Council on Energy, Environment and Water Integrated | International | Independent

Suggested Citation: Chaturvedi, Vaibhav. 2021. Peaking and Net-Zero for India’s Energy Sector CO2 Emissions: An Analytical Exposition. New Delhi: Council on Energy, Environment and Water.

The study focuses on insights related to four alternative scenarios: 2030 peak–2050 net-zero, 2030 peak–2060 net-zero, 2040 peak–2070 net-zero, and 2050 peak–2080 net-zero. If 2050 were chosen as a net-zero year and if carbon capture and storage (CCS) technology were commercially unviable by then, this would imply that:

The key considerations in the selection of peaking and net-zero years should be the average per capita income, economic growth rate, a ‘reasonable’ pace of transition determined by the gap between peaking and net-zero years, the possibility of lock-ins and stranded assets, the cumulative emissions across the alternative peaking year–net-zero year combinations, and the economic trade-offs as presented here.

Emission mitigation is a key policy objective for policymakers in India and the world. In 2020, many countries and regions, including China, the European Union (EU), Japan, Korea, and the UK, announced their net-zero ambitions (Varro and Fengquan 2020; Croatian Presidency of the Council of the European Union 2020; Reuters 2020; The Government of the Republic of Korea 2020; The Government of the United Kingdom 2020). With President Biden in office, the US is also expected to announce 2050 as the target year for achieving net-zero emissions for the US economy if he follows through on his pledge (Birol 2021). The Paris Agreement calls for limiting the global temperature increase to “well below 2 degrees Celsius” relative to pre-industrial levels. This makes it imperative that the world as a whole and individual countries begin their transition to a ‘net-zero’ greenhouse gas (GHG) emitting economy as early as possible. Achieving this target implies a significant increase in the rate of reduction of global emissions, a challenge for many countries. This is especially true for low-middleincome and rapidly growing economies such as India, which need to address the development aspirations of their citizens while trying to reduce emissions simultaneously.

India is one of the fastest growing economies in the world. The per capita carbon dioxide emissions, 1.82 tCO2 in 2016, was much lower than the global average of 4.55 tCO2 (World Bank 2021). Owing to its population and size of the economy, India became the fourth highest emitter in 2017 (UNEP 2019). Because India’s emissions are expected to continue to increase, its emission mitigation strategy and targets are crucial in the global climate debate.

The IEA in its recently released India Energy Outlook explores the ‘net-zero’ question (IEA, 2021a). While this analysis is useful, it is constrained by the exploration of a single scenario, namely net-zero by mid-2060s. In order to inform this critical debate in India, it is important to present alternative scenarios and highlight the trade-offs among these. Moreover, the IEA report does not dwell either on the question of peaking year, or the character for such a net-zero future, with the key insights from the report mainly focused on intermediate years and required transitions in the next two decades on the path to achieving net-zero by mid-2060s.

While the world awaits India’s announcement on a netzero year, such a statement cannot be delinked with the choice of a peaking year. For developed economies already on a declining emissions trajectory, the peaking year is not a discussion agenda. However, for fast-growing economies with a rising emissions trajectory, the need to understand the key variables that impact the choice of a peaking year is as critical as the determinants for the choice of a net-zero year. The choice of a peaking year is implicit in India’s net-zero discussion, and the two need to be analysed together.

A crucial question is: Can India peak its emissions within the next couple of decades and then continue a net-zero trajectory? The analytical exposition in this brief aims to discuss the underlying variables that will impact India’s peaking year and the journey toward net-zero emissions. The numbers in this brief refer to India’s energy and industrial process-related carbon dioxide emissions, which accounted for 88 per cent of its total GHG emissions in 2016, including land use, land-use change, and forestry (Ministry of Environment, Forest and Climate Change 2021), and the implications and insights are essential for India’s consideration of a peaking year and net-zero target.

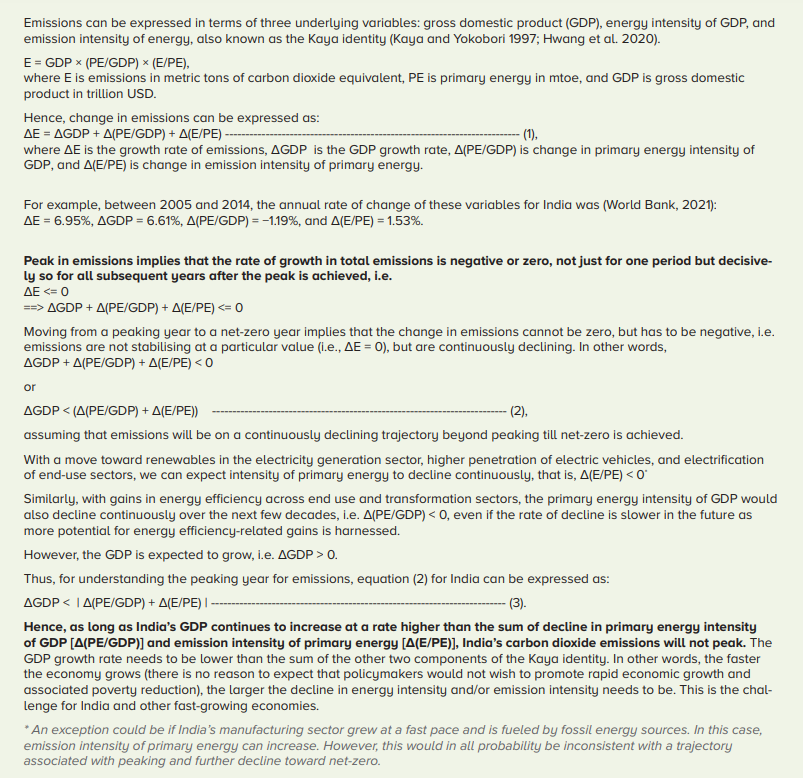

Box 1 presents an analytical exposition of the meaning of peaking emissions based on three underlying variables: gross domestic product (GDP) growth, rate of change in primary energy intensity of GDP, and rate of change of emission intensity of primary energy. The peak emissions can be explained by the combination of these three variables. For a growing economy such as India, the key insight from the analytical exposition is as follows:

As long as India’s GDP continues to increase at a rate higher than the sum of the decline in primary energy intensity of GDP and emission intensity of primary energy, India’s carbon dioxide emissions will not peak.

Box 1: A simple arithmetic expression to explain peak in emissions

The year for peak emissions and achieving net-zero is a policy choice. Here, we provide an overview of the following four alternative scenarios for India’s peaking and net-zero years: 2030 peak–2050 net-zero, 2030 peak–2060 net-zero, 2040 peak–2070 net-zero, and 2050 peak–2080 net-zero. Based on equation (3), as given in Box 1, we can determine the effort required for peaking as follows:

GDP growth rate − sum of decline in PE intensity of GDP and decline in emission intensity of PE = effort gap

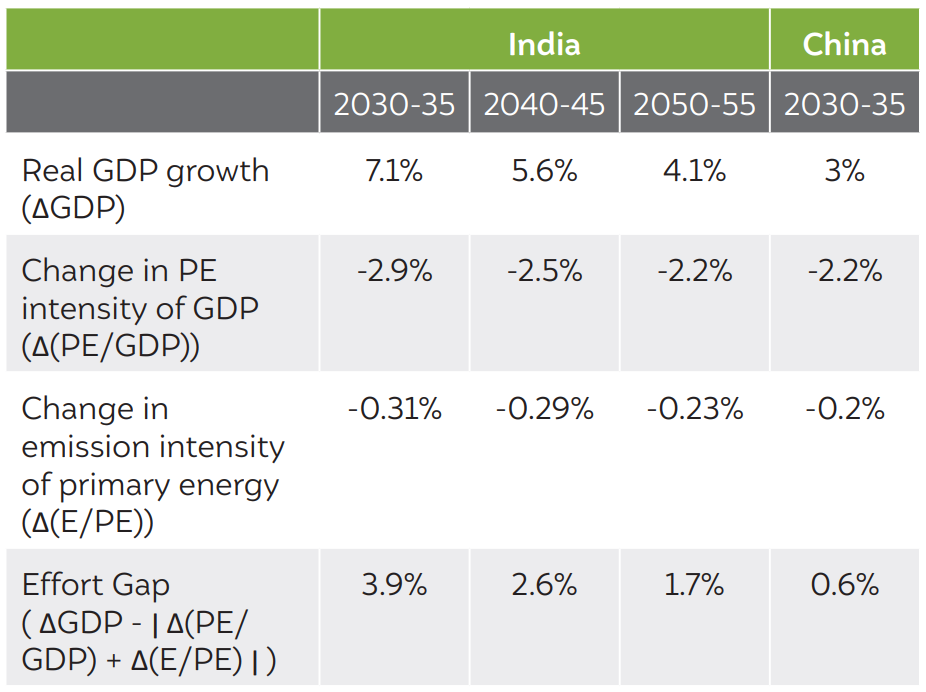

The higher the effort gap, the higher the effort required for emissions to peak. Table 1a lists our estimates for the gap in the reference scenario1 for the years immediately after the peaking year.

Table 1a Effort gap in the reference scenario

Source: Author's analysis

When could India’s carbon dioxide emission peak? If India chose to peak in 2030, then from the next year onwards, it would have to ensure that the combined rate of decline in the primary energy intensity of GDP and emission intensity of primary energy is higher than the GDP growth rate, and the effort gap would have to be bridged. Hence, it is clear from Table 1a that, with a natural decline in the GDP growth rate, the effort gap declines over time, and bridging this gap becomes easier in later years. However, if the peaking year is 2025, the effort gap would be even higher. Compared to India, bridging the gap after its peaking year is much easier for China, as its real GDP growth rate post-2030 is expected to be much lower and the per capita income is expected to be much higher. In other words, China aims to peak emissions at a much higher level of development.

If India chose to peak in 2030, then from the next year onwards, it would have to ensure that the combined rate of decline in the primary energy intensity of GDP and emission intensity of primary energy is higher than the GDP growth rate, and the effort gap would have to be bridged. Hence, it is clear from Table 1a that, with a natural decline in the GDP growth rate, the effort gap declines over time, and bridging this gap becomes easier in later years. However, if the peaking year is 2025, the effort gap would be even higher. Compared to India, bridging the gap after its peaking year is much easier for China, as its real GDP growth rate post-2030 is expected to be much lower and the per capita income is expected to be much higher.

Compared to India, bridging the gap after its peaking year is much easier for China, as its real GDP growth rate post-2030 is expected to be much lower and the per capita income is expected to be much higher. In other words, China aims to peak emissions at a much higher level of development.

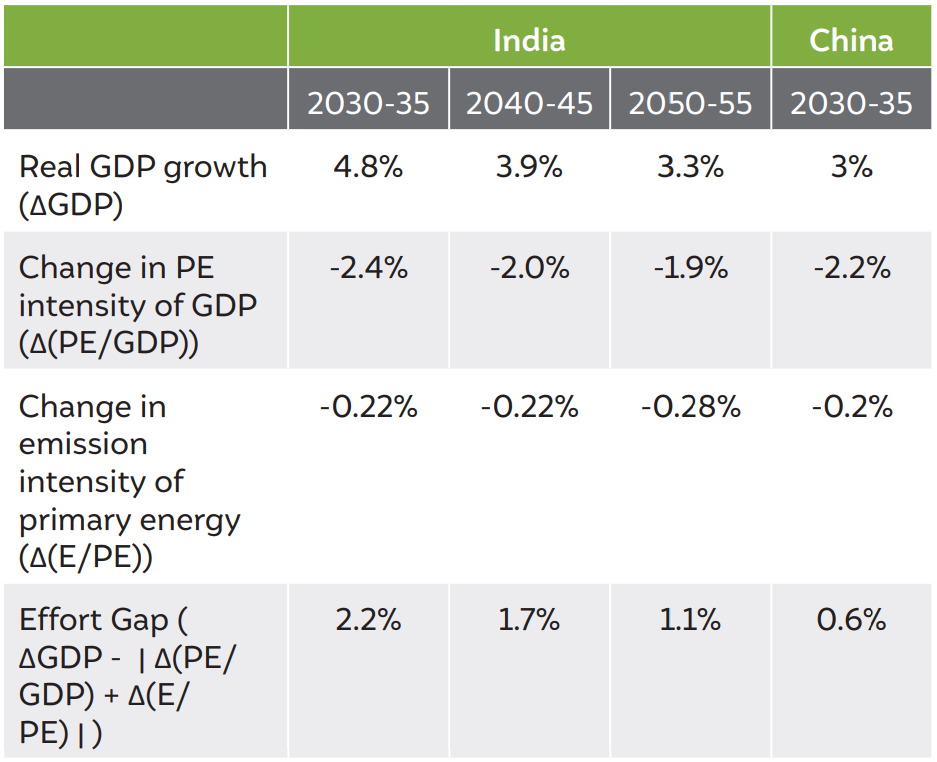

Table 1b Effort gap in the low GDP growth scenario

Source: Author's analysis

In a low GDP growth scenario, India’s effort gap would be lower (table 1b); however, it would still be much higher than China’s effort gap. The corresponding effort gaps for 2030–35, 2040–35, and 2050–55 are 2.2 per cent, 1.8 per cent, and 1.4 per cent, respectively, in India’s low economic growth scenario. The underlying economic growth assumption under the low economic growth scenario for India during 2015–50 is 4.54 per cent compound annual growth rate (CAGR) compared to 6.16 per cent CAGR for the reference scenario. The fluctuations in emissions intensity of primary energy and primary energy intensity of GDP reflect the numerous changes in these variables across various demand, supply, and transformation sectors hidden in the aggregate number presented here.

China has sustained a high GDP growth rate for more than three decades, resulting in high per capita income and the associated emissions. As the economy grows, the rate of economic growth is expected to slow down. Continued improvements in the emission intensity of primary energy and primary energy intensity of GDP, along with lower GDP growth rates, would allow it to peak its carbon dioxide emissions in the next decade. However, India’s case is different, mainly because of the higher GDP growth rate expected for the next few decades. Although significant progress has been made in terms of the growth in renewable energy penetration in the grid, electrification of the transport sector, and energy efficiency improvements in the buildings and industrial sector, the GDP growth effect will overpower these positive developments by a large margin for the next few decades if things continue to evolve as they have in the last decade, or along the BAU pathway.

The combination of a high GDP growth rate and a continuously declining energy efficiency improvement rate implies that the rate of decline in emission intensity of primary energy for India needs to be increased drastically to overcome the effort gap and push the peak to pre-2050. This essentially means fuel switching at a fast pace across sectors. Renewables would have to accelerate much quicker, electric vehicles would have to penetrate in a large way as early as 2030, and the industrial sector would need to move away from fossil fuels to electricity as early as possible. Energy efficiency improvements across sectors, while critical, along with high renewable energy share in the power sector, will not deliver the required shift in the peak before 2050.

A shift towards the manufacturing sector, as envisaged in the Make in India initiative, would make the transition across sectors, as discussed above, even more important as traditional manufacturing units are fossil-intensive and can negatively impact the rate of decline in emission intensity of primary energy. India needs to identify manufacturing sectors where electricity can be used as a fuel instead of fossil fuels, as well as reduce the cost of electricity to make this fuel competitive.

It should be noted here that bridging this gap is not just a matter of GDP growth. A key determinant of this effort is the cost-effectiveness of mitigation technologies and the favourable underlying societal conditions to adopt them. In general, if a mitigation technology becomes cost-effective, it would be available for all countries through diffusion. The market would ensure the rapid penetration of cost-effective technologies. This has been proven by the rapid global uptake of solar photovoltaic technology and the rapid increase in electric vehicle sales worldwide. Thus, we can expect that a similar mitigation technology suite is available worldwide at any given point in time. The required pace of deployment of these technologies for moving towards a net-zero world across different countries is determined by the speed of economic growth in these regions. Faster deployment of mitigation technologies to match the rapid economic growth would imply a need for rapid systemic changes and that all underlying societal factors vital for the transition align to ensure rapid systemic change. In mature economies with a slower pace of economic growth, several underlying systems assist the required pace of transition. This may not be true for emerging economies.

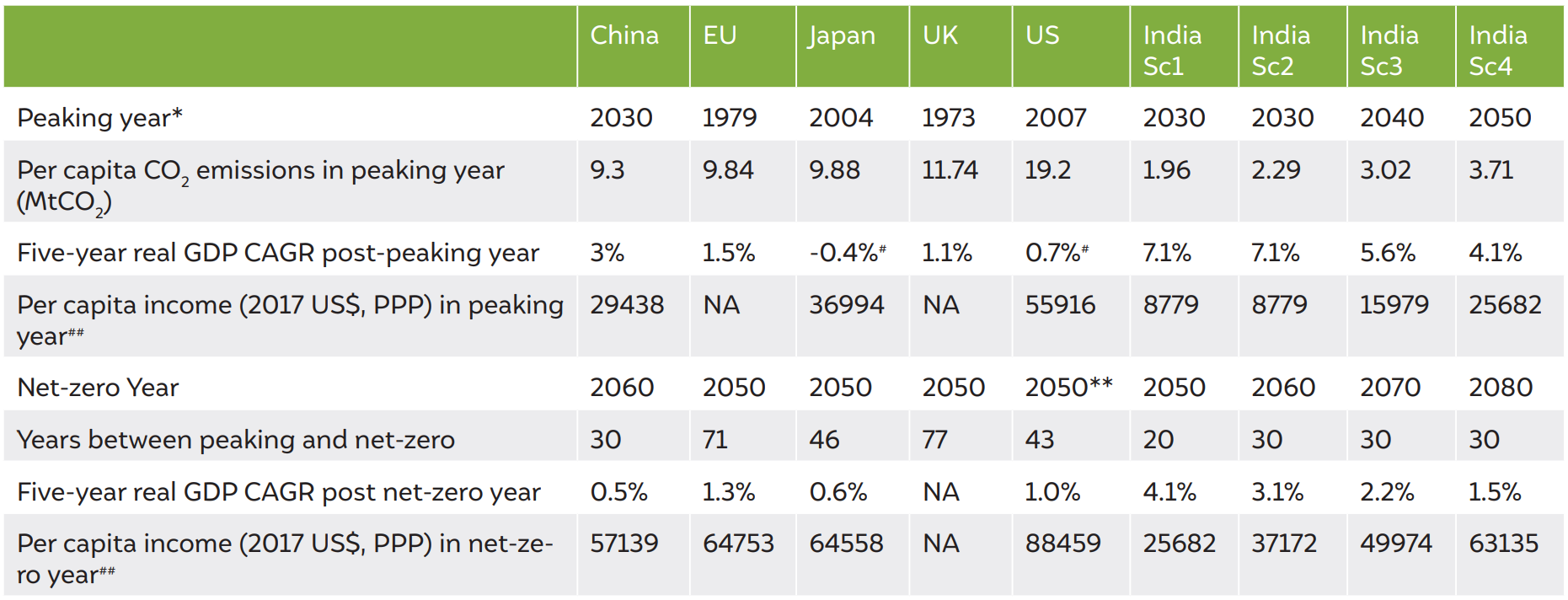

As discussed in the section above, the pace of the required transition is important and is determined by many variables. Table 2 presents a comparison of some countries that have announced their net-zero ambition with India’s potential scenarios.

Table 2 Comparison of some key variables for countries with net-zero ambition and India

Source: Author's analysis

Some key insights emerge from Table 2. First, the per capita emissions for all other economies, including China, are much higher than those of India, even if one assumes peaking for India in 2050. Second, India’s real GDP growth rate would be much higher than any other country after their peaking years, implying a much higher effort required by India to peak and subsequently reduce emissions. Third, India would have a much lower per capita income to support the transition, even if it began the transition in 2040. Finally, the gap between the peaking year and net-zero year has been long for most countries, signifying a pace of transition that reflects a relatively less disruptive impact on energy systems and the society.

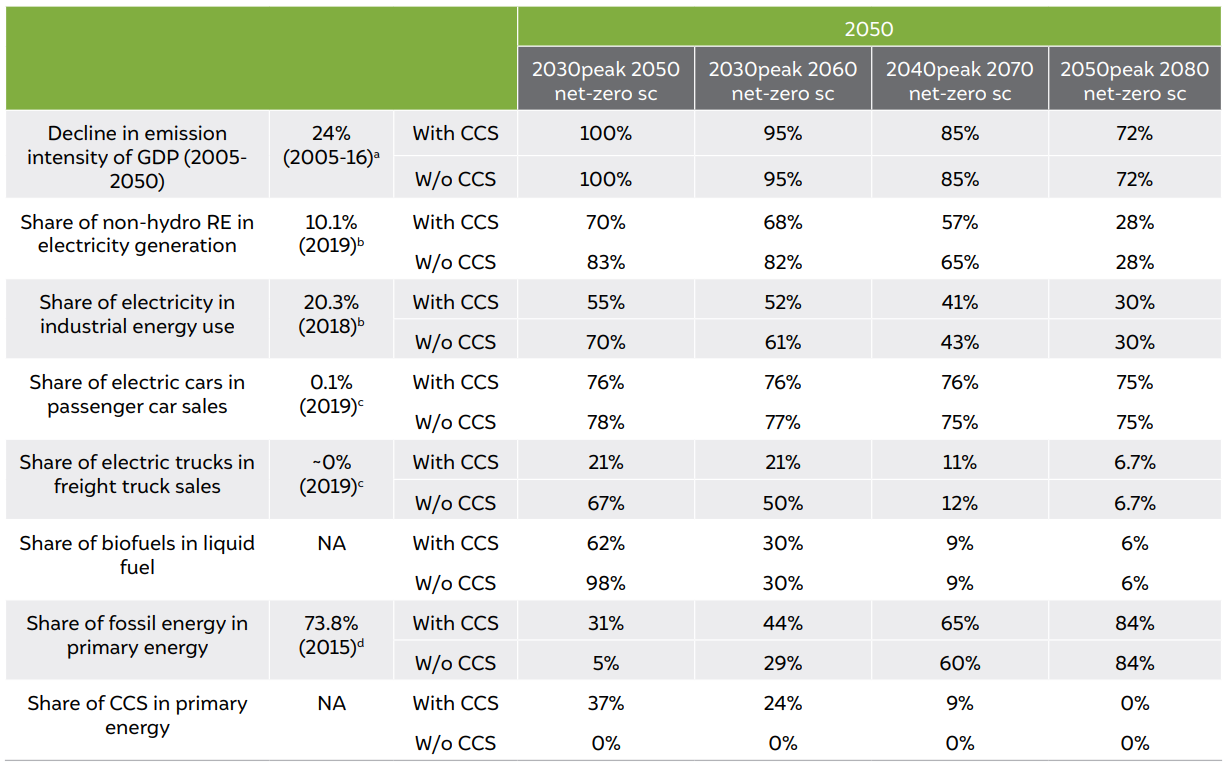

Irrespective of the challenges emerging from economic growth for the transition to a net-zero world, India needs to take decisive action to mitigate climate change. It needs to announce peaking and net-zero years urgently. However, it is not necessary to announce the peaking year. South Korea, for instance, has just announced a net-zero year, although it is unclear whether its emissions have peaked. Although India could follow a similar approach, it would not be the best strategy. A net-zero year as far as 2070 or 2080 would not push key economic actors to take decisive actions. The peaking year is a critical marker and provides a clear policy signal to various stakeholders. Table 3 presents some key indicators for the alternative peaking and net-zero scenarios discussed in this brief. These are presented for two alternative worlds, one in which carbon capture and storage (CCS) technology is available, and other in which the world does not rely on this technology. CCS is a controversial technology, and presents a perverse incentive (a sort of moral hazard) to not do much in the near-term. Progress on this technology has been very slow, although IPCC assessments (e.g. see IPCC, 2018) highlight the importance of this technology for deep decarbonisation.

Table 3 Key progress indicators across alternative peaking and net-zero year combinations in ‘with’ and ’without CCS’ scenarios

Source: Author's analysis

The critical variables discussed in earlier sections provide an overview of one of the most important challenges for the transition as a result of economic growth. Table 3 presents what this would mean across sectors. Clearly, the effort required is very high in scenarios with an early peak and a rapid decline. The table shows that availability, or absence, of CCS would define the shape of India’s energy systems, regardless of the choice of peaking and net-zero year. While there is progress on this technology, it is far from satisfactory. If this technology is not commercially available, India will have to largely get out of fossils in and beyond the net-zero year. Some fossil energy use (<5% in PE) could continue as it would be offset by bioenergy crops, which would act as a carbon sink. The share of other technologies like solar and liquid biofuels, and electrification of end-use sectors, would have to grow significantly in the absence of CCS. Electrification of industries as well as freight transport would have to happen much faster as oil and coal use would have to be phased out in the absence of CCS. Biofuels would have to play an important role, with or without CCS, although lack of availability of CCS would imply an even higher use of biofuels in India’s oil supply chain. Costs of hydrogen produced from renewable sources would have to fall drastically in the next decade for it to play an important role in the net-zero future. India might not have enough land to grow bio-energy crops, which has been a concern. But in the future net-zero world, liquid biofuel would be imported by India like oil is imported today. In such a scenario, biomass-rich regions like Brazil could replace the role of West Asia as the suppliers of liquid fuels.

Although the role of sustainable lifestyles has become crucial in the transition debate, rapid technological advances as described above need to be made to address the challenge of decarbonisation. However, this challenge must not ignore the reality of climate change.

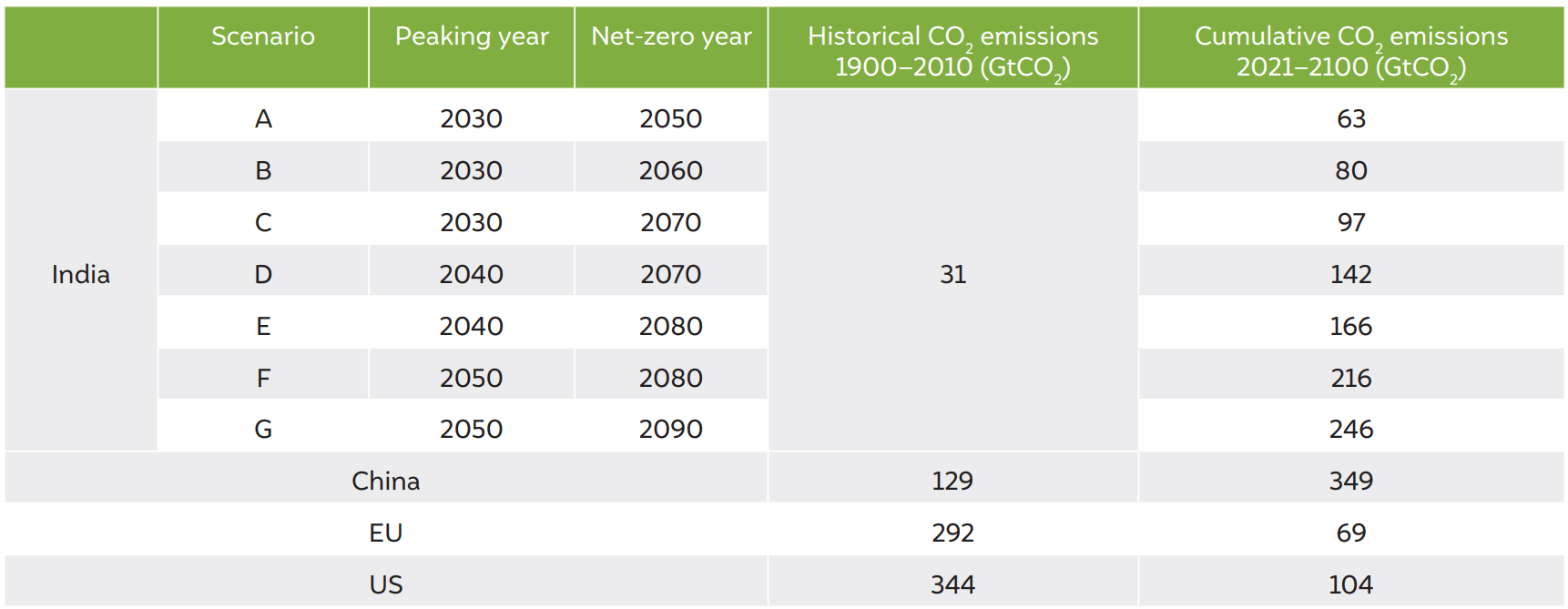

Delaying a peak in emissions would have a larger impact on climate change. Hence, it is critical that India does not wait until 2050 to peak its emissions. Postponing peaking and net-zero years will increase India’s climate impact, which needs to be minimised to the largest extent possible. Table 4 presents the estimates of India’s cumulative emissions to help us understand the comparative climate impact of these alternative scenarios.

Table 4 Cumulative emissions impact of alternative peaking and net-zero year combinations

Source: Author's analysis

While scenarios A and B are the most suitable from a climate change mitigation viewpoint, India can choose these scenarios only if substantial financial and technological support are available from other developed countries. However, given experience, this seems challenging. In contrast, postponing the peaking year until 2050 would be highly damaging from a climate perspective. To compare the above estimations of cumulative carbon emissions across various peaking and net-zero year combinations for India with other regions, the 2021–2100 cumulative emissions based on their net-zero ambition would be 349 GtCO2 for China, 69 GtCO2 for the EU, and 104 GtCO2 for the US. When historical emissions are included in the comparison, India’s numbers pale in comparison to China, the EU, and the US. Of course, if economic growth turned out to be lower and the cost of mitigation technologies declined faster than anticipated, Indian policymakers, industrial leaders, and consumers could harness the opportunity and aim to achieve net-zero as early as possible. There would be some important economic tradeoffs that India would have to deal with on the path towards achieving a net-zero year. Some benefits are clear. A decisive shift towards a ‘net-zero’ economy provides an opportunity to pivot economic growth around green infrastructure creation. Be it generation and transmission infrastructure for non-fossil energy sources, or an even larger electricity system for rapid electrification of various end-use sectors. Early shift would ensure avoidance of lock-ins. There would, however, be some trade-offs as well:

Electricity prices for households would increase: The cross-subsidy based electricity pricing regime has to be dropped for a rapid electrification of industrial energy use. This would mean household electricity prices would have to be increased. In absence of this, government’s budgetary burden could increase significantly as the financial viability of distribution companies will be further hit.

Railways passenger tariff would increase: Coal freight is significant for the revenues of Indian Railways IR). A net-zero India means that the IR would lose this significant source of revenue, forcing it to either raise revenue through freight or passenger sources. Freight charges are already high in order to subsidise passenger fares. In all likelihood, millions of passengers dependent on subsidised railway charges would face increasing prices to compensate for the loss of revenues from transporting coal.

Coal-dependent states would face fiscal challenges: Some states in India, particularly in the eastern belt such as Odisha and Jharkhand, generate a sizeable source of their state government revenue from the energy sector. Going out of fossils, specifically coal, would mean that these states not just think about a new economic development paradigm drastically different from their current economic approach, but are well onto that pathway by 2050.

Coal sector jobs would be lost: Over half a million coal mining workers would have to be provided with alternative gainful employment opportunities commensurate with their skills or retrained for work in other related energy sectors or be given severance packages in the event of shut down of this sector. Coal India Ltd. would have to wind down operations, at least in its current avatar.

Geopolitics would shift: A net-zero target would also bring about a dramatic shift in the geopolitics of energy. India could start importing biofuels from Southeast Asia or South America, which are rich in water resources. This will break transform existing energy relationships, such as with West Asia, and create new opportunities as well as tensions. The reliance on critical minerals, which are used in clean energy and clean mobility sectors, would also grow.

Along with economic growth and the economic trade-offs presented above, there are four critical considerations in choosing peaking and net-zero years. First is the duration between a peaking and a net-zero year. In general, countries take at least 30–40 years to transition from a peak to a net-zero year (Table 2). This pace of transition appears to be manageable. Several underlying societal factors need to be adjusted to ensure a smooth and equitable transition. Second is the cumulative emissions associated with each peaking and net-zero year combination. A delay in peaking, generally speaking, does imply an increase in the cumulative emissions between the peaking and net-zero year. Third is the possibility of stranded assets. The greater the delay, the higher the possibility of long-term lock-ins and stranded assets in the future, as well as higher cumulative emissions. The fourth is the availability of an economically viable mitigation technology set, particularly biomass, carbon capture and storage (bio-CCS) and/or green hydrogen. The larger the portfolio available for mitigation, lesser is the over-reliance on one or two key technology options. As shown in table 3, CCS gives an option to continue with fossils to some extent. Bio-CCS gives an option to emit in some sectors, which are ‘netted’ through negative emissions from the bio-CCS technology.

Climate change impacts are pushing policymakers toward meaningful near-term actions to reduce emissions. Some large countries have announced their ambition to achieve net-zero economies in the future. This provides a critical and clear policy signal for actors to rally around and increase the pace of transition. India is an influential nation in the climate change debate, and the world keenly awaits its decision on net-zero.

This brief presents a simple analytical formulation to better understand the challenges associated with alternative combinations of peaking and net-zero years for India. First, it highlights that for a rapidly developing economy, the choice of peaking year is implicit in the selection of a net-zero year; hence, it is important to assess peaking year to inform the decision-makers who will be impacted by the transition.

The analytical formulation shows that the ‘effort gap’ is significantly impacted by the economic growth rate. For India, peaking in 2030 would be very challenging given the expected economic growth rates for at least the next two decades. With such growth rates, the rate of fuel shift toward non-fossil energy and decrease in primary energy intensity of GDP needs to be much faster compared to other countries like China, which are going to peak when their economies are much larger and their economic growth rates are comparatively much lower.

In summary, the rate of expected GDP growth would make it very challenging for India to have an early peak, and it needs a much faster transition in terms of fuel shift across sectors in the economy compared to countries that are expected to have a lower GDP growth rate in the next few decades, such as China. These shifts need a step-change in how India’s demand and supply sectors operate and, hence, would have significant near- and long-term costs. While a near-term transition from peak to net-zero presents opportunities for a green infrastructure driven economic growth agenda, it would also present many critical trade-offs amplified by the rapid pace of required transition towards a net-zero world for a low-income yet rapidly growing economy. It is important to recognise the trade-offs so that appropriate domestic measures can be taken. Moreover, this would require active support for India’s transition from and in collaboration with advanced economies in terms of financial invesments and technology transfer/ co-development. India needs to invest in technologies that can reduce energy intensity and emission intensity, and would need international support in order to pursue more aggressive route to decarbonisation. Clearly, India will need to do more than its fair share for the world to achieve the “well below 2 degrees Celsius” target.

The key considerations for selecting peaking and netzero years should be per capita income, economic growth rate, a ‘reasonable’ pace of transition determined by the gap between peaking and net-zero years, possibility of lock-ins and stranded assets, and the cumulative emissions across the alternative peaking year–net-zero year combinations. The chosen combination should provide India sufficient time to develop and ensure that the climate impact is minimised. It is clear that the transition towards decarbonisation that is already underway needs to be accelerated urgently to ensure the bending of emissions curve below the BAU trajectory. An ambitious decarbonisation plan should not be ruled out; however, it would not be possible without significant and steady financial and technical support from the developed world.

How can Carbon Markets Scale Durable Carbon Dioxide Removal in India?

Sustainable rice cultivation in India

EU Carbon Border Adjustment Mechanism

Roadmap for a Net-Zero Power Sector in Gujarat