Council on Energy, Environment and Water Integrated | International | Independent

Suggested Citation: Bagui, Debanjan, Prateek Aggarwal. 2026. Maximising Rooftop Solar Performance by Enabling a Robust O&M Ecosystem: A Multi-billion Market Opportunity in India’s Residential RTS Segment New Delhi: Council on Energy, Environment and Water

India’s residential rooftop solar (RTS) sector has experienced unprecedented growth in recent years. As of April 2026, the residential RTS installed capacity has exceeded 10 GW, with more than 60 per cent of the total capacity added since the launch of the PM Surya Ghar: Muft Bijli Yojana in 2024 (MNRE 2026; Gulia et al. 2024). Ambitious national targets, complemented by increasing electricity demand and supportive policy instruments, have enabled this growth. More than 3 million households across the country have already adopted RTS systems, while the target is to reach 10 million households (30 GW) by 2027 (MNRE 2024, MNRE 2026).

This expansion of distributed generation marks a structural shift in how electricity is produced and consumed at the household level. As installations scale up, ensuring that systems deliver their projected output consistently over their operational lifetime becomes central to preserving their economic and environmental value. Against this backdrop, the study is guided by four central questions:

India’s residential rooftop solar (RTS) sector has experienced unprecedented growth in recent years. As of April 2026, the residential RTS installed capacity has reached over 10 GW, with more than 60 per cent of the total capacity added since the launch of the PM Surya Ghar: Muft Bijli Yojana in 2024 (MNRE 2026, Gulia, et al. 2024). Ambitious national targets, complemented by increasing electricity demand and supportive policy instruments, have enabled this growth. More than 3 million households across the country have already adopted RTS systems, while the government aims to expand installations to 10 million households (30 GW) by 2027 (MNRE 2024, MNRE 2026).

This expansion of distributed generation marks a structural shift in how electricity is produced and consumed at the household level. As installations scale up, ensuring that systems deliver their projected output consistently over their operational lifetime becomes central to preserving their economic and environmental value. Against this backdrop, the study is guided by four central questions:

From the outset, India’s RTS policies, including the PM Surya Ghar: Muft Bijli Yojana, have rightly prioritised accelerating RTS adoption. However, post-installation maintenance and long-term operational performance remain areas where policy direction is still evolving. While residential RTS systems are generally considered low-maintenance, basic upkeep such as periodic cleaning, system diagnostics, and routine servicing are essential to ensure that they deliver their expected electricity output over time.

To better understand how maintenance is currently delivered in the residential RTS segment, we engaged with more than 60 RTS vendors across multiple states/Union territories (including Bihar, Delhi-NCR, Gujarat, Madhya Pradesh, Odisha, Rajasthan, Uttar Pradesh, and Uttarakhand) through structured surveys and one-on-one consultations. The consultations sought to understand the scope of services currently offered under the PM Surya Ghar: Muft Bijli Yojana, vendor practices around maintenance delivery, and the structural constraints affecting service provision.

The findings pointed out that although the PM Surya Ghar: Muft Bijli Yojana mandates five years of free maintenance, the scope of services and minimum frequency of visits are not clearly defined. As a result, maintenance delivery varies significantly across vendors, ranging from quarterly visits to once-a-year servicing. In many cases, service provision remains reactive, initiated only when consumers report system issues. Table ES1 summarises these findings.

Table ES1. Evaluating the operational realities of residential RTS maintenance services

| Theme | Prevailing market practice |

|---|---|

| Service awareness | Almost all vendors are highly aware of the five-year free annual maintenance contract (AMC) mandate; however, the actual scope of services delivered varies significantly across vendors. |

| Scope of maintenance service | Cleaning services are typically not included in free AMC provisions, which are largely limited to basic electrical and system health checks. Vendors generally provide guidance to consumers on recommended cleaning practices. |

| Cost structure | Most vendors report that the "free" five-year AMC is not actually free; costs are predominantly embedded in the initial installation price. |

| Service frequency | Service delivery is predominantly reactive. Maintenance is mainly carried out at the consumer's request rather than through scheduled visits. |

| Paid AMC uptake | Consumer willingness to subscribe to paid O&M services after the initial five-year period remains limited, with most households expressing hesitation or indifference towards renewal. |

Source: Authors’ analysis

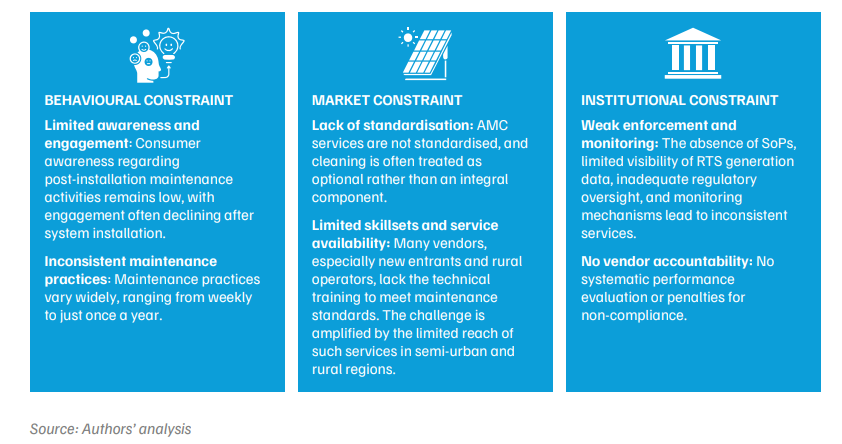

The findings suggest that maintenance remains a peripheral activity within the residential RTS ecosystem, shaped by a combination of behavioural, market, and institutional factors. Together, these factors create a system-level bottleneck that limits the realisation of the full economic and environmental potential of RTS systems (Figure ES1).

Figure ES1. From low consumer awareness to weak regulatory enforcement, systemic gaps hinder effective maintenance services

There is substantial evidence that regular maintenance is a crucial component in ensuring the long-term performance of solar systems (Abdulla, Sleptchenko, and Nayfeh 2024). Irregular maintenance practices can significantly reduce energy generation, accelerate system degradation, and compromise the long-term durability of residential RTS installations. Over time, this directly affects the financial viability of systems by eroding expected savings and shortening lifetimes. The implications extend beyond individual consumers to the entire RTS ecosystem (Figure ES2). To assess these implications at scale, the report models performance variance across five scenarios. These range from ideal system operation (15 per cent CUF) to extreme underperformance (3 per cent CUF). The analysis evaluates how deviations from projected generation output affect household savings, subsidy efficiency, discoms’ planning assumptions, and realised emissions outcomes.

Figure ES2. Financial implications of irregular maintenance for different stakeholders in the residential RTS ecosystem

The observed gaps in awareness, standardisation, and service consistency point not only to structural weaknesses but also a significant untapped market opportunity within the residential RTS ecosystem. As installation capacity is scaled up, the cumulative base of systems requiring periodic servicing is expected to grow rapidly, driving rapid expansion of an emerging economic opportunity.

Along with significant market opportunities, the O&M sector also holds strong employment potential. Considering national target of 30 GW RTS capacity, this could generate approximately 0.33 million (3.30 lakh) jobs in the O&M sector (CEEW, NRDC 2026).

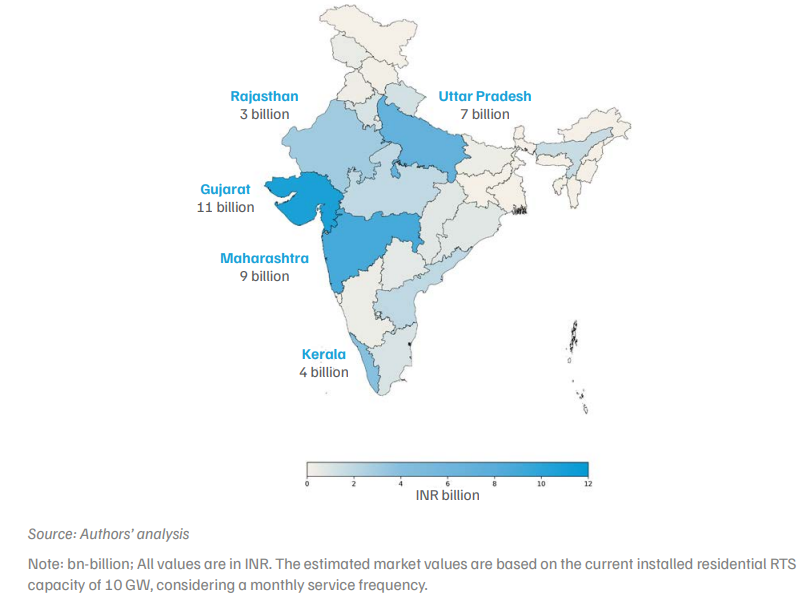

Figure ES3. More than 70% of the market opportunity for bundled maintenance services is concentrated in 5 states

While the multi-billion recurring O&M market presents a massive opportunity, it remains highly fragmented, unorganised, and lacks standardisation. As installations scale up from 3 million households to tens of millions, the structural gap is likely to widen unless service delivery becomes formalised. To institutionalise maintenance practices and to capture the economic value, the ecosystem must shift towards structured, tech-enabled business models. This report proposes two scalable frameworks to create an accountable maintenance ecosystem:

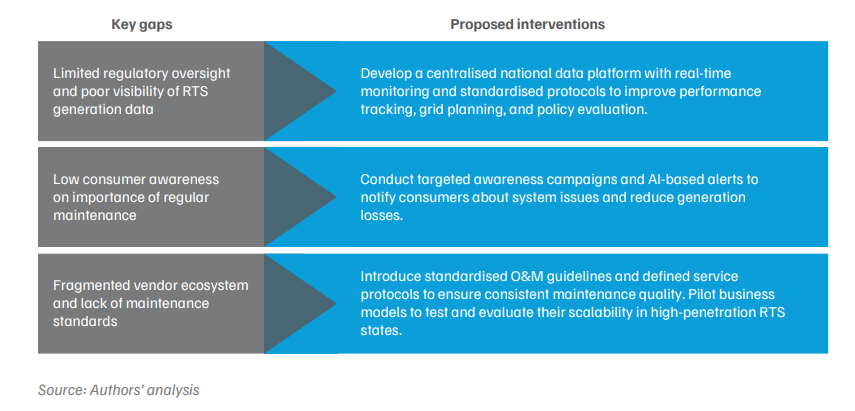

While the proposed business models can improve the accessibility, accountability, and standardisation of RTS maintenance services, structural gaps persist, including low consumer awareness and limited visibility of generation data. As India expands its RTS footprint, the focus must move beyond installation and capacity addition to prioritising sustained system performance as well. Figure ES4 presents a strategic roadmap outlining key steps to achieve this transition.

Figure ES4. Strategic roadmap for strengthening system performance in India’s residential RTS ecosystem

No, rooftop solar systems require minimal maintenance; periodic cleaning (Preferably biweekly) and basic inspections to ensure optimal performance are usually sufficient.

Schedule maintenance during early morning or near sunset to avoid disrupting generation. Clean panels using water and a soft microfibre cloth, preferably low-mineral water. Avoid abrasive cleaners or pressure washers, and do not climb or stand on panels.

A solar meter usually records your solar generation, but its installation depends on your state and electricity service provider. Additionally, a smart inverter can also track your solar generation and is generally connected to a mobile app via Wi-Fi for real-time monitoring.

What Drives Rooftop Solar Installation Decisions in Indian Homes?

Building a People-centric Energy Future:

Roadmap of the methodology to assess the climate co-benefits of the SUP ban in Tamil Nadu

Roadmap of the methodology to assess the climate co-benefits of the SUP ban in Maharashtra