Council on Energy, Environment and Water Integrated | International | Independent

This paper examines how emerging economies can design effective emissions trading systems (ETSs), drawing on insights from a KAPSARC-CEEW workshop and a comparative analysis of China, India, Viet Nam, and Türkiye. It finds that these systems benefit from alignment with national development goals and generally adopt phased implementation, often beginning with intensity-based targets, free allocation, and limited coverage to balance economic and environmental goals. Over time, ETSs tend to evolve toward greater stringency, broader sectoral scope, and improved market functioning through iterative learning. A central finding is that robust monitoring, reporting, and verification systems are essential for effective ETSs. The paper also evaluates the role of offsetting, using carbon credits from outside the ETS scope, highlighting their potential to enhance flexibility while cautioning against risks to environmental integrity. Finally, it underscores the growing influence of global dynamics, including carbon border measures and market cooperation, in shaping domestic carbon market strategies. Overall, ETS effectiveness depends on adaptive, context-specific design rather than a single universal model.

Amid signs of slowing global climate momentum, carbon markets, specifically government-regulated ones, appear to be gaining momentum. Emissions trading schemes (ETSs) are at the heart of these developments.

The reason is threefold. First, studies suggest that governmentregulated carbon pricing schemes are among the most cost-effective instruments for managing greenhouse gas (GHG) emissions (Eden et al. 2018; Bai and Ru 2022; Chai et al. 2022; Ahmad, Li, and Wu 2024). Cost effectiveness is of particular salience for developing countries as they consider ways to reduce emissions.

Second, past experience demonstrates that only governmentregulated, compliance-based systems, as opposed to voluntary ones, can drive emission reductions at large scale: privately regulated carbon market standards that cater to voluntary uses are prone to conflicts of interest and quality issues,1 which can be addressed through government regulation and oversight.

Third, with an increasing number of countries contemplating border carbon adjustments, carbon pricing compliance schemes have been emerging as an attractive option to enable the retention of related revenue domestically.

Various countries, particularly emerging economies, are considering or developing new market schemes, many of which are compliance-based. At the same time, many existing ETSs are undergoing major changes and design upgrades – with the Chinese national ETS expanding its coverage and moving to an absolute cap as the most recent and notable example.

By and large, ETSs are complex instruments, with deep interactions across key policy areas, such as industrial policy, trade, and energy pricing. Their development and operation are multifaceted endeavors, and their setup tends to be highly context-specific and time-consuming.

To gain an up-to-date view of this dynamic and complex landscape of compliance carbon market developments in emerging economies, KAPSARC and CEEW convened an expert workshop in Riyadh on 27 October. The event approached the topic through four sessions: (1) drawing on lessons from existing ETSs; (2) identifying the drivers and shapers of compliance markets in emerging economies; (3) assessing the potential gains from integrating carbon crediting into compliance schemes; and (4) discussing the benefits of cooperation and harmonization among market schemes.

This joint Commentary by authors from CEEW and KAPSARC builds on the presentations and discussions at the Riyadh workshop, complemented by secondary literature sources, and puts forward an analytical view on the core topics discussed. The core focus of the paper is effectiveness – how emerging economies can develop and operate carbon market schemes that deliver on their intended objectives and targets effectively, including delivering the desired emission reductions cost-effectively while ensuring environmental integrity.

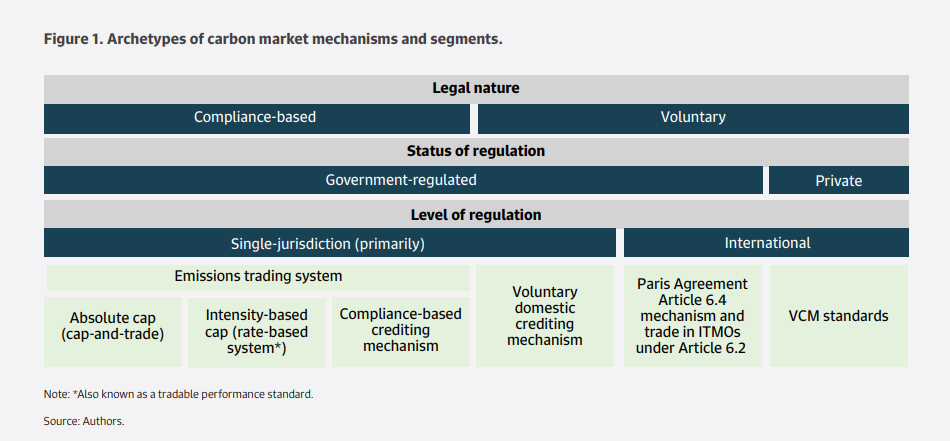

Carbon market mechanisms can be segmented based on various features, including their legal nature (compliance-based vs. voluntary), status of regulation (government vs. private), and level of regulation (single-jurisdiction vs. international), as shown in Figure 1.

The main focus of this Commentary is on compliance-based, government-regulated, single-jurisdiction markets, which are generally referred to as ETSs. As of late 2025, only six developing countries2 had operational ETSs or similar compliance-based trading schemes. China had eight subnational ETSs in place, alongside its national-level ETS (ICAP 2025a; World Bank 2025a).3 India, Indonesia, Mexico, Montenegro, and South Korea also had national-level ETSs.

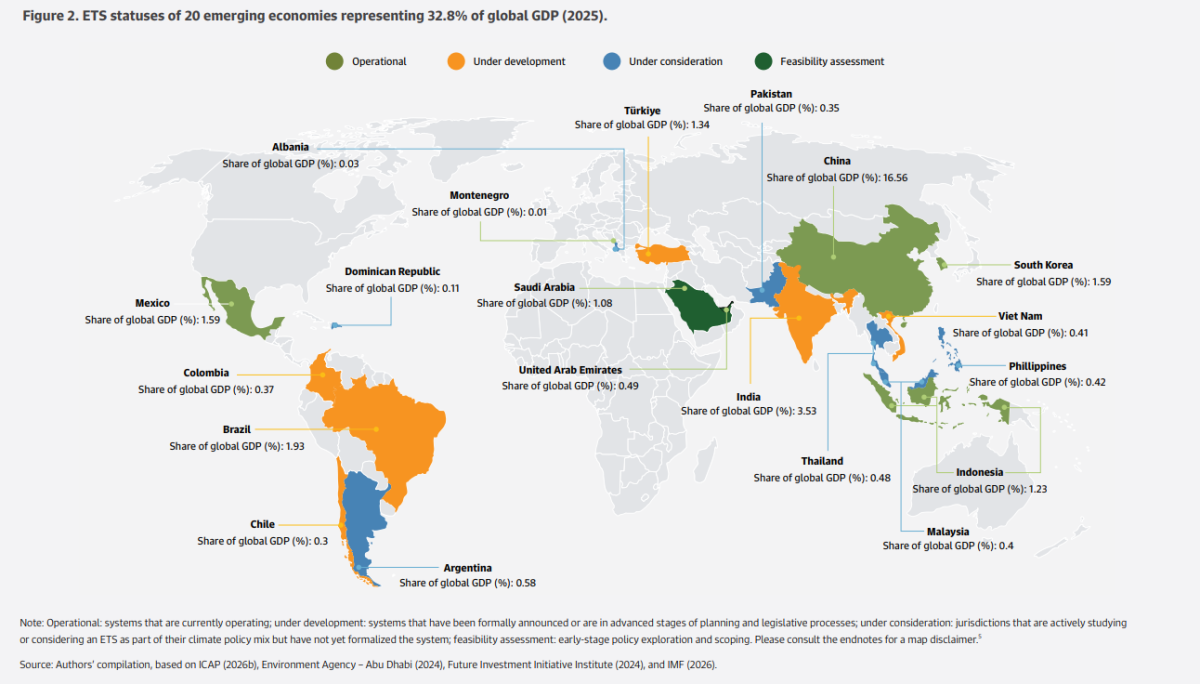

However, in addition, five developing nations (Brazil, Chile, Colombia, Türkiye, and Viet Nam) have ETSs under development, and a further seven (Albania, Argentina, the Dominican Republic, Malaysia, Pakistan, the Philippines, and Thailand) are classified by the International Carbon Action Partnership (ICAP) and the World Bank as considering one (ICAP 2025a; World Bank 2025a). Furthermore, in the Gulf, the United Arab Emirates and Saudi Arabia have been assessing the feasibility of an ETS (Environment Agency – Abu Dhabi 2024; Future Investment Initiative Institute 2024).

Together, these 20 emerging economies comprise a major share of the global GDP, meaning choices related to the development and operation of carbon market schemes will have major ramifications beyond emissions, affecting the global economy, trade, and development more broadly (see Figure 2). Notably, 12 of these 20 countries are located in Asia, where the region’s second-largest economy, Japan, is also in the process of operationalizing an ETS, making Asia a hotspot of compliance carbon market development. Of the remainder, six are in Latin America and two are in Europe.

The following sections focus on analyzing some of the most advanced systems illustrated in Figure 2. Section 3 begins by drawing lessons from some of the more mature systems. Section 4 then presents deep dives into four major emerging economy ETSs: China, India, Türkiye, and Viet Nam. Section 5 identifies lessons from integrating offsetting into carbon pricing compliance schemes in Colombia and South Africa. Section 6 briefly examines Japan, which has been a pioneer in engaging with multiple developing countries in international cooperation on carbon crediting.

Of the 38 ETSs operational today, 25 are located in developed economies. Out of the 14 hosted in developing countries, China alone hosts nine. Excluding ETSs that have been operational for less than five years, there are 23 ETSs in total, from whose experiences countries now developing or operationalizing ETSs can draw. This section summarizes lessons from these schemes.

From the developing world, only eight Chinese pilots and the Korean ETS are included among the 23 older systems. The remaining 14 are located in Europe (EU ETS and the Swiss ETS), Asia (New Zealand ETS, the Japanese city ETSs in Tokyo and Saitama, the Australian Safeguard Mechanism, and Kazakhstan’s ETS), and North America (California’s cap-and-trade [CaT] system, RGGI,6 the Massachusetts scheme in the United States, Québec’s CaT, Alberta’s TIER,7 subnational schemes in Newfoundland and Labrador and Saskatchewan, and the federal Output-Based Pricing System [OBPS] in Canada).

A study by Wahbah and Luomi (2025), which compared 37 operational ETSs, identified patterns that newer systems are also likely to follow:

• Strategic role: ETSs may be used either as explicit carbon pricing or signaling tools to drive emission outcomes, or they can be set up as signaling tools for the longer term.

• Increasing stringency: The coverage, complexity, and stringency of ETSs – including prices – tend to increase over time.

• Endogenous learning: Systems learn iteratively from their own experiences as they gain insights into the functioning of the market and its participants and gather more and better emissions data.

• Exogenous learning: Systems build on others’ experiences, particularly in relation to flexibility mechanisms (e.g., offsetting) and price and supply adjustment mechanisms (e.g., market stability reserves [MSRs]). However, reaching system maturity takes time, and leapfrogging enabled by accumulating global experience does not appear to apply to ETSs, given their highly context-specific nature.

• Adaptation to local context: Overall, given the broad – and continuously widening – set of design feature options and their possible combinations, ETSs can be adapted to vastly different country circumstances.

3.1 EU ETS, California CaT, and Canada’s Federal OBPS

These major developed-country ETSs differ in their design characteristics, representing examples of both absolute cap-and-trade systems (EU and California) and intensity-, rate-, or tradable performance standard-based systems (Canada) for cap setting. They also use diverse mechanisms to manage prices (MSR in the EU, an auction reserve price as the floor price in California, and direct payment as the ceiling in Canada) and apply different approaches to flexibility (e.g., the EU currently does not allow offsetting, California links with Québec, and domestic credits are eligible in Canada). While the EU ETS applies uniform rules to all member states, Canada allows each province or territory to develop its own system for large emitters.

Common across all these systems is that they currently deploy a form of output-based allocation through free allocations provided to trade-exposed, high-emitting sectors. The EU and California auction allowances for the power sector, with California auctioning a share via consignment auctions (ICAP 2025a; ICAP 2025c).8 The EU is in the process of phasing in auctioning for its trade-exposed sectors as well, and is introducing its Carbon Border Adjustment Mechanism (CBAM) in tandem to protect these industries from carbon leakage (European Union 2023).

3.2 South Korea

South Korea, which joined the industrialized countries’ Organisation for Economic Co-operation and Development in 1996,9 still relied on the steel, petrochemical, and refinery industries for its economic development in the 1980s and 1990s. It formally established an ETS in 2015, following a gradual process that started with a presidential initiative in 2008, which led to the establishment of medium-term emission reduction targets for 2020 and 2030.

Both the emission reduction target setting and subsequent ETS design involved more than 100 meetings and public hearings with trade unions, civil society, and experts. The legal foundation for the Korean ETS was established between 2009 and 2012, and the ETS was preceded by a “target management system” that focused on emissions monitoring, reporting, and verification (MRV), and strengthening market participants’ experience with mitigation and related strategies.

The Korean ETS has been operating since its inception with absolute caps, despite the national 2020 GHG target being an intensity-based one. Absolute caps are applied to achieve certainty over emissions outcomes and the volume of allowances to be allocated (and auctioned), and to promote stability in allowance prices. The strategic approach driving allowance distribution has been to start with free allocation to gain participants’ acceptance, introduce benchmarking for free allocations as soon as data availability allows, and gradually increase the share of auctioning.

3.3 Lessons

Important broad lessons can be derived from these four major schemes:

• Leadership: Both political leadership and thorough stakeholder engagement can be crucial success factors in establishing an ETS.

• Data: High-quality, third-party-verified, entity-level data is crucial for system functioning.

• Getting started: Systems can be, and are only, refined as experience accumulates – it is impossible to design a perfect system on paper.

• Cap: Absolute caps are perceived to provide more certainty for system participants. Of relevance for emerging economy contexts is the Korean experience, namely, that setting an absolute cap does not preclude the possibility of allowing total emissions to initially increase to limit the economic impacts of the ETS on system participants. Consistency of the ETS cap with national emissions targets can also ensure fair burden-sharing across sectors.

Relating to the distribution of allowances, existing schemes have shown that:

• Auctions: These can be useful for market liquidity, price transparency, and stability. They also raise government revenue that can be reallocated to support further mitigation or to compensate for distributional effects.

• Free allocation: These may be useful from a political acceptance perspective and to address carbon leakage concerns and consumer price impacts. However, governments tend to initially overallocate rather than underallocate. Price discovery is also, in practice, difficult when high or all shares of allowances are allocated for free. Limitations on banking can encourage further market activity in systems with low levels of auctioning.

• Driving mitigation: Decreasing the share of free allocations by tightening intensity benchmarks over time can be implemented alone or in parallel with the introduction of auctions to strengthen market liquidity and deliver higher mitigation outcomes. In addition, governments may consider introducing so-called income-based policy instruments, such as clean subsidies or tax incentives, which can be targeted to address the distributional impacts of ETSs.

• Iterative adjustments: Experience suggests that allocation is a matter of “market art” rather than “market science” – each system, each phase, and even each compliance period is different, and regulators will need to iteratively adjust their allocation policies and rules.

Specifically, in relation to allowance prices, experiences and stakeholder views indicate:

• Objectives, not prices: Focusing on whether ETSs achieve their intended objectives and align with broader climate targets may offer a more constructive framing than judging them by allowance prices. If a country is on its desired trajectory, emissions are declining, and compliance levels are high, price should be a secondary concern.

• Signal of low-cost options: Instead of implying low ambition, low allowance prices can also signal the existence of low-cost mitigation options in the system.

• Allocation as the cause: Low prices do not necessarily indicate market failure, but simply a market that is functioning in response to overallocation. This tends to occur in the early stages of ETSs when governments err on the side of more allocations.

• Stakeholder buy-in: While low prices are less effective in sending a long-term signal on the need to decarbonize, in some countries, introducing high prices “too early” is perceived as counterproductive for constructive industry engagement in ETSs.

Since the EU launched the world’s first ETS focused on GHGs in 2005, emissions trading has gradually evolved from a predominantly developed-country instrument to one increasingly adopted by emerging economies.

Over the past five years, particularly across Asia, countries have accelerated efforts to design, pilot, or operationalize their own national ETSs. This reflects a structural shift in climate policy, where market-based mechanisms are increasingly seen as tools for achieving objectives that span emission reduction, economic efficiency, and alignment with global trade and climate requirements.

Among emerging economies, India, China, Viet Nam, and Türkiye represent four distinct but converging pathways toward establishing national carbon markets. Together, these countries represent approximately 22% of global GDP (IMF 2026) and all are currently either actively operationalizing or significantly expanding their national ETSs. Their ETS development is shaped by a mix of climate ambition, institutional readiness, industrial structures, global supply chain dynamics, and the need to balance economic growth with decarbonization.

These four countries were selected because they represent major emerging economies that are among the earliest to move toward economy-wide or nationally coordinated ETS frameworks, offering instructive examples of how large developing economies are designing compliance carbon markets. While other major emerging economies have also pursued emissions trading, their systems either remain in early operationalization (Brazil), prolonged pilot phases (Mexico), or are currently limited in sectoral scope (Indonesia).

Despite being at different stages of maturity, ranging from China’s and India’s operational national schemes to Viet Nam’s and Türkiye’s pilot phases, these systems reveal both shared strategic patterns and divergent policy choices.

This section first provides an overview of the evolution of these four national carbon market compliance schemes and then identifies cross-cutting themes across the countries’ trading scheme pathways.

4.1 Comparative Overview of ETS Evolution in Four Emerging Economies

4.1.1 China

China’s ETS is the most advanced among emerging economies, shaped by more than a decade of structured learning that began with its deep engagement in the Clean Development Mechanism (CDM) in 2005. The CDM era created a strong institutional foundation, including the training of verifiers, the emergence of project developers, and the development of regulatory systems, many of which later transitioned directly into ETS capacity and functions.

In parallel, several CDM projects were eventually converted into domestic credits for use in compliance and voluntary markets (Ba, Thiers, and Liu 2018). Building on this, China launched a total of 12 regional ETS pilots to test allocation models, MRV systems, registry platforms, and compliance behavior, creating a skilled administrative and industrial workforce and significantly improving emissions data quality.

This groundwork enabled the launch of the national ETS in 2021, initially limited to the power sector. Based on its pilot experiences, China opted to use technology-based and intensity-based benchmarks, which were deemed aligned with China’s economic growth trajectory (Ewing 2024). China is now preparing to transition to absolute caps by 2026 (ICAP 2025d), signaling a tightening of climate ambition in line with its 2030 emissions peak and 2060 carbon neutrality goals (ICAP 2025i).

From 2025, the ETS has expanded to include steel, cement, and aluminum smelting, bringing 1,334 additional emitting entities under its scope and raising coverage of the country’s total carbon emissions from 40% to 60% (Ministry of Ecology and Environment of the People’s Republic of China 2025). The coverage of gases has also broadened to include tetrafluoromethane (CF4 ) and hexafluoroethane (C2 F6 ) emissions from the aluminum sector. The next phase of expansion is likely in 2027, with the inclusion of further major emitting industries (IEEFA 2025).

Since 2025, offset credits from the China Certified Emission Reduction (CCER) government-managed voluntary program are allowed to be used by compliance entities for up to 5% of their verified emissions to maintain strong internal abatement incentives.

China’s path demonstrates the importance of piloting for readiness, aligning design with national development priorities, and maintaining strong political support, making the Chinese ETS the world’s largest and a reference model for other emerging economies.

4.1.2 India

India established the framework for the Indian carbon market under the Carbon Credit Trading Scheme (CCTS). Within the scheme, the institutional structure comprises a national steering committee, co-chaired by the Ministry of Power and the Ministry of Environment, Forest and Climate Change. Grid India functions as the registry, and the Bureau of Energy Efficiency (BEE), a nodal body within the Ministry of Power, serves as the administrator.

The CCTS consists of two mechanisms: the compliance mechanism and the voluntary offset-based mechanism. The compliance mechanism follows a bottom-up, intensity-based target-setting approach informed by sectoral marginal abatement cost curves. Emission-intensive industrial plants designated as obligated entities are required to meet assigned greenhouse gas emission intensity (GEI) targets.

While allocation within the target is free, India does not issue allowances, as the EU ETS or the Chinese national ETS does, for example. Instead, after the compliance cycle, credits are issued only to entities that overachieve their targets, in amounts corresponding to the overachievement, while those that fall short must purchase credits from the market and surrender them to the government to cover the gap.

Under the voluntary offset mechanism, non-obligated entities may voluntarily register projects that reduce, remove, or avoid GHG emissions for the purpose of seeking issuance of carbon credit certificates. Figures A1 and A2 provide further details about the CCTS, including its mechanisms of credit generation and trading, among others.

The CCTS is built on more than a decade of institutional experience under India’s national Perform, Achieve and Trade (PAT) scheme, which regulates energy efficiency through installation-level targets set via detailed energy efficiency audits. The adoption of the CCTS reflects India’s shift from monitoring energy efficiency to emissions intensity. The sectors transitioned from the PAT scheme to the compliance mechanism under the CCTS include steel, aluminum, cement, chlor-alkali, petrochemicals, petroleum refineries, pulp and paper, and textiles. In addition, India’s experience with renewable energy certificates, Energy Conservation Act reforms, and years of MRV capacity building created the institutional backbone needed for the emissions market scheme.

Unlike China, India intentionally excluded the power sector during early implementation due to the highly regulated nature of the industry, tariff design challenges, and interactions with overlapping policies. This reflects India’s careful approach to balancing climate goals with affordability and energy security.

India’s compliance scheme implements emissions intensitybased target setting (Bureau of Energy Efficiency 2024), which is consistent with its NDC commitment and is also perceived to be aligned with its projected economic growth trajectory. Offsetting is not allowed in the compliance market to ensure a focus on direct industrial mitigation.

The CCTS requires robust MRV for compliance, mandating annual GHG monitoring by obligated entities, adherence to ISO 14064 standards, and verification by Accredited Carbon Verification Agencies (ACVAs)(Sentra World 2025). Key elements of the MRV framework include digital tracking, standardized reporting of emissions intensity data to the BEE (Press Information Bureau, Government of India 2024), and adherence to sector-specific intensity targets set by the government, with reporting due within months of the compliance year.

Key lessons from India stem from its decade-long experience in implementing the PAT scheme, which has enabled the development of robust institutional capacity, facility-level data systems, and compliance infrastructure necessary for detailed target-setting mechanisms. In that sense, its adoption of emissions intensity-based targets reflects the perceived compatibility and scalability of this approach for growing economies without impacting economic growth. Crucially, the evolution of PAT has shown that strong MRV governance, including standardized baselines, accredited third-party verification, and strong governance oversight, is a prerequisite for the functioning of a credible system.

4.1.3 Viet Nam

Viet Nam is currently establishing its own carbon market under its 2050 net-zero roadmap (ICAP 2025h). Guided by Decision No. 232/QD-TTg and Decree 06/2022/NĐ-CP, a pilot phase from August 2025-2028 precedes a full rollout after 2029 (Chu 2025). During full implementation, the system is expected to include expanded coverage and possibly more advanced allocation arrangements, such as auctioning.

The pilot phase is being applied to around 150-200 facilities in three high-emission sectors, namely, thermal power, cement, and steel, which together account for 40% of Viet Nam’s total emissions (Mt. Stonegate 2025).

These sectors were chosen based on two criteria. First, they are major national emitters and therefore central to the country’s overall mitigation profile. Second, they are among the industrial categories most exposed to the EU CBAM, meaning that failure to demonstrate emission reductions could result in a loss of export competitiveness.

Viet Nam is therefore using sector inclusion not merely as an environmental measure but also as a trade and industrial competitiveness strategy. By targeting sectors already integrated into global value chains, Viet Nam strengthens the resilience of its export economy and aligns domestic policies with international carbon cost pressures.

As the market matures, other sectors, such as transportation, commercial real estate, and additional industries, are expected to be included over time, but only once MRV capability, administrative preparedness, and stakeholder acceptance reach the required thresholds (Mt. Stonegate 2025).

Under its regulatory framework, both domestic allowances and international carbon credits are tradable within the same marketplace, operated by the Hanoi Stock Exchange. In the pilot phase, all allowances are allocated freely, with the possibility of introducing auctioning in the future, and emissions targets are set based on intensity benchmarks.

The revised decree introduces a range of flexibility mechanisms, under which covered entities are allowed to use offsetting credits for up to 30% of their compliance obligations, which is significantly higher than, for example, in China. Unused allowances may be banked for use in future compliance periods until the end of 2030 (ICAP 2025h). The system also allows entities to borrow up to 15% of allowances from future allocation periods to meet current compliance obligations.

Drivers of Viet Nam’s carbon market include severe climate vulnerability, net-zero 2050 commitments, export exposure to the EU CBAM, the objective of attracting transition finance (including under the country’s Just Energy Transition Partnership) (Saio 2026), and the desire for a flexible, investment-friendly decarbonization pathway.

Data, MRV, and governance remain the core challenges: data inconsistencies and limited verification capacity underpin an intentional choice to use the ETS pilot phase as a period for learning to strengthen MRV methodologies and institutional readiness (Tang and Mizunoya 2024).

Viet Nam’s carbon market represents a structured, pragmatic, and internationally aware approach to emissions regulation. It balances national climate commitments with industrial competitiveness, particularly in export markets vulnerable to the CBAM. By anchoring the system in strong legal frameworks, establishing clear institutional mandates, sequencing implementation through a multi-year pilot phase, and adopting flexible compliance mechanisms, Viet Nam has created a realistic pathway for decarbonizing heavy industry while maintaining economic momentum.

As MRV systems mature, coverage expands, and the market transitions toward more advanced allocation models, Viet Nam is positioned to evolve into a credible and regionally significant carbon pricing system, demonstrating that emerging economies can design sophisticated market mechanisms tailored to their development stage and trade exposure.

4.1.4 Türkiye

Türkiye’s ETS is emerging as a direct response to EU CBAM trade exposure, including an intent to align with the EU ETS model, which would allow for future system linkage and cross-border offset recognition (Asici 2025). Nearly half of Türkiye’s exports go to the EU, and many of its key industrial products fall under CBAM-covered sectors. Without a domestic carbon price, Türkiye is estimated to face rising CBAM liabilities of potentially up to €2-$5 billion in additional costs per year by 2030.

Starting in 2014, the Turkish MRV system progressed over five years to include more than 400 installations, accounting for 48.8% of total emissions. This provided strong technical capacity for ETS implementation. With the passing of its first Climate Law in 2024, Türkiye obtained the legal mandate to operationalize its ETS.

The rollout is phased as follows:

• Pilot phase (2026-2027): This covers core CBAM sectors (iron and steel, aluminum, cement, fertilizer, electricity, and hydrogen) (Kınıkoğlu 2026).

• Full implementation (2028 onward): This expands to all sectors covered by the MRV regulation.

Türkiye has adopted an intensity-based cap system that includes free allocation based on benchmarks. The inclusion threshold is set at 50,000 tonnes CO2 e for installations in the power and industry sectors (ICAP 2025e). Domestic carbon credits are expected to be allowed for up to 10% of surrender obligations after, but not during, the pilot phase. A carbon mechanism board and a market stability board will balance carbon price levels with macroeconomic considerations.

Türkiye must navigate a delicate balance given that its ETS will not, in its initial stages, establish an “effective carbon price” (European Union 2025), and it remains uncertain whether the EU would recognize Turkish ETS allowances in some form for CBAM adjustment purposes. At the same time, without auctioning, the Turkish ETS will not generate the revenues needed to help the fiscal recovery associated with CBAM payments.

4.1.5 Others

Besides India, China, Viet Nam, and Türkiye, several other major emerging economies, especially in Asia, are rapidly advancing their domestic carbon compliance pricing frameworks.

Indonesia has already launched its national ETS and is gradually expanding coverage, while Thailand and the Philippines are both in the final stages of readiness and are expected to implement full ETS systems in the short to medium term. Malaysia, meanwhile, has announced plans to introduce a national carbon tax from 2026 (IETA 2025) before transitioning to an ETS. Mexico also provides an important point of reference, having implemented Latin America’s first ETS through a pilot phase launched in 2020 alongside existing carbon taxes at federal and local levels.

More broadly, developments across Latin America, including Brazil’s recent legislative progress toward establishing a national emissions trading framework, signal that interest in market-based carbon pricing instruments is expanding beyond Asia. Together, these developments indicate a broader regional shift among emerging economies toward market-based carbonpricing policy instruments.

4.2 Cross-Cutting Themes Across Emerging Economy ETS Pathways

Across the developments in India, China, Viet Nam, and Türkiye, several clear patterns emerge:

1. Policy alignment with NDC and net-zero commitments: All four economies are calibrating ETS design to align with medium- and long-term climate trajectories and 2030, 2050, and 2060 target milestones, while placing a strong emphasis on preserving the space for economic growth. For example, China’s national ETS is explicitly embedded within its dual-carbon goals of peaking emissions before 2030 and achieving carbon neutrality by 2060, while India’s emerging CCTS has been framed as a mechanism to support its updated NDC targets and longer-term net-zero commitment by 2070. Similarly, Viet Nam and Türkiye have integrated ETS development into broader climate policy frameworks and NDC implementation strategies. In this sense, ETS development is perceived as reinforcing the credibility of these countries’ international commitments.

2. Value of pilots and earlier market mechanisms: China’s pilots and India’s PAT scheme demonstrate that prior experience, such as carbon crediting (including the CDM), subnational pilot ETS schemes, or energy efficiency certificate trading, helps build institutional readiness, MRV systems, and industry familiarity with carbon market schemes. China’s regional pilots provided the institutional and technical foundation for the national ETS, while India’s PAT scheme has helped build industry familiarity with trading-based compliance instruments. Rapidly growing economies such as Viet Nam and Türkiye are similarly using pilot phases and phased implementation approaches to build regulatory capacity and market readiness before full-scale ETS implementation.

3. CBAM as a major motivating force: External climate-trade dynamics, particularly the EU’s Carbon Border Adjustment Mechanism, are increasingly shaping ETS policy design across emerging economies. Türkiye and Viet Nam, both highly integrated into EU-facing manufacturing value chains, show the strongest CBAM-driven policy momentum toward ETS implementation. At the same time, CBAM is also influencing policy discussions in India and China by reinforcing the importance of domestic carbon pricing frameworks for maintaining export competitiveness and regulatory alignment with evolving global climate policy regimes. In this sense, CBAM has functioned as a “butterfly effect,” accelerating ETS development across multiple emerging economies.

4. Preference for intensity-based caps: Intensity-based caps have been preferred by most fast-growing economies where industrial output continues to rise and emissions have not yet peaked or plateaued. China’s national ETS, for instance, currently relies on benchmarks tied to output based intensity metrics, while India’s carbon market builds on the intensity-reduction logic of the PAT scheme. Similarly, policy discussions in Viet Nam and Türkiye indicate a preference for bottom-up mechanisms that accommodate continued industrial growth during the early phases of ETS development. In such contexts, intensitybased caps are viewed as a way to balance emissions mitigation with economic growth. While absolute emissions may continue to increase as output expands, the policy focus remains on improving emissions intensity per unit of output, rather than “constraining” production itself. This approach applies particularly during the initial phases of their ETSs. Absolute caps are often perceived as politically and economically challenging in these developmental contexts, given concerns around industrial competitiveness and economic growth.

Across all four economies, the reliance on intensity-based caps during early phases reflects their broader developmental trajectories. However, China’s expected transition to an absolute cap beginning in 2026, aligned with its anticipated emissions peak, illustrates a potential pathway for other emerging economies as they approach emissions plateauing and greater economic maturity.

Table 1 provides a structured comparison of the policy approach, design features, and institutional arrangements of the four ETSs. It highlights how each country differs in terms of cap setting (rate- or intensity-based vs. cap-based), sectoral coverage, allocation methods, MRV readiness, use of offsets, participation of financial actors, and institutional design. Overall, the table helps situate domestic ETSs within a broader international context, while illustrating the developmental trajectories and reform pathways of ETS frameworks across the Global South.

| Parameter | India | China | Türkiye | Viet Nam |

|---|---|---|---|---|

| Carbon market description and status | CCTS (compliance mechanism + separate voluntary credit market); compliance mechanism operational since 2025 | National ETS operational since 2021 (covering the power sector), building on seven regional pilots in operation since 2013 that cover sectors and entities not included in the national system; domestic crediting mechanism also in place | Draft ETS law and pilot design under development, with a launch targeted for 2025-2026 | ETS under preparation; pilot launched in 2025, with the market expected to become fully operational in 2029; domestic crediting mechanism also planned |

| Coverage | Aluminum, iron and steel, chlor-alkali, pulp and paper, textiles, petrochemicals, petroleum refineries, cement, fertilizers | Power sector; expansion to steel, cement, aluminum, and other industrial sectors scheduled | Expected to cover energy-intensive industries (pilot phase to cover EU CBAM-exposed sectors) | The pilot covers electricity, iron and steel, and cement (two EU CBAM-exposed sectors); expansion is expected to cover additional industrial sectors, followed by waste, buildings, and agriculture |

| Cap setting | Intensity - (rate)-based | Intensity-based; transition from intensity- to absolute cap is expected | Intensity-based | Intensity-based |

| Allocation approach | Free, output-based benchmarking (tCO2e per unit of output), based on sector-specific GHG emissions intensity trajectories | Free, actual output-based benchmarking (OBA) (tCO2/MWh), differentiated based on power plant capacity and fuel source; auctioning expected to be introduced gradually | Free, benchmarking (tCO2e/output) | Free, benchmarking (tCO2e/output) |

| MRV system status | Detailed and standardized MRV framework under CCTS, with fuel- and activity-based monitoring, accredited third-party verification, and mandatory annual reporting to the Bureau of Energy Efficiency (BEE) and State Designated Agencies; further harmonization and digital integration underway | Highly mature and centralized MRV framework with sector-specific guidelines, mandatory monitoring plans, frequent (monthly) reporting, and provincially organized verification under monitoring, evaluation, and enforcement oversight; continuously refined since 2013 | Well-established, EU-aligned MRV system with annual reporting and accredited third-party verification, covering ~50% of national emissions and operational since 2015 to underpin the upcoming ETS | MRV system under development with international support |

| Offsetting use and eligibility | Currently no; provision to allow the use of credits to meet compliance obligations | Yes (5%); covered entities can use CCERs generated from projects not covered by the national ETS for up to 5% of their verified emissions | Yes, post-pilot (10%); domestic credits are expected to be allowed up to 10% of surrender obligations after, but not during, the pilot phase | Yes (planned); domestic credits are expected to be allowed, including from agriculture, forestry, and other land use and renewable energy; credits from domestic and international sources, including the Clean Development Mechanism, the Joint Crediting Mechanism, and the Article 6.4 Mechanism of the Paris Agreement, are likely to be permitted for compliance within defined thresholds (up to 30%) |

| Parameter | India | China | Türkiye | Viet Nam |

|---|---|---|---|---|

| Participation of financial players | No; financial intermediaries or traders are not permitted under CCTS | Currently no; only compliance entities can participate; financial players are expected to be allowed in a future phase (the Ministry of Finance published an interim policy that categorizes only purchased allowances, and not those received for free, as assets in financial statements) | Likely; the government is exploring participation by financial players | Unclear; decision remains pending; phased inclusion is possible |

| Banking and borrowing | Unlimited banking of credits; no borrowing | Limited borrowing allowed (2021-2022); banking initially unrestricted, later capped based on sales-linked limits | Allowed (10-year validity) and right to borrow | Banking allowed during the pilot (until 2030); borrowing allowed up to 15% of current obligations |

| Institutional design | BEE, under the Ministry of Power, functions as the regulator; the Grid Controller of India and the Central Electricity Regulatory Commission serve as the registry and market trading regulator; institutional architecture is evolving, with the National Steering Committee for the Indian Carbon Market acting as the apex governance and oversight body, providing strategic guidance on market design, targets, rules, crediting, and overall implementation to BEE | Mature multi-tier administrative system with provincial authorities, involving three levels of government | Ministry of Environment, Urbanization and Climate Change is responsible for overall ETS management and chairs the multi-ministerial Carbon Market Board, which acts as the high-level decision-making body for the ETS; Energy Exchange Istanbul serves as the market operator; the Energy Market Regulatory Authority regulates market compliance | Ministry of New and Renewable Energy is responsible for regulatory development, governance, while the National Registry, while the Hanoi Stock Exchange will operate the carbon exchange; the Ministry of Finance oversees financial governance and market stability rules |

Carbon credits, as opposed to emission allowances (sometimes also referred to as credits, for example under the Indian CCTS compliance scheme, for example), generally refer to units generated from carbon crediting mechanisms that are either government-regulated or privately managed, but participation in related market activities is always voluntary, whether on the supply or demand side (see Figure 1).

Carbon credit markets have major potential to enhance the effectiveness of countries’ mitigation efforts, in addition to providing flexibility for ETS participants.10 Domestic carbon credits that originate outside the scope of ETSs, as well as international carbon credits that meet specific accounting criteria, can play this role. This section reviews developments in this space and draws lessons from two emerging economy contexts, Colombia and South Africa.

Currently, two-thirds (a total of 24) of operational ETSs allow use of carbon credits toward compliance, either fully or partially, with the shares ranging from a few percent to, in theory, 100% (World Bank 2025a; ICAP 2025a).

The share of carbon credit retirements for compliance purposes globally reached 24% in 2024, with the remainder used for voluntary claims (World Bank 2025b).11 This share equated to approximately 60 MtCO2 e, which remains a minuscule amount when compared to emissions capped under compliance schemes globally, such as the EU ETS cap, which in 2024 totaled nearly 1.5 GtCO2 e (ICAP 2026b). However, with the new ETSs on the horizon, these volumes can be expected to grow.

As of mid-2025, there were 33 government-regulated crediting mechanisms and a further 11 under development or consideration worldwide (World Bank 2025a). Issuances from these mechanisms in 2024 constituted only approximately 10% of total credit issuances globally (World Bank 2025b).

Most existing ETSs that allow offsetting for fulfilling participants’ compliance obligations currently permit only domestic credits. In addition, internationally transferred mitigation outcomes (ITMOs) are already accepted by some carbon pricing compliance schemes (for example, Switzerland, South Korea, and Singapore) and are being explored in others (see Section 6 for a discussion of ITMOs).

Among emerging economies, Colombia and South Africa have gained experience in integrating domestic and international credits into domestic compliance schemes. Both currently have a carbon tax in place, and Colombia is also operationalizing an ETS.

5.1 Colombia

Colombia’s carbon tax was first established in 2016 to comply with the country’s commitments under the Paris Agreement. Prices have ranged between US$5 and US$7. Under the Carbon Tax Exemption Mechanism established the same year, compliance entities were initially allowed to offset up to 100% of their tax obligations with CDM or VCM credits from projects hosted in Colombia. The tax regime currently limits the use of offsets to 50% and plans to decrease this to 30%. Once operational, Colombia’s ETS will allow up to 10% of participants’ compliance obligations to be fulfilled by carbon credits (ICAP 2026c).

Colombia’s experience with offsetting has delivered important lessons for its carbon tax and ETS:

• Successes: Among the positive outcomes, the offsetting provisions created one of Latin America’s most dynamic carbon markets – with cumulative use of offsetting credits totaling 121 MtCO2 e as of March 2025 (Ministerio de Ambiente y Desarrollo Sostenible de Colombia 2025) – contributed to national MRV capacity and registry system development, and strengthened coordination and cooperation between the country’s Ministry of Environment and Ministry of Finance.

• Challenges: These have included market volatility due to changes in fuel demand and tax rates, as well as an initial supply constraint for domestic credits, which led the regulator to allow a six-month window for accepting international (i.e., hosted outside Colombia) credits. This, in turn, resulted in low prices and created administrative complexities for the government. Finally, high shares of offsets have also led to lower tax revenues.

5.2 South Africa

A carbon tax has been in place in South Africa since 2019 as the main instrument to support the country’s NDC and long-term decarbonization targets. The nominal tax rate initially stood at approximately US$6, but various discounts, including a free allowance component, reduced the effective rate. The related Carbon Offset Administration System provides further flexibility for tax-liable entities. The country previously allowed 5% offsetting, but this will increase to 10% (for fugitive and process emissions) and 15% (for combustion emissions) from 2026. At the same time, the carbon tax rate is being gradually increased to approximately US$27 in 2030.

As a result, demand for carbon credits has been growing. Eligible offsets must be hosted in South Africa, and projects must fall outside the scope of the tax. A total of 18.6 MtCO2 e worth of credits have been retired as of 2024 (Sa, Shezi, and van der Hoven 2025). The number of projects remains limited, however, and demand is expected to outstrip supply for the foreseeable future. In addition, one project currently supplies more than 80% of credits. South Africa does not currently have a purely local standard, although a domestic framework has been under development, and the country has sought to encourage greater diversity of projects by broadening the scope of eligible activities, specifically by granting more international VCM standards domestic standard status.

Lessons learned from the South African experience include:

• Mitigation beyond the cap: Allowing offsetting can incentivize the development of local crediting projects.

• Market concentration poses challenges: Markets with a limited number of large compliance entities – with one taxpayer in South Africa purchasing approximately 70% of all credits – combined with a small number of crediting projects create a concentration risk that must be carefully managed by the government. Establishing a local credit standard can be a tall order in most economies due to the scale required for such standards to become self-sustaining. A possible solution is to allow global standards to qualify for local standard status, provided that they meet domestic quality and other eligibility criteria.

Credits generated under Article 6 rules and traded internationally as ITMOs have the potential to play a major role in compliance markets if integrity is ensured. This section examines these prospects and related early experiences.

Historically, the CDM was a major source of offsetting credits for the EU ETS in its phases 1-2, but the EU largely discontinued this option in 2013. The discontinuation was influenced by concerns over the quality of the credits, specifically related to additionality and the conservativeness of baselines (see, e.g., Michaelowa et al. 2019; Luomi, Bosse, and Sergeeva 2025). Paris Agreement Article 6.2 and 6.4 rules and standards now build on these lessons, with the specific aim of supporting countries’ NDC achievement, and with environmental integrity, transparency, robust accounting rules, and avoidance of double counting as the core principles of Article 6.2.

Some countries have already communicated their intention to use ITMOs toward domestic mitigation policies or target achievement: Switzerland allows the use of ITMOs by motor fuel importers for compliance under its CO2 law, and Singapore intends to use ITMOs toward its 2030 NDC (Article 6 Implementation Partnership 2025). The EU has not yet confirmed whether ITMOs would be eligible for offsetting in the EU ETS but has confirmed that ITMOs could be used toward its 2040 mitigation target achievement (European Union 2025).

For emerging and developing economies, the question of whether to allow ITMOs for domestic target achievement or carbon market compliance purposes is complicated by the fact that many of these countries still perceive themselves as potential suppliers of ITMOs rather than buyers. For instance, while Colombia’s carbon tax mechanism is, in principle, able to receive ITMOs toward compliance, the country has also simultaneously been exploring ITMO sales (Giraldo, Bassi and Castellano 2025).

For more industrialized economies, where lower-cost mitigation options are becoming scarce, the equation is more straightforward. South Korea and Japan, for example, view themselves clearly on the buyer side and are planning to allow ITMOs for use toward compliance in their national ETSs (IETA 2025).

6.1 Japan

In the case of Japan, ITMOs are expected to play a major role in providing flexibility and cost-effectiveness for the country’s mitigation efforts and its ETS. Japan’s mandatory ETS will begin in 2026, covering 60% of the country’s emissions. Japan is estimated to generate compliance demand of 60 million tonnes of credits annually against a domestic supply of less than 1 million tonnes. Due to this imbalance, Japan has been investing in international partnerships, such as the Joint Crediting Mechanism (JCM), to bridge the gap. The ETS will allow domestic and JCM credits to be used for up to 10% of participating entities’ compliance obligations.

Lessons from Japan’s experience with the JCM include:

• Successes: Japan has effectively used the JCM not merely as a trading tool but as a vehicle for technology transfer. By deploying low-carbon Japanese technology in partner countries, Japan secures credits for its own compliance while supporting the host country’s development and mitigation efforts (since the credits are shared). As of late 2025, more than 200 JCM projects are either registered or under development in ASEAN countries, with Indonesia, Thailand, and Viet Nam accounting for the majority.

• Challenges: Based on the JCM portal, credits totaling only 817 ktCO2 e have been issued to date, mostly from small-scale projects (JCM 2025).15 The JCM experience implies that scaling up credit demand without a strong source of demand can be complicated. Other related challenges include a focus on a limited range of technologies, rigid governance, and the ownership of the credits resting with the government rather than private project developers or companies (e.g., Kondo 2023; JCM 2025).

6.2 Outlook

Globally, there are major opportunities and challenges for scaling up international crediting markets in support of countries’ NDC achievement and the effectiveness of their carbon compliance schemes. Article 6.4 has, to date, largely fulfilled expectations among the carbon market community as a quality benchmark for high-integrity projects and crediting. Significant developments have occurred in this space in recent years.

A challenge relating to Article 6.2, however, remains. Governments may, in principle, generate ITMOs from VCM credits if they deem these to be of sufficient quality by authorizing them for transfer as ITMOs. This carries a risk of undermining the quality of Article 6 credits.

Furthermore, a major challenge to the future credibility of international credit markets stems from past crediting systems where such high-quality standards have not been applied, which has undermined credibility and demand for credits. The first example was the CDM, and the second, more recent example involves credits issued by nongovernmental crediting programs (also known as independent, or VCM, standards).17 Experience has shown that trust in credit markets is easy to undermine and hard to regain.

In addition to ETSs and carbon tax regimes worldwide potentially serving as a source of demand for ITMOs, International Civil Aviation Organization's (ICAO) Carbon Offsetting and Reduction Scheme for International Aviation (CORSIA), which requires a corresponding adjustment for eligible credits (ICAO TAB 2024),18 is also expected to become a major source of ITMO demand. Discussions are also ongoing on the potential for ITMOs to qualify toward EU CBAM compliance, either on a tonne-to-tonne basis or, more likely, a price basis.

International cooperation in carbon pricing can take multiple forms, ranging from informal policy coordination and the harmonization of market design features to deeper institutional integration across jurisdictions. At the most advanced end of this spectrum lies the formal linking of ETSs, where allowances become mutually tradable across markets, effectively creating a larger and more integrated carbon market.

7.1 Theoretical Rationale for Linking Carbon Markets and Practical Challenges

From a theoretical perspective, linking ETSs can improve overall system efficiency through increased liquidity and cost-effectiveness (Beuermann, Hauptstock, and Them 2018). In theory, linking expands the pool of available allowances and abatement opportunities, enabling emissions reductions to occur where they are cheapest. This enhances economic efficiency gains while promoting price convergence across jurisdictions (Doda, Quemin, and Taschini 2019b; Santikarn et al. 2018).

Such flexibility is particularly valuable in allowing markets to adjust to varying economic and policy conditions while maintaining cost-effective emissions reductions. By equalizing carbon prices, linking can reduce carbon leakage, enhance market liquidity, and make aggregate abatement efforts more effective and affordable (Pyrka and Jeske 2024).

However, the number of successful ETS linkages remains limited. Existing examples, such as the EU-Swiss ETS linkage and the California-Québec system, have largely succeeded due to similarities in economic structures and political contexts (Ranson and Stavins 2015). Achieving such alignment across more diverse jurisdictions remains challenging.

A key constraint is the loss of regulatory autonomy, as governments may be reluctant to cede control over domestic carbon prices. Concerns also arise around free-riding, particularly if one jurisdiction adopts less ambitious targets to generate surplus allowances.

Differences in system design further complicate linkage. These include variations in cap-setting approaches, sectoral coverage, allowance allocation methods, price stability mechanisms, MRV systems, and institutional capacity for enforcement and coordination.

Jurisdictions may also face welfare losses due to terms-of-trade effects, namely, losses that arise when price convergence increases production costs and worsens trade competitiveness in initially low-price jurisdictions, particularly in regions exporting allowances. For instance, simulations of EU-China ETS linkage suggest that full linkage may result in welfare losses for China due to adverse competitiveness impacts, whereas restricted or partial linkage can mitigate these effects (Winkler, Peterson, and Thube 2021).

Additionally, exposure to economic shocks originating in partner markets increases perceived risks, further limiting political appetite for full integration (Santikarn et al. 2018).

7.2 Varieties of ETS Linkages

In practice, carbon market linkages can take multiple institutional forms, depending on the depth and design of cooperation.

Linkages may be bilateral or multilateral, involving two or more jurisdictions. They may also be direct or indirect: direct linkage occurs when one ETS accepts allowances from another, while indirect linkage involves recognition of units from a third system. For example, both the EU ETS and the New Zealand ETS initially allowed the use of certified emission reductions from the CDM and emission reduction units from Joint Implementation (Henderson, Meidan, and Hove 2022).

Article 6.2 of the Paris Agreement also accommodates ETS linkage by enabling the transfer of ITMOs across borders in support of countries’ NDC achievement. However, effective implementation requires robust accounting frameworks to ensure environmental integrity. Of crucial importance is accurate quantification of the “shift in emissions” resulting from linkage, namely, the redistribution of emissions due to cross-border trading. This is critical for applying accurate corresponding adjustments and preventing double counting (Schneider, Claudius, and La Hoz Theuer 2018).

Linkages can further be classified as complete or restricted, depending on whether mutual recognition of allowances is unconditional or subject to limits (Jiang et al. 2022). Finally, they may emerge through top-down approaches, such as international frameworks (e.g., under the United Nations Framework Convention on Climate Change), or bottom-up agreements between jurisdictions (Green, Sterner, and Wagner 2014).

A more gradual pathway, often described as “linking by degrees,” involves aligning rules, price levels, and design features over time. This incremental approach can help mitigate adverse terms-of-trade effects. These effects, driven by asymmetric cost pass-through and trade adjustments, may offset gains from allowance exports and lead to uneven welfare outcomes (Santikarn et al. 2018).

7.3 Linking in Practice: Lessons From Existing Models

Insights from real-world experiences highlight how some of the challenges described above can be addressed in practice. Systems such as the EU-Swiss ETS linkage and the California-Québec model demonstrate that stable integration is possible through regulatory alignment, harmonized rules, shared infrastructure, and coordinated governance.

The California-Québec system, in particular, illustrates how deep linkage can be achieved through shared auctions and fully fungible allowances (Burtraw et al. 2013). At the same time, ongoing negotiations, such as those between the EU and the UK, underscore the complexity of aligning cap ambition, legal frameworks, and market stability mechanisms (López Hernández and European Parliamentary Research Service 2025).

These experiences highlight that partial or restricted linkage arrangements can offer a pragmatic middle ground. By limiting the extent of allowance fungibility or introducing quantitative restrictions, jurisdictions can capture some efficiency gains while retaining greater control over domestic carbon prices and managing distributional impacts. Such hybrid approaches may be particularly relevant in early-stage or heterogeneous markets where full integration remains politically or institutionally unfeasible.

Looking ahead, designing carbon markets with linkage in mind from the outset, often referred to as “designing for linkage,” can reduce future integration frictions. This is especially relevant for emerging economies, many of which are adopting intensity-based ETSs aligned with development priorities. Notably, there are currently no examples of intensity-based ETSs being formally linked to other systems.

In this context, “soft linkage” approaches, such as harmonizing registries, MRV standards, and accounting frameworks without enabling full allowance trading, offer a pragmatic pathway as an intermediate step. By embedding compatibility in core elements, such as data systems, governance structures, and regulatory frameworks, these approaches can help build institutional credibility, regulatory trust, and technical readiness, while reducing long-term transaction costs and enabling smoother transitions toward deeper forms of integration as markets mature.

7.4 Beyond Market Linkage: Issue Linking and Broader Cooperation

Beyond formal ETS linkages, cooperation can also take broader forms through “issue linking,” which connects carbon pricing to trade, investment, and technology transfer frameworks (Melchor and Shaparia 2024).

A topical example is the potential use of Article 6 credits in relation to the EU’s CBAM. While the current framework recognizes only explicit carbon prices paid in the country of origin, discussions are ongoing on whether internationally transferred mitigation outcomes could be indirectly recognized in the future (European Union 2025; Gualandi2026).

Article 6.8 of the Paris Agreement further provides a “safe space” for nonmarket approaches, enabling flexible cooperation beyond tradable carbon units. Instruments such as green investment treaties or Just Energy Transition Partnerships illustrate how countries can exchange market access for decarbonization investments.

In this context, “exchanging market access for decarbonization investments” refers to arrangements in which preferential trade access, finance, or technology is provided in return for verifiable investments in low-carbon infrastructure. These may include improved export conditions, access to capital, or participation in long-term procurement arrangements for green goods.

In practice, such cooperation can extend beyond tariff preferences to encompass guaranteed demand mechanisms and strategic industrial partnerships. For instance, an advanced economy could provide preferential import access or long-term offtake agreements for green steel in exchange for investments in hydrogen-based direct reduced iron production and supporting renewable energy infrastructure in an emerging economy. Structured under cooperative frameworks aligned with Article 6.8, such arrangements can complement carbon market mechanisms by aligning trade incentives with long-term decarbonization pathways.

Such approaches are particularly relevant for emerging economies, where development priorities may constrain near-term climate action. Given the growing share of global exports from developing countries, market access can serve as a powerful lever for decarbonization when embedded within equitable cooperation frameworks (World Bank 2023; UNCTAD 2024).

By linking climate action with broader economic incentives, these approaches move beyond cost efficiency toward fostering innovation, technology diffusion, and more balanced participation in global green value chains.

Taken together, these developments suggest that the future of international carbon market cooperation is likely to extend beyond formal linkage toward a more diverse ecosystem of hybrid arrangements. Combining market-based carbon pricing instruments with trade, finance, and technology partnerships offers a more flexible and politically feasible pathway for scaling global climate action in a fragmented policy landscape marked by varying levels of climate ambition, capacity, and development priorities.

Over the past decade, ETSs have emerged as one of the most effective market-based instruments for achieving decarbonization across economies. As countries seek optimal ways to reduce emissions and accelerate low-carbon technology transitions in line with their NDCs and in support of the collective goals of the Paris Agreement, ETSs will increasingly be viewed as important tools for supporting cost-effective emissions reductions. This is particularly the case in a global context that has the potential to be increasingly shaped by border carbon adjustment mechanisms.

Undoubtedly, the most defining characteristic of ETSs is their compliance-based nature. Unlike voluntary carbon markets, participation in ETSs is mandated by regulation, with covered entities required to surrender allowances equivalent to their verified emissions. This regulatory obligation anchors demand for allowances and underpins the credibility and environmental integrity of the system. As a result, ETSs function not only as price-discovery mechanisms but also as enforceable policy instruments that translate national emissions targets into binding mitigation obligations for regulated sectors, thereby contributing to the achievement of broader global climate goals.

Considering the context of emerging economies specifically, the strength of ETSs lies in their versatility and ability to provide a degree of flexibility in how, when, and where emissions are reduced. As market-based mechanisms, they allow countries to tailor design features to political economy contexts, stages of economic development, and growth priorities. However, ETS effectiveness depends critically on the interplay between design choices and national circumstances, with the former including the type and stringency of the cap, target-setting approaches, allocation methods, trading rules, and the treatment of offsets and voluntary credits.

These choices both interact with each other and with the various structural and dynamic factors unique to each ETS jurisdiction and can only be discovered via practical operations. At the same time, the success of ETSs depends on carefully balancing institutional readiness, stakeholder capacity, robust MRV systems, and adaptive governance.

Effective ETS implementation requires learning from historical experience and continuously refining system design to reflect evolving national circumstances, economic conditions, and policy objectives.

Going forward, the relevance of ETSs will extend beyond domestic emissions reductions. Their interaction with voluntary carbon markets, Article 6 mechanisms, and border carbon measures is expected to play a central role in shaping demand for project-based carbon credits. ETSs are therefore not only compliance instruments but also important drivers of investment in mitigation and removal activities, particularly in sectors outside direct regulatory coverage.

Drawing on comparative evidence from existing and emerging systems, three policy-relevant insights stand out:

1. Prioritize phased implementation over upfront optimization: ETSs in emerging economies function best when introduced as adaptive policy instruments rather than fully optimized systems from the start. Early-stage design choices, such as intensity-based caps, high levels of free allocation, and limited coverage, reflect pragmatic responses to economic growth imperatives, competitiveness concerns, and data constraints. Evidence from China, India, Türkiye, and Viet Nam shows that these features can facilitate political acceptance and institutional learning without necessarily precluding future ambition. Tightening benchmarks, expanding sectoral coverage, and transitioning toward absolute caps over time will allow systems to mature alongside improvements in data quality and administrative capacity.

2. Invest early and decisively in MRV and institutional capacity: Across all cases examined, robust MRV systems emerge as the single most critical prerequisite for ETS credibility and effectiveness. High-quality, entity-level GHG emissions data, supported by robust third-party verification, underpin compliance, market confidence, and informed regulatory adjustment. Countries that build on prior experience, for example, through local ETS pilots, CDM participation, or a national energy efficiency trading scheme, enter ETS implementation with a clear advantage. In contexts where MRV systems are still maturing, ETS pilots primarily function as learning tools, highlighting that credible carbon prices can only emerge once emissions data are reliable, rather than through adjustments to prices or auction design alone.

3. Use flexibility mechanisms cautiously and strategically: Using offsetting as an ETS flexibility mechanism can enhance cost-effectiveness and mobilize mitigation beyond ETS coverage if designed carefully. However, evidence from emerging economy contexts indicates that generous or poorly calibrated credit use risks weakening domestic mitigation incentives, reducing fiscal revenues, and increasing market concentration (when a small number of firms or projects dominate offsetting transactions). Similarly, while international cooperation and ETS linkage offer theoretical efficiency gains, practical implementation is constrained by political economy considerations and divergent ambition levels. A phased, bounded approach to offsetting, anchored in strong domestic mitigation incentives, and a system designed with future interoperability in mind, can offer a more resilient pathway.

Beyond design and sequencing choices, the long-term effectiveness of ETSs ultimately hinges on governance, credibility, and strategic integration with the evolving global carbon market architecture. Strong political leadership, reinforced by sustained and inclusive stakeholder engagement, is essential to establish legitimacy, manage distributional impacts, and maintain policy continuity over time.

While ETSs are inherently iterative and benefit from learning by doing, clarity around cap setting remains critical: experiences such as Korea’s illustrate that absolute caps can coexist with transitional flexibility while better aligning ETS trajectories with national emissions targets and burden-sharing objectives.

Looking ahead, the growing relevance of Article 6 mechanisms and ITMOs, alongside prospects for international ETS linkages, underscores the need for systems that are interoperable, environmentally robust, and resilient to trade and border carbon dynamics, particularly for trade-exposed emerging economies navigating an increasingly carbon-constrained global economy.

Fundamentally, no single ETS blueprint is suitable for all emerging economies. Effective systems are characterized by alignment with national climate and development objectives, strong institutional foundations, gradual scaling up of ambition, and continuous learning. As ETSs increasingly interact with trade policy, industrial strategy, and international carbon markets, early design and sequencing choices will shape not only emissions outcomes but also competitiveness, fiscal space, and long-term integration into evolving global carbon market architectures.

An ETS is a market-based mechanism that caps emissions and allows entities to trade allowances or credits. It is important for emerging economies because it enables cost-effective emissions reductions while supporting economic growth, particularly in contexts where development and industrial expansion remain priorities

ETSs in emerging economies tend to be phased, intensity-based, and initially limited in scope, reflecting the need to balance emissions reduction with economic growth. Over time, these systems evolve toward greater stringency, broader coverage, and improved market functioning.

Robust MRV systems ensure data accuracy, transparency, and compliance, forming the backbone of credible carbon markets. Without strong MRV, carbon markets risk weak enforcement, low trust, and poor environmental outcomes.

Pilot phases and prior mechanisms help build institutional capacity, data systems, and market readiness. They allow policymakers to test design features and refine systems iteratively before full ETS implementation.

How can Carbon Markets Scale Durable Carbon Dioxide Removal in India?

Sustainable rice cultivation in India

Roadmap for a Net-Zero Power Sector in Gujarat

EU Carbon Border Adjustment Mechanism

Challenges to Deep-Decarbonization to Achieve Net Zero for India: A Review