Council on Energy, Environment and Water Integrated | International | Independent

Bamboo is a fast-growing, woody grass known for its strength and rapid renewability, making it a valuable resource across various sectors, including furniture, construction, and power generation. India possesses the largest bamboo-bearing area globally (Bansal 2020). Despite its abundance, India imported 88 per cent of the raw material required for bamboo-based industries in 2021 (Mathur 2023). This is because much of India's bamboo resources are in protected areas, steep slopes, and remote regions, making harvesting and extraction undesirable and challenging. Additionally, low bamboo productivity in forested areas escalates raw material costs, making imported bamboo economically favourable for domestic industries (FMC 2022). Therefore, there is a pressing need for large-scale bamboo cultivation to unlock the potential of the bamboo-based economy. Establishing bamboo plantations and processing units has the potential to stimulate the local rural economy and increase farmers' incomes. Odisha can accelerate economic growth and contribute to India's self-reliance mission by scaling both bamboo demand and supply through commercial cultivation on wasteland and its utilisation in sectors like furniture, construction, agarbatti, charcoal, packaging, etc.

Jobs, market and investment opportunity

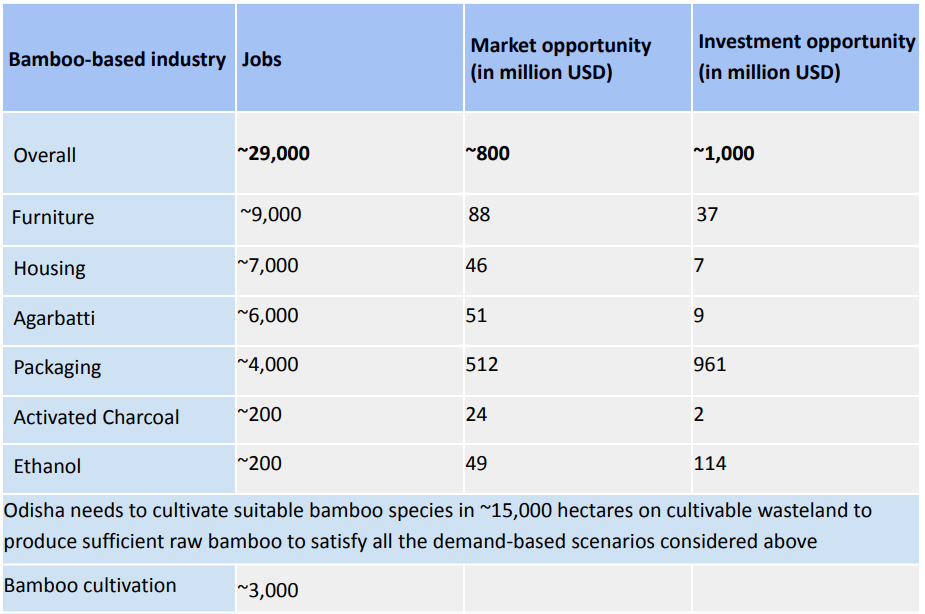

By cultivating bamboo across ~15,000 hectares (~3 per cent) of cultivable wasteland and integrating it into bamboo-based industries such as furniture, housing, agarbatti, packaging, activated charcoal, and ethanol, Odisha could generate ~29,000 jobs by 2030 (of which 3,000 jobs are created through cultivation). The endeavour requires a cumulative investment of ~USD 1,000 million, unlocking a market opportunity worth ~USD 800 million annually.

Table 1- Employment, Market, and Investment Potential for Various Bamboo-Based Sectors in Odisha by 2030 under Ambitious Scenarios

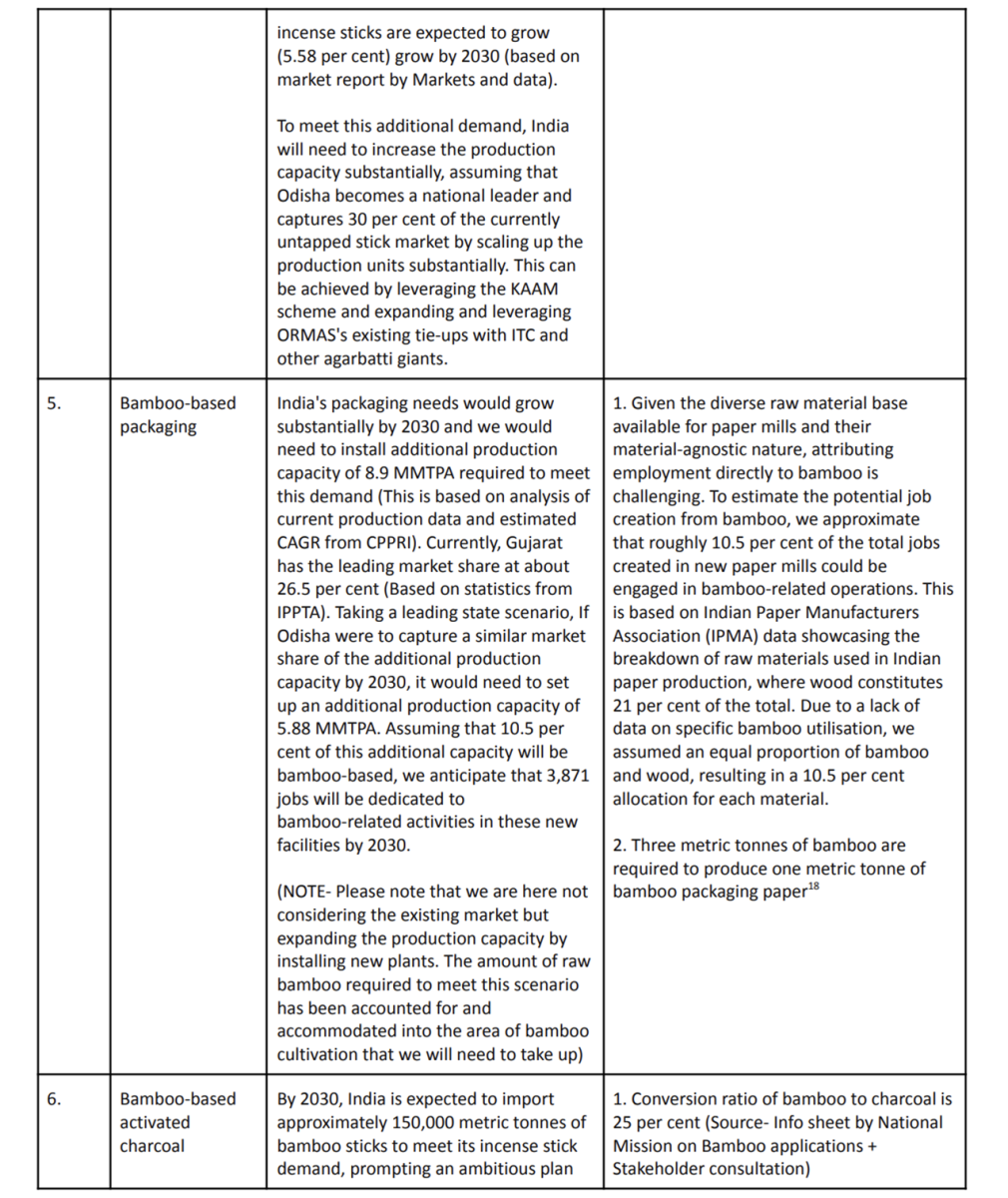

Reduce import reliance: India imports 88 per cent of the raw materials needed for bamboo-based industries from other countries (Mathur 2023). By investing in the bamboo value chain—expanding bamboo cultivation and strengthening processing capacity to produce finished products—Odisha can increase self-sufficiency and reduce import dependence.

Achieve energy security: Odisha can strengthen state and national energy security by investing in bamboo-based biofuel technology, as bamboo serves as a promising feedstock for biofuel production (Chin et al. 2017). This investment offers Odisha a valuable opportunity to develop its bamboo value chain.

Enhanced income and quality of life for rural women and artisans: a. By engaging in various stages of the bamboo value chain—from harvesting to processing and marketing, women can secure better livelihood opportunities (Datta et al. 2017), which would not only boost their financial independence but also raise their status within their communities. b. Artisans often lack access to markets and technology, and their income fluctuates due to seasonal demand and agricultural cycles. Investing in bamboo value chains, particularly bamboo mat weaving for construction-grade mat boards, allows Odisha to support artisans with new market opportunities, better production technologies, and financial assistance (Patel et al. 2022).

Reduces GHG emissions: Bamboo reduces GHG emissions by acting as a carbon-negative plant, capturing more CO2 than it emits throughout its life. It stores 30-120 mg of carbon per hectare and sequesters 6-13 mg annually (Manandhar 2019). The carbon stored in bamboo remains locked within its biomass, whether used in products or construction materials, preventing its release (Shukla & Joshi 2020). Bamboo also serves as an energy-efficient building material, requiring only 30 MJ/m3 per N/mm2 production, far less than concrete, steel, and lumber, which need 240, 500, and 80 MJ/m3 per N/mm2 , respectively. Bamboo processing consumes just one-eighth of the energy needed for concrete, one-sixteenth for steel, and half for lumber (Gutiérrez 2000).

Restore degraded ecosystems: Promoting bamboo farming on wastelands 5 could help reduce soil erosion, as a single bamboo plant can help bind soil up to six cubic metres. Bamboo also improves soil fertility by adding organic matter, which enriches the ecosystem and creates habitats for various primate species (Shukla & Joshi 2020).

Overall, strengthening bamboo value chains will directly contribute to seven of the seventeen sustainable development goals (SDGs), including poverty reduction (SDG 1), access to energy (SDG 7), economic growth (SDG 8), resilient cities (SDG 11), responsible production and consumption (SDG 12), climate action (SDG 13), and biodiversity conservation (SDG 15). This approach will also foster stronger implementation and partnerships (SDG 17) (INBAR 2015).

Bamboostan, a Guwahati-based startup, is building a robust bamboo supply chain in the Northeast by procuring raw bamboo from farmers and processing it into beams, sticks, slats, and other products for the construction and paper industry. Bamboostan procures nearly 24,000 MT of raw bamboo annually from local farmers to ensure a steady supply of standardised bamboo products to private players, thereby creating value for local communities by providing steady income and livelihood opportunities6.

1. Role of departments:

Odisha Bamboo Development Agency (OBDA): OBDA is responsible for promoting the overall growth and development of the bamboo sector in Odisha. Therefore, it would play a significant role in scaling up the bamboo value chains. It should promote integrated development, which involves coordinating on-farm and off-farm activities to ensure a seamless flow from bamboo cultivation to final product manufacturing. OBDA also provides technical support, market linkages, research, and innovation, encourages investment, and fosters collaboration between various departments.

Forest, Environment and Climate Change Department: The department can facilitate coordination, support policy implementation, and ensure adherence to environmental regulations during the planning and scaling up of the bamboo value chain in Odisha.

Micro, Small, and Medium Enterprises Department (MSMED): The MSME department can play a pivotal role in supporting OBDA by collaborating with incubators such as Sambalpur University and KIIT-TBI, as well as initiatives like StartUp-Odisha, to promote bamboo-based startups, providing financial support, facilitating market access, promoting research and development, and streamlining licensing procedures. The MSME department could collaborate closely with Mission Shakti to effectively engage women SHGs and their federations in bamboo product production in value chains such as bamboo mats, etc.

Housing and Urban Development Department: The department can champion bamboo as a construction material by actively endorsing bamboo-based housing projects and collaborating closely with OBDA. Targeted policies and incentives, such as mandating that 30 per cent of government housing integrate bamboo as its primary raw material, can stimulate the adoption of bamboo-based construction techniques among builders and developers. Moreover, by organising capacity-building workshops and launching awareness campaigns, the department can raise awareness and generate demand for bamboo-based construction solutions across the state.

Odisha Rural Development and Marketing Society (ORMAS): ORMAS is an autonomous body under the Odisha Panchayati Raj Department that could help OBDA promote bamboo-based industry in rural areas by assisting in forming bamboo-based producer groups, and providing support in technology adoption, product diversification, packaging, branding, and sales. ORMAS should also facilitate market linkages by organising buyer-seller meets and creating an online marketplace for bamboo products.

Odisha State Pollution Control Board: The Odisha State Pollution Control Board (OSPCB) should regulate bamboo-related ventures to ensure compliance with environmental standards and promote sustainable practices. This involves conducting Environmental Impact Assessments, advocating for the adoption of cleaner technologies, and organising training initiatives to raise awareness. By doing so, the OSPCB can actively promote the establishment and operation of environmentally responsible bamboo industries in Odisha.

Indian Council of Forestry Research and Education (ICFRE): ICFRE can conduct advanced research on bamboo species, sustainable forestry practices, and perform ecological mapping to evaluate bamboo quantity, productivity, and area coverage.

Science and Technology Department (S&TD): The department could work to improve the bamboo sector through technology promotion and its dissemination by including bamboo as a special area in the S&TD supported incubators, and other programmes. The department could also promote application-oriented research in the bamboo sector and support projects that are entrepreneurial in nature and can be commercialised.

Odisha Skill Development Authority (OSDA): OSDA should integrate bamboo value chain-related skilling into coursework and offer specialised training programmes and workshops to enhance the skills of bamboo farmers, artisans, and entrepreneurs working in the bamboo sector. OSDA also has the potential to facilitate the adoption of modern technologies and offer entrepreneurship support services to aspiring bamboo entrepreneurs.

Odisha can establish a focused policy on the bamboo-based economy, assign specific mandates and roles to different line departments regarding bamboo and its products’ promotion, and set targets for monitoring bamboo development in the state, similar to Assam, Tripura, and Nagaland.

2. Role of the private sector:

Corporate social responsibility (CSR): Private players can help mobilise the CSR funds to raise bamboo plantations. They can also enable bulk procurements from the farmers to ensure long-term income security for cultivators. i. Dalmia Cement, for instance, is attempting to make its cement greener by using bamboo instead of fossil fuels to make cement and collaborating directly with bamboo farmers to ensure backward linkage. ii. ITC is taking proactive measures to support bamboo farming in India's northeastern states, facilitating a stable supply of bamboo sticks for its agarbatti brand, Mangaldeep. This initiative not only promotes sustainable sourcing practices but also significantly uplifts the livelihoods of local communities. iii. Financiers will play an important role in enabling finance for cultivation, processing, and downstream operations in the form of working capital and project financing.

Collaborations: The private sector should work closely with farmers, either through CSOs or directly, to share knowledge about bamboo species, quality, and cultivation practices. This collaboration will help farmers produce the high-quality bamboo needed for downstream processing. Private players should also partner with OSDA to align skilling initiatives with industry requirements and work with ORMAS to ensure that farmer producer organisations (FPOs) support industry-aligned objectives. Another important role that the private sector could play is by collaborating with SHG federations through initiatives like Mission Shakti. Such partnerships should focus on enabling more value addition to bamboo by farmers rather than viewing communities solely as suppliers of raw materials.

Product design: The private sector could play a crucial role in addressing functional gaps in scaling up the bamboo value chain by innovating in product designs and improving quality to better meet customer needs.

3. Role of local administration and civil society organisations (CSOs):

Shifting focus: Despite being the second-largest producer of bamboo globally, India has a negligible presence as a supplier in the world's bamboo market. This is primarily due to India's continued focus on low-value and slow-moving products, such as handicrafts and utility items made from unprocessed bamboo. These products often require specific bamboo species that are hard to source, further limiting their scalability. Additionally, India's bamboo market is primarily driven by domestic demand, and we currently import significant amounts of bamboo to meet internal needs (INBAR 2018). While addressing this domestic shortfall is critical, there is also a distinct opportunity to capture global markets with high-value and industrial bamboo products, such as bamboo-based packaging and construction materials. Meeting domestic demand for products like agarbatti should remain a priority but simultaneously pursuing global opportunities for industrial products will help diversify the sector and tap into larger markets.

1. Sector-wide challenges

a. Limited awareness: Currently, the general awareness about bamboo's use beyond the handicraft sector, such as in construction and packaging, is relatively limited among the masses, as well as with industry players.

Way forward: We can increase consumer awareness regarding different use cases of bamboo by incorporating bamboo as road dividers, ceilings in government buildings, and furniture in public parks, as well as by launching public awareness campaigns to encourage broader adoption of bamboo in non-traditional sectors.

b. Locational challenges: Bamboo-based industries are often far from bamboo-bearing areas, leading to increased raw material procurement costs driven by historical industrial zoning and availability of infrastructure rather than proximity to raw materials (Awadh 2010).

Way forward: To ensure the year-round availability of cheap raw materials, manufacturers should situate their production units closer to bamboo cultivation areas. This needs to happen in parallel with CSOs encouraging more farmers to adopt bamboo cultivation through FPOs and linking them with bamboo-based manufacturers to provide assured markets to farmers. The private sector, through CSOs, can mainstream the use of hand-held mechanised equipment, allowing farmers to create bamboo splinters on the field before aggregating them to be sent to manufacturing units, which can increase a truck's loading capacity, saving further transportation costs.

c. Low price competitiveness: Bamboo-based bioplastics and mats are taxed at 18 per cent GST, while bamboo flooring faces 12 per cent GST. Taxing bamboo-based products at a higher GST rate than conventional products makes them less appealing to consumers.

Way forward: Reducing GST to 5 per cent for the above-mentioned bamboo-based products can make them more attractive to consumers and encourage greater adoption of these products among end-users7.

d. Lack of research and development: Bamboo sector faces a significant challenge due to insufficient research and development (R&D) on effective raw material utilisation and product design limiting the ability to create a diverse range of standardised products to maximise economic potential of bamboo.

Way forward: To significantly reduce waste during the harvesting and primary processing of bamboo, we must encourage farmers to adopt simple hand-held tools that enable sustainable harvesting while reducing wastage. We need to mainstream cost-effective and innovative technologies that enable cultivators and bamboo-dependent communities to produce diverse industrial applications for bamboo, including charcoal production, packaging solutions, composite materials, and biofuels (Liese and Kohl 2015).

e. Financing needs: Financing bamboo-related projects presents challenges, particularly for startups and entrepreneurs testing new technologies. The National Bamboo Mission (NBM) provides substantial financial support through a credit-linked back-ended subsidy8 , but it requires entrepreneurs to contribute 10 per cent of the total project cost. The government covers 50 per cent through subsidies, and banks finance the remaining 40 per cent. This model works well for entrepreneurs with proven technologies in a mature market, but it poses challenges for small startups experimenting with newer technologies that need to overcome entry barriers.

Way Forward: Foster innovation by providing smaller grants similar to BIRAC BIG grant9 to support startups working on novel industrial applications of bamboo. These grants better suit entrepreneurs testing new technologies by reducing entry barriers.

f. Lack of perceived demand: Several bamboo-based companies we consulted expressed concerns about the perceived lack of demand for non-traditional bamboo products like bamboo charcoal, bamboo based packaging, and construction materials. This lack of demand arises from customers being unaware of these products and high price points (Patel et al. 2022; APN-GCR 2020).

Way forward: The government of Odisha can drive initial demand for non-traditional bamboo products like bamboo-based construction products through public procurement programmes, such as mandating that some percentage of all government housing projects utilise bamboo as the primary raw material by including these bamboo-based products in the rate schedule. Players manufacturing other non-traditional products, such as bamboo packaging, must also work closely with end-users to tailor their products per customer requirements. Securing long-term supply agreements with guaranteed buy-back provisions would offer manufacturers greater price stability, while end-users could benefit from emission reduction credits for adopting sustainable bamboo solutions.

2. Sector specific challenges:

a. Bamboo-based construction sector

i. Perception of durability: Traditional construction materials such as steel and cement are perceived to be more durable than bamboo-based alternatives. The issue worsens further as architects and engineers do not know how to use bamboo in construction effectively, nor are they interested in learning about it as they require additional learning effort (UNDP 2023).

Way forward: The government should take the lead in mainstreaming the use of bamboo in construction by utilising bamboo to lay the foundation and interior decoration of important public buildings (Yadav and Mathur 2021). This can be done by encouraging states to include bamboo in the schedule of rates for construction and by developing these construction projects in PPP10 mode by incentivising the private players to use bamboo as a construction material through subsidies, tax break and other incentives. Innovations such as engineered bamboo products11 have improved the performance and durability of bamboo. However, more innovation, research support, and widespread dissemination of existing technology and know-how among architects and construction workers are needed. To promote bamboo-based construction, we must integrate bamboo into coursework through specialised training programmes and workshops for architects and engineers supported by organisations like BMTPC 12and the Construction Skill Development Council of India13.

ii. High entry barriers: New entrants in Advanced Housing Construction Materials (AHCM)14 manufacturing faces significant challenges, such as high initial capital investment and limited access to technology, as many of these technologies are imported. Without government support, it is difficult for new players to gain market share.

Way forward: The government could offer fiscal incentives to establish manufacturing units and invest in R&D to develop low-cost indigenous technology, reducing import dependence and supporting local manufacturing. Reducing GST rates on bamboo-based construction products would lower costs and make them more attractive to manufacturers and builders15.

b. Bamboo-based furniture industry

i. Physiological barriers: Joining two pieces of bamboo together to make an aesthetically pleasing and durable modern furniture is difficult due to the natural physiology of bamboo (Pritchard 2023). The inter-nodal distance varies greatly depending on its species, age, and growing conditions of bamboo (Dessalegn et al. 2022). This irregularity results in misalignment, and inconsistent load-bearing capacity at joints impacts the durability of the product.

Way forward: The government must collaborate with the National Institute of Design to foster innovative design processes that use bamboo's natural characteristics to create modern, aesthetically appealing furniture (Susanth et al. 2023). These modern joinery techniques need to be documented in the form of process manuals and disseminated among artisans, designers, and manufacturers.

ii. Poor quality of products: Despite Indian artisans producing bamboo-based furniture for several years, the Indian bamboo furniture sector has struggled to scale up and capture market share. This stagnation results from the current approach to design and construction that relies heavily on hand-held tools and semi-mechanised processes, which limits efficiency and consistency in product quality (Susanth et al. 2023).

Way forward: Industry needs to adopt a component-based production system to facilitate easier production, transport, and assembly of bamboo furniture, making it more competitive in the market. By breaking down furniture into standardised components, manufacturers can streamline the production process, reduce labour costs, and improve quality control (Susanth et al. 2023). Implementing knockdown joints will not only enhance the structural integrity of the furniture but also make it easier for consumers to transport and assemble their purchases. This flexibility can attract a broader customer base, particularly among urban dwellers who may prioritise space-saving solutions.

c. Bamboo cultivation:

i. Limited demand: Despite initiatives like the Atal Bamboo Samruddhi Yojana in Maharashtra, the farmers are still not motivated to grow bamboo and remain reluctant to cultivate bamboo due to a lack of visible demand from industry players (Gawande 2021). Moreover, even if farmers are interested in bamboo cultivation, funds allocated for bamboo cultivation under the National Bamboo Mission support only high-density bamboo plantations on wastelands suitable only for paper mills or biomass and not for any specialised end use such as construction that is highly valued by industry. However, farmers generally lack this technical knowledge along with which bamboo species best suits a particular industrial application, resulting in low-quality produce not utilised by industry.

Way forward: CSOs can disseminate useful technical knowledge regarding bamboo cultivation in a comprehensible manner to motivate formation of bamboo-based FPOs. CSOs can then help in linking these FPOs with industry players through long-term assured buy back contracts to facilitate transparent interactions between producers and bamboo-based product manufacturers.

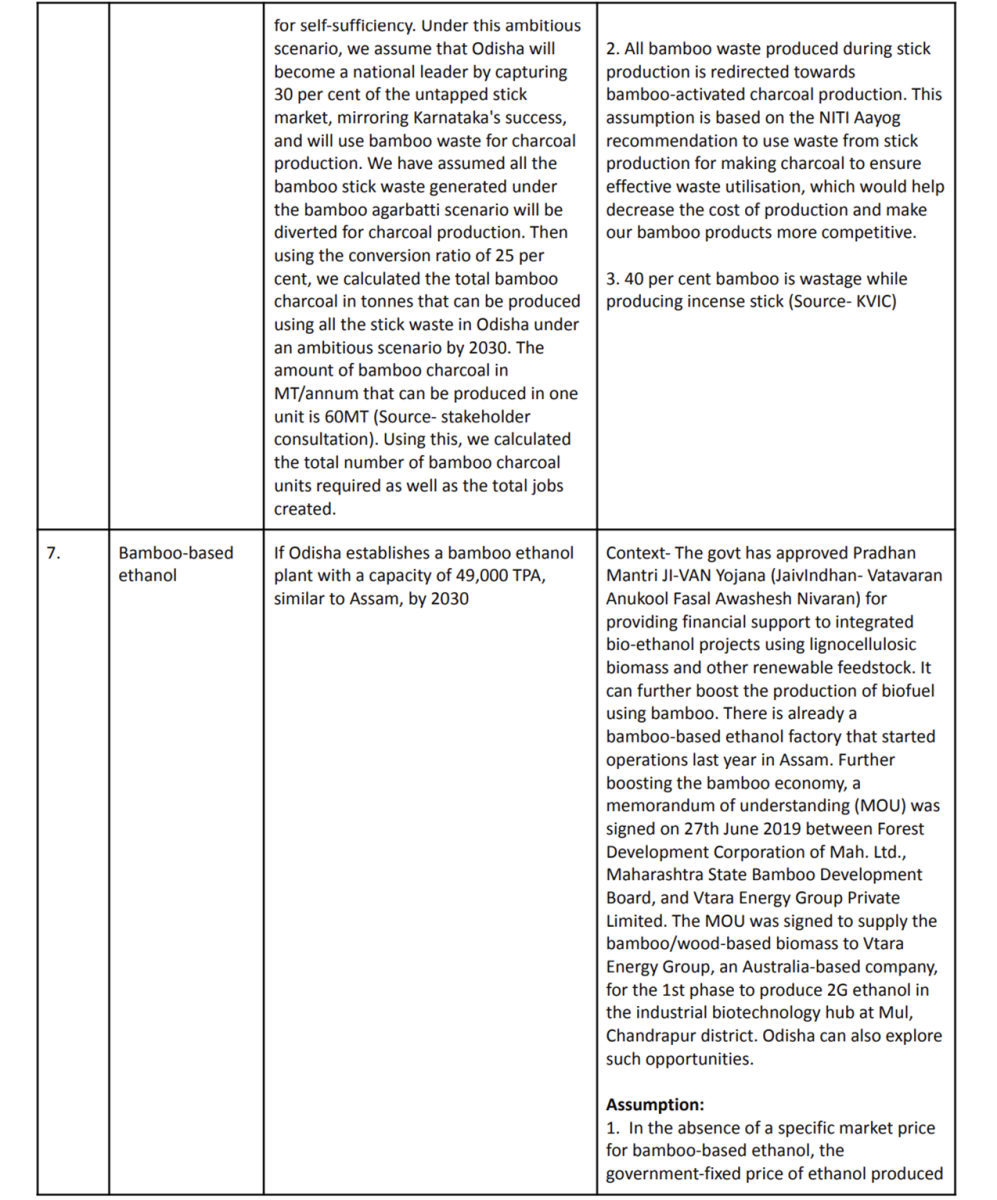

d. Bamboo-based ethanol:

i. Increased production cost due to pretreatment steps: Bamboo requires additional pretreatment steps before it can be used as a feedstock for biofuel production due to its high lignocellulose content. This increases production costs and reduces the economic feasibility of bamboo based biofuel (Liang et al. 2023).

Way forward: Biofuel producers should use post-production bamboo waste generated by other sectors, such as agarbatti and furniture, for biofuel generation as it is already pretreated (NRL 2020-21) to reduce operational costs.

Risk-proofing the scale-up of bamboo-based products

1. Environmental risks associated with scaling up the bamboo value chain include:

a. Harmful chemical use: Harmful chemicals, such as Copper chrome boron (CCB) 16 , are used during secondary processing to extend the shelf life of bamboo, which can have adverse effects on biodiversity.

Mitigation: To promote sustainability within the bamboo value chain, we need to transition to eco-friendly alternatives such as water leaching treatment and smoke treatment and use botanical extracts such as neem oil (Kaur et al. 2016).

b. Large-scale monoculture: The widespread adoption of large-scale bamboo monoculture raises social and environmental concerns such as habitat destruction, loss of biodiversity, and soil degradation (Bowyer 2014).

Mitigation: The state should promote bamboo cultivation primarily via mixed cropping, intercropping, or agroforestry settings.

c. Risks associated with cultivable wasteland utilisation: Utilising cultivable wasteland for bamboo cultivation poses ecological risks due to unclear classification of wastelands and lack of understanding about their ecological importance.

Mitigation: Wastelands may support unique ecosystems and serve as habitats for various species, including endangered grassland birds. Additionally, these areas might provide ecosystem services such as soil stabilisation and water regulation. Therefore, repurposing such areas for bamboo cultivation requires thorough ecological assessments to mitigate potential adverse impacts on biodiversity and other environmental functions (Kar et al. 2024).

d. Increased emissions: Processing bamboo stick waste to produce activated charcoal can lead to more emissions if not done in a controlled manner.

Mitigation: To prevent this, charcoal units must follow strict regulations and ensure that the Odisha State Pollution Control Board (OSPCB) regularly monitors these units.

2. Diverting land for bamboo cultivation to satisfy energy needs: While bamboo has significant potential as a renewable energy source (bamboo- based ethanol), focusing solely on energy production could lead to the diversion of valuable land that could otherwise be used for more critical purposes, such as food security and the production of sustainable materials.

Mitigation: It is important to prioritise food, feed, and material applications of bamboo over energy usage, as this aligns with bioeconomy principles (Stegmann, Londo and Junginger 2020). This approach ensures that bamboo contributes to food security, provides raw materials for various industries, and supports rural livelihoods while balancing energy needs with sustainable land use.

The bamboo value chain includes several key segments:

Raising bamboo plantations.

Harvesting and primary processing of bamboo

Transporting and directing harvested bamboo to industries utilising it as raw material

Secondary processing of bamboo to create intermediate products

Utilising intermediate products to manufacture finished products

Distributing finished bamboo products to end consumers

For the scope of this study, we have limited the analysis to the direct employment generated from bamboo cultivation, harvesting, and the production of finished bamboo products. Jobs created in marketing, sales, and distribution of harvested bamboo to bamboo-based industries or finished bamboo products to end-users have not been included.

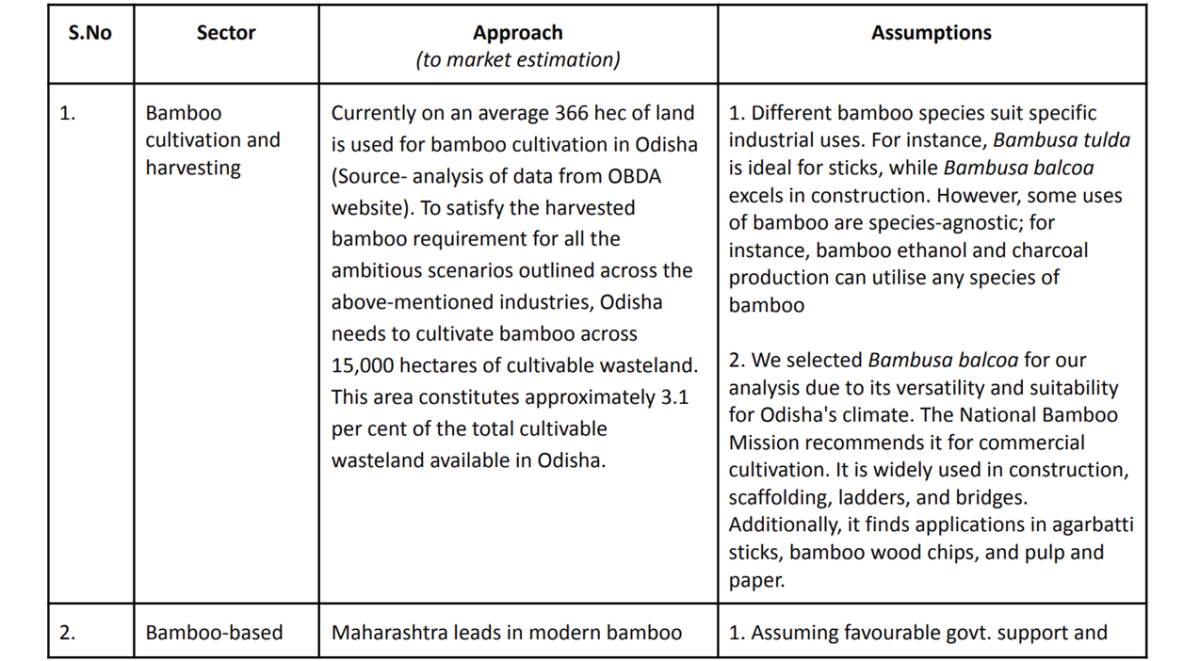

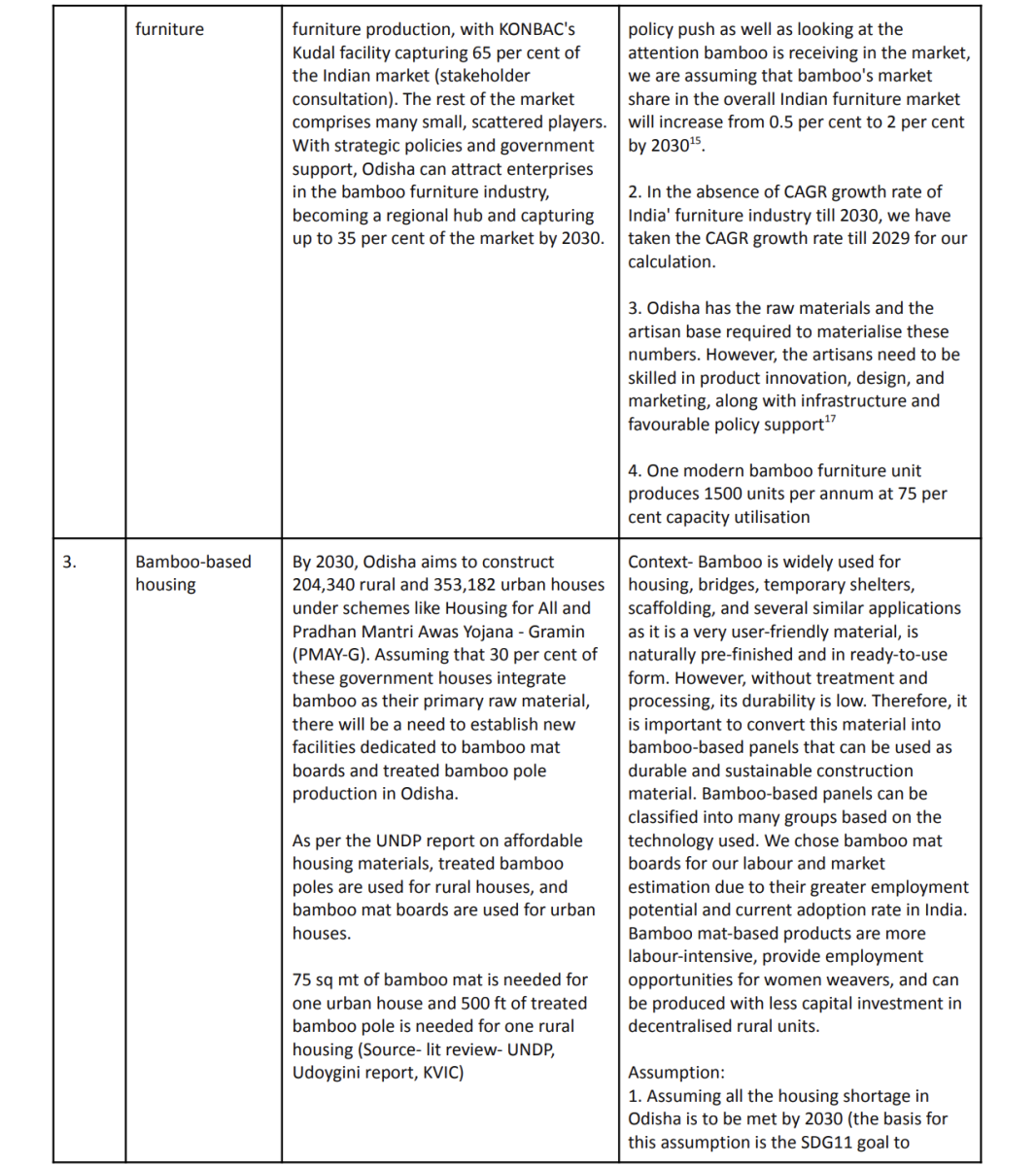

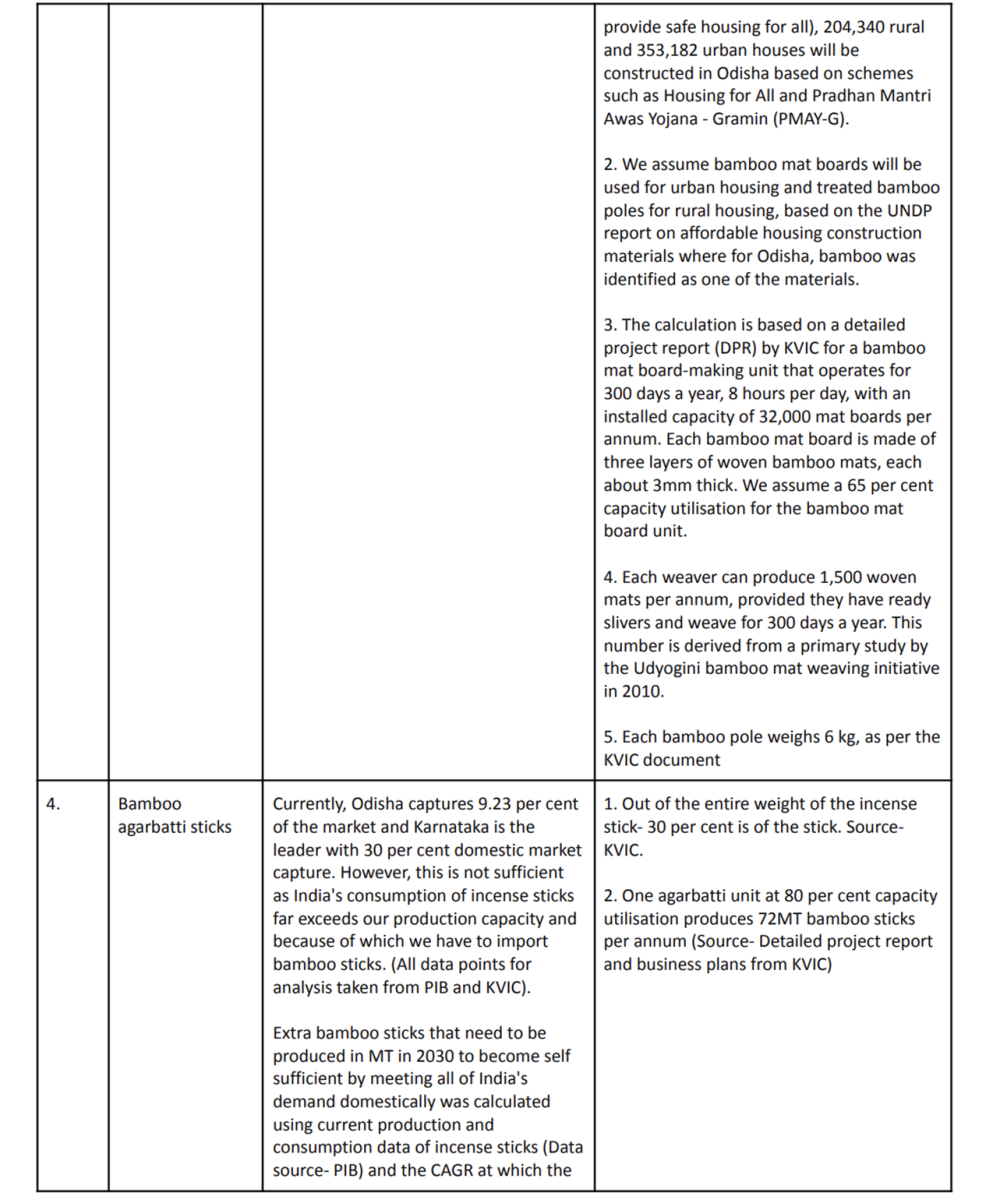

We estimated the future demand for select bamboo-based industries in Odisha for 2030. Using this demand mapping, we calculated the total annual bamboo requirement as raw material for these industries. Based on the raw materials required for select bamboo-based industries in 2030, we identified the cultivation area needed to meet the projected demand in Odisha by 2030.

Market sizing (in units):

1. To identify potential markets for Odisha's bamboo, we developed a qualitative framework informed by stakeholder consultations. This framework prioritises markets based on key factors such as scalability, availability of suitable bamboo species, existing market conditions, supply chain challenges, and alignment with national objectives. By leveraging industry insights and secondary literature review, the framework pinpoints markets with the highest growth potential in Odisha by 2030. It is important to clarify that the exclusion of certain markets does not imply a lack of future opportunities, but rather a focus on near-term scalability and alignment with policy goals.

2. Our analysis, supported by secondary research and stakeholder consultations, identified the following potential markets for bamboo in Odisha: activated charcoal, ethanol, sticks, furniture, construction (housing), and packaging. These markets were selected for their strong scaling potential due to the availability of suitable bamboo species and their alignment with emerging demand trends and national policy priorities. By concentrating on these promising sectors, we aim to maximise Odisha's economic returns from the bamboo industry by 2030.

We excluded bamboo for paper and handicrafts from this analysis. The paper industry has largely shifted to using agroforestry species, and current policy frameworks do not strongly support bamboo as a raw material for paper production. Similarly, the bamboo handicraft sector, while important, faces limitations in scalability, making it less suitable for large-scale commercialisation.

Bamboo pellets were also excluded from our analysis. Our methodology prioritised value chain activities with significant job creation potential. Odisha can meet its biomass pellet requirements for the 7 per cent co-firing mandate by 2030 using agricultural residues. This approach avoids diverting land from bamboo cultivation to energy production and adheres to bioeconomy principles that prioritise food and material needs over energy production.

Market sizing (in units):

● Step 1: Define your market based on your set parameters and scoping principles.

● Step 2: Identify potential market: Identify all possible markets for your product/service, then select a target market.

● Step 3: Deciding on the unit: Decide on the type of unit that will be considered for the estimation. The type of unit considered will vary depending on the value chain and market considered for the estimation.

● Step 4: Calculating the total number of units to be considered based on the scenario considered.

Table 1: Approach to estimate market potential (in units) of bamboo-based products is as follows:

Key informant interviews (KIIs) were conducted with nine players working in the bamboo value chain based on purposive and convenience sampling to capture the number of people employed in that facility, average capacity utilisation, production capacity, etc.

We also derived full-time equivalent (FTE) figures from secondary literature, including detailed project reports (DPRs) for some sub-value chains, such as bamboo agarbatti and bamboo ethanol. We further validated these DPRs through stakeholder consultations wherever possible.

To calculate the FTE/job multiplier, the total number of working days considered per annum was based on the average number of working days in the industry gathered through KIIs.

The formula used to calculate FTE for bamboo product-based VCs:

FTE/annum unit = Total number of people employed in a facility on a full time basis19 / annual capacity of bamboo production facility (MT/annum)

a. In cases like bamboo cultivation, where job tenure is five years or less, we calculate job multipliers using the formula mentioned above. These job multipliers are referred to as ‘Job years’. To convert them into FTE, we divide the total job years by five20

Total jobs21 = FTE/per MT of product X market potential (total product produced in MT in 2030)

Table 2: The sector-wise FTE considered are as follows:

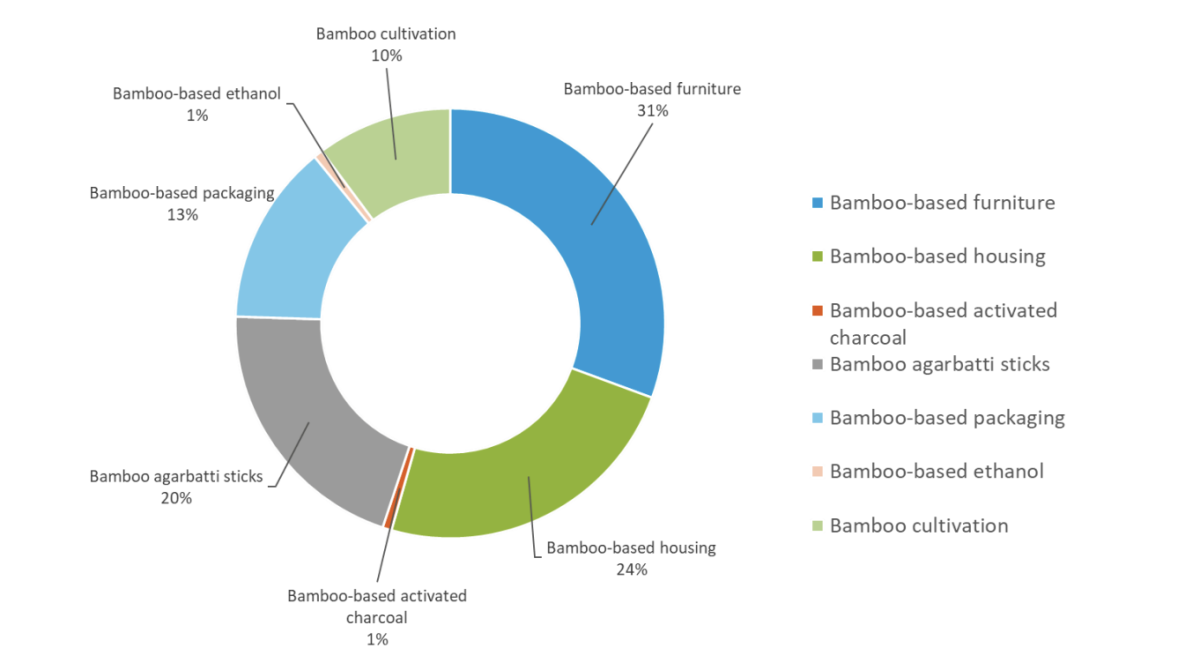

Figure 1: Sector-wise division of jobs

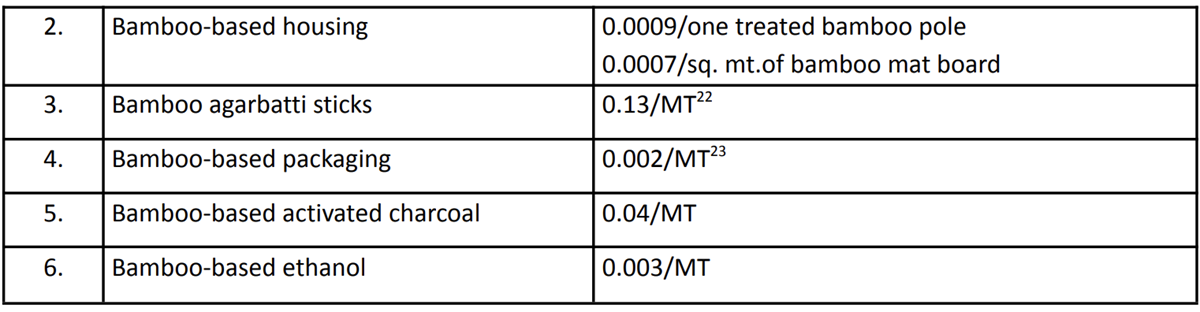

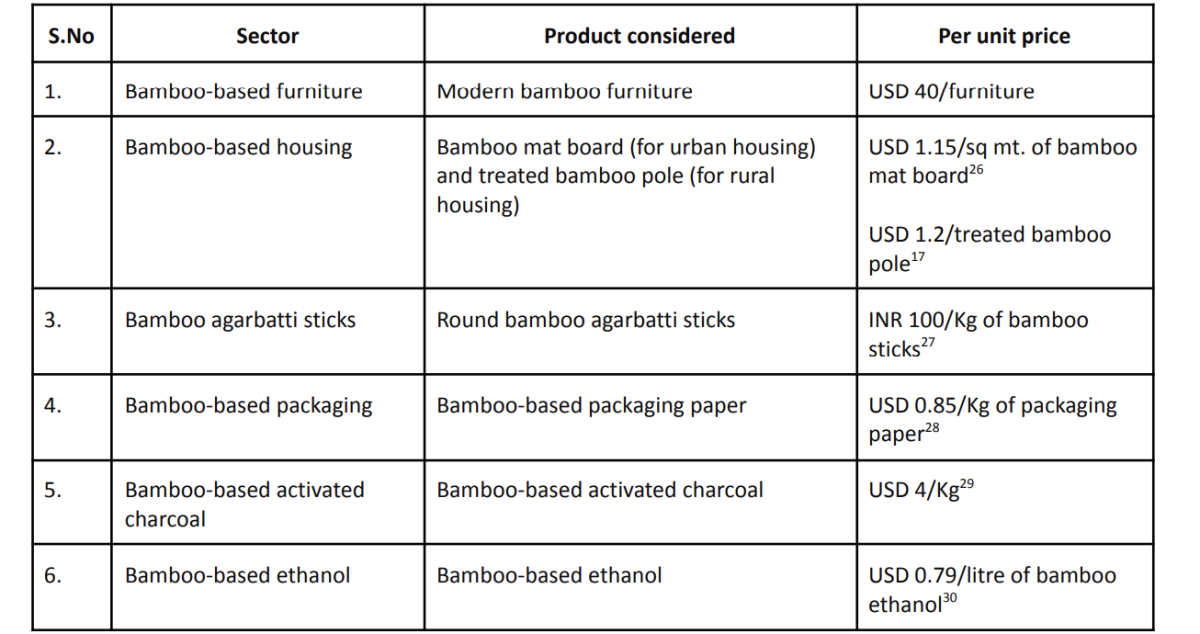

Market opportunity (in value) estimation

To estimate the potential market opportunity for bamboo-based products in Odisha, we multiplied the total number of products required in 2030 for each sector by the sale rate of bamboo products at B2B24 either through stakeholder consultations or through rates mentioned on third party sites such as IndiaMART.

Table 3: The sector-wise per unit prices of bamboo-based products25 are as follow

![]()

We calculated the total investment needed to realise the projected market opportunity by focusing solely on capital expenditure (CAPEX). When determining the number of units or facilities required to meet 2030 demand, we rounded up any decimal values.

The total investment opportunity was calculated using the following formula:

Total Investment opportunity = (Total number of units required to be set up by 2030) X (CAPEX required to set up one unit)

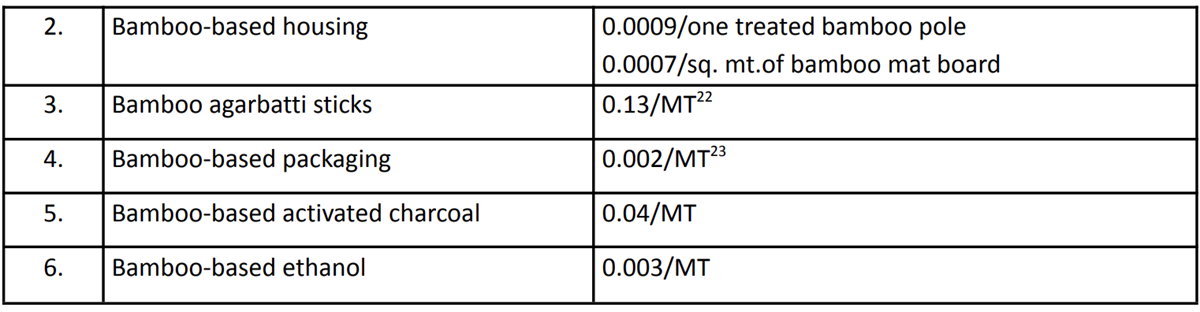

Table 4: The sector-wise CAPEX considered are as follows:

References

Mathur, Jatin. 2023. “The Bamboo Puzzle: Why India imports despite abundance?.” National economic forum, October 16, 2023. https://nationaleconomicforum.in/research/f/the-bamboo-puzzle-why-india-imports-despite-abund ance#:~:text=India%2C%20despite%20having%20the%20world's,in%202021%20%5BINBAR%202021 %5D.