Council on Energy, Environment and Water Integrated | International | Independent

Northvolt, a Swedish battery manufacturer, once captivated global attention with its mission to produce batteries with a 90 per cent lower carbon footprint. Empowered by a strategy based on cleaner processes and strategic independence in energy storage, the company seemed poised to revolutionise the European battery industry. The same ambitions, which once received much optimism and praise, now invite scrutiny following the company’s bankruptcy filing. Critics have pointed to safety issues, operational inefficiencies, cell chemistries, and logistical hurdles like language barriers and factory locations. How did these cracks form, and what can emerging battery manufacturers learn from this cautionary tale? With the energy transition relying on the competitiveness of clean-tech manufacturing, drawing lessons in building resilient and scalable solutions is imperative at this juncture.

In November 2024, Northvolt filed for Chapter 11 bankruptcy in pursuit of a strategic realignment, with only 30 million USD of available cash and 5.8 billion USD in debt. Chapter 11 procedures allow management to maintain control and reset their financial trajectory during the restructuring. Historical examples like General Motors and American Airlines have shown the potential for recovery through restructuring after bankruptcy. For Northvolt, this process could lower its capital cost, eliminate significant debt, and provide a second chance. For policymakers and emerging manufacturers, this points to the complexities of scaling green technologies, highlighting the need to solve both ecosystem issues and operational challenges. Northvolt’s trial-and-error offers three crucial insights, not just for itself but for other emerging players, especially in markets like India, that are seeking to build a sustainable and competitive battery manufacturing ecosystem.

First-of-a-kind projects can include multiple unknowns, stemming from not just innovative technology, but also new business models, unique manufacturing processes, new skills, uncertain reliability of counterparties and technology adoption levels. In the climate-tech sector, such first-time projects can be both capital-intensive and highly risky. In such scenarios, offtake agreements — commitments from buyers to purchase a product — become a cornerstone of the financial strategy, as they validate market demand and instill confidence in investors. In India, for instance, Amara Raja has signed an MoU with manufacturer Ather for supplying electric vehicle (EV) batteries that will be manufactured in their Telangana plant.

The battery market in Europe and North America is driven by EVs, therefore Northvolt focused on manufacturing EV batteries. In EV production, batteries can comprise the single largest cost component. Hence, there is also an incentive for automakers to secure long-term battery procurement deals at agreed-upon prices. Northvolt’s offtake agreements, as well as investments, were closely tied to the burgeoning electric vehicle industry, with automakers like BMW, Scania, and Volkswagen as key clients and investors. As per Northvolt’s latest annual report, their largest shareholder Volkswagen holds a 21 per cent stake in the business. Ultimately, Northvolt’s capital and business strategy was banking on the continued growth of the EV market.

Given both businesses' nascent and interdependent nature, market fluctuations in one can quickly and significantly ripple through the other. Hence, one of the most significant blows for Northvolt came through BMW’s termination of a EUR 2 billion supply contract in June 2024 — citing quality and delivery issues — eliminating an important revenue stream and shaking investor confidence. Compounded by a slowdown in European EV sales, Northvolt’s challenges mirror those faced by peers like Umicore and BASF.

Since its genesis in 2017, Northvolt quickly began attracting funds. Before the flagship Northvolt Ett factory – 'ett' being Swedish for "one” – had even manufactured its first cell in 2021, the company secured multi-billion-euro pre-production contracts with BMW and Volkswagen, alongside raising additional capital that included a USD 1.6 billion debt round and a USD 600 million equity round. According to its latest 2023 annual reports and bankruptcy fillings, Northvolt had received investments totalling EUR 15 billion (16 billion USD) — through a mix of debt, equity, and grants — making it one of Europe’s best-funded startups. Northvolt presents a curious case of a business that had no trouble attracting money but ended up in a liquidity crisis shortly after.

To attract financiers and carve a niche in a highly competitive industry, new entrants may announce ambitious, large-scale plans with aggressive timelines, walking a precarious line between ambition and practicality. This is due to the high-risk nature of first-time projects that can make securing debt capital particularly challenging. Equity financing plays the main role in earlier stages, but excessive equity may risk diluting ownership, creating long-term strategic complications, and fostering growth-chasing tendencies. The battery manufacturing process roughly consists of 18 steps, and the equipment for all these steps has to be calibrated and synchronised properly to allow efficient production. Going from lab scale to commercial scale in batteries includes technical challenges such as maintaining uniformity of electrode coating and precise stacking of the jelly roll. Economies of scale are crucial in the battery business, but growth needs to be systematic. If equity-financing dynamics compel manufacturers to pursue rapid growth and overpromise in offtake agreements, then they are likely to rush through the learning curve and underdeliver later. This can quickly erode trust and long-term competitiveness.

In late 2023, the Swedish business daily Dagens Industri revealed Northvolt’s third-quarter results, showing that they had delivered only 79.8 MWh of battery cells — lower than even 0.5 per cent of its planned 16 GWh annual capacity for 2024. This discrepancy stemmed from reported challenges such as mismatched production parameters and equipment capabilities from suppliers, unclear process engineering, and limited knowledge transfer from their equipment supplier Wuxi due to linguistic and contractual difficulties. Notably, the Chinese supplier Wuxi is amongst Northvolt’s largest unsecured creditors, highlighting how such inefficiencies became a significant impediment to Northvolt’s growth. The challenge was perhaps compounded by the practical difficulty of simultaneously scaling multiple businesses — battery chemicals, cells, recycling, and research — leading to the rapid depletion of cash reserves, far outpacing any revenue generated. Ultimately it was this rapid scaling that strained their resources.

Authors’ compilation based on Northvolt Sustainability and Annual Report 2023, Sifted, and Reuters.

Bringing a new battery to market is an arduous, multi-year journey — typically spanning 4-10 years — and can be fraught with delays, supply chain disruptions, technological bottlenecks, chemistry changes, manufacturing hurdles, fundraising struggles, and macroeconomic factors like interest rate changes. While the exact nature of these challenges may be unpredictable, their inevitability is certain. Weathering these challenges in a technology-intensive business, while also maintaining a unique selling proposition at a reasonable cost, may prove exceptionally difficult.

Northvolt's focus on Lithium-Nickel Manganese Cobalt (L-NMC-811) chemistry initially aligned with market demand, particularly the preferences of European EV manufacturers and supported by surging cobalt prices and sustainability concerns around cobalt mining. One GWh of the NMC-811 cathode contains an additional 77 tonnes of cobalt and 767 tonnes of nickel, compared to 1 GWh of Lithium Iron Phosphate (LFP) cathode. LFP has no cobalt and nickel, drastically reducing its cost and making it more sustainable than NMCs. NMC’s nickel content, on the other hand, enhances the energy density and reduces the dependency on cobalt, but it also complicates the manufacturing processes and compromises the battery stability and safety. However, since 2023, cobalt prices have been plummeting continuously, and increasing the manganese content in battery electrodes has shown improvements in their structural strength, thermal stability, and sustainability. As a result, many manufacturers are now reverting to medium-nickel chemistries such as NMC-622 and NMC-532, which can provide similar performance characteristics at a lower cost and better safety.

The cost and quantity of critical materials are significant contributors to the overall battery cost. Thus, chemistry choices and innovations have a direct impact on margins. In China, battery giants have been constantly improving the performance and safety of their LFP chemistry while maintaining low prices, expanding LFP’s application beyond grid-scale energy storage towards EVs. In response to the affordability and sustainability trends, Northvolt ventured into Sodium-Ion Batteries (SIBs) in 2023. However, SIBs are not a popular choice for use in EVs as they do not have enough energy density. Northvolt, who began with seemingly suitable chemistry, thus ended up missing an important transition in the EV space and manufacturing expensive NMCs instead.

While Northvolt offered a cleaner, localised supply chain, its battery remained fundamentally similar to those already available in the market, likely at a higher price. With the prices of lithium-ion battery packs falling 20 per cent year-on-year and reaching 115 USD/kWh in 2024, tight competition could make staying afloat difficult. As capacity ramp-up remains a significant challenge, producers may need to focus on fundamentals and unit economics before building a unique selling proposition.

Northvolt's setback reflects a convergence of issues, highlighting the need for meticulous financial planning, operational readiness, and the construction of strategic partnerships. In such a capital-intensive, complex, and nascent industry, success will mean clear coordination and collaboration across the value chain; automakers must make appropriate offtake contracts, suppliers must take risks in scaling equipment, and policymakers and domestic stakeholders must align regulatory and infrastructural support. Careful construction of this ecosystem will allow companies to de-risk their operations.

For consumers, three main parameters are still the priority concerns — performance, cost, and safety. Hence, while innovation and unique selling propositions are important, they must be grounded in immediate commercials and market realities. Northvolt’s ambitions, whether misplaced or not, may remain unachievable if risks and rewards across product design, business strategy, and financial planning are not carefully balanced. Efficient scaling and high product quality require focusing on the supply chain one step at a time and mastering the manufacturing line. For emerging gigafactories that can be vulnerable to such early-stage missteps in capacity expansion and financial structuring, new forms of offtake agreements and deal terms might be useful in alleviating growth pressures.

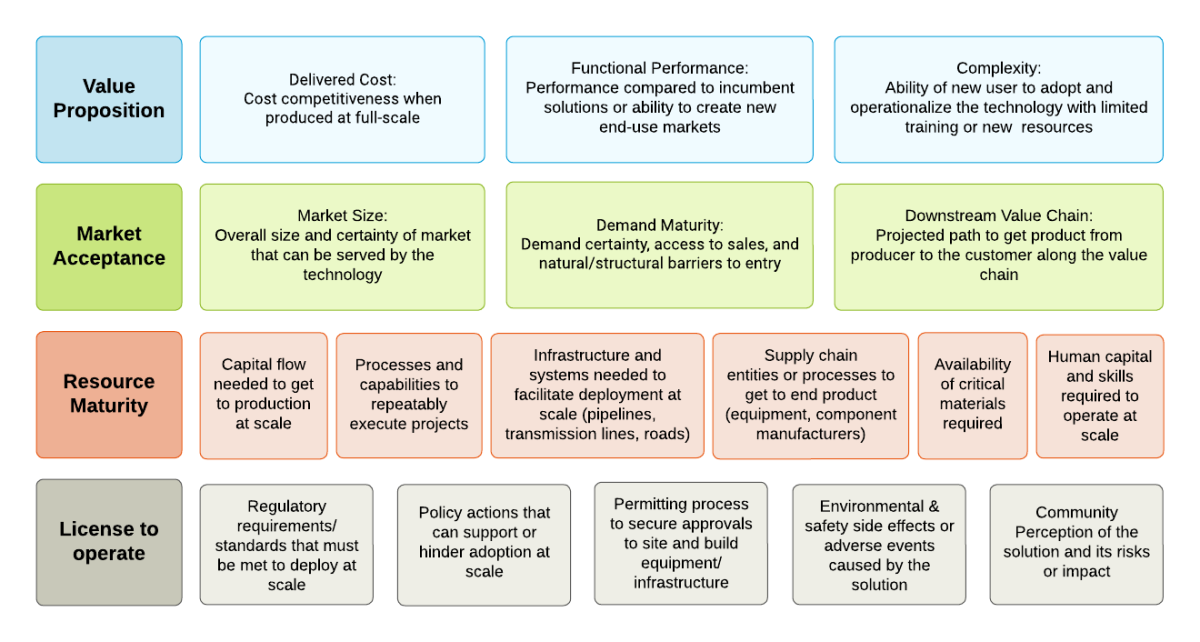

For instance, going beyond traditional one-to-one procurement deals by pooling suppliers and off-takers can protect against individual defaults at either end of the deal. Founder-friendly financing options can also be explored at early stages, such as Simple Agreements for Future Equity (SAFEs), which allow startups to raise funds without an immediate valuation. Unlike other convertibles, SAFEs convert to equity at a later date without accruing interest. However, greater risk appetite at any stage of funding must be accompanied by a keen eye for evaluating the technical potential of a solution. Hence, funds and funders of all kinds; equity, philanthropic or catalytic capital, strategics, government grants, and project Investment, will play an important role. More comprehensive evaluation frameworks can also be used for well-informed decision-making. The Commercial Adoption Readiness Assessment Tool (CARAT) prepared by the US Department of Energy — a checklist which considers factors such as supply chains, costs, regulations, and market acceptance — is a good example of the same, which complements the widely known Technology Readiness Levels.

Source: Authors’ Compilation based on National Association of State Energy Officials and Sightline Climate

Most importantly, businesses must take an active role in voicing concerns for such bottom-up risks, while governments focus on minimising systemic vulnerabilities from a top-down perspective, keeping in mind frontier technologies, encouraging mineral exploration, and addressing trade barriers. In India, several companies have submitted bids for the production of advanced chemistry cells under the central government's production-linked incentive scheme. To their advantage, many upcoming Indian manufacturers have an existing market presence in adjacent businesses such as lead-acid batteries and EV production. However, scaling the battery gigafactory dream will present new challenges, especially on the technological front.

As Northvolt’s experience makes clear, mastering cell manufacturing is not straightforward, and navigating the ladder of commercialisation will be vital for the success of India's battery industry. Northvolt’s journey, though fraught with challenges, offers invaluable lessons for those charting a similar path in cracking the code to competitiveness and driving the energy transition.

The authors express their gratitude to Akshay Singhal, Founder and CEO, Log9; Labanya Prakash Jena, Consultant, CEEW; Rohit Vedhara, Climate Tech Director, Aum Energy; Shiva Shanker, Partner, Ankur Capital; Vijayanand Samudrala, President, Amara Raja Advanced Cell Technologies; and Vishnu Rajeev, Investment Principal, Speciale Invest for their invaluable insights that helped enrich this article.

Shruti Gauba and Aanya Singh are Research Analysts at the Council on Energy, Environment and Water (CEEW). Views are personal. Send your comments to [email protected].

Add new comment