Council on Energy, Environment and Water Integrated | International | Independent

Suggested Citation: Warrior, Dhruv, Akanksha Tyagi, and Rishabh Jain. 2023. How Can India Indigenise Lithium-ion Battery Manufacturing? Formulating Strategies across the Value Chain. New Delhi: Council on Energy, Environment and Water.

Scaling and stabilising lithium-ion battery cell manufacturing in India is critical to India realising its decarbonisation goals. This issue brief deconstructs the lithium-ion battery cell manufacturing process, estimates the material and finance requirements, and offers a blueprint for a possible indigenisation strategy. A significant portion of the rapidly growing battery demand projected between 2021-2022 and 2029-30 from India’s power and mobility sector can be met by domestic battery manufacturing. This study finds that enabling such a large-scale buildout will require mobilisation of significant capital and securing of battery components and electrode materials to supply the industry.

Developing indigenous upstream and midstream capacity in lithium-ion battery supply chains were identified as avenues for significant additional value capture. The study concludes that India will need to focus on innovation, ecosystem building and securing cathode mineral supplies to secure this nascent industry.

Energy storage technologies are expected to play a critical role in the decarbonisation of the electricity and transport sectors, which account for 49 per cent of India’s total greenhouse gas emissions (CO2 equivalent) as of 2016 (MoEFCC 2021). Among the several technologies available for energy storage, lithium-ion-based batteries are expected to dominate the sector in this decade (IEA 2021). With nearly non-existent infrastructure across the supply chain and limited deployment experience, it is crucial for India to gain more control over the supply chain of lithium-ion batteries. Given the complexity of the global supply chain, scaling up and stabilising battery cell manufacturing is critical to India realising its decarbonisation goals. In this issue brief, we deconstruct the lithium-ion battery cell manufacturing process, estimate the material and finance requirements, and offer a blueprint for a possible indigenisation strategy.

The cumulative storage demand will vary significantly based on the trajectory of the country’s transport and power sectors. For this study, we estimate the demand for utility-scale storage based on the recently announced energy storage obligation by the Ministry of Power (MoP 2022). The notification recommends stored renewable energy comprise 4 per cent of total consumption by 2030. Our analysis suggests that this would translate to approximately 327 GWh of storage capacity by 2030 (CEA 2022).

The remaining demand (576 GWh) from electric vehicles (EVs) is estimated based on a 2020 study by the Council on Energy, Environment and Water (CEEW), which estimates the stock of EVs in India in 2030 under the EV30@30 scenario (Soman, et al. 2020).

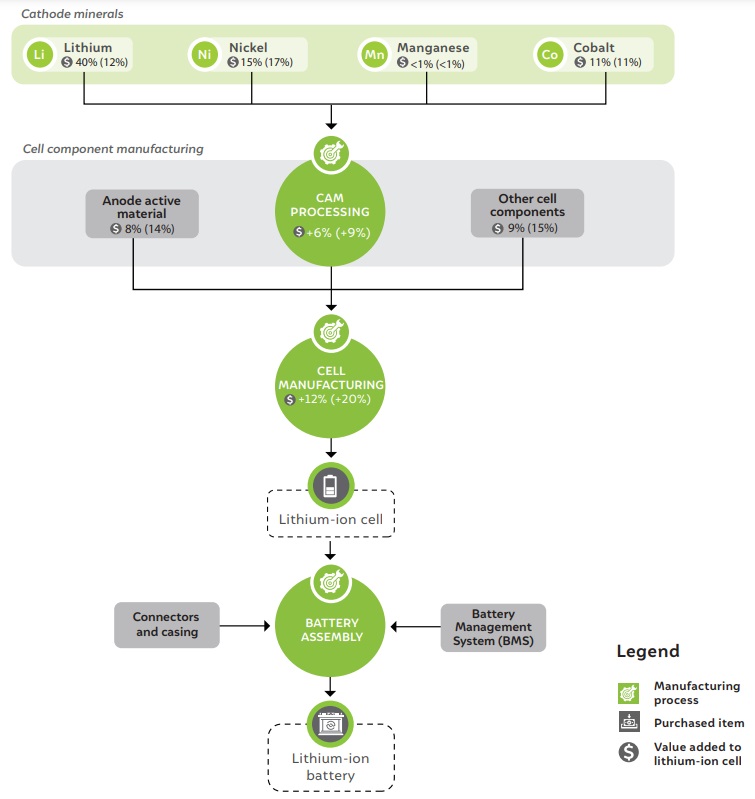

Figure ES1 shows the various stages and value addition possible in the value chain for lithium nickel manganese cobalt (Li-NMC) batteries. Although the current focus of Indian companies is on battery cell manufacturing, the upstream process will likely be the next focus area as more cell manufacturing plants are commissioned in India. These industries include graphite anode production and cathode active material production as well as electrolyte, separator, and current collector manufacturing.

Among these, active cathode material production is most critical. The market prices of the minerals that go into the battery cathode are highly volatile. As commodity prices fluctuate, so will the actual cost of batteries based on their chemistry. Further, securing reliable access to minerals is a new challenge. Given India’s low natural endowment of most lithium-ion battery minerals, between 12–60 per cent of the value chain is subject to imports.

In our analysis, we assume that new battery manufacturing facilities have a minimum capacity of 5 GWh. The total cost, including land acquisition, factory floor space, warehousing, and connecting utilities, could lie between USD 325–450 million (INR 2437–3375 crore1 ) for each 5 GWh facility. Furthermore, these factories will be energy intensive, with a 5 GWh production facility consuming about 250 GWh (250 MU) annually.

We use three scenarios with varying degrees of indigenisation and technology mixes to estimate India’s active electrode (cathode and anode) and electrolyte requirement to meet the energy storage demand of 903 GWh by batteries (Table ES1).

Figure ES 1 Lithium nickel manganese cobalt (Li-NMC-622) chemistry value chain

Source: Author’s analysis, Argonne National Laboratory 2020, Shanghai Metals Market (SMM n.d.), CellEst 2019

Note: The value added to the finished LIB cell at each stage of the value chain is provided for June 2022 and June 2021 (in brackets). CAM processing value add includes value added during precursor CAM processing. For components other than CAM, the value of the consumable to the manufacturer have been provided as their value share. Other cell components refer to: separator [VA - 3%(6%)], aluminium current collector [VA - <1%(<1%)], copper current collector [VA - 2%(4%)], electrolyte [VA - 2%(4%)]; cell casing value not considered in analysis. Values may not add up to 100% due to rounding. CAM: cathode active material.

Table ES 1 The scenarios developed for active electrode material and electrolyte demand estimation

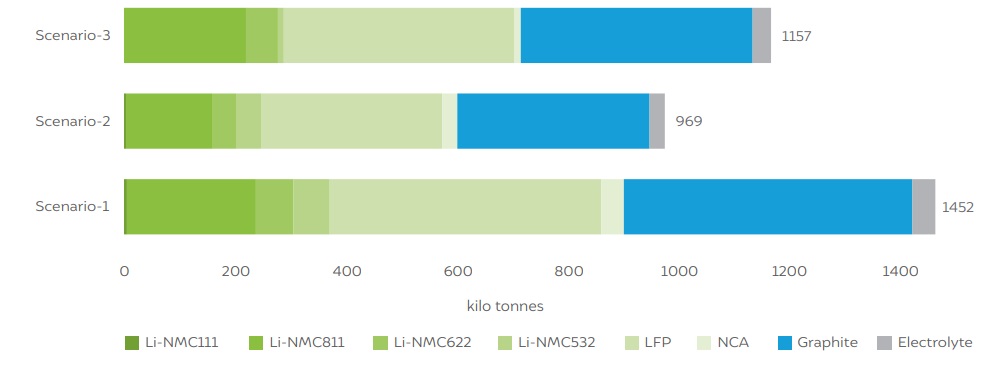

As Figure ES2 shows, demand is highest in Scenario 1 (1452 kt); it is characterised by high indigenisation (60 per cent of the cumulative demand) and the market is largely dominated by lithium-ion-based chemistries.

Meanwhile, Scenario 3 – with the same level of indigenisation but other emerging technologies, like redox flow and solid-state batteries – features less demand for active materials and electrolytes (1157 kt).

Figure ES 2 Cumulative active material requirement (kilo tonnes, kt) for India’s storage ambitions under different scenarios (2022-2030)

Note: Li-NMC — Lithium nickel manganese cobalt; LFP— lithium ferro phosphate; NCA—nickel cobalt aluminium

Source: Author’s analysis

As per the third Biennial Update Report (BUR) that India submitted to the United Nations Framework Convention on Climate Change (UNFCCC), the share of the electricity and transport sectors in total CO2 emissions was nearly 49 per cent in 2016 (MoEFCC 2021). In July 2021, India’s peak demand soared to record levels of 203 GW (CEEW-CEF 2021). Going forward, it is expected that by FY2030, the peak electricity demand will increase to 334 GW and the total electricity generation requirement will be 2,229 BU (CEA 2022). Decarbonising the electricity and transport sectors hence becomes critical to combating climate change. During the COP 26 UN Climate Change Conference, India announced ambitious national targets for 2030, including building its non-fossil energy capacity to 500 GW by 2030; meeting 50 per cent of its electricity requirements from renewable energy by 2030; reducing the total projected carbon emissions by one billion tonnes, and reducing the carbon intensity of its economy by less than 45 per cent (PMO India 2021).

Designing infrastructure to meet our climate commitments along with peak and total electricity demand can be tricky for planners. Multiple factors, like technology readiness, environmental impact (cradle-to-grave), upfront investment, recurring costs, manufacturing capabilities and import dependence – such as for raw materials and final products, reuse- (and recycle-) ability, along with workforce and skillset, play important roles.

Energy storage can significantly impact how we generate electricity and how we travel. Without an energy storage system, we will need to arrange balancing assets, like thermal or gas power plants, to serve loads during hours with limited renewable energy generation. Without scaling up energy storage, the transport sector will not be able to transition to electric vehicles (EV), and the sector will continue to burn large quantities of fossil fuels. Once the required technologies mature, EVs may be able to support the grid by storing electricity and supplying it back to the grid through charging stations capable of bi-directional flow. Hence, energy storage must be looked at as strategic infrastructure, and policy reforms need to be formulated to deploy and manufacture energy storage technologies, and procure the necessary raw materials for their production.

Broadly, energy storage technologies can be classified into five categories:

• Mechanical: pumped hydro and flywheels

• Electrical: capacitors and superconductors

• Electrochemical: lead-acid and lithium-ion batteries

• Chemical: hydrogen • Thermal: molten salts

Interestingly, each storage technology has different characteristics, like energy density, charge-discharge rate, cycle life, and efficiency. Hence, we need to select the technology appropriate to each application after considering all parameters. While several of these technologies will have a place in the future grid and mobility sector, one kind of technology shows the greatest promise in driving the deployment of energy storage in the immediate future: lithium-ion batteries (LIB). Hence, in this issue brief, we focus on this incumbent technology from the lens of indigenising the value chain.

Deployment :

India has not announced any deployment targets for energy storage in the stationary or mobility sectors. Consequently, there are no consolidated estimates for the country’s energy storage requirements. A few studies put the cumulative demand from grid-related applications in the range of 108–252 GWh by 2030 ( (CEA 2020); (Abhyankar, Deorah and Phadke 2021); (WartsilaKPMG 2021)). Recently, the Ministry of Power announced Energy Storage Obligation which recommends stored renewable energy comprise 4 per cent of total consumption by 2030 (MoP 2022).

In 2019, India committed to the EV30@30 campaign (Clean Energy Ministerial 2019). Based on this target, a 2020 study by the Council on Energy, Environment and Water (CEEW) estimates the demand for batteries for EVs in 2030 to be 72–766 GWh (Soman, et al. 2020). We consider different scenarios based on the share of EVs in new vehicle sales and mode-share (high public transport, high private transport, and high shared mobility) within EVs.

So far, the mobility sector has created the maximum demand for batteries, whereas only a limited number of projects have been deployed at the grid scale. For instance, about 0.4 million EVs were sold in India in FY22 (CEEW-CEF 2022), while only two utility-scale battery projects have been deployed between FY19– FY22. Tata Power, along with AES and Mitsubishi, deployed India’s first utility-scale battery (10 MW/10 MWh) in New Delhi (Tata Power 2019). In 2020, NLC and L&T Constructions commissioned India’s first solar energy storage hybrid system (20 MWAC solar and 16 MW/8 MWh battery) in South Andaman (L&T Construction 2020). Later, BSES Rajdhani also set up a 100 kWp solar and 466 kWh battery project in Delhi (BSES 2021). Energy storage coupled renewable energy tenders are also being announced, with the SECI issuing a 1200 MW tender with a two-part tariff (peak and offpeak) and INR 2.88 (USD 0.032 )/kWh as a fixed, flat off-peak tariff (SECI 2020). ReNew Power and Greenko, two independent power producers, won 300 MW and 900 MW capacity at peak tariffs of INR 6.12 (USD 0.086)/ kWh and INR 6.85 (USD 0.096)/kWh, respectively (CEEW-CEF 2020). In 2021, NTPC invited EoI to set up 1,000 MWh of grid-connected battery energy storage systems for its power stations (NTPC 2021). A recent draft regulation allows energy storage to participate in the ancillary services market (CERC 2021). Following this, the government announced plans to tender 4,000 MWh of storage for ancillary services at four regional load dispatch centres (RLDC) (Economic Times 2021) and a 12 GWh battery energy storage project in Leh to be used as transmission and generation assets (MoP 2021).

Manufacturing :

Unlike with deployment, India has already taken steps to develop a framework for the development of indigenous battery manufacturing. In 2019, the Union Cabinet approved the National Mission on Transformative Mobility and Battery Storage to drive clean, connected, shared, sustainable, and holistic mobility initiatives (PIB Delhi 2019). It has proposed a phased manufacturing programme to support domestic battery manufacturing and EV components. The establishment of skill development programmes on EVs at the Indian Institutes of Technology (IITs) and the implementation of a PLI scheme for advanced chemistry cell (ACC) battery manufacturing are highly positive developments. In May 2021, the Cabinet approved the PLI scheme, National Programme on Advanced Chemistry Cell (ACC) Battery Storage, to achieve a manufacturing capacity of 50 GWh of ACCs and 5 GWh of “niche” ACCs (PIB 2021). Over five years, the scheme will disburse INR 18,100 crore as an incentive, linked to a percentage of the price of batteries sold. It focuses on the indigenisation of the value chain and sets a target of 60 per cent domestic value addition in five years. The scheme received 10 bids with a cumulative capacity of 130 GWh against the target of 50 GWh (PIB 2022), with Reliance New Energy Solar Limited, Ola Electric Mobility Private Limited, Hyundai Global Motors Company Limited, and Rajesh Exports Limited eventually winning the bid (PIB 2022).

These schemes have surely attracted the industry’s attention. Several Indian companies, such as Amara Raja and Exide, offer batteries for applications like electric vehicles, power backup, and frequency and voltage regulation. Reliance Industries has also committed to investing INR 75,000 crore (USD 10 billion) towards setting up giga-factories for new energy components, including batteries (RIL 2021). International technology providers are also planning to set up battery manufacturing plants in India. Industry and academia are conceptualising collaborations to develop new technologies further and help them reach market scale. Some key mentions are the memoranda of understanding (MoU) between Council of Scientific and Industrial Research- Central Electro Chemical Research Institute (CSIR-CECRI) and Tata Chemicals (Tata Chemicals 2018) and a similar tie-up between the Indian Space Research Organisation (ISRO) and ten Indian companies and start-ups for lithium-ion technology (ISRO 2018).

1.2 Objective

While India’s battery manufacturing sector is yet to take off, globally the lithium-ion battery manufacturing capacity has been growing rapidly. A battery manufacturing capacity of nearly 500 GWh was deployed in 2020, with about 40 per cent of this capacity consisting of large battery giga-factories (Moores 2021). While a few Indian companies have already begun domestic battery pack assembly, as we mentioned before, this has not kept pace with the growing Indian storage market. The resultant import bill for batteries has already touched USD 1.8 billion in 2022, as Figure 1 shows – with USD 1.6 billion (or over 85 per cent) worth of imports from China (including Hong Kong) (MoC&I n.d.).

Figure 1 India’s lithium-ion battery imports have risen significantly despite the COVID-19 pandemic

Source: Authors’ compilation from MoC&I import export data for HS code 85076000: Electric Accumulators (Lithium-ion)

As India aspires to develop a battery manufacturing ecosystem, it is important to identify potential opportunities across the entire manufacturing value chain. This will help policymakers to cultivate a resilient domestic manufacturing industry. Stakeholders on the verge of making key investment decisions are also expected to benefit from this research.

Our overarching objective in this issue brief is to guide the discussions and decisions of investors and policymakers to create a holistic battery manufacturing ecosystem. We do this by bridging the information asymmetry around the battery manufacturing industry and its supply chains; estimating the investment, energy, and material requirements of planned battery manufacturing facilities; and outlining the innovations in the battery manufacturing process that will help drive down costs. To estimate the active material requirement, we have developed three scenarios with varying levels of indigenised manufacturing of cumulative energy storage demand and technology mixes. The report assumes that the entire energy storage demand is met through batteries. Inclusion of other technologies like pumped hydro storage will reduce the demand from batteries. Scenario 1 assumes 60 per cent of the energy storage demand is met from domestic manufacturing (indigenisation level), with the IEA’s 2030 technology split for the utilityscale and EV sectors (IEA 2021). Scenario 2 considers a lower indigenisation level of 40 per cent with the same technology mix. Scenario 3 posits technological disruption and assumes an accelerated uptake of new technologies. Hence, we assume that the IEA’s 2040 technology mix (IEA 2021) will meet 60 per cent indigenisation in 2030.

Deployment targets are essential inputs to estimate the key cell components required to manufacture battery cells. In our study, we focus on estimating the demand for active electrode materials (cathode and anode) and the electrolyte. We use Ministry of Power’s Energy Storage Obligations till 2029-30 for estimating the utility-scale storage requirements and share of EV sales until 2030. Based on the existing analysis, we calculate the active electrode material and electrolyte requirements for three different scenarios.

Table 1 shows the annual targets (percentage) for storing the renewable energy between 2022-23 to 2029-30. We use the 19th Electric Power Survey (CEA 2022) to get India’s peak energy demand (GWh) during this period to estimate the obligated stored energy (GWh) and corresponding battery requirement (GWh) (Table 1).

Table 1 Projections for utility-scale energy storage requirement

Source: Authors’ analysis based on CEA 2022 and MoP 2022

The cumulative energy storage demand from grid applications comes to about 327 GWh by 2030.

Earlier, four studies have tried to estimate the energy storage requirements of the Indian grid by 2030. The cumulative demand, as indicated in Table 2, ranged between 108 to 152 GWh.

Table 2 Studies estimating India’s grid-connected energy storage requirement

Source: CEA 2020; Spencer, et al. 2020, Abhyankar, Deorah and Phadke 2021; Wartsila-KPMG 2021

For the demand for batteries in the transport sector, we rely on a 2020 study by the CEEW, which estimates the stock of EVs in India in 2030 under different scenarios (Soman, et al. 2020). Following India’s commitment to the EV30@30 campaign (Clean Energy Ministerial 2019), the report presents the socio-economic and environmental benefits of such a transition for the Indian economy compared to business as usual. It further varies the mode-share (high public transport, high private transport, and high shared mobility) assuming the 30 per cent EV sales in 2030 to present battery demand in three different scenarios. We share the demand for batteries under various scenarios in Table 3.

Table 3 Battery demand in the transport sector during 2022–2030

In our study, we use the resultant vehicle stock of the EV30@30 scenario to estimate the battery demand for the mobility sector. Therefore, the cumulative demand.

3.1 Methodology

India’s cumulative demand of 903 GWh for energy storage by 2030 is split among several technologies like lithium-ion-based batteries, redox flow batteries, and solid-state batteries. For this purpose, we rely on the IEA’s estimates of technology bifurcation in the utilityscale storage and electric mobility sector for 2030 and 2040 (IEA 2021).

• Scenario 1 (S1) – base case: In this scenario, we assume technology deployment based on the IEA’s 2030 market share. The indigenisation level for technology manufacturing is fixed at 60 per cent.

• Scenario 2 (S2) – low indigenisation: This scenario estimates the mineral requirement with 40 per cent indigenisation.

• Scenario 3 (S3) – disruptive: In this scenario, we assume an accelerated adoption of advanced technologies. For this, we use the IEA 2040 technology market share. The indigenisation level remains unchanged at 60 per cent.

3.2 Results

Our analysis shows that the utility-scale sector will be dominated by lithium ferrophosphate (LFP) batteries, while the other variants of lithium-ion batteries like nickel manganese cobalt oxide (NMC) have minuscule or negligible shares (Table 4). NMC batteries have a higher energy capacity than LFP batteries but are also costlier (Krishna 2022). Utility-scale applications require large storage capacities (MW scale); hence, the project costs can be substantial. Since these applications do not have space constraints, technologies with a lower energy capacity can be used to minimise project costs. So LFP technology is a popular alternative to NMC. For similar reasons, vanadium redox flow batteries are suitable for utility-scale applications and may see an accelerated adoption in caesura of technological innovations that enable market disruption (disruptive scenario). The base case also contains a small share of other battery technologies that are being tested out for these applications. Although the IEA report does not mention these chemistries, based on current global deployments, it can be assigned to batteries like lead acid (CNESA 2021a). These technologies are not included in the disruptive scenario, which is dominated by other cost-competitive and efficient alternatives for this application, like LFP and redox flow batteries.

Unlike the utility-scale sector, the transport sector relies on high energy density battery technologies, especially for the light-duty vehicles (LDV) segment (Table 5). Expectedly, LDVs predominantly use NMC and nickel cobalt aluminium oxide (NCA) batteries. On the contrary, the increased availability of hosting space and economies of scale makes LFP an attractive option for heavy-duty vehicles (HDV). In a disruptive scenario, advanced batteries, like all solid-state batteries (ASSB),3 will be used in these sectors as substitutes for a share of lithium-ion-based batteries. However, our analysis does not cover these emerging technologies, as a majority of these are at the prototype manufacturing stage, and so there is limited data available on their specifications.

Table 4 Demand for various energy storage technologies in the three scenarios for utility-scale storage (2022- 2030)

Source: Authors’ analysis based on information compiled from IEA 2021

Table 5 Demand for various energy storage technologies in the three scenarios for transport (EV30@30) (2022-2030)

Source: Authors’ analysis based on information compiled from IEA 2021

The findings in our energy storage outlook for 2030 are indicative of the magnitude of demand that can be expected for battery storage technologies in India over the coming decade. There could be a battery storage capacity requirement of nearly 900 GWh for mobility and stationary storage applications, and a vast majority (75–99 per cent) of this demand will need to be met in the form of lithium-ion batteries. For at least the next decade, several lithium-ion battery manufacturing facilities can be set up in India to meet this demand. The emergence of new technologies needs not deter these plans. For example, sodium-ion batteries can also be produced using a similar method to lithium-ion batteries; these can be used as a drop-in technology using the same plants that initially produced lithium-ion batteries (Roberts and Kendrick 2018).

The government and industry are already capitalising on this opportunity. Following the recent PLI scheme announcement, many established battery players, as well as fresh entrants to the space in India, have announced plans to build large-scale integrated battery manufacturing facilities, or giga-factories, by either expanding existing assembly plants or building brand new facilities (PV Magazine 2021). This scheme has attempted to drive the deep indigenisation of the battery value chain, mandating that companies based in India achieve 60 per cent domestic value-add to the manufactured cells within five years (PIB 2021). This target is ambitious and will require manufacturers not only to construct the announced manufacturing facilities – which currently do not exist at any scale in India – but also to support the establishment of a domestic battery component and materials manufacturing sector by 2030.

What path towards indigenisation will be most beneficial for companies entering the battery manufacturing space in India? The PLI scheme provides a basis for such a strategy, starting downstream, and then working up the value chain. But our research also highlights some strategic decisions that will have a major impact on the extent and pace of indigenisation for battery manufacturing companies. In this section, we will showcase the potential paths to indigenisation by illustrating the battery value chain in detail and using the existing government requirement of 60 per cent as a benchmark for adequate value chain on-shoring.

In Figures 3 and 4, we map out each of the steps in the battery value chain, from the sourcing of raw materials and components to the processing, manufacturing, and assembly of the finished battery. Given that the focus of indigenisation in India is primarily on advanced chemistry cells, our analysis is also primarily aimed at cell manufacturing and its upstream supply chain. We also provide the value added to the finished good (LIB cell) at each stage of the value chain for both June 2022 and June 2021 (in brackets, Figures 3 and 4). The stark difference between these two sets of figures is because of the rapid rise in commodity prices during the first few months of 2022, particularly for metals like lithium, nickel, and cobalt.

We map two of the most prominent value chains: that of NMC (Li-NMC-622) and LFP chemistry LIBs, although several other chemistries exist. These two value chains provide us useful frames of reference for the potential of indigenisation in India, as well as the susceptibility of battery prices to commodity price volatility.

Figure 3 Lithium nickel manganese cobalt (Li-NMC-622) chemistry value chain

Source: Author’s analysis, BatPaC 5.0, Shanghai Metals Market (SMM n.d.) ,CellEst 2019

Figure 4 Lithium iron phosphate (LFP) chemistry value chain

Source: Author’s analysis, BatPaC 5.0, Shanghai Metals Market (SMM n.d.) ,CellEst 2019

How can indigenisation go forward?

Evidently, cathode metals are the largest contributors to the final cost of a LIB cell (between 13 and 67 per cent in the highlighted value chains). Yet, and more importantly, the extent of this contribution is highly dependent on the battery chemistry and the market price of commodities. This is critical from the point of view of indigenisation; India’s mineral reserves are deficient in lithium, nickel, and cobalt, and importing these metals will be necessary if and when cathode active material production is set up in India later in the decade (Indian Bureau of Mines 2020). On-shoring will only be possible for other portions of the value chain.

The value addition from cell manufacturing is also noteworthy. While cell manufacturing involves the integration of many high-value components, the process itself only contributes 11–25 per cent to the final value of the cell (assuming large-scale production and depending on chemistry and commodity prices). This means that while cell manufacturing is an important first step, the main focus of indigenisation will need to be setting up battery materials processing and components manufacturing industries.

As per the ACC PLI scheme, we can expect 60 per cent domestic value addition by around 2027 or 2028. Even before this, the mother units will be required to provide 25 per cent domestic value addition by 2024. Attaining the initial 25 per cent value addition by solely setting up cell manufacturing might be difficult if commodity prices stay inflated, and manufacturers might need to add some quantity of component manufacturing as part of their mother units. They may also keep the sales price of the manufactured cells high, with these prices being offset by the subsidies disbursed.

As domestic cell manufacturers attempt to indigenise the remainder of their supply chain, they will need to catalyse the on-shoring of most, or all, of the battery component manufacturing industries. They will likely have to focus on the graphite anode material production (natural and synthetic) and cathode active material processing industries, which together contribute 13–35 per cent of the value of the LIB cell.

This phased approach to indigenisation promoted by the ACC PLI scheme formalises the roadmap envisioned by NITI Aayog and RMI in 2017 (NITI Aayog and Rocky Mountain Institute 2017). Cell manufacturing will likely scale up by the middle of this decade, and domestic supply chains will need to catch up by the end of the decade. The final phase of indigenisation will be the securing of critical minerals for domestic precursor cathode active material (pCAM) and CAM processing. But this sourcing challenge is likely to be a major concern only after 2028 or 2029, once India is home to a sizeable capacity for the cathode material processing.

Using cell manufacturing as the lynchpin of Indian indigenisation, in this section, we provide a detailed estimate of the investment required to set up LIB manufacturing plants in India (integrating cell manufacturing and battery assembly). We also highlight the energy that these plants will draw from the grid during operation, and the demand for materials that they will generate in the coming decade, which will need to be met by both imports and domestic production.

5.1 Capital expenditure

The initial investment needed to establish a battery manufacturing plant has fallen significantly in recent years, from above USD 0.3 (INR 22.5)/Wh of annual production capacity in 2011 to less than USD 0.1 (INR 7.5)/Wh of annual production capacity in 2019 (Bennett and Munuera 2020). Yet, since economies of scale can only be achieved at or above 2 GWh of annual manufacturing capacity (Mauler, Duffner and Leker 2021), the capital expenditure requirement is still on the order of several hundred million dollars. This cost is predominantly due to the multi-stage process involved in battery manufacturing, which requires a variety of specialised equipment, a factory floor, and a dry room to house this equipment.

Figure 8 A 5 GWh lithium-ion (NMC-622) battery manufacturing facility requires more than 230 million USD of equipment, distributed unevenly between manufacturing stages

Source: Authors’ analysis; Argonne National Laboratory (2020)

To estimate capital costs, we use a bottom-up model developed by Argonne National Laboratory (Nelson, et al. 2019), with the added assumption that capital equipment will need to be imported before suitable alternatives are found domestically. Just the cost of the capital equipment used in a plant capable of producing 5 GWh of NMC-622 batteries is estimated at USD 234 million (INR 1755 crore).

These costs are not spread evenly across the production stages, however. As Figure 8 shows, battery assembly requires more manual inputs – and thus lower equipment costs – than the other stages. On the other hand, electrode production is a highly automated process, and thus it entails more expenditure on manufacturing equipment. But it is the cell finishing process that requires the largest investment in capital equipment. There is a high cost associated with the electrical and electronic equipment used during cell formation.

Equipment costs are also not consistent across battery giga-factories producing different types of batteries. The energy density of the chemistry used (higher energy density corresponds to lower equipment costs) – particularly the number of cells and batteries produced – plays a major role in determining the initial investment required. Our analysis suggests that the total cost to a company setting up a 5 GWh plant, including the cost of land acquisition, factory floor space, warehousing, and connecting utilities, could lie anywhere between USD 325 million and USD 450 million (INR 2437–3375 crore).

For the 100 GWh of manufacturing capacity that we believe will be required in India to meet 60 per cent of the demand by 2030 (Scenario 1), the total investment requirement could approach USD 8 billion (INR 60,000 crore).

5.2 Energy demand

Energy is a key input in the battery manufacturing process. The high energy consumption is due to the need to eliminate moisture from the electrodes during cell production. Dry room conditions require the use of large industrial dehumidifiers and chillers (Dai, et al. 2019), and the final vacuum drying of the electrodes makes use of large quantities of heat as well (Kurland 2020). Similarly, heat is also used during the solvent recovery process. Together, these processes contribute to at least 80 per cent of the energy demand from the battery manufacturing process (Yuan, et al. 2017).

Based on publicly available figures, the energy usage in existing North American and European giga-factories is estimated to be 50–65 kWh per kWh of battery production (Kurland 2020), while plant-level data from a Chinese giga-factory indicates an energy requirement of nearly 50 kWh per kWh of batteries manufactured (Dai, et al. 2019). For a 5 GWh giga-factory, this would entail an annual energy demand of nearly a quarter of a terawatt-hour (TWh) or 250 GWh. If such a plant were set up in Gujarat and connected to the local utility, annual electricity costs would be around INR 122 crore (USD 16.2 million) (GERC 2020), and INR 2440 crore (USD 325 million) annually for the potential 100 GWh worth of plants that could be built by 2030.

The demand for the key battery materials by 2030 under different scenarios is derived from Argonne National Laboratory’s Battery Performance and Cost (BatPaC) model (Argonne National Laboratory 2020). The BatPac model gives the requirement (kg/kWh) of different components (active electrodes and electrolytes) at the cell level (Box 4).4 This number is multiplied by the demand for these technologies (Tables 4 and 5) to get the quantity of the cell component required by 2030.

India’s energy storage ambitions would require significant quantities of various active electrodes and electrolytes (Table 7 and Figure 10). Following the base case, a total of 1452 kilo tonnes (kt) of active electrodes and electrolytes would be required to meet the demand for 60 per cent of the 903 GWh energy storage capacity through domestic manufacturing. This decreases to 969 kt if India decides to meet 40 per cent of the cumulative demand through domestic manufacturing. Furthermore, if the Indian RE industry decides to opt for a more strategic mix of battery technologies, contrary to the current market trend – like in scenario 3 – then the demand for these components reduces to 1157 kt by achieving 60 per cent indigenisation. Specifically, India can reduce its dependence on critical cathode materials like Li-NMC811 and Li-NMC-532. The mineral requirement from the transportation sector will also vary with “how India moves”. The changing share of private vehicles, public transport, and shared mobility in new EV sales can considerably change the cumulative mineral requirement and the share of active electrodes and electrolytes like Li-NMC variants and NCA. Our analysis indicates that in the base case, the cumulative mineral demand is least when the share of public transport is highest in new EV sales, followed by the case where shared mobility has the maximum share.5 The demand is maximum when private vehicles dominate new EV sales (Annexure 2). In such a scenario, high energy density batteries, like NMC and NCA, dominate the technology mix, whereas with an increased share of public transport, the demand for lower energy density technologies like LFP increases.

Table 7 Cumulative requirement in kilo tonnes for active electrodes and electrolytes for India (2022-2030) under different scenarios

Source: Authors’ analysis

Figure 10 Cumulative active material requirement for India’s storage ambitions under different scenarios (2022-2030)

Source: Authors’ analysis

In this section, we discuss the key considerations for India to indigenise lithium-ion battery manufacturing. The recommendations are divided into three sections: innovation in manufacturing, policy changes, and R,D&D.

The first bucket of recommendations, which focus on improving the manufacturing process, are specific to lithium-ion battery technology. The other two themes of recommendations, on policy changes and broader R&D, are for the energy storage ecosystem. The development of the sector at large is critical for lithium-ion battery manufacturing to thrive.

But given the increasing cost of key battery materials, especially lithium, battery prices did not reduce in 2021 (Lee 2021). This rally in commodity prices, as well as the maturing of manufacturing processes globally, could hinder the competitiveness of battery storage technologies. Further progress will require a series of innovations in battery manufacturing processes, both in terms of incremental process improvements as well as in the complete overhaul of manufacturing methods and battery materials.

• Focus on battery cell component manufacturing

In the prevalent lithium-ion batteries (NMC and LFP), about 13–35 per cent of the value-add comes from manufacturing the active cathode and anode materials. India can leverage its experienced chemical industry to manufacture these components for domestic consumption as well as exports. The government could also emphasise chemistries that do not rely on geographically constrained minerals to abate supply chain risks and increase domestic value capture.

• Reduce materials costs

With the significant increase in commodity prices, bringing down material costs has become a key concern in battery innovation. This can be achieved in a variety of ways. Firstly, the choice of battery chemistry is paramount. Most manufacturers balance the price of battery materials with its potential energy density when designing the most cost-optimised battery. Given the price volatility of key battery materials such as cobalt, the demand for chemistries such as LFP might increase (Spilker 2021). Improved cell and battery architectures may allow chemistries with less critical mineral content to close the energy density gap with their higher critical mineral content counterparts (Walz 2021).

Another path for potential innovation is greatly increasing the energy densities of batteries by making use of new materials, with a minimal increase in the materials demand. At present, the focus of this push for energy density improvement is the battery anode (Scott 2019). Graphite anodes, which have thus far been preferred for their stability, are now seen as a key bottleneck in achieving greater energy density. Several alternatives exist; graphite anodes with a high silicon content, or lithium anodes, can potentially be used in a lithium-ion battery. The key challenge lies in designing a stable battery using these anodes while reducing non-material-related production costs by improving processes and scaling up manufacturing.

It might also be possible to reduce material costs by increasing the thickness of the electrode and creating more energy-dense cells. Currently, the limiting factor to increasing the electrode thickness is the restricted discharging rate (power density) as electrode thickness increases (Hawley and Li 2019). There are several proposed modifications to the electrode material that tackle this limiting factor; an effective doubling of electrode thickness could reduce cell costs by as much as 25 per cent (Hawley and Li 2019). One such solution that has already seen proposed investment in India is the semi-solid electrode, which uses a cathode electrolyte mixture and eliminates the need for binders (PV Magazine 2021a).

• Minimise electricity usage

Given the high energy requirement during battery manufacturing, reducing the energy intensity of battery manufacturing will enable further cost reductions in the production process. The most promising avenue for cost reduction is eliminating the need for solvents in electrode production. One proposed way to minimise the use of solvents is to use electrostatic spray deposition, where a gun sprays the aluminium foil with a cathode mixture of carbon black, active material, and binder (Hawley and Li 2019). Another less energy-intensive solution is the use of dry roll-to-roll manufacturing processes. Here, both the binder and the solvent are completely eliminated from electrode manufacturing. The active material, along with a compressible graphene layer, is pressed between two aluminium sheets (Hawley and Li 2019).

Manufacturers could also target reducing energy usage to maintain dry room conditions. Cell manufacturing is a moisture-sensitive process; manufacturing plants set up in geographies with low relative humidity would consume much less energy to ensure the required ambient moisture levels.

• Overhaul battery formation and ageing

Battery formation and ageing are the most costintensive processes in battery manufacturing. By modifying aspects of these processes, the equipment costs of battery manufacturing can be brought down significantly.

Since formation cycling may take between 3–7 days, and formation cycling and rack equipment are the biggest contributors to capital expenditure (CAPEX) costs in a battery manufacturing plant, efforts are underway to shorten or eliminate the formation cycling process to significantly reduce battery manufacturing costs. For example, atomic layer deposition (ALD) of artificial solid-electrolyte interphase (SEI) layers on the electrodes might be able to bring down formation cycling times to less than 10 hours (Wood III, Li and An 2019). The ageing process could also be optimised. With more precise quality-control processes, the potential for internal short-circuiting in cells could be evaluated through advanced analytics rather than physical measurements, thereby ensuring that most cells do not require the ageing process (Kupper, et al. 2018).

• Lower customs duties and tariffs on cell components:

The Indian government has already announced its intention to bring down the GST rate on LIBs from the current 18 per cent and 5 per cent (Baruah 2022). But for battery manufacturing facilities to be established in India, the focus on indirect tax reforms will have to shift to battery components and active materials. Currently, the GST rate and customs duty levied on battery parts (HS code: 85079090) sit at 18 per cent and 10 per cent, respectively. It is also unclear whether all battery components and materials will come under the ambit of this HS code or be taxed as distinct products. By bringing the indirect taxes and duties on these components down to 5 per cent (GST), and exempting customs duty for at least the next few years (say, up to 2025), the government can ensure the competitiveness of batteries manufactured in India vis-à-vis foreign players and also increase the demand for locally produced batteries in India.

• Support the industry target low-carbon markets:

Indian cell and battery manufacturers will begin targeting markets like the EU, which will put up emissions-linked trade barriers on batteries in the coming years (European Parliamentary Research Service 2022). Similar regulations are already in place in the solar industry in countries like France and South Korea (Bellini 2019). The government could help the industry target growing low-carbon markets by allowing them cheap and ready access to clean energy. This could be done first and foremost by enabling open-access connections to cell manufacturers, which will be a state prerogative. States should notify their open-access rules in line with the new Green Open Access Rules notified by the Ministry of Power at the centre (PIB 2022). At the same time, India should also pursue trade agreements with countries or regional blocs instituting lowcarbon policies. Finally, the government can fund pilot projects for low-carbon battery components and material manufacturing plants, which will need novel manufacturing methods – such as the use of green hydrogen for thermal energy during refining and processing – to decarbonise.

• Set ten-year targets:

We recommend that state electricity regulatory commissions (SERCs) set targets for storage deployment, in consultation with the Central Electricity Authority (CEA), Power System Operation Corporation (POSOCO), the respective State Load Despatch Centres (SLDCs), and other stakeholders. This would begin the process of investing in understanding applications and business models, which is essential to scale up private finance into storage. For example, the Rajasthan Electricity Regulatory Commission (RERC) proposed setting 5 per cent of the state’s renewable purchase obligations (RPO) each year as the target for storage (RERC 2021). Internationally, regulators in many states in the US require utilities to set up storage projects (Twitchell 2019).

• Provide financial and infrastructural support:

The energy storage manufacturing sector is yet to kickstart in India. To remain competitive, manufacturers would need to set up giga-factories, which would require a significant amount of CAPEX at affordable rates. The government can provide access to finance and infrastructure by sensitising key institutions across the country. The government has already allocated INR 18,100 crore (USD 2.4 billion) under the Production Linked Incentive (PLI) scheme – the National Programme on Advanced Chemistry Cell (ACC) Battery Storage – to achieve a manufacturing capacity of 50 GWh of ACC and 5 GWh of “niche” ACC (PIB 2021). Based on India’s deployment targets, the government could devise new support programmes in the short to medium term. One such programme could be to provide financial (CAPEX) support to battery component manufacturers. This will also provide a positive signal to investors regarding upstream battery industries.

• Support recycling:

Key battery minerals are concentrated in particular geographic areas and are mined by a limited number of companies. In addition, there is a significant lead time from identification to the mining process. It is expected that recycling can reduce the primary supply requirement for key minerals like copper, nickel, lithium, and cobalt by up to 10 per cent by 2040 (IEA 2021). Estimates show that the global recycling capacity of lithium would be 180 kt/year by 2021. Nearly half of the capacity is expected to emerge in China (IEA 2021). In the absence of long-term supply agreements, the government must focus on scaling up recycling infrastructure for batteries.

• Address regulatory roadblocks:

When storage is coupled with renewable energy sources, it may be considered part of the renewable generation (Parikh 2020). However, when used for ancillary services, it may be considered a grid element similar to transmission assets, where load dispatch centres may contract an independent operator for these services (RERC 2021). Storage may also be set up as a merchant capacity, while behind-the-meter storage would be considered part of micro-grids. Thus, the policy should explicitly classify storage based on where it connects with the network and its purpose, which would provide clarity on the regulatory amendments required. Storage can also play a key role in managing demand variability and network management, such as through load-levelling applications. Demand-side management regulations, already notified by most states, should be updated to open funding avenues for storage projects. For example, this is already taking place in the State Energy Conservation Fund and the Power System Development Fund. This would also allow states to tap into synergies with other technologies, such as energy-efficient appliances and demand-side response programmes.

• Support disoms:

The Forum of Regulators should design model regulations specifying methodologies to design and evaluate proof-of-concepts for storage applications developed by discoms. Organisations such as the Energy Efficiency Services Limited and Convergence Energy Services Limited can support discoms in demonstrating the applications of storage in the distribution network and designing model contracts for the procurement of services.

• Secure critical minerals for cathode active material (CAM) production:

Given the absence or limited availability of key lithium-ion-battery-related raw materials in India and the evolving landscape of global supply chains, India should strategically develop a plan to secure adequate access to these raw materials to support its goals of indigenisation of the upstream battery value chain. Since the requirements for these raw materials are unlikely to materialise until the latter half of the decade, we have explored recommendations on this issue in other paper (Dutt Arjun and Akanksha Tyagi 2022).

Clear objectives

The Ministry of Power and the Ministry of Road Transport and Highways should set clear objectives and targets for batteries in grid and electric vehicles as part of the energy storage roadmap. It will be critical for driving innovation in energy storage. These cost and performance targets will provide clear direction to R&D and financing institutions as well as help set parameters to transparently evaluate technologies. Such targets should be identified by gathering inputs from multiple stakeholders in the sector.

• Target cost reduction: This can be facilitated by decoupling long-duration, short-duration and EV storage technologies in India’s energy storage policy. This will allow for highly ambitious targets for longer-duration energy storage in India (in line with global targets such as the 90 per cent levelised cost of storage reduction target in the US) (US Department of Energy 2021). Research can be provided by Department of Science and Technology to achieve these targets.

• Prioritise end-use applications: Identification of applications and the determination of applicationlinked performance metrics are critical in evaluating the success of newly developed technologies.

• Drive innovation through performance metrics and domestic value-add: The programme can target maximising domestic value-add and improving specific parameters, like cycle life, recyclability, domestic supply chain coverage, and safety. This would help make the manufacturing industry more agile and resilient.

Strengthen stationary energy storage R&D in domestic institutions

• Build institutions: Centres of excellence (COE) can be created in publicly funded institutions for energy storage, and in particular, long-duration energy storage. These centres should be multidisciplinary in nature, given the wide variety of potential storage technologies. Additionally, players should establish partnerships between Indian institutions and international private or government organisations in energy storage.

• Provide R&D budgets: The state can set up a dedicated R&D funding programme for battery storage research, such as the one that the UK implemented for EV batteries. This programme provides grants for targeted research that addresses various cost or performance parameters identified as part of objective-setting (UKRI 2021). Such funding can be open to both institutions and industries.

Increase the sustainability of the manufacturing process

Manufacturing companies with a high dependence on a specific country or mineral vendor should focus on finding alternatives and substitutes to critical minerals with a stretched supply chain. Additionally, they need to focus on improving the sustainability of the manufacturing process by reducing electricity, water, land, and material usage.

Commercialise research products through lab-to-market support

Research outputs often fail to be commercialised. Bridging the gap between public research funding and private sector financing is a major roadblock in bringing energy technologies to the market(Murphy and Edwards 2003). Policy support is required to ensure that domestic energy storage innovation can be at commercially competitive rates.

• Provide start-up incubators and technology industrialisation centres: Energy storage startups will require large capital infusions during the prototyping and early pilot phases. Incubators will need to be set up to help these start-ups gain access to funding and reach out to industry partners for collaboration. Such incubators, built on a collaborative model between industry players and the government, have already seen success in the biotechnology industry in India (BIRAC 2021) as well as in energy technology incubators in Europe (EIT InnoEnergy 2021). States can take a lead and set up an energy storage technology industrialisation centre should be set up to support the scaling up of production through up-skilling and product improvement(UKBIC 2020).

• Facilitate demonstration projects: The lack of field-validated operational experience is often a major roadblock to the commercialisation of new storage technologies (US Department of Energy 2020). Central funding for demonstration projects, provided through a competition based on stringent performance criteria, would help innovators gain necessary technical and operational experience (Department for Business, Energy and Industrial Strategy 2021). Further, to speed up the deployment of business model demonstrations, a facilitating organisation should be set up to bring together discoms and energy storage developers. This organisation would independently evaluate proposals and recommend the necessary financial support.

• Develop skills: Developing core competencies in energy storage research, as well as in the related manufacturing and deployment workforces, will be essential to enable a large-scale roll-out of energy storage in India. China, for example, has developed an action plan for developing undergraduate majors and cross-discipline education in energy storage from 2020–2024 (CNESA 2021b). India’s Ministry of Education should undertake such a coordinated focus on energy storage across India’s higher education institutions.

Multiple interventions are required to ensure that investors are interested in funding battery manufacturing. Broadly, these interventions can be categorised into three types:

Taking a strategic view on the sector will ensure that India is a trend-setter, and not a follower, in the battery manufacturing ecosystem. In the absence of such a concerted strategy, the government would need to intervene periodically through artificial support measures.

Energy storage systems are slated to play a critical role in the global decarbonisation process, leading to an exponential increase in their demand. Trends suggest that batteries based on lithium-ion technology will have the largest market share in the foreseeable future. India should strive to not only meet the demand via domestic manufacturing but also aim to become an export powerhouse. This would require the government to think strategically about different aspects of the value chain – procurement, manufacturing, deployment, and recycling. The progress on each of these aspects is currently limited and would require a mix of stakeholders – from government, industry, research, and academia – to work together. The accessibility of minerals at favourable prices will be a critical aspect for global competitiveness. India’s foreign policy must align with new trends and target strategic interventions in key geographies.

Designing a long-term roadmap is the most urgent intervention that the government needs to undertake. This will help stakeholders across the value chain align with the country’s long-term vision. A specific focus on R&D, process improvements, and recycling can reduce the need to source cell components from other countries. Academia must immediately start designing courses and curricula to meet the increasing demands of the workforce. Through multiple interventions, India can indigenise a large part of the lithium-ion battery manufacturing ecosystem.

Advancing Solar Cell Manufacturing in India

Establishing a Sodium-ion Battery Ecosystem in India

Making India a Hub for Critical Minerals Processing

State of the Sector: Critical Energy Transition Minerals for India