Council on Energy, Environment and Water Integrated | International | Independent

Suggested citation: Warrior, Dhruv, Vibhuti Chandhok, Abhinandan Khajuria, Shruti Gauba, and Rishabh Jain. 2024. Strengthening India's Clean Energy Supply Chains: Building manufacturing competitiveness in a globally fragmented market. New Delhi: Council of Energy, Environment and Water.

This report provides an in-depth analysis of India’s potential as a global manufacturing hub for the clean energy sector while addressing challenges such as intense competition and market uncertainties. Focusing on solar photovoltaics, wind turbines, and lithium-ion batteries, it identifies key supply chain segments for an indigenisation strategy through product space map analysis, industry insights, and a thorough literature review of manufacturing processes. Given the strategic factors influencing this sector—geoeconomic opportunities, technological advancements, energy transitions, and security—the report calls for a shift from conventional industrial and trade policies, which may prove inadequate in a market dominated by developed economies having massive fiscal bandwidths. Indigenising clean energy manufacturing is strategically crucial for establishing the foundation for a future green economy and positioning India as a competitive global player. Moreover, by capitalising on a fragmenting global market, India can attract international investment and diversify supply chains currently concentrated in the People’s Republic of China, enhancing its role in the global energy transition.

The pace of deployment of clean energy is increasing at an unprecedented rate every year. Presented with the opportunity to produce for both domestic and international markets, clean energy manufacturing in India is poised at a critical juncture. In a fragmenting global market, India possesses the potential to become a globally competitive manufacturing hub. However, this opportunity is also accompanied by several risks arising from global manufacturing overcapacities, razor-thin profit margins in the post-COVID economy, and uncertainties associated with domestic demand. These risks threaten the investments of USD 4.56 billion (INR 36,492 crore) committed by governments to catalyse this nascent sector through Production-linked incentive (PLI) schemes.1 Strategic policy choices made now will determine whether Indian manufacturers of clean energy technologies emerge as world leaders or remain reliant on continuous government support in the short to medium term.

Precisely targeted policymaking is essential to align the wide-ranging economic prospects of indigenisation with India’s energy security and energy transition goals. Therefore, we critically evaluate the strategic value of deepening clean energy manufacturing in this report, and assess the efficacy of central government policies at realising this value. We argue that the conventional industrial and trade policy tools instituted so far can prove inadequate in securing the myriad strategic advantages of this sector, given the intense competition across various segments of the supply chain, and the larger fiscal capacities of other developed economies. We aim to fill these gaps by providing a nuanced rationale and a methodological approach for advancing the indigenisation of this sector in India.

Recognising that industrial development is a gradual process contingent on a country’s existing production capabilities, we utilise product space mapping analysis to identify segments of the supply chain that India should prioritise in its indigenisation strategy. We complement this with a bottom-up analysis based on stakeholder engagements, discussions with industrial players, and literature reviews to complete the identification exercise. Identification of the relevant supply chain segments is hence based on a comprehensive and methodological approach, taking into account their complexity, competitiveness, impact on the total cost of the final technology/product, and potential to open up pathways into more complex sectors.

To ensure a focused analysis, we deep-dive into three key clean energy technologies –solar photovoltaics, onshore and offshore wind turbines, and lithium-ion batteries. Each has a mature manufacturing sector globally as well as an existing demand base in India, offering relevant insights to scale these sectors rapidly. We also touch upon certain alternate solar, wind, and battery technologies where relevant to the discussion. However, we have not assessed the supply chains for clean energy technologies such as green hydrogen or biofuels in this study. By addressing the strategic imperatives and identifying key areas for policy intervention for select technologies, we aim to provide targeted recommendations for India – and possibly other developing countries – to build sustainable, future-oriented, globally competitive clean energy value-chain segments.

Clean energy manufacturing not only offers pathways for decarbonisation, but can also enhance energy independence, foster value-addition in manufacturing, and create positive externalities on growth and innovation (more details in Table ES1). Indigenising this sector thus supports distinct yet interconnected avenues of strategic value to the Indian economy – resilience and security; domestic value capture; export opportunities; and structural transformation. We take the view that Indian manufacturing policies have yet to make significant progress towards maximising value across all four avenues. In its policy development, it is crucial for India to balance the important, albeit uncertain, benefits of export-oriented growth, value addition, and techno-economic transformations against the important, but limited, benefits of energy security.

Table ES 1: There are four avenues of strategic value from deepening clean energy manufacturing in India

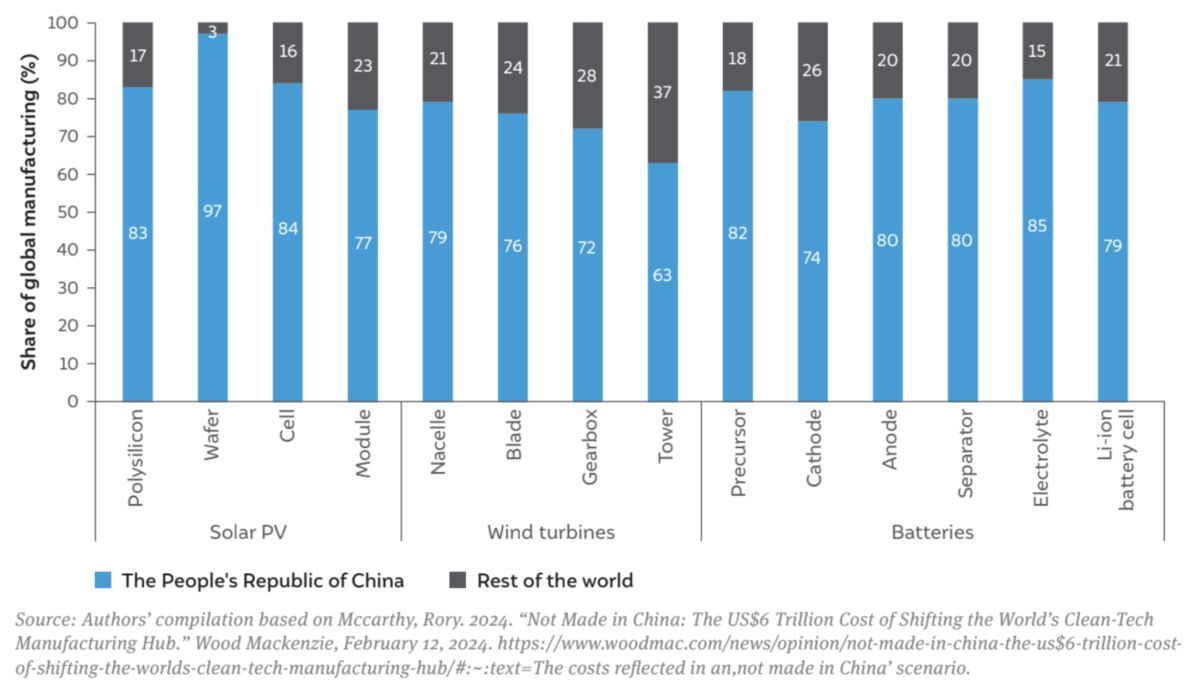

The manufacturing sector in the People’s Republic of China has been the front-runner in clean energy technology, dominating the global market for nearly a decade (Figure ES1). While this concentration is alarming, India needs a well-informed response to Chinese market dominance as various manufacturing policies could lead to very different types of economic impact. For instance, policies aiming for complete control over clean energy manufacturing through very high tariff barriers and domestic content requirements (DCRs) could rapidly increase domestic value capture. However, these measures could also negatively impact innovation, reducing export competitiveness and limiting technological spillovers into the broader economy, as well as slowing deployment due to higher technology prices. From a security standpoint, policymakers will need to consider two important points: first, clean energy technologies and their embodied materials last for decades within the energy system and secondly, the cartel-like behaviour seen amongst producers within the petroleum sector will not be as significant in the clean energy sector (World Economic Forum 2024). We therefore recommend a balance between policies that support increased domestic control and those that encourage innovation and global competitiveness.

Figure ES1 : The People’s Republic of China dominates the global clean technology manufacturing capacities

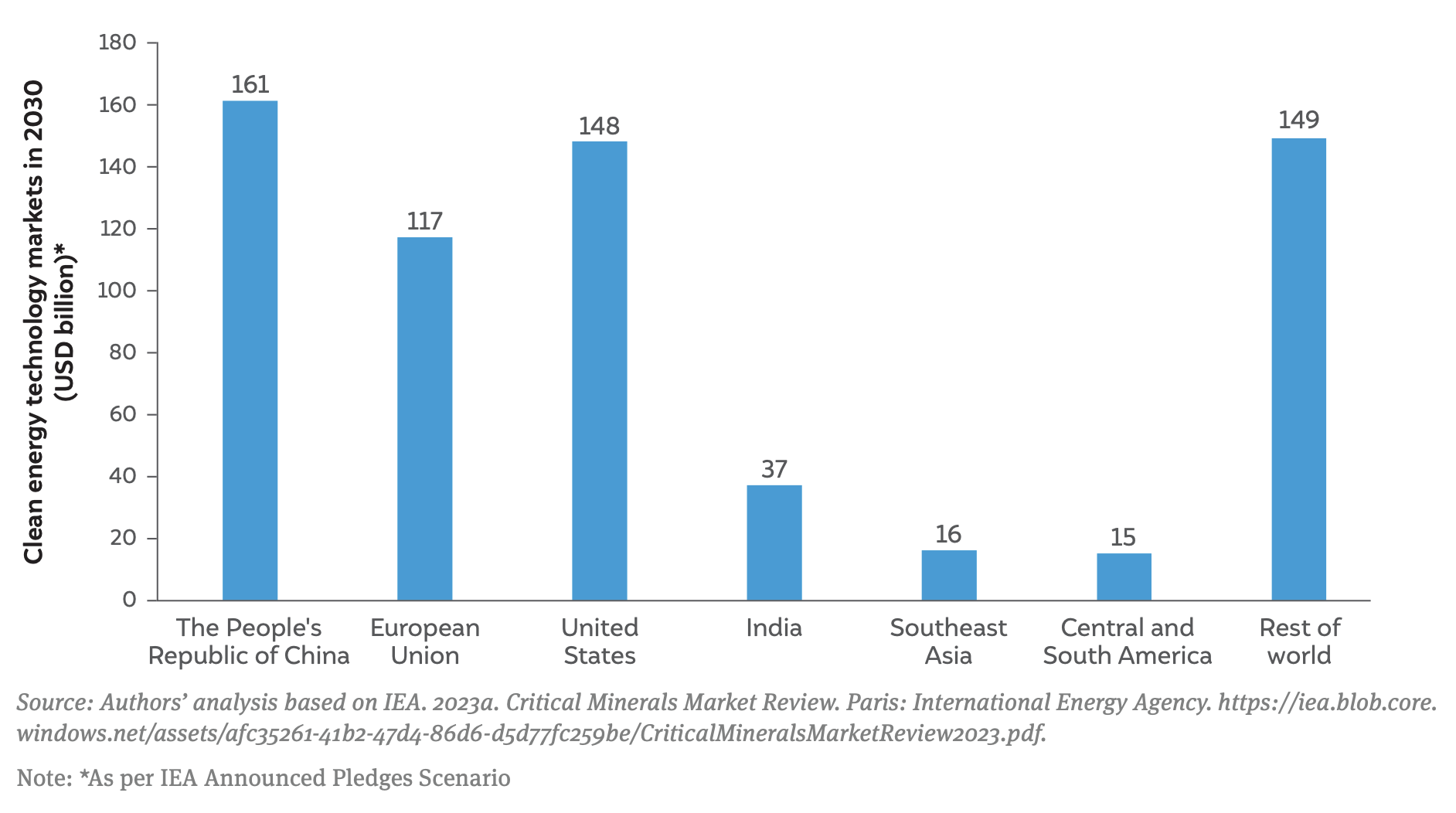

Approaching this sector strategically could also open up huge export opportunities for India. In Figure ES2, we showcase the International Energy Agency’s (IEA) more conservative estimate of the clean energy market in 2030, representing an annual demand of around USD 640 billion. We expect this demand will be evenly spread across the PRC, Europe, and the United States, each with markets sized at around USD 140 billion. In contrast, the Indian market is likely to be much smaller at around USD 40 billion, or about 6 per cent of the global market. However, orienting India’s clean energy industries to be competitive globally could potentially unlock a much larger market even in a conservative deployment scenario.

Figure ES2: India’s market size for clean energy technologies is expected to remain smaller than other key nations in 2030

However, the challenge of a changing global reality is particularly significant. Since 2020, clean energy technologies have gone from a severe global supply crunch, both of components and final products, to significant oversupply, with crashing product prices – primarily due to rapid growth of supply from the PRC. This situation of oversupply is expected to continue into 2030 (IEA 2023a). The United States and Europe have responded to the economic and energy security threat they perceive from this concentration and its potential to reindustrialise their economies by implementing strong industrial and trade policies such as the Inflation Reduction Act (IRA) in the United States and the Net Zero Industry Act (NZIA) in Europe (EurpoeanCommission 2023.; IEA 2023f). These initiatives are expected to attract significant investment in the years ahead, potentially drawing investment away from Global South economies such as India (IEEFA-JMK 2023). Unless it collaborates with like-minded countries and opens up free trade access, India may jeopardise its own access to essential global markets.

In this report, we have identified those segments which can contribute at least one of the following to the Indian economy:

1. Manufacturing competitiveness

2. Solutions to supply or technology risks in Indian manufacturing

3. Enable a high-tech manufacturing and innovation ecosystem.

This identification is guided by a dual approach: bottom-up research that utilises stakeholder consultations and roundtable discussions with manufacturers, along with a quantitative, topdown analysis that utilises the product space mapping methodology (elaborated in Section 4.2).

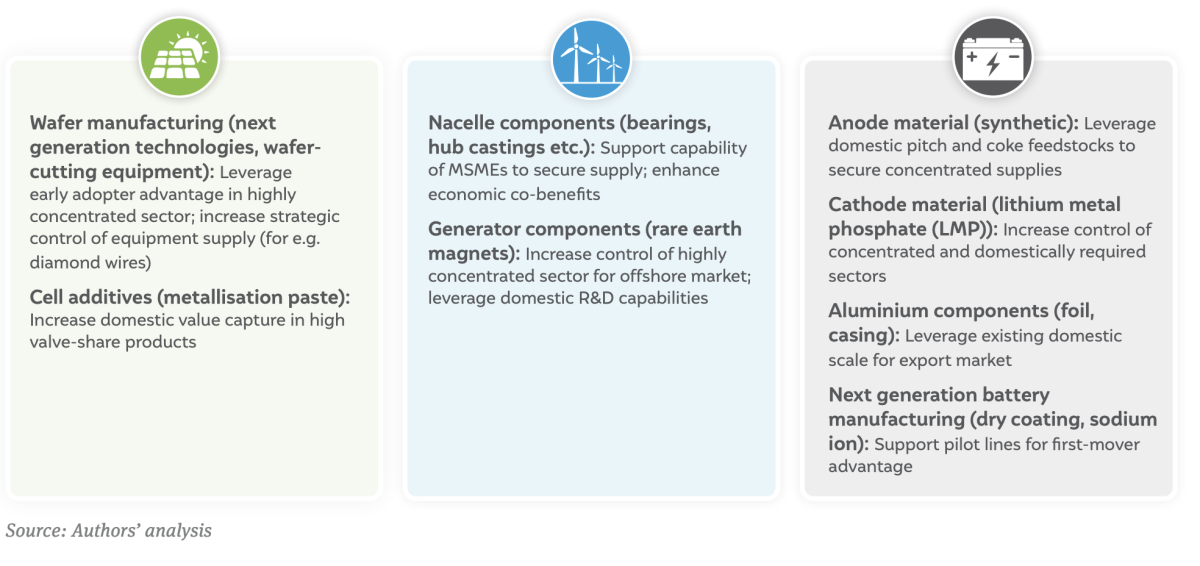

Focus areas based on market analysis and stakeholder consultation: Based on our assessment of global market developments and India’s domestic requirements and existing capabilities within product segments, we have shortlisted nine components that Indian policymakers should focus on to enhance policy support (Figure ES3). We have prioritised supply-chain segments with a high market concentration, high technological complexity, or high impact on final product cost.

Figure ES3: Technology-specific focus areas for policymakers

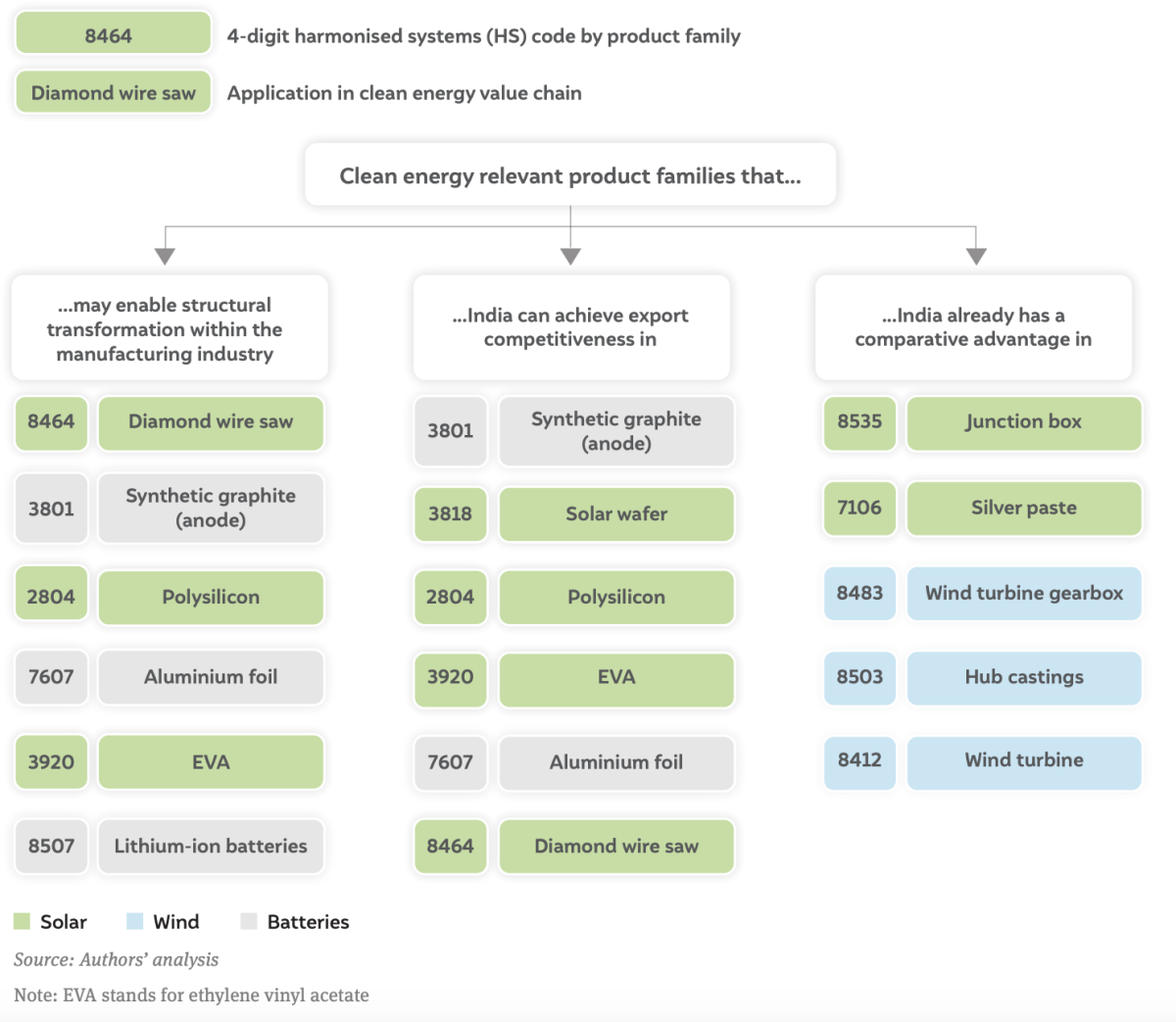

Focus areas based on the product space map method: Further, the product space approach can help policymakers in India assess the broader ecosystem effects and opportunities from scaling various clean energy components (Harvard University 2024b). Findings from the economic complexity concept inherent to the product space approach can be generalised; however, these findings can only be a preliminary guidance for policymakers and must be complemented by technology-specific market research and stakeholder consultations. Table ES2 highlights clean energy–relevant product families (details in Section 5.2) that India may prioritise, either to achieve global competitiveness or to enhance spillover effects in the economy. Source: Authors’ analysis Note: EVA stands for ethylene vinyl acetate

Table ES2: Top clean energy-relevant product families relevant for India

We recommend that the Indian government respond to this new global paradigm and maximise strategic value for the Indian economy with a two-pronged approach. First, India should complement its PLI schemes and broad technology-level trade policies by identifying specific clean energy supply-chain segments/components for scaling through tailored support and market protection. Secondly, India must re-evaluate and reconfigure its policies to address domestic policy uncertainties, respond to global demand variability, and ensure the availability of sufficient input materials, technological expertise, finance, and other manufacturing enablers in the domestic ecosystem. Collating insights from both these approaches, we recommend policy priorities for India in the clean energy manufacturing sector (Figure ES4) that can advance the identified supply-chain segments and maximise strategic value for the Indian economy.

Figure ES4: A comprehensive strategy to drive India towards a competitive clean energy supply chain

The clean energy sector is characterised by intricate manufacturing processes essential for producing key technologies such as crystalline silicon solar photovoltaics (c-Si), wind turbines, and lithium-ion batteries. Each of these technologies requires a series of complex steps, from the synthesis of raw materials to the assembly of final products, involving capital and energy-intensive operations. These manufacturing processes are collectively referred to as the clean energy value chain.

As a large share of carbon emissions are attributed to the energy sector, the International Energy Agency (IEA) estimates that the proportion of renewable energy in the electricity mix must increase from 28.7 per cent in 2021 to 90 per cent by 2050 to achieve global net-zero goals. For example, the foundations of lithium-ion battery manufacturing in India are closely associated with the decarbonisation of the transportation sector and, as such, climate policies are closely linked with the clean energy sector.

Clean energy manufacturing not only offers pathways for decarbonisation, but can also enhance energy independence, foster value-addition in manufacturing, and create positive externalities on growth and innovation. This sector supports distinct yet interconnected avenues of strategic value to the Indian economy – ensuring resilience and security, capturing supply chain segments for domestic manufacturing, export opportunities, and enhancing structural transformation.

India aims to install 500 GW of non-fossil power capacity by 2030. As per estimates by the Central Electricity Authority (CEA), the likely installed capacity by the end of the year 2029-30 would include approximately 99 GW of wind-generated power (about 12 per cent of installed capacity), and 292 GW of solar-generated power (about 37 per cent of installed capacity).

Advancing Solar Cell Manufacturing in India

Establishing a Sodium-ion Battery Ecosystem in India

Making India a Hub for Critical Minerals Processing

State of the Sector: Critical Energy Transition Minerals for India