Council on Energy, Environment and Water Integrated | International | Independent

Suggested Citation: Chaudhary, Megha, Saakshi Purohit, Manas Vijayan, and Bhawna Tyagi. 2026. What Drives Rooftop Solar Installation Decisions in Indian Homes? Understanding Household Decision-making Through a Pan-India Survey. New Delhi: Council on Energy, Environment and Water.

India's residential rooftop solar adoption is at an inflection point. The launch of Pradhan Mantri Surya Ghar: Muft Bijli Yojana (PMSGY) in February 2024 has nearly doubled the sector's growth rate from a CAGR of 45% to 85%, with more than 4 million households solarised as of May 2026. This report presents findings from the first-ever national consumer-side survey on residential RTS since the PMSGY launch, based on a survey of 17,094 households across 22 states and Union Territories. It traces the consumer journey from need recognition through perception, accessibility, and affordability to post-installation experience, identifying where dropouts occur and what targeted interventions can convert intent into action. The findings suggest that the greatest opportunity lies not in creating demand but in enabling action.

On 21 May 2026, India witnessed an all-time high peak electricity demand of 270.7 GW at 3.47 p.m., but the country’s renewable energy push helped it tide over the surge comfortably. Solar energy, including rooftop solar (RTS), alone helped tackle 22 per cent of the demand (National Power Portal 2026), highlighting its importance as a key pivot of India’s energy transition efforts. Within this sector, residential RTS is a significant focus area for the government in the pursuit of its Net Zero goal.

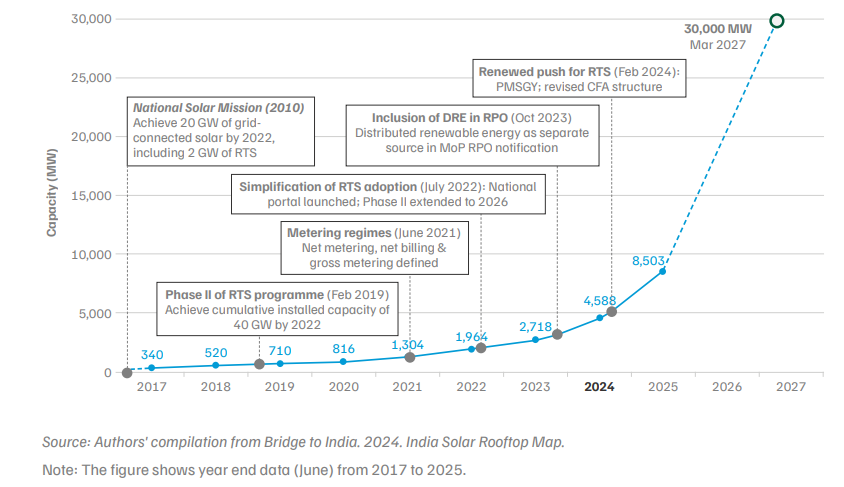

India’s journey in residential RTS adoption is at an inflection point. The launch of a dedicated scheme, Pradhan Mantri Surya Ghar: Muft Bijli Yojana (PMSGY), in February 2024 marked a decisive policy shift. It has helped nearly double the sector’s growth rate from a CAGR of 45 per cent in 2017-2023 to 85 per cent in 2024-2026 (Bridge to India 2024). As of 31 May 2026, PMSGY has received 6.9 million applications and 4 million households have been covered under the scheme. Currently 11.9 GW of capacity has been installed-nearly doubling the entire residential RTS capacity built over the preceding decade.

In absolute terms, the number of households solarised in India (4 million [National Power Portal 2026]), are also now comparable to Australia, a pioneer in residential RTS installation where 4.3 million households solarised over a span of 15 years (Australian Government 2026), even though Australia continues to lead in per capita RTS installations with approximately one in three equipped with RTS (Australian bureau of statistics 2025). To reach the 10 million mark by March 2027, India needs to sustain its current momentum to solarise 0.6 million households per month between June 2026 to March 2027 to reach the 10 million mark. At the same time, there can be an increased effort to diversify the adoption beyond the five states-Gujarat, Maharashtra, Rajasthan, Uttar Pradesh and Kerala, accounting for more than 71 per cent of national installed capacity.

Figure ES1. PM Surya Ghar Yojana nearly doubled the residential RTS growth rate

Nearly two-third of the households applying for RTS proceed to installation, showcasing that the PMSGY is performing well among those who start the journey (Ministry of New and Renewable Energy 2026). The priority now should be to widen the pipeline by reducing the drop outs occurring at every stage of the RTS adoption journey. Our analysis suggests that the dropouts occur in households facing information, procedural, and financial challenges.

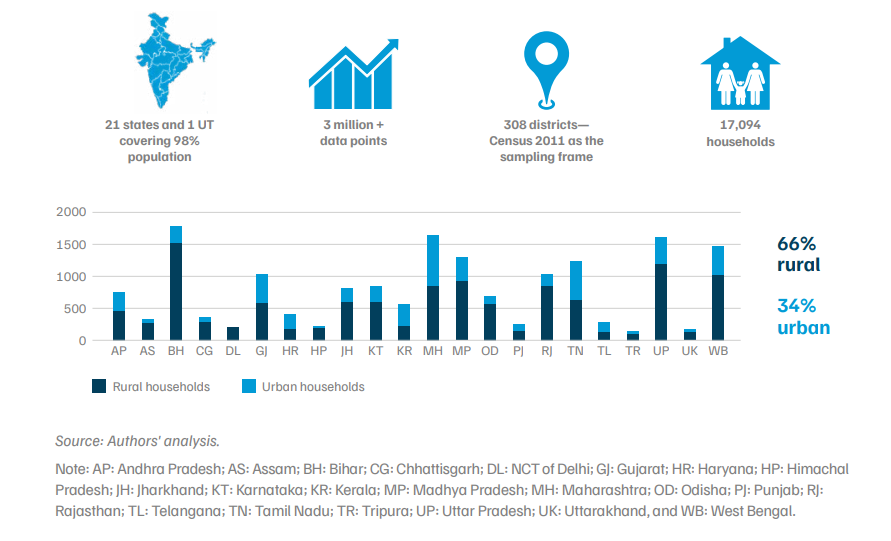

This report-the first-ever national consumer-side survey on residential RTS since PMSGY launch, is an attempt to understand the bottlenecks currently hobbling its expansion and suggest ways to overcome the challenges. Based on a survey of 17,094 households across 21 states and 1 union territory (UT), it set out to answer four questions:

To answer these questions, the study adopts a consumer journey framework, tracing the path from need recognition through perception, accessibility, and affordability, and to post-installation experience. The findings help frame stage-specific targeted interventions to reduce attrition rate.

Figure ES2. Survey highlights-21 states and 1 UT, 3 million+ data points

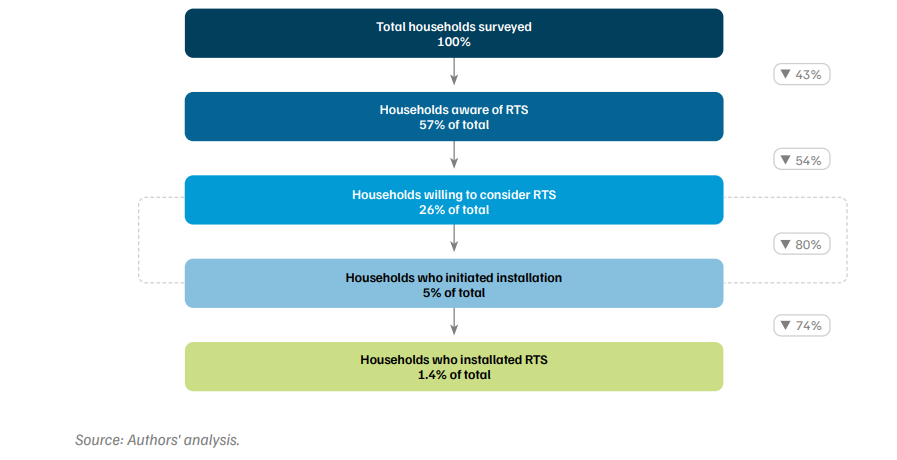

The findings of our survey suggest that the greatest opportunity in India’s RTS programme lies not in creating demand but in enabling action. The survey found that out of the 57 per cent who are aware of RTS, half (26%) were willing to consider RTS, 5 per cent initiated installation, with 1.4 per cent completing the process (Figure ES3). The drop between the journey of willingness to action reveals that insights and nudges from trusted sources can ensure continued momentum and adoption. The survey shows that awareness has significantly improved over the years but more targeted interventions can convert the intent into action.

Figure ES3. The willingness is high and the opportunity now lies in enabling action

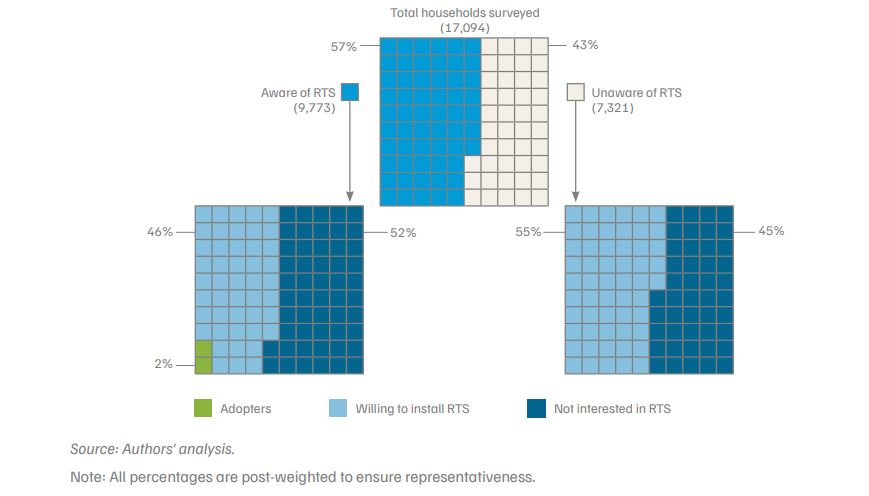

Figure ES4. Among households that were previously unaware, 55% reported being willing to adopt RTS

To sustain PMSGY’s momentum and convert demand into action, we structured targeted interventions around the five stages of consumer journey:

Residential rooftop solar helps households generate electricity at the point of consumption, reducing pressure on the grid while contributing to India's clean energy and Net Zero goals. During India's peak electricity demand of 270.7 GW on 21 May 2026, solar energy contributed about 22 per cent of the country's power needs.

Based on the survey findings, rooftop solar adopters in India are experiencing an average bill reduction of ~71 per cent, which amounts to more than INR Three Lakh savings in electricity bills over the lifespan of the system (25 years).

The report finds that the largest opportunity lies in helping households move from interest to action. Many households are aware of rooftop solar and willing to adopt it, but face challenges related to information, procedural complexity, trusted guidance, and financing awareness. Among all the households that are aware of residential rooftop solar, only 52 per cent are aware of the national scheme on RTS, Pradhan Mantri Surya Ghar: Muft Bijli Yojana.

The study was conducted through a telephonic survey of 17,094 households across 21 states and 1 union territory, representing 98 per cent of India's population, making it one of the largest consumer-focused studies on residential RTS conducted post PMSGY in India.

Current adoption is concentrated among affluent urban households with elevated electricity consumption. However, the study identifies substantial untapped demand across other household segments, alongside high satisfaction levels regarding electricity bill savings and overall rooftop solar performance across all categories.

Rooftop solar adoption is primarily facilitated by the PM Surya Ghar scheme, which offers capacity-based subsidies alongside low-interest, collateral-free financing for consumers requiring additional financial support. Additionally, a few states provide supplementary state-level subsidies and incentives to further accelerate adoption.

The survey highlights the importance of trust-based outreach and peer learning. Government departments are the most trusted source of information for 71 per cent of households, while over 90 per cent of adopters report positive experiences and 87 per cent are willing to recommend their vendors. Leveraging trusted institutions and satisfied adopters can help convert awareness into large-scale adoption.

Maximising Rooftop Solar Performance by Enabling a Robust O&M Ecosystem

Building a People-centric Energy Future:

Roadmap of the methodology to assess the climate co-benefits of the SUP ban in Tamil Nadu

Roadmap of the methodology to assess the climate co-benefits of the SUP ban in Maharashtra