Paper

Money Talks?

Risks and Responses in India’s Solar Sector

Kanika Chawla

June 2016 | Sustainable Finance

Suggested citation:Chawla, Kanika. 2016. Money Talks? - Risks and Responses in India’s Solar Sector. New Delhi: Council on Energy, Environment and Water.

Overview

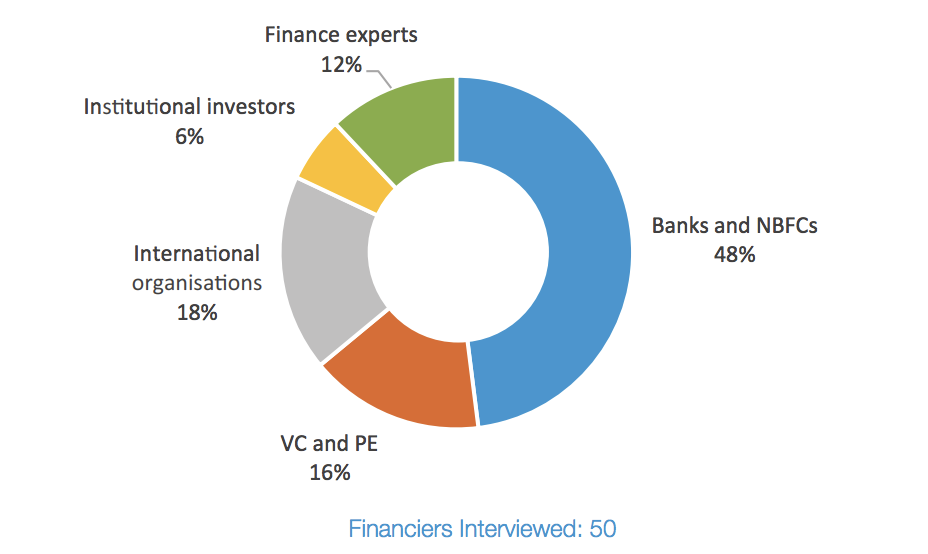

This working paper examines the risk prevalent in solar finance market. The analysis is based on the responses of 50 financiers, who have either contributed or evaluated proposals to contribute debt or equity to solar power projects in India. It captures the various impediments that financiers perceive and how financial flows react to each of these risk variables. Further, it provides risk mitigation and new sources of finance supply in the industry.

The government estimated an investment of USD 92 billion, which would be required to reach the 100 GW solar target. However, the availability of finance for solar projects has not kept pace with the optimistic commitment being made by government and developers.

Key highlights

- The total investment requirements to meet the 100 GW would range between USD 120 billion and USD 147 billion, including costs of projects, metering infrastructure and gas-based back-up.

- Public sector banks have committed USD 10 billion to solar power projects over the next six years, with additional commitments being made by private banks such as YES Bank and ICICI Bank.

- The debt from banks and Non-Banking Finance Companies (NBFCs) is mostly constrained by off-taker risk, followed by technology risk, construction and regulatory risks in the form of clearances, land acquisition, and rule of law, raising the risk profile of solar projects.

- The debt from international organisations is constrained by off-taker risk, foreign exchange risk and construction and regulatory risk. Equity from international organisations is highly sensitive to technology risk associated with a solar project.

- The risks that are likely to plague equity investors are technology risks, offtaker risk, foreign exchange risk and construction and regulatory risks. Equity investors are especially affected by policy uncertainty and project delays, which have been categorised as regulatory risks.

- Institutional investment is not being directed towards solar as institutional investors prefer low risk projects, with high credit ratings.

Composition of Financiers Interviewed

Source: Author's analysis

- Nearly 75 per cent of the bankers interviewed expressed concern over the delays in projects due to policy paralysis plaguing clearances and land acquisition.

- Nearly 67 per cent of respondents suggested that private equity from foreign investors or lack of familiarity with the project developer, especially in the case of first-time developers, raised the risk profile of solar projects.

- Government policies such as single window clearances for solar projects in some states, such as Andhra Pradesh and Tamil Nadu, and the setting up of solar energy zones and solar parks, reduce the construction and regulatory risk significantly.

- A total of 33 solar parks have been approved across 21 states in India, with a total sanctioned budget of USD 57.5 million.

- The proposed green corridor project would provide a dedicated transmission network for renewable energy, connecting solar parks around the country and mitigate infrastructural challenges.

- Foreign financing is often affected by currency fluctuations.

- Debt financing in India faces challenges such as inferior terms of debt from bank loans and the lack of a robust bond market.

- The regulatory constraints include the RBI stipulating a loan ceiling of USD 2.3 million per borrower for purposes like solar based generation.

Key recommendations

- Create a model agreement for Infrastructure Debt Funds (IDF) and NBFC, which include government guarantees for off-taker risks and robust termination procedure for solar projects. This could attract large sums of institutional finance, into operational solar projects.

- Set-up a credit enhancement mechanism which could be managed through international organisations, leveraging their high credit rating to lower risk premium on select solar projects.

- Reduce risks by financing through green bonds, which could fill some of financial gaps and mobilise large quantities of finance at lower interest rates often for longer tenures than bank loans. A green bank is another supply enhancing mechanism that can be used.

- Restructure the debt of utilities and improve their efficiency.

- Leverage the role of international finance, as it plays a critical role in India’s renewable energy deployment.

- Use innovative instruments to mobilise finance from sources that have not yet been explored or tapped at scale, in line with the investments needed to reach 100 GW of installed solar capacity by 2022.

Certification and standardisation of solar technology could bring down the cost of due diligence required to be done by the lenders. Currently, certification of solar PV modules is not mandatory. The high cost of testing and certification, ranging between USD 38,500 – 41,500 per project47, deters developers from getting certified despite the benefits.