by way of amendment to the Act in Parliament. These typically have been amended by the finance acts passed to implement the annual budgets. The central government, however, is empowered to exempt any good from BCD either partially or entirely.

Each good in the first schedule also falls under a customs tariff head (CTH) and assigned a number which is also the numeric code for that good for international trade purposes (called the ITC (HS) code). Further, by way of notification number 24/2005-Customs dated 1 March 2005, and as amended from time to time (the ‘Exemption Notification’), the central government had exempted goods falling under the tariff item 8541 from the whole of the customs duty. This exemption complies with India’s commitment under the World Trade Organisation’s (WTO) Information Technology Agreement -1 (ITA-1) which requires members to eliminate tariffs on IT products covered by it.

Until the amendment on 1 February 2020, the CTH for ‘solar cells whether or not assembled in modules or panels’ was 8541.40.11 and the rate of duty was nil. Though certain solar panels or modules equipped with ‘blocking diodes and bypass diodes’ were classified under heading 8501 (as ‘electric motors and generators’) and attracted 7.5 per cent BCD.

The amendment

In the Finance Bill, 2020, the tariff item 8541.40.11 has been replaced by two items: 8541.40.11 and 8541.40.12 which are described as ‘solar cells, not assembled’ and ‘solar cells, assembled into modules or made up into panels’ respectively, and a rate of tariff of 20 per cent has been prescribed against each of the tariff items. It is important to understand that though this provision is immediately effective, the BCD is still nil since the Exemption Notification is subsisting. It is pertinent to note that the Exemption Notification has not been consequently amended to reflect the split in tariff heading of solar cells and modules.

Further, the exemption of these items from Social Welfare Surcharge (which surcharge was introduced in 2018 budget) (SWS) has been withdrawn by way of notification number 9/2020 dated 2 February 2020, and consequently, a surcharge of 10 per cent of the BCD payable will be applicable on solar cells and modules.

The Finance Ministry appears to have made these changes pursuant to the specific request of the Ministry of New and Renewable Energy (MNRE). In September 2019, it was reported that (here and here) MNRE had proposed imposition of basic customs duty (BCD) on solar cells and modules April 2021 onwards and recommended that there be two different BCD tariff heads for solar cells and solar modules. The proposed rates were staggered starting from 10 per cent in April 2022 to 30 per cent from January 2023 onwards. MNRE further asked the finance ministry to exempt products such as wafers, EVA, glass, silver, paste, frames, and structures, used to manufacture modules in India, from customs duty until 31 December 2023, after which 15 per cent BCD could be imposed on these products as well. The move is part of the government’s bid to boost local manufacturing and protect domestic companies from cheaper imports under the ‘Make in India’ scheme.

Safeguard duty on solar cells and modules

On 30 July 2018, by way of a notification, the Ministry of Finance (Department of Revenue) has imposed an ad valorem safeguard duty (SGD) on solar cells (on cells imported from China and Malaysia and other developed countries). The safeguard duty was implemented in a staggered manner starting with 25 percent which was reduced to 15 per cent for the period 30 January 2020 to 29 July 2020. This notification has been amended on 2 February 2020 to reflect the split in the tariff headings of solar cells and solar modules.

Applicability of customs duty in SEZs

It is necessary to direct attention to the applicable duties on cells and modules manufactured in special economic zones (SEZ) because there is a substantial presence of cell and module manufacturing capacity across the country’s SEZs. As per data compiled by the Directorate General of Trade Remedies, as of July 2018, SEZs have cell and module manufacturing capacities of 2000 MW and 3825 MW respectively, as against 1164 MW and 5053 MW capacities in the rest of the country.

As per provisions of the Special Economic Zone Act, 2005, goods cleared from SEZs to the domestic tariff area (DTA) are subject to payment of the same customs duties as are applicable on imported goods. This provision was used to make the SGD imposed in 2018 applicable to cells and modules manufactured in SEZs. BCD will also apply to goods manufactured in SEZs and cleared in the DTA.

Applicable GST

All imports are deemed as inter-state supplies and the integrated goods an services tax (IGST) is levied on imported goods in addition to the applicable customs duties. Photo-voltaic cells, whether or not assembled in modules or made up into panels attract an integrated GST rate of 5 per cent. The tax is calculated on a compounded basis. That is, the IGST is levied on the value of the good plus the applicable customs or any other chargeable duty.

When will the Exemption Notification be withdrawn?

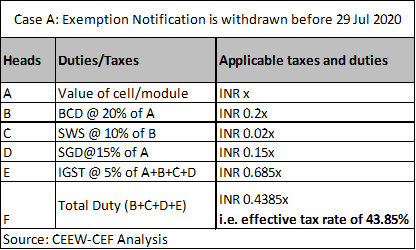

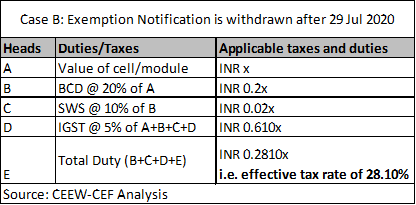

Solar developers are in a state of uncertainty due to these recent developments. It is expected that the Exemption Notification will continue to be effective until the applicability of SGD till 29 July 2020. However, no clarification has been given by the government till date, on this. In the absence of clarity, multiple scenarios are possible with varying implications on the effective tax rate on imported solar cells and modules.

Hence, without SGD, the minimum effective tax rate is going to be at least 28.10 per cent. In case the Exemption Notification is withdrawn while SGD continues to be applicable, the tax incidence on imports can go up to 43.85 per cent as well.

Further, the Finance Ministry can modify the Exemption Notification in a manner in which there is a separate duty structure for cells and modules. These uncertainties would be severely detrimental to the investment decisions of developers. In 2018, the uncertainty surrounding the imposition of the safeguard duty resulted in reduced participation of developers in renewable auctions. In 2019, CEEW noted that between January and April 2018, only 1.25 GW of capacity was awarded against the 13.3 GW of capacity tendered.[1] The imposition of SGD also resulted in multiple petitions before the electricity regulatory commissions (ERC) for the inclusion of SGD imposition as a ‘Change in Law’ event in the power purchase agreements. Ultimately, many of these petitions were granted and the consumers eventually bore the higher cost.

The imposition of the BCD on solar cells, in contravention of the ITA-1, may also be susceptible to challenge under the WTO’s dispute procedure. Though considering the crisis at the Appellate Body, which has arisen due to the USA’s blocking of further appointments to the WTO dispute settlement body, it is unlikely that any challenge will be practically possible. However, the impending presidential elections in November 2020 in the USA and the possible effect on WTO policies adds another layer of ambiguity.

Conclusion and way forward

CEEW had, in early 2019, recommended that trade data be recorded separately for solar cells and modules. This would allow for more targeted policy making for the two separate products. The imposition of SGD on solar cells was eventually detrimental to only the developers without the corresponding benefits.[2] It is hoped that the split in the classification of cells and modules will ultimately lead to more targeted policies for each of them. Also, manufacturers based out of SEZs will lose the competitive advantage over their DTA counterparts since BCD will be applicable to the final value of the product (unlike SGD which was applicable only to raw material which was imported in the SEZ). We may even see manufacturers shift out of DTA to ensure competitiveness when compared to imported products.

As a result, there is an urgent need for clarity and certainty on the customs duty structure. Lessons from the imposition of the safeguard duty have demonstrated the need for certainty and transparency. Any delay in clarity will lead to higher tariffs, anticipation and dampening of investor confidence, and lower participation in bids leading to a recap of the adverse impact the inefficient imposition of policies witnessed in 2018.

References

- [1] Dutt, Arjun, Manu Aggarwal, and Kanika Chawla. 2019. What is the Safeguard Duty Safeguarding? Analysing Impact on Solar Manufacturing and Deployment in India. New Delhi: Council on Energy, Environment and Water, p.8

- [2] Ibid, p. 62.