Issue Brief

Greening New Pastures for Green Investments

Kanika Chawla, Arunabha Ghosh

September 2019 | Sustainable Finance

Suggested citation: Chawla, Kanika, and Arunabha Ghosh. 2019. Greening New Pastures for Green Investments. New Delhi: Council on Energy, Environment and Water.

Overview

This brief demonstrates that the energy transition in the countries in which energy demand is accelerating is constrained by availability and affordability of finance. It examines the demand for capital in emerging economies and their current political economy and investment landscape. Further, it discusses the evolving capital structures that can plug the gaps in these emerging markets. The brief also makes recommendations that would facilitate a robust energy transition.

Key Highlights

- In 2018, lower-middle and low-income countries housing well over 40 percent of the world’s population accounted for less than 15 percent of energy investment.

- Financing costs account for the largest component of renewable energy tariffs – between 50 and 65 per cent – in India. The share is even higher in other developing countries where the risk premium is higher.

- Renewable energy projects face both an availability and an affordability constraint. Several investors, especially those with limited risk appetites such as institutional investors, do not even consider investing in most developing economies.

- Risk perceptions are exacerbated by information asymmetry about progress made in clean energy. Accessible, reliable, and comprehensible data is necessary (but not sufficient) for creating deep markets and attracting investment.

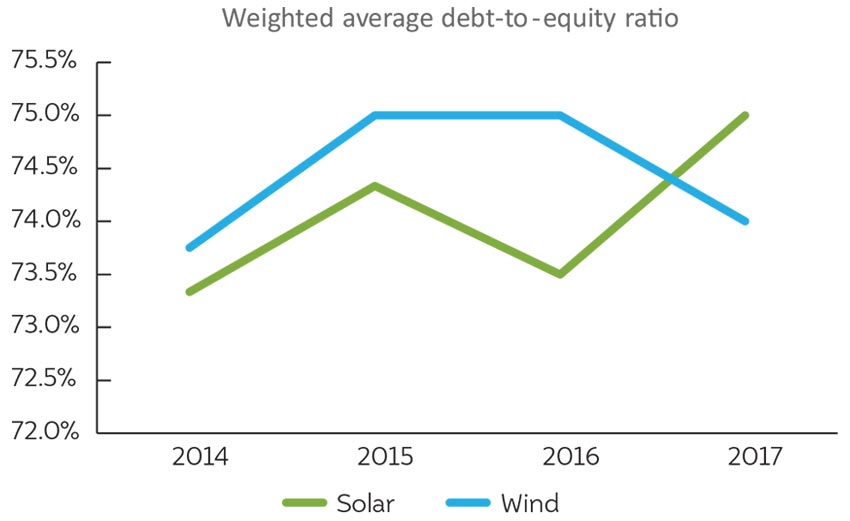

Shares of debt in capital structures for solar PV have converged with and even surpassed those for wind

Source: CEEW & IEA, Clean Energy Investment Trends: Evolving Risk Perceptions for India’s Grid-Connected Renewable Energy Projects, 2019

India scenario

- Meeting India’s clean energy commitments to the UNFCCC would require a tripling of investment flows. Investment flows in India have averaged around USD 10.3 billion over a five-year period ending 2018.

- The capital structure of wind projects has remained stable with debt-to-equity ratios averaging 75:25. But the share of debt has risen for solar PV, with more 75:25 structures in recent years.

- Interest rate spreads over bank benchmark lending rates also fell between 75 to 125 basis points for both wind and solar PV in India between 2014 and 2018. Loan tenures increased during the same period as lenders became more comfortable in extending longer term loans.

- Equity investors with access to favourable sources of finance have had more success in winning project capacity at competitive auctions. The share of top 10 firms was around 80 percent in both wind and solar projects.

Other developing economies

- Multiple interests and the complex governing mechanisms have heightened risks for investors in Indonesia, thereby constraining the growth of renewable energy investments.

- Sustained policy uncertainty, project execution delays, and political upheaval from 2015 to mid-2018 resulted in a major slowdown in the renewable energy sector in South Africa.

- However, major domestic market interest in scaling up renewable energy supply in South Africa. The drivers include domestic currency financing, bankable power purchase agreements, and certainty over demand growth.

Evolving capital structures

- A multi-risk and multi-country approach such as a Common Risk Mitigation Mechanism would reduce the exposure for any single country, investor or project developer.

- Grid Integration Guarantee (GIG) can indemnify solar and wind generators against loss of revenue due to the curtailment of renewable power from the grid.

- Green bonds would offer a useful complement to existing sources of debt capital for financing clean energy projects.

Key Recommendations

- Formulate a Climate and Clean Energy Finance Commission. The Commission will design a targeted plan for leveraging existing institutions and governance structures to address the accessibility and affordability of capital for the energy transition.

- Commence an Africa-India Clean Energy Co-Learnings Programme to facilitate business-to- business exchanges between leading players in emerging markets.

- Reduce information asymmetries between clean energy projects and prospective investors. The CEEW Centre for Energy Finance can play a major role as a non-partisan market observer and driver.

The Indian green bond market witnessed its first issuance in February 2015 and 27 green bonds have been issued by 18 issuers until May 2019, cumulatively amounting to USD 7.6 billion.