Council on Energy, Environment and Water Integrated | International | Independent

Context: India’s clean energy, electronics, and defence sectors rely heavily on rare earth permanent magnets. With global processing dominated by China, this reliance creates strategic supply risks.

Challenge: Long project timelines, volatile prices, technology risks, and weak demand visibility make rare earth manufacturing a difficult prospect for private capital to finance independently.

CEEW’s recommendation: Targeted public finance, risk-sharing mechanisms, and international partnerships can help India build resilient, competitive non-Chinese supply chains.

Since 2025, the United States has been deploying a strategic critical mineral security policy that posits the government as a crucial player in shaping market forces. Using a mix of public finance, diplomatic coordination, and regulatory acceleration, it has deliberately sought to amend market structures rather than simply subsidising suppliers. This new approach was most clearly implemented in a landmark agreement between the US Department of Defence (DoD) and MP Materials in July 2025. The deal has put forth a template for more interventionist industrial policies, paving the way for subsequent agreements in sectors vital to both economic and energy security, such as chipmaking, steel, and nuclear energy.

India, too, has begun taking additional steps to ensure critical mineral security. The Union Budget 2026–27 announced dedicated rare earth corridors in mineral-rich states, and customs duty exemptions for equipment used in the processing of critical minerals. To scale domestic production, the government also launched a sales-linked incentive and capital subsidy scheme for rare earth magnet manufacturing. Backed by an outlay of INR 7,280 crore, the scheme will reduce upfront investment costs and provide subsidies linked to sales performance. But to reap the full rewards of these strategic decisions, India needs to reckon with the structural problems of its critical minerals market, while remaining a competitive market actor.

This is the first of a two-part series examining how strategic public investment can address market failures and catalyse clean energy and critical mineral value chains. Part one examines how supply-chain linkages and new industrial policy tools can help build domestic resilience. Part two will discuss how international partnerships can support more resilient supply chains.

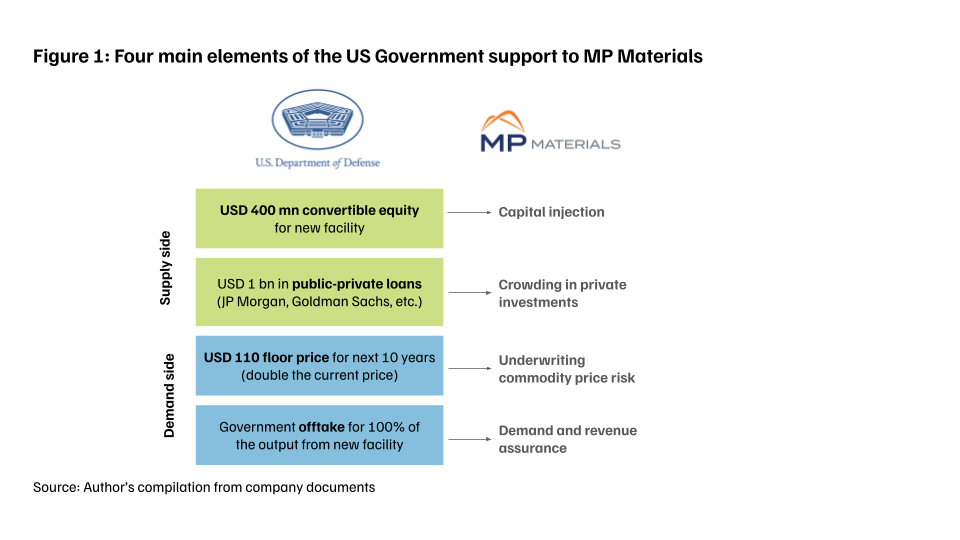

The agreement between the US DoD and MP Materials shows how the DoD is exercising greater market intervention and absorbing any price, demand, and technology risks. MP Materials mines and processes rare earth minerals, primarily Neodymium (Nd) and Praseodymium (Pr), which are used for making rare earth permanent magnets (NdPr magnets).

To implement this strategy, the US is using both demand- and supply-side tools (Figure 1). Firstly, the DoD is investing USD 400 million in a new facility for the company, scheduled to be commissioned in 2028. As part of the company’s ‘10X’ expansion project, DoD’s investments will add 7,000 metric tonnes (MT) to MP Materials’ current production capacity of 1,000 MT, along with another 2,000 MT to be added independently by the company. Secondly, the DoD has committed to purchasing the entire output from the same facility. The agreement also includes a decade-long price guarantee set at nearly double the market price at the time of the deal. Essentially, the DoD compensates the company when prices fall below the floor, and receives 30 per cent of revenues above the floor during high-price periods, thereby sharing upside gains while protecting against losses. Lastly, by stabilising revenues and signalling long-term policy support, such guarantees attract private capital, as seen by the subsequent investment and rare earth permanent magnet purchase commitment with MP Materials from Apple.

Folowing the MP materials agreement, several more ‘America-first’ deals have been set on a similar template. Across the rare earth mineral value chain, the US administration has offered support to various firms. To support the exploration and development of critical minerals, the administration has preemptively acquired 10 per cent equity stakes in Trilogy Metals, a company that is yet to start the permitting process for its most advanced projects. For the expedited refining and processing of critical minerals, ReElement Technologies has received loan guarantees and deferred equity shares as state support. Companies such as Vulcan Elements, which are utilising the refined critical minerals to produce downstream components such as magnets, have also received federal support. Similarly, several other companies in the critical minerals sector, such as Ucore Rare Metals, USA Rare Earths, and Lithium Americas, have received state support via a bouquet of instruments.

In a geopolitically uncertain era, governments are increasingly investing in domestic manufacturing. Mines take nearly a decade to develop in response to rising prices, and often face high market concentration, with individual producers significantly influencing supply and price. This can disincentivise private capital from investing. Private financiers alone may lack the long-term, low-cost capital pools and the technology assessment capabilities to accurately assess risks. Hence, state investments can play a crucial role in underwriting risks. This new role of the state is not limited to critical minerals. It has also expanded into strategic sectors such as semiconductors, nuclear energy, and steel, as evidenced by its investments in companies including Intel, Westinghouse, and US Nippon Steel.

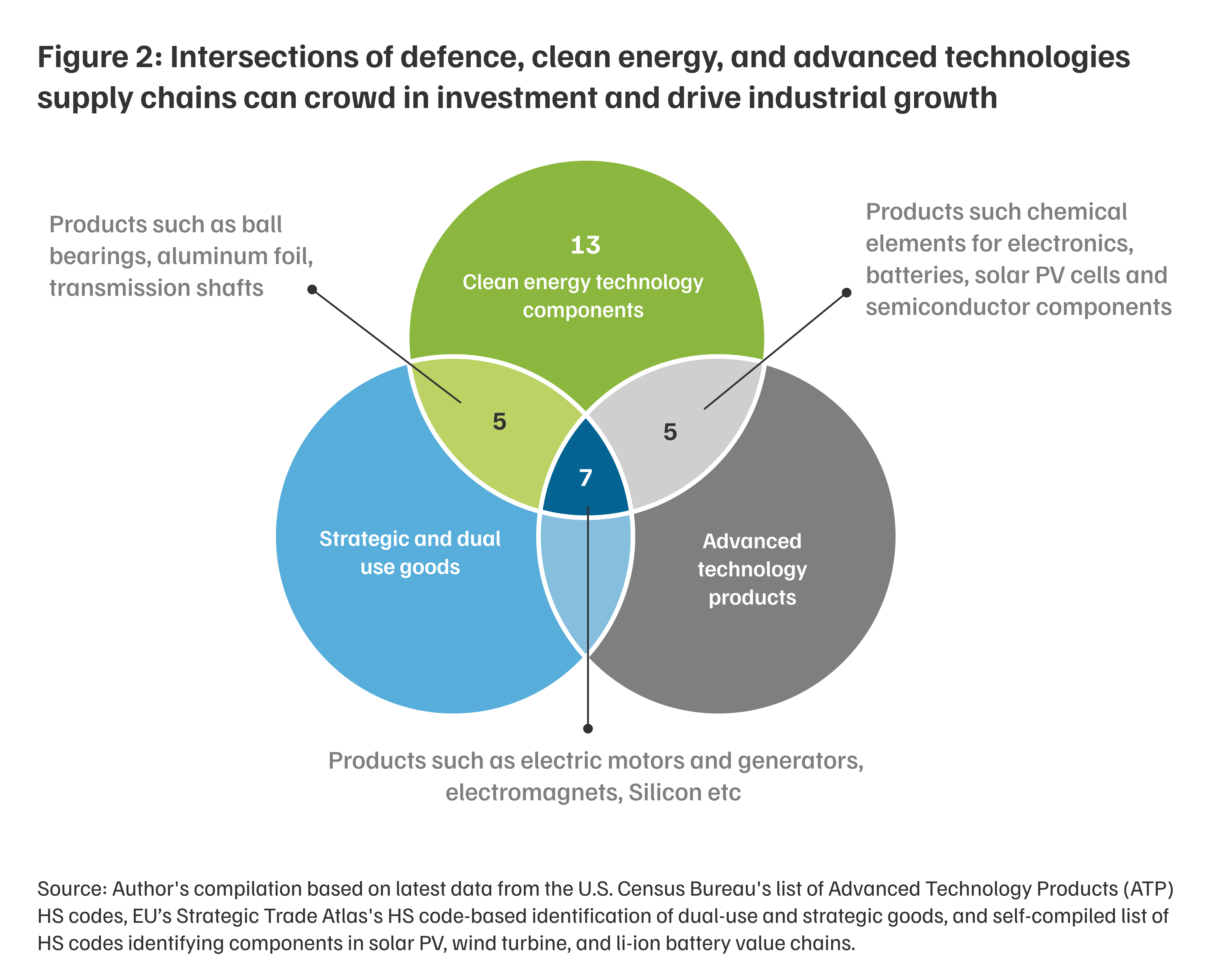

Public investment in ‘anchor’ sectors such as defence, metals, aerospace, etc., can create spillover benefits for critical mineral and clean energy value chains that share underlying materials and components. Sectors like defence are strategically prioritised, less price-sensitive, and may have higher budget allocations, allowing their linkages to play a catalytic role. For instance, while the defence sector is the immediate beneficiary of the MP materials deal, increased production of rare earth permanent magnets will also support industries such as automotives and clean energy. Clean energy supply chains comprise several components classified as ‘dual-use’ goods that can be used for both civilian and military applications. Besides defence, these value chains also share synergies with sectors such as chemicals, electronics, and digital infrastructure, and contribute to overall manufacturing sector growth (Figure 2). Missing these industrial linkages may risk foregoing a critical opportunity for India’s manufacturing-led growth aspirations.

These deals exemplify how countries with supply chains critical to economic security could start building markets without having to wait for ‘incentive prices’ that crowd in private players. However, such state-influenced measures in advanced economies could also distort global price signals and create more barriers for developing economies, constraining their mineral, energy, and technology supply chains.

While the state plays a catalytic role in absorbing market uncertainty, it is equally important to ensure that the tools of such intervention are chosen cautiously. In this changing landscape, India should explore financing mechanisms and partnerships that hedge early-stage risks in strategic sectors and are aligned with fiscal and institutional realities. Market distortions can be extremely difficult and expensive to correct; therefore, support should be fiscally bounded, transparent, and tied to clear performance benchmarks. Avoiding overreliance on firm-specific interventions, India should carefully consider new approaches while remaining a disciplined and competitive market participant. This need not be implemented in isolation. India can deepen coordination with like-minded partners to achieve comparable scale in production and demand as it continues to strengthen manufacturing capabilities at home.

The focus on market failures, however, should not overshadow the technical complexities that underpin many challenges in these sectors. Commercial de-risking must be complemented with broader measures that address underlying bottlenecks. Even with funding and offtake guarantees, projects remain exposed to execution risks from facility build-out delays, permitting hurdles, technology risk in new extraction, refining and processing technologies, and demand uncertainty in downstream markets. Complementary measures supporting processing and recycling pilots, establishing public–private R&D accelerators, and streamlining regulatory approvals can lower additional risks and strengthen supply chains. These measures will be essential to secure competitiveness in the long run.

India need not copy the US policy playbook, but it must realise that public capital and targeted guarantees can build confidence in emerging sectors that may otherwise struggle to flourish independently. Given the overlapping nature of these supply chains, deliberately seeding industrial capacity in clusters with strong technological and application spillovers can build a highly resilient domestic economy. Fostering technology leadership and building dynamic ecosystems that will define competitiveness in the coming decades will be decisive in positioning India as a critical node in the emerging non-Chinese supply chains.

Shruti Gauba is a Research Analyst at the Council on Energy, Environment and Water (CEEW). Send your comments to [email protected].

Add new comment