Overview

This issue brief evaluates the role of the high costs of domestic finance and land and in pushing up renewable energy tariffs in Indonesia. The country’s energy transition has been embroiled in challenges that have prevented large scale solar and wind capacity development. Two of the major challenges are land acquisition and unviable tariff caps. This brief analyses a specific project where these constraints do not apply - the 145 MW floating plant being developed by PLN (Indonesia’s state-owned power utility) and Masdar. The plant is being developed at a tariff of USD c 5.8/kWH, which is around 26% lower than Indonesia’s average generation cost of USD c 7.66/kWH in 2018. It illustrates that a 22% reduction in tariffs is possible for land-based utility projects. Additionally, it offers recommendations for attracting international capital and de-risking renewable energy investments in Indonesia.

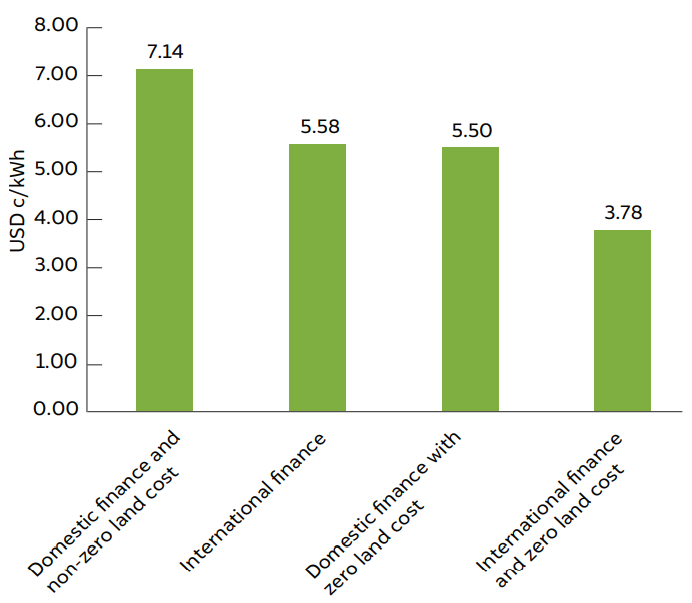

Variations in utility-scale solar tariffs under various scenarios

Source: CEEW-CEF analysis

Key highlights

- The floating solar project has several competitive advantages. PLN does not have to bear any additional costs for leasing space on the lake to set up the project

- This enables the developers to save on land-related costs, which amount to 20 to 30 per cent of the capex of comparable projects developed on land in Java

- It is assumed that Masdar will raise the debt capital for the project on its own balance sheet or will guarantee its repayment

- Since Masdar is a state-owned entity, the debt is assumed to be raised at close to the sovereign borrowing rate for the Abu Dhabi government

- Offtake risk is reduced given that PLN would be the purchasing counterparty

- For floating solar, the largest share - 49 per cent - of the levelled cost of electricity comes from the high capex associated with equipment (solar modules, inverters, floating structures, and other balance of system)

- For a utility-scale solar in Java for a project financed with domestic capital and with land costs also factored into the inputs, finance costs account for approximately 48 per cent of the tariff, equipment costs for 27 per cent, and land costs for 21 per cent.

- Utility-scale projects financed by international sources of capital could achieve a 22 per cent reduction in tariffs compared to those funded by domestic sources. If land costs were eliminated, tariffs would decline by 23 per cent

- If international costs were applied and land costs were eliminated simultaneously, the tariffs would decline by 47 per cent.

Key recommendations

- Government agencies should take up land aggregation to lower land acquisition risks for developers

- Review existing regulatory structures and address PLN’s conflicts of interest

- Create certainty of demand for RE by:

- conducting regular tenders for RE procurement

- setting renewable portfolio standards for commercial and industrial consumers and PLN

- Review existing capacity-planning methodologies and assumptions to avoid overcapacity in generation

- Announce a multi-year tendering schedule to create a clear pipeline of RE projects for developers

- Address land and transmission constraints by:

- facilitating RE grid integration using flexible sources of generation

- strengthening existing transmission infrastructure

- establishing solar/wind parks

- Address the skill gap in the RE sector

- Adopt catalytic financing to facilitate the flow of RE investments at scale

- PLN should consider adopting new utility-led rooftop solar business models (implemented in India) to drive rooftop solar adoption