Council on Energy, Environment and Water Integrated | International | Independent

Suggested Citation: Garg, Aditya, Sonal Kumar, Torgrim Asphjell, Shikha Bhasin, and Jitendra Bhambure. 2025. Unlocking Financing for Refrigerant Management: Policy Pathways for a Circular Cooling Economy in India. New Delhi: Council on Energy, Environment and Water.

Lifecycle refrigerant management (LRM) broadly involves prevention of refrigerant emissions from the cooling devices during its operational life, and recovery of refrigerant for recycling and reuse, or safe disposal at the end-of-life (EOL) of these devices. Several countries have taken initiatives for the implementation of LRM practices, however, one of the major challenges faced is ensuring the financial sustainability of businesses involved in implementation of various stages of LRM. Operationalisation of LRM practices would require creating an entire ecosystem of reverse supply chain involving recovery of refrigerants; collection, aggregation, and testing; transport and logistics; reclamation, testing, packaging, and resale; and destruction of gases. A mechanism that can help in the generation of sustained and adequate revenue from LRM activities, would ensure incentives and sustainable business case for the personnel and enterprises involved in the implementation of LRM practices.

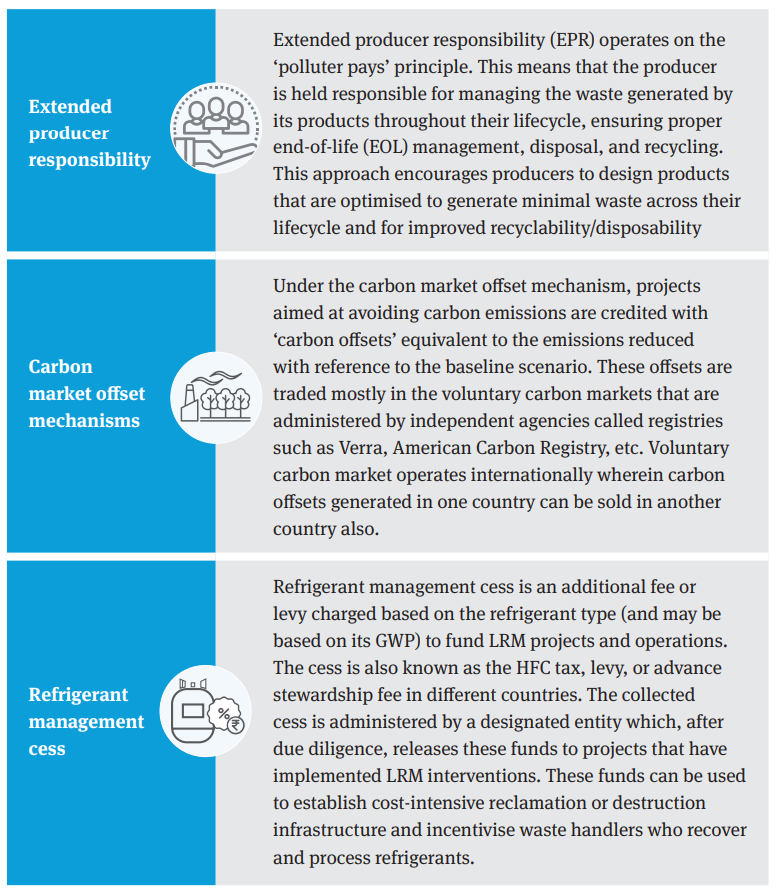

Globally, the policy approach adopted for financing LRM can be broadly categorised into three:

This report discusses these three policy approaches to develop an understanding of their implementation framework and procedures involved, stakeholders and their roles, and measures needed for to enable the adoption of any of these policy approaches for financing LRM practices in India.

India can avoid generating around 2 billion tonnes of carbon dioxide (CO2) equivalent emissions by 2050 by employing lifecycle refrigerant management (LRM) practices (Kumar et al. 2023). LRM is a comprehensive set of strategies to mitigate the risks of refrigerant emissions by managing them in an environment-friendly manner throughout their lifecycle – from production to disposal. LRM addresses the following aspects of the refrigerant lifecycle (TEAP–UNEP 2024):

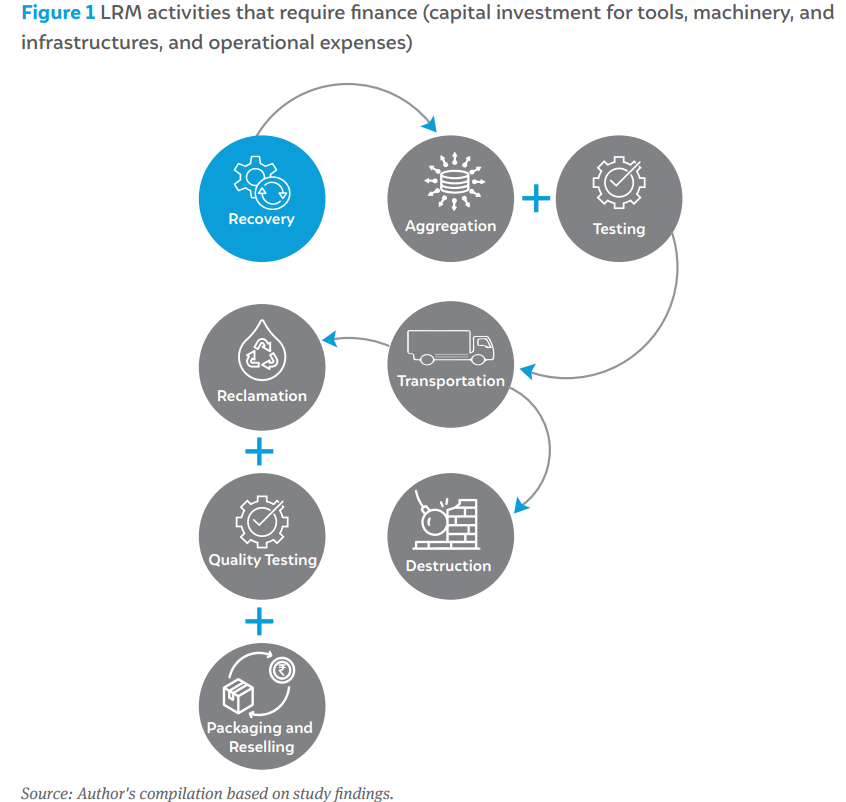

Implementing LRM practices requires a comprehensive reverse supply chain ecosystem involving the recovery of refrigerants; collection, aggregation, and testing; transport and logistics; reclamation, testing, packaging, and resale; and destruction of gases (Kumar et al. 2023). Creating and sustaining such an ecosystem requires finance for capital investments – to establish the necessary infrastructure, including recovery machines, collection and aggregation centres, test labs, and reclamation and destruction facilities – as well as meet operational expenses. This is why it is essential to incentivise key actors to adopt LRM practices and ensure the long-term financial sustainability – beyond a grant or one-time financial support – of the businesses and enterprises involved in implementing various LRM stages.

Different countries have adopted various policy approaches to generate the financial support needed to implement LRM. These policy approaches can be broadly classified (in no order of preference) into three categories.

We have identified key challenges and findings associated with each policy approach to finance LRM implementation in India.

I. Extended producer responsibility

In India, the E-Waste (Management) Second Amendment Rules, 2023, and the Draft Endof-Life Vehicle (Management) Rules, 2024, mandate refrigerant management based on the EPR approach. These policies cover a majority of cooling products that contain refrigerants. However, the detailed implementation guidelines and procedures for implementation of refrigerant management as specified under these rules, are still under development: The key findings and challenges to adopting EPR for financing LRM in India are identified as below.

II. Carbon market offset mechanisms

Leveraging the carbon market’s offset mechanism, wherein carbon offsets generated for avoiding refrigerant emissions through LRM practices are purchased by entities willing to offset their emissions, encourages and funds emission reduction LRM projects. Article 6 of the Paris Agreement deals with carbon credits. In November 2024, member countries adopted rules and guidelines to implement Article 6.2 and Article 6.4 of the Paris Agreement1 , which focus on carbon trading through bilateral or cooperative approaches and international market mechanisms (UNFCCC 2024). The Indian government is working toward developing carbon markets in the country, and it has finalised a list of activities to be considered for trading carbon credits under Article 6.2 (MoEFCC 2023d). LRM is not included in this list currently, but it may be considered in future revisions. This report is primarily focused on the use of voluntary carbon market (carbon offset) mechanism to support LRM practices.

III. Refrigerant management cess

Refrigerant management cess is a policy mechanism to secure funds for financing and incentivising LRM infrastructure and operations (AHRI 2018). It is a form of carbon tax that is imposed on greenhouse gas emissions, aiming to make polluting activities more expensive and encourage their reduction. Typically, it is charged upstream to the manufacturers and importers of refrigerants, which is then eventually passed on to the end consumers.

In India, there has not been any cess on refrigerants. However, this policy mechanism has been used in other sectors. For example, India imposed a clean energy cess (later termed as clean environment cess) on coal lignite and peat in the year 2010. The fund collected was earmarked for financing and promoting initiatives aimed at clean environment. However, the fund was merged with the compensation cess after the rollout of the Central Goods and Service Tax Act, 2017 (SSEF 2018; IISD 2018).

These three policy approaches can be adopted in combination or independently to ensure sustainable financing for LRM activities. Based on the learnings from the global and Indian experiences, certain initiatives need to be undertaken for effective adoption of these policy approaches. We have outlined the recommended actions as follows.

I. Extended producer responsibility

II. Carbon market offset mechanisms

III. Refrigerant management cess

In addition to the recommendations outlined above for each policy approach, complementing initiatives aimed at standardisation of LRM processes, capacity building of servicing technicians and waste handlers, awareness generation among stakeholders, including consumers, and establishing of necessary infrastructure and market linkages are required. Also ensuring harmony between the chosen policy approach and the existing regulations, such as the Ozone Depleting Substances (Regulation and Control) Rules, 2000, E-Waste (Management) Rules, 2022, and Draft End-of-Life Vehicles (Management) Rules, 2024, will be essential. This will enable smooth coordination among stakeholders and the effective implementation of LRM practices.

Lifecycle refrigerant management (LRM) can help mitigate the environmental impacts of refrigerant emissions and aid in achieving phase-down targets. LRM offers a comprehensive set of strategies to mitigate the risks refrigerant emissions by managing refrigerants in an environmentally sound manner throughout their entire life cycle. It encompasses the production, storage, and transportation of refrigerants, the design, manufacturing and installation of refrigeration, air-conditioning, and heat-pump equipment (RACHP), its operation and maintenance, as well as the recovery, reuse, and environmentally sound disposal of refrigerants. (UNEP TEAP 2024)

The demand for cooling in India has been rising rapidly. As per the India Cooling Action Plan, the cooling demand is expected to grow 8-10 folds during 2017-18 to 2037-38 across various demand sectors (MoEFCC 2019). The cooling devices largely rely on vapour compression based cooling technologies that use refrigerant gases. Given the demand, a significant amount of these gases have accumulated within the existing stock of cooling devices, which is expected to grow before the gases are phased out. A recent study estimates that, if left unattended, the emissions generated by these refrigerant gas banks globally could equal 91 billion tonnes of carbon dioxide (CO2) emissions by 2100 (EIA, IGSD, NRDC 2022). As per CEEW estimates for India, in the absence of LRM practices, refrigerant accumulated in the stock of cooling devices will eventually emit into the atmosphere and will contribute to 2 billion tonnes of CO2–equivalent emissions by 2050 (Kumar et al. 2023). Recognising the issue, several countries have introduced initiatives to implement LRM practices (Garg et al. 2023). The scope and implementation mechanisms of these initiatives vary across countries.

The Montreal Protocol 1987 and its subsequent amendments aim to control the production and consumption of substances —including refrigerant gases with ozone depletion potential (ODP) or high global warming potential (GWP) —with the final objective of completely phasing them out. LRM is also increasingly getting focus at the Montreal Protocol platforms. The 35th Meeting of Parties of the Montreal Protocol 2023 encouraged governments to develop strategies, policies, and activities for adoption of LRM practices. The parties constituted a dedicated task force under their Technology and Economic Assessment Panel (TEAP) to examine and recommend policy measures and options to promote more sustainable technologies and secure financing to support them (OS-UNEP 2023).

The Indian government has also introduced interventions over the past few years to operationalise LRM practices. Several hundred recovery machines were distributed to servicing technicians across the country at subsidised rates, and 18 mini-reclamation centres were set up (MoEFCC 2019). The Ozone Cell has been regularly educating servicing technicians about LRM via their magazines, day-long events, and training programmes. The MoEFCC has mandated e-waste recyclers and vehicle scrappage facilities to recover refrigerants for their safe disposal in their E-Waste Management Second Amendment Rules, 2023, and Vehicle Scrappage Policy, 2021 (MoEFCC 2023a).

Despite these efforts, the average rate of refrigerant recovery in developed countries has been modest. In developing and least-developed countries, it has been notably minimal (Garg et al. 2023). In India, recent research by CEEW shows that effectively operationalising LRM practices requires a comprehensive approach involving initiatives on many fronts. These include introducing policies based on robust data, creating an inventory of refrigerant banks, incentivising and building the capacity of key actors, establishing a reverse supply chain and the infrastructure needed for LRM, and ensuring the financial sustainability of stakeholders involved in implementation at various stages of LRM among others (Kumar et al. 2023).

A policy mechanism to creating sustainable business models is essential to ensure the financial sustainability of the enterprises involved in LRM implementation, and hence to ensure the effective and sustained implementation of LRM.

LRM interventions broadly encompass the following areas:

Original equipment manufacturers (OEMs) are primarily responsible for the interventions to improve design and product quality and its financing, which may reflect in their product pricing. Implementing better operational practices requires building the capacity of technicians and encouraging users/owners to adopt recommended practices. While the cost of the initiatives towards capacity building and awareness generation are usually borne by the public sector and OEMs, the additional costs for adopting the recommended installation and servicing practices would be borne by the users/owners.

This report primarily focuses on the third set of interventions and discusses the potential financing mechanisms that can help generate a sustainable revenue through LRM activities for the end-of-life (EOL) management of refrigerants.

Implementing LRM practices requires a comprehensive reverse supply chain ecosystem, involving the recovery of refrigerants (on-site or off-site); collection, aggregation, and testing; transport and logistics; reclamation, testing, packaging, and resale; and finally, destruction of the gases. Creating and sustaining such an ecosystem will require capital investments to establish necessary infrastructure, including recovery machines, collection and aggregation centres, test labs, reclamation and destruction facilities, and to meet operational expenses. Figure 1 illustrates the various LRM stages that require financing.

Regular and adequate revenue from LRM implementation activities can establish a sustainable business case for the individuals and the enterprises involved in the implementation of LRM practices, ensuring their sustenance and independence in the long term. During the Hydrochlorofluorocarbon (HCFC) Phase-out Management Plan (HPMP) Stage-II (2017-24), 18 mini-reclamation centres were set up in different parts of India with support from the Multilateral Fund (MoEFCC 2019). However, one of the major challenges reported was the lack of a sustainable business model for these facilities (Bhasin et al. 2019). Recognising this need, in the HPMP Stage-III (2023-30), there is a focus on developing sustainable business models for LRM facilities.

Globally, various policy approaches have been adopted by different countries to generate the financial support needed to implement LRM. These policy approaches can be broadly classified (in no order of preference) into three categories. Different countries have typically used one or a combination of the approaches detailed here.

These policy approaches can be adopted in combination or independently to ensure sustainable financing for LRM activities.

The objective of this report is to discuss these policy approaches and the measures needed for their effective implementation. Each section covers the following aspects of a policy approach:

For this report, we adopted a methodology that had three components: extensive desk research; an in-depth, questionnaire-based consultation with stakeholders; and convenings in the form of workshops or panel discussion, to gather stakeholders’ inputs. Our desk research involved reviewing the existing literature to develop a theoretical foundation and learn about best practices. We further complemented this with one-on-one interviews with selected experts based on a semi-structured questionnaire to gather practical insights into the implementation of these policy approaches and their challenges. Finally, we convened panel discussions with the stakeholders and presented our findings at various forums, which provided us with a varied perspective and validated our findings.

The following sections of this report discuss the three policy approaches and the measures needed for their implementation. In Section 2, we discuss EPR, in Section 3, we discuss carbon market’s offset mechanisms, and in Section 4, we explore refrigerant management cesses. Finally, we summarise these discussions and offer our conclusions in Section 5.

Extended producer responsibility (EPR) is one of the most widely used financing approaches worldwide to manage decommissioned products at the end of their lifecycle. This approach emerged in the late 1980s in Europe to effectively manage packaging waste (OECD 2016). Since then, EPR has expanded to sustainably managing electrical and electronic appliances, plastics, tyres, vehicles, and many more products, making it an essential policy approach. Under the EPR framework, producers are held financially and operationally accountable for collecting, recycling, and safely disposing EOL products. Although its success rate differs across products and geographies, overall, it has increased waste recycling and reduced landfill use as compared to the no-mandate baseline (OECD 2016).

Theoretically, holding producers accountable both encourages and incentivises them to prevent waste at the origin of a product’s lifecycle (OECD 2016). Producers not only possess product-specific knowledge, but also control production, material selection, and design. Consequently, they are well-placed to use materials that are financially and operationally optimal for recycle and reuse.

ERP is also consistent with the ‘polluter pays’ principle. This principle asserts that those generating waste should bear the costs associated with EOL management, rather than taxpayers or society at large. Producers are required to either directly handle EOL management of their products or hire a third-party waste handler to collect, recycle, or safely dispose them.

However, producers eventually pass on these costs to the end user by adding them to the product’s final market price. As a result, consumers end up bearing the financial burden associated with responsible waste management.

India’s EPR-based waste management system and its implementation

India has adopted the EPR approach to manage various waste such as e-waste, plastic waste, etc. The Central Pollution Control Board (CPCB) in India – a statutory body under the Ministry of Environment, Forest and Climate Change (MoEFCC) – governs the formulation and implementation of guidelines, standards, and regulations for managing different categories of waste under the EPR approach.

Most air conditioning and refrigeration devices are categorised as electronic waste in India, and their EOL management is governed by the E-Waste (Management) Rules, 20225 (MoEFCC 2022). EOL management of decommissioned vehicles is governed by the Draft End-of-Life Vehicles (Management) Rules, 2024 (MoEFCC 2024). The implementation mechanisms and integration of EOL refrigerant management into these Rules are discussed below.

E-Waste (Management) Rules, 2022

The 2022 E-Waste Rules override the Rules introduced by the MoEFCC in 2016 to tackle the growing problem of e-waste. Earlier legislations and their amendments successfully enabled manufacturers to recycle and safely dispose of 26.3 per cent of the total e-waste generated in the financial year (FY) 2020–21, although a few challenges remained (Gupta 2023).

The 2022 E-Waste Rules aim to ease implementation, enhance monitoring and enforcement, increase compliance, and broaden the range of electronic appliances covered. The 2022 E-Waste Rules offer a market-driven, more comprehensive framework to manage over a hundred types of electrical and electronic appliances at their EOL (MoEFCC 2022). More importantly, the 2022 E-Waste Rules have expanded the range of cooling appliances and included managing refrigerant gases in their scope (MoEFCC 2023a).

With regard to the EOL management of e-waste, the 2022 E-Waste Rules require only four stakeholders —producers, manufacturers, recyclers and refurbishers —to register themselves on the CPCB’s e-waste management portal (MoEFCC 2022). Explicitly regulating only major stakeholders that play a significant part in the e-waste ecosystem enhances the government’s compliance supervision efforts.

Under the 2022 E-Waste Rules, producers of electronic products must furnish detailed information about their products —such as the specifics of their components and number of units sold —on the CBCB’s e-waste management portal on a quarterly basis (MoEFCC 2022). Based on the average life of a product and its sales volume, producers are assigned annual e-waste recycling targets – also referred to as EPR targets – that they are obliged to meet for a specific financial year.

The 2022 E-Waste Rules set strict recycling targets for producers, starting at 60 per cent in FY 2023–2024, rising to 80 per cent by FY 2027–28 (MoEFCC 2022). In FY 2023–24, producers must recycle 60 per cent of all electronic appliances sold in the market X years ago, where ‘X’ is the average life of that product as specified in the 2022 E-Waste Rules (MoEFCC 2022). For example, the 2022 E-Waste Rules consider the average life of a domestic air conditioner to be 10 years. Therefore, a domestic air conditioner manufacturer must recycle 60 per cent of all the products they sold in the market 10 years back.

As per the 2022 E-Waste Rules producers must meet their annual recycling targets by purchasing EPR certificates from recyclers and refurbishers registered on the CPCB’s portal (MoEFCC 2022). Similar to offsets issued in the carbon market to project developers based on verified emissions reductions, the CBCB issues EPR certificates to recyclers and refurbishers based on the information they provide on the portal regarding the quantity of e-waste components they process. Companies can purchase these EPR certificates from recyclers to meet their annual targets (MoEFCC 2023c). The number of certificates that companies buy must be commensurate to their annual recycling obligations. Currently, EPR certificates are issued and traded in terms of quantities (in kg) of certain metals recovered from recycling of e-waste which includes aluminium, gold, iron, and copper.

However, the 2022 E-Waste Rules pose certain implementation and compliance challenges. Presently, compliance is primarily monitored based on the recovery and recycling of the metals mentioned earlier. This may drive e-waste recyclers to prioritise the extraction of these metals, as financial benefits and compliance requirements are tied to their recovery and recycling. Consequently, other materials, such as refrigerants, might be overlooked or improperly handled since they do not contribute to recyclers’ compliance requirements or provide a financial incentive. Funding and incentivising proper refrigerant management must be incorporated into the 2022 E-Waste Rules to ensure that refrigerants are handled in an environmentally sound way as well.

Draft End-of-Life Vehicles (Management) Rules, 2024

The implementation framework of the Draft End-of-Life Vehicles (Management) Rules, 2024, is similar to the 2022 E-Waste Rules (MoEFCC 2024). OEMs are given annual recycling targets based on the average life of a vehicle. Registered Vehicle scrappage facilities (RVSFs) must report the amount of waste they have recycled. Based on this information, the CPCB issues them with EPR certificates that can be traded with OEMs. As of 2024, EPR certificates are issued only for the amount of steel that is collected and recycled by a RVSF (MoEFCC 2024).

As in the 2022 E-Waste Rules, the Draft End-of-Life Vehicles (Management) Rules, 2024, also mandate RVSFs to recover refrigerants from EOL vehicles but lack further guidance on postrefrigerant recovery stages such as reclamation or destruction, and compliance mechanisms to ensure effective refrigerant management.

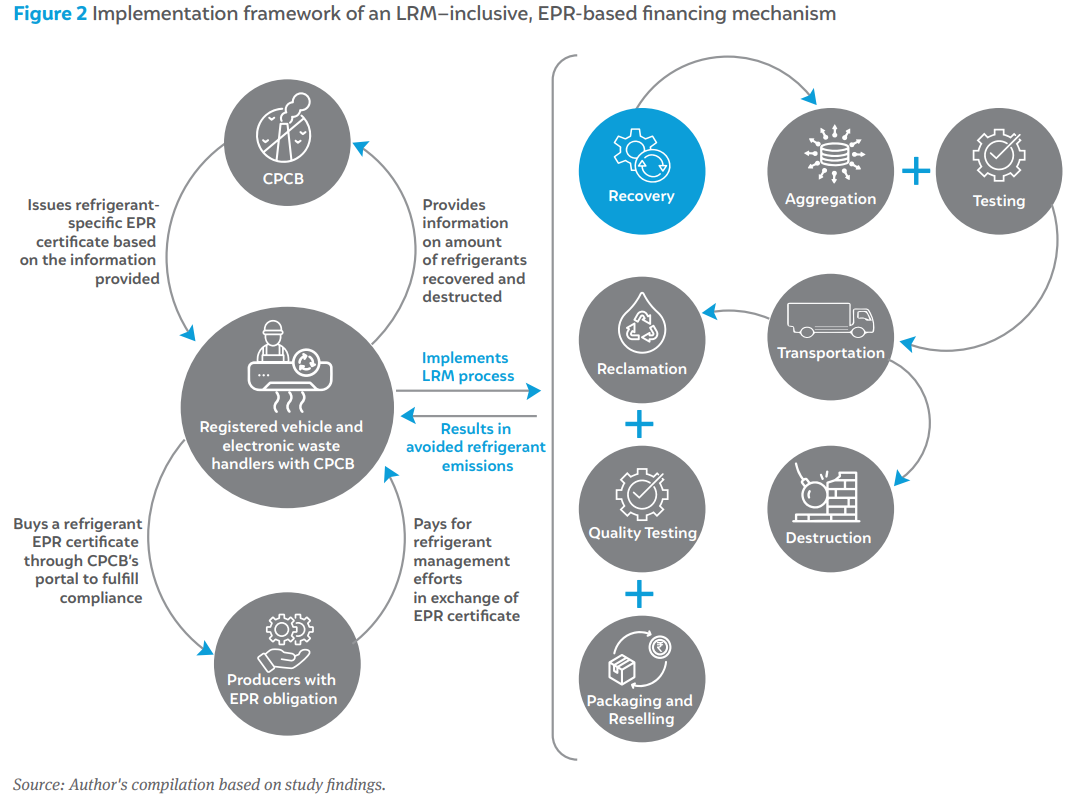

The design and implementation modalities of a potential EPR-based financing mechanism that integrates LRM practices are outlined in Figure 2. This proposed model involves three key stakeholders: electronic and vehicle waste recyclers, producers with EPR obligations, and the CPCB.

The EPR-based model offers several key advantages in terms of financing refrigerant management in India.

Leverages existing regulations and infrastructure

This model leverages the existing 2022 E-Waste Rules and the Draft End-of-Life Vehicles (Management) Rules, 2024, along with established infrastructure and stakeholders involved in electronic and vehicle waste management. This integration streamlines the implementation and reduces the need to create an entirely new framework and a reverse supply chain.

Self-sustained financing mechanism

The mechanism, incorporating refrigerants into the EPR certification process, establishes a self-sustaining financing mechanism driven by the demand–supply dynamic between producers and recyclers. Producers’ obligation to purchase refrigerant–specific EPR certificates will channel funds towards recyclers, incentivising proper LRM practices.

Promotes circularity of refrigerants and the cooling sector

The proposed EPR framework promotes the circularity of refrigerants and the cooling sector. It encourages OEMs to prioritise recovery, reclamation, and destruction of high-GWP refrigerants, thus eliminating waste and promoting resource efficiency. Including LRM requirements in waste management regulations disincentivises OEMs from using high-GWP refrigerants in their cooling products, encouraging a shift towards low-GWP and natural refrigerants.

The Law on Recycling of Specified Kinds of Home Appliances and Law on Recycling End-of-Life Vehicles govern EOL management of electric and vehicle waste and their refrigerants in Japan. The implementation framework differs from that of India because the law in Japan requires end consumers to request and pay retail shops or recyclers to collect, transport, and recycle their decommissioned appliances. However, equipment manufacturers are responsible for aggregating, recycling, or disposing appliances and their components, including refrigerants.

These laws mandate vehicle and electronic waste handlers to recover and store refrigerants before dismantling cooling devices or vehicles at recycling centres. Waste recyclers are also required to send refrigerants for further treatment – reclamation or destruction – at an approved and registered facility. These laws also have reporting requirements. Waste recyclers must maintain comprehensive records of the amount of recovered refrigerants sent for further treatment. Japan has achieved a refrigerant recovery rate of up to 41 per cent from EOL cooling appliances and aims to recover up to 75 per cent by 2030.

Our literature review and discussions with industry stakeholders revealed specific gaps in the current Rules regarding LRM. Additionally, stakeholders – particularly e-waste handlers – highlighted specific challenges to integrating LRM within their operations. To address these issues and create a conducive environment to effectively implement EPR mechanism for LRM practices, we recommend establishing the following enablers.

Make refrigerants a criterion to issue EPR certificates

Mandating the inclusion of refrigerants as a parameter to issue EPR certificates —similar to the four metals under the E-Waste Management Rules, 2022, and the Draft End-of-Life Vehicles (Management) Rules, 2024 —is crucial. It will ensure that producers are directly involved in financing and supporting LRM operations. It will also incentivise recyclers and hold them accountable for properly recovering, handling, and destroying refrigerants extracted from discarded cooling appliances and vehicles. Moreover, establishing this obligation will nudge producers to optimise their refrigerant usage, invest in anti-leakage technologies, and explore low-GWP or natural alternatives.

Publish and enforce comprehensive guidelines and standards

The CBCP should develop clear and detailed guidelines and standards in consultation with industry experts to safely handle, recover (during decommissioning), store, transport, and reclaim or destroy refrigerants. This will help waste handlers build the capacity and infrastructure required to fulfill their compliance requirements. Since stakeholders are likely to be new to LRM practices, the government should set relatively relaxed targets for refrigerant recovery and management as compared to other metals. This will allow stakeholders to gradually build capabilities and infrastructure, making the transition smooth and increasing recovery rates.

Formalise the informal waste management sector and integrate it into both Rules

As per the CPCB, in FY 2020–21, only 26.3 per cent of India’s total e-waste was processed by the formal waste management sector. The rest was either dumped in landfills or was handled by the informal waste management sector (Gupta 2023). Given this, the ambitious target of sustainably managing 80 per cent of the country’s waste by 2027-28 resents manufacturers and recyclers with some complex challenges.

Currently, both Rules only cover registered recyclers and do not account for informal players, who currently form a major chunk of India’s waste management sector. Measures must be taken towards formalisation of the informal sector and their integration into both Rules through incentives and capacity building programmes. This will play a significant role in achieving environment-friendly e-waste handling and recycling, increased EOL refrigerant recovery rates, and broader participation and compliance with the proposed LRM-inclusive EPR model.

Enforce robust monitoring and reporting mechanisms

The CBCP should mandate electronic and vehicle waste recyclers and refurbishers to maintain records and report on the recovery, reclamation, transportation, and disposal of used refrigerants. We recommend regular audits and inspections by the CPCB and concerned authorities of waste management facilities to ensure compliance with LRM implementation guidelines outlined in both the waste management Rules.

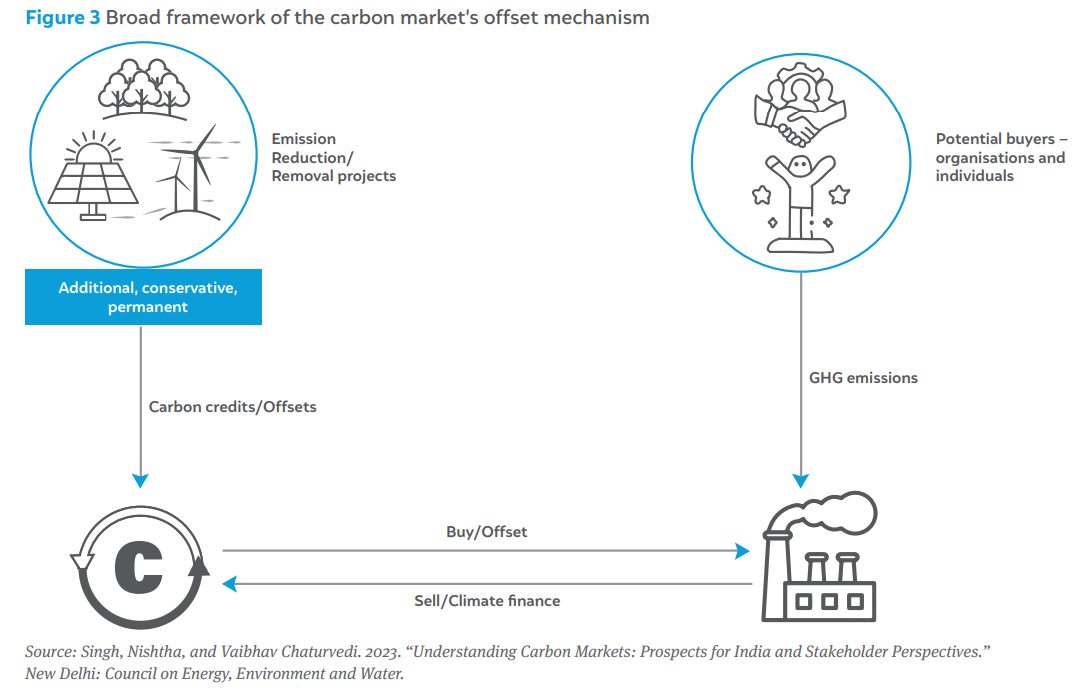

Over the last two decades, the carbon market has emerged as an agent of climate action, providing a mechanism to financially incentivise emissions reductions and mobilise investments in low-carbon technologies and projects worldwide. It can be described as a marketplace where carbon offsets/allowances are traded as a commodity. It exists in two distinct forms: the emissions trading scheme (ETS) and the offset–based approach (Singh and Chaturvedi 2023). The two differ significantly in terms of the fundamentals of their framework, and their operational scope.

Emissions trading scheme

An ETS –also called a cap-and-trade scheme –is a regulatory mechanism where a governing body sets a maximum limit (or cap) on the total emissions that can be generated by a specified group of entities called ‘obligated entities’ (Singh and Chaturvedi 2023).6 This maximum emissions limit is divided among the obligated entities in the form of carbon or emissions allowances. If obligated entities exceed their allocated emissions, they must purchase carbon or emissions allowances from the carbon market. These allowances are sold by obligated entities that have emitted less than the allowed emissions, thus they possess carbon allowances in surplus. This approach is primarily used to reduce emissions in hardto-abate sectors such as steel and cement production and the chemical industry (Singh and Chaturvedi 2023).

In some cap-and-trade schemes, obligated entities are allowed to offset a certain portion of their emissions by purchasing carbon offsets. One example of this is California’s cap-andtrade programme which allows obligated entities to offset 4 per cent of their emissions by purchasing carbon offsets (CARB 2024).

Offset–based approach

The offset approach —also called a baseline-and-credit scheme —is another form of a carbon market. In this approach, private project developers conceptualise and implement a project that emits lesser GHG emissions than the baseline scenario. The baseline scenario is estimated based on the assumption that emissions will be higher in the absence of this proposed project (Singh and Chaturvedi 2023). Emissions reductions achieved through the project are converted into carbon offsets.

The offset approach allows individuals and businesses to reduce their carbon footprint voluntarily by purchasing carbon offsets from project developers rather than attempting to decrease their own emissions. It is important to note that project developers are not obliged to develop emissions reduction projects; they may develop them voluntarily (CF 2021). Moreover, offset purchasers may or may not be mandated by law to reduce their emissions or reduce their carbon footprint.

In November 2024, member countries adopted rules and guidelines to implement Article 6.2 and Article 6.4 of the Paris Agreement at the 29th Conference of the Parties to the UN Framework Convention on Climate Change, which focus on carbon trading through bilateral or cooperative approaches and international market mechanisms (UNFCCC 2024). The Indian government has introduced initiatives to develop carbon markets in the country. To begin, it has finalised a list of activities to be considered for trading carbon offsets under Article 6.2 (MoEFCC 2023d). LRM activity is not included in this list currently, but it may be considered in future revisions.

This report is primarily focused on the voluntary carbon market (carbon offset) mechanism. The subsequent section of this chapter discusses more about how the offset mechanism is implemented and the procedure for generating carbon offsets from emission reduction projects, particularly in the context of refrigerant management. The framework for the implementation of the offset approach is shown in Figure 3.

Due to the high GWP of refrigerants, LRM projects stand to reduce emissions in large quantities, which can then be converted into carbon offsets and sold on the carbon market. For instance, the destruction of only 1 tonne of HFC–410A (hydrofluorocarbons) can prevent up to 2,088 tonnes of CO2–equivalent emissions and can yield up to 2,088 tradeable carbon offsets. Assuming that each carbon offset generated by a refrigerant destruction project was priced at USD 30 per carbon offset in 2022 (UNDP 2023), this project alone could generate revenue of up to USD 62,640.

The revenue generated by selling offsets is significantly more than the total average cost incurred in destroying refrigerants. As per a 2023 study by the German Corporation for International Cooperation, the average cost of destroying refrigerants was USD 30 per kilogram for a low-effort region, and USD 48 per kilogram for a medium-effort region (GIZ 2023). Low-effort and mediumeffort regions refer to how accessible the used refrigerants are for destruction. Low-effort regions include metropolitan areas and medium-effort regions include sparsely populated areas. This estimated cost includes project expenses related to recovery, collection, transportation, and storage. Thus, carbon offsets could be crucial for the financial viability of refrigerant destruction projects that would have otherwise not be undertaken, enabling organisations to overcome economic barriers and contribute to significant emissions reductions.

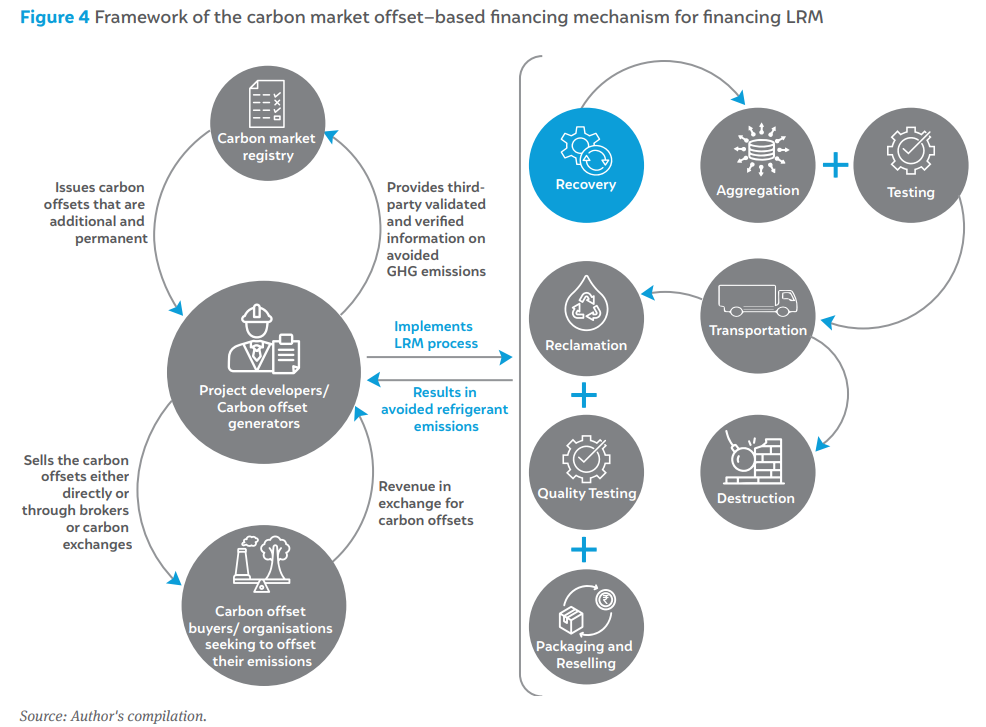

A representation of the framework of a carbon market offset–based financing mechanism for an LRM project is shown in Figure 4.

Voluntary carbon markets are administered by independent agencies called carbon offset programmes. These are organisations that establish the rules, processes, and infrastructure to implement offset mechanisms (CF 2021). They develop and approve methodologies, accredit validation and verification bodies (VVBs), maintain registries, and issue carbon offsets. Examples include Verra, Gold Standard, the Climate Action Reserve, and the Clean Development Mechanism which was developed under the Kyoto Protocol.

Generating carbon offsets through emissions reduction projects —including refrigerant reclamation or destruction projects —involves a series of standardised steps and engages multiple stakeholders (CF 2021). It is governed by stringent principles and methodological approaches to ensure the quality, additionality, and environmental integrity of carbon offsets (ICF 2010).

One of the important criteria for a project to be eligible to generate carbon offsets is the criteria of additionality. Specifically, A project must prove that the emissions reductions it achieves are additional, and this reduction would not have occurred in the absence of the project (Barata 2016). For example, if there is any regulation mandating certain activities for reduction of carbon emission, reductions achieved through those activities cannot qualify for carbon offset. Additionality criteria is critical to the integrity of the offset mechanism.

In case of LRM projects, a project developer could be an entity that directly executes either all or some operations, or it may be an agency coordinating various LRM activities. A project developer could be an e-waste recycler or an EOL vehicle recycler who recovers and collects refrigerants in bulk. It could be an entity managing a destruction or reclamation facility that outsources other LRM activities – recovery, aggregation, testing, and transportation – while bearing the associated costs. It could be a public–private partnership entity that coordinates the implementation of LRM under an EPR/product stewardship system.

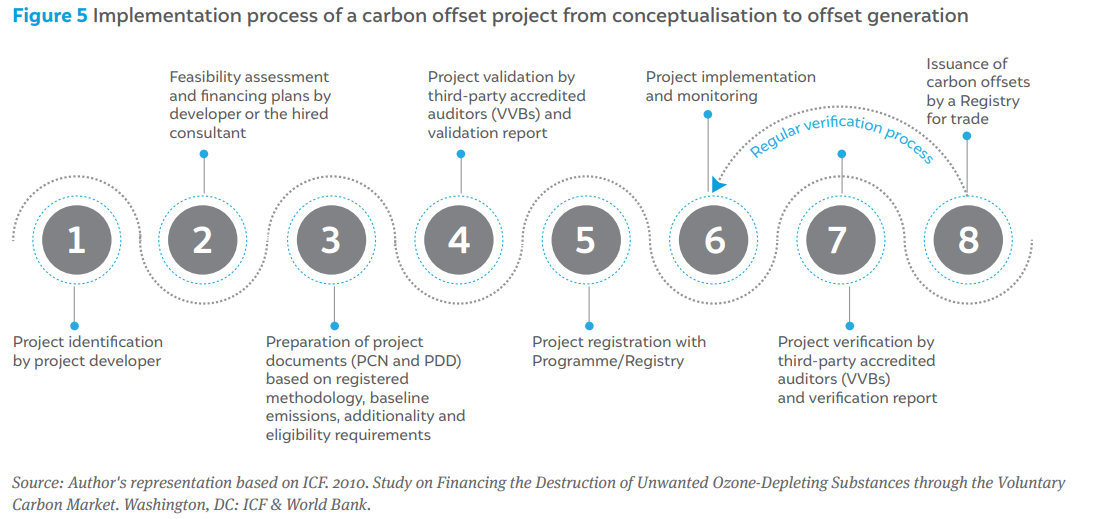

This is the process that a project developer conceptualising and implementing an emissions reduction project must follow. This process is also shown in Figure 5 (CF 2021; ICF 2010).

Step 1: Project and methodology identification

The first step involves identifying a project that can reduce greenhouse gas emissions and a corresponding methodology approved by carbon offset programmes like Verra, Gold Standard, or the American Carbon Registry. The methodologies available for refrigerant reclamation and destruction projects are compared in Table 1.

A project developer must demonstrate that the source of the refrigerants collected for reclamation or destruction is eligible as per the methodology. The project developer must also ensure that the refrigerant type to be processed has been approved for processing under the selected methodology. Not all methodologies are applicable to all types of refrigerants. Finally, a project developer must also furnish documents specifying where and from which application the refrigerants were recovered and processed.

A project developer must determine the project’s additionality. This means that it must demonstrate that the project’s activities, such as refrigerant destruction or reclamation, are not already mandated by Indian law or regulations, and that they go beyond common industry practices. In case the project’s activities are already mandated by law, and the compliance rate is lower than the approved threshold specified in the methodology, the project developer must furnish these details by citing documents published by the government.

In case of a destruction project, the project developer must ensure that the refrigerants are destroyed in facilities recommended by the Montreal Protocol’s Technology and Economic Assessment Panel (TEAP) (TEAP–UNEP 2018).

Step 2: Feasibility assessment and financing plans

This step involves conducting a detailed feasibility assessment of the project, either by the project developer or an external consultant. The assessment should include a financial plan to secure the upfront capital required for the project’s development, a breakdown of implementation and transaction costs, and the potential revenue from selling the carbon offsets.

Step 3: Preparing project documents

Upon finalising the project and its methodology, the project developer prepares project concept notes (PCN) and a project design document (PDD) as per the requirements prescribed in the methodology and the carbon offset programme or registry where the project is to be registered. The PCN and PDD outline the project’s business case, demonstrate its additionality, confirm the applicability of the methodology, and provide estimates of the cost, projected offset generation, potential revenue from carbon offset sales, and other vital details.

Step 4: Project validations by VVBs

Independent, third-party auditors accredited by offset programmes conduct a project validation, which includes reviewing the PCN, PDD, and the project’s compliance with the methodology being used. Their validation report plays a crucial role in confirming a project’s adherence to methodologies and serves as a key document for carbon offset generation.

Step 5: Project registration with the registry

Upon successful validation, the project is registered with the concerned registry to record and trade offsets generated by the project.

Step 6: Project implementation and monitoring

This step represents the actual execution of emissions reduction activities. In this phase, project emissions are monitored as prescribed by the methodology and are then deducted from the baseline emissions to calculate the verified emissions reductions and generate carbon offsets. Project implementation can run for several months or years.

Step 7: Project verification

This involves periodic verification of a project’s implementation by registry–accredited VVBs. Verifications guarantee continuous adherence to the methodology and ensure that emissions reductions are actually happening at the project site. The VVB conducts a thorough evaluation of the project’s performance and submits a verification report to the carbon market registry.

Step 8: Issuing and retiring carbon offsets

Based on the verification report, the registry issues carbon offsets to the project developer. Subsequently, these carbon offsets are eligible for trade to offset carbon emissions. Once offsets are used by companies or individuals, the registry retires them.

The carbon market offset–based financing approach establishes a market-based mechanism for project developers to access financing by generating and selling verified carbon offsets. The carbon market registry acts as the central entity that issues tradeable offsets. The registry enables transparent transactions between parties engaged in this market-based approach to refrigerant management.

Table 1 Comparative analysis of existing methodologies by different registries governing EOL refrigerant management

| Parameters | American Carbon Registry | American Carbon Registry | American Carbon Registry | Verra | Climate Action Reserve | Climate Action Reserve |

|---|---|---|---|---|---|---|

| Methodology | Destruction of Ozone Depleting Substances and High-GWP Foam v2.0 (last revised in 2023) | Destruction of Ozone Depleting Substances from International Sources v1.0 (last revised in 2021) | Certified Reclaimed HFC Refrigerants, Propellants, and Fire Suppressants v2.0 (last revised in 2022) | Recovery and Destruction of ODS (VM0016) v1.1 (last revised in 2017) | U.S. Ozone Depleting Substances Project Protocol (last revised in 2012) | Article 5 Ozone Depleting Substances (last revised in 2012) |

| Eligible gases | CFC, HCFC, HFC | CFC | HFC | CFC, HCFC | CFC, HCFC | CFC |

| Eligible processes | Destruction | Destruction | Reclamation | Destruction | Destruction | Destruction |

| Eligible process technologies | TEAP–approved | TEAP–approved | Any technology, but purity should comply with AHRI8 700 standards | TEAP–approved | TEAP–approved | TEAP–approved |

| Parameters | American Carbon Registry | American Carbon Registry | American Carbon Registry | Verra | Climate Action Reserve | Climate Action Reserve |

|---|---|---|---|---|---|---|

| Eligible refrigerants | 1. Recovered from equipment 2. Government stockpiles |

1. Recovered from equipment 2. Government stockpiles |

1. Recovered from equipment 2. Government stockpiles 3. Recovered from foams |

1. Recovered from equipment 2. Government stockpiles 3. Recovered from foams |

1. Recovered from equipment 2. Government stockpiles 3. Recovered from foams |

1. Recovered from equipment 2. Government stockpiles |

| Eligible sourcing location | USA or Canada | Outside USA | USA, Canada, or Mexico | Parties to the Montreal Protocol | USA | Article 5 countries |

| Eligible processing location | Anywhere | Anywhere | USA, Canada, or Mexico | Parties to the Montreal Protocol | USA | USA |

| Additionality factors | 1. Regulatory surplus 2. Practice-based performance standard 3. If no law, carbon offsets issued for all emissions reductions 4. If law exists with some percentage defined for recovery and destruction, carbon offsets issued only for the emissions that exceed what is required to comply with those laws |

1. Regulatory surplus 2. Practice-based performance standard 3. If no law, carbon offsets issued for all emissions reductions 4. If law exists with some percentage defined for recovery and destruction, carbon offsets issued only for the emissions that exceed what is required to comply with those laws |

1. Regulatory surplus 2. Practice-based performance standard |

1. Legal requirement test 2. If no law, carbon offsets issued for all emissions reductions 3. If law exists with less than 50% compliance rate, carbon offsets issued for emissions reductions that exceed the baseline compliance rate 4. Common practice test |

1. Legal requirement test 2. Performance standard test |

1. Legal requirement test 2. Performance standard test |

| Parameters | American Carbon Registry | American Carbon Registry | American Carbon Registry | Verra | Climate Action Reserve | Climate Action Reserve |

|---|---|---|---|---|---|---|

| Considered baseline emissions | 100% baseline emissions rate for all eligible sources | Ten-year baseline emissions rate for diversified with gases and ranges from 61–95% | 98% baseline emissions rate for all recovered and reclaimed HFCs | 1. In 5 countries, 100% baseline emissions rate at EOL 2. The ten-year baseline emissions rate for stockpiled gas that can be legally resold is 65%. 3. The ten-year baseline emissions rate for stockpiled gas that cannot be legally resold must be calculated based on the quantity leaked between seizure and destruction. |

1. In Article 5 countries, 100% baseline emissions rate at EOL. Otherwise, CAR protocol’s default rates 2. Ten-year baseline emissions rate for stockpiled gas is 65%. |

1. In Article 5 countries, 100% baseline emissions rate at EOL. 2. The ten-year baseline emissions rate for stockpiled gas that can be legally resold is 94%. 3. The ten-year baseline emissions rate for stockpiled gas that cannot be legally resold must be calculated based on quantity leaked between seizure and destruction. |

| Considered project emissions | 1. Transportation 2. Destruction 3. Removal of foam in a non-enclosed equipment de-manufacturing system |

1. Transportation 2. Destruction |

Project emissions are assumed to be negligible | 1. Transportation 2. Destruction 3. Energy consumption |

1. Transportation 2. Destruction 3. Energy consumption |

1. Transportation 2. Destruction 3. Energy consumption |

| Project start date | After complete phase-out | After complete phase-out | Check | After complete phase-out | After complete phase-out | After complete phase-out |

| Standards' own registry system | Yes | Yes | Yes | Yes | Yes | Yes |

| Fees | 1. Account opening: USD 500 2. Annual account fee: USD 500 3. Credit issuance fee: none 4. Project registration fee: USD 1,000 5. ACR VVB fee: USD 2,500 |

1. Account opening: USD 500 2. Annual account fee: USD 500 3. Credit issuance fee: none 4. Project registration fee: USD 1,000 5. ACR VVB fee: USD 2,500 |

1. Account opening: USD 500 2. Annual account fee: USD 500 3. Credit issuance fee: none 4. Project registration fee: USD 1,000 5. ACR VVB fee: USD 2,500 |

1. Annual account fee: USD 500 2. Project registration fee: USD 1,000 3. Credit issuance fee: USD 0.10/credit |

1. Account opening: USD 500 2. Annual account fee: USD 500 3. Credit issuance fee: USD 0.10/credit 4. Project registration fee: USD 1,000 |

1. Account opening: USD 500 2. Annual account fee: USD 500 3. Credit issuance fee: USD 0.10/credit 4. Project registration fee: USD 1,000 |

Source: Author's compilation based on secondary research and stakeholder consultations

Using carbon market offset–based mechanisms to finance LRM practices has certain advantages.

1. Potential to address all sources of refrigerant banks

This approach has the potential to address refrigerant banks from various sources. This includes refrigerants recovered not only from e-waste or vehicle scrappage, but also during servicing operations, in stockpiles of phased-out refrigerants, and other sources. This allows it to be a more comprehensive solution to manage the entire refrigerant bank.

2. Additional source of revenue without burdening the consumer

Unlike EPR or carbon cess mechanisms, wherein the cost of EPR compliance or carbon cess is ultimately accounted in the product price and the cost burden is finally transferred to the consumers, the carbon market stands out as it generate additional revenue through the trade of carbon offsets.

Box 2: Leveraging carbon markets for destruction of ozone-depleting substances (ODS) in Ghana

An example of a project carried out under the carbon market offset approach is Ghana’s CFC–12 stockpiles collection and destruction project developed in 2018. It was the first such project in the country, undertaken by Tradewater in partnership with City Waste Recycling Limited (CWR), (CWR), Ltd. (a recycling centre in Pokuase. The CWR located and collected cans and cylinders of CFC–12 refrigerant dispersed throughout Ghana. In the second stage, CWR recovered refrigerants from EOL refrigerators. Over 15 tonnes of these ozone-depleting refrigerants were shipped to the US for destruction. The project was conducted under Verra’s methodology, which allows project developers to collect and destroy ozone-depleting substances in any country. The project generated more than 150,000 tonnes of carbon offsets.

This section outlines enablers critical in implementing a carbon-offset-based financing approach for operationalising LRM in India and other Article 5 countries.

I. Establish the credibility and integrity of carbon offsets

This is key to securing LRM project financing. Refrigerant reclamation and destruction can result in permanent and verified emissions reductions. This is because, when refrigerants are reclaimed or destroyed as per approved methodologies, it prevents their release into the atmosphere, resulting in real, measurable, and permanent emissions reductions. Thus, it is essential that refrigerant reclamation and destruction projects adhere to internationally recognised methodologies while generating offsets. In addition, stringent monitoring, reporting, and verification (MRV) processes involving accredited VVBs are needed to ensure that the offsets generated are credible and additional.

There have been a few instances where the credibility of a project was compromised, or the emissions reduction was overestimated. One notable example is the HFC–23 destruction project in 2006. Refrigerant manufacturers were caught producing more HFC–23 (GWP 12,400) intentionally to earn more carbon offsets from their destruction, undermining the intended purpose (EIA 2020).

II. Ensure methodologies are inclusive and comprehensive

Most existing methodologies allow sourcing and reclamation or destruction of refrigerants only in non-Article 5 or developed countries. A few others allow sourcing in Article 5 countries but require them to be exported to the US, Canada, or Mexico for reclamation or destruction. Only one methodology (Verra) permits sourcing and destruction in Article 5 countries.

Further, the methodologies do not cover all refrigerant gases. Most of them allow only chlorofluorocarbons (CFCs) and hydrochlorofluorocarbons (HCFCs) to be reclaimed or destroyed, not HFCs.

Also, it is necessary for a project to comply with the additionality criterion, i.e., LRM operations should not be mandated by any existing laws or regulations. Some methodologies approve of project development in regions with low compliance with laws on refrigerant recovery and destruction. For example, Verra’s methodology permits project development if the region’s compliance rate is below 50 per cent. In such cases, carbon offsets are not granted for the entire quantity of emissions reduced by the project. Instead, they are only issued for reductions that exceed the baseline compliance rate. For instance, if the compliance rate in the baseline scenario is assumed to be 30 per cent, offsets will only be granted for the additional 70 per cent improvement over the baseline. This approach accounts for the fact that some level of compliance is expected due to existing rules. Therefore, it only rewards the project for achieving emissions reductions beyond the expected baseline compliance level.

Thus, methodologies need to be more comprehensive in terms of covering a wide range of gases, considering HCFC and HFC phase-out/down timelines, allowing sourcing and reclamation or destruction within the same Article 5 country, enforcing stringent MRV processes, and considering low compliance rates when assessing a refrigerant reclamation or destruction project.

III. Spread awareness and strengthen capacity-building efforts

It is critical to raise awareness among potential project developers, e-waste handlers, and other stakeholders about LRM and the offsets generation opportunities presented by the carbon market and equip them with the skills to avail of them. Knowledge-sharing platforms should be established for project developers, VVBs, and relevant industry professionals to access information on on carbon market offset mechanisms, methodologies, MRV processes, and best practices.

IV. Facilitate cross-border refrigerant movement for reclamation or destruction

As discussed earlier, most existing methodologies require reclamation or destruction to happen in the US, Canada, or Mexico. This is because non-Article 5 countries like the US already have established, efficient, and TEAP–approved infrastructure for refrigerant reclamation and destruction. Hence, in some cases, it may be financially viable for project developers to export the refrigerants collected from one country to another where these facilities are operational.

However, the Basel Convention —which regulates the transboundary movement of hazardous waste —requires mutual consent or agreement between the two countries prior to export of recovered refrigerants, if it is classified as ‘hazardous waste’. This process may involve high administrative efforts, costs, and time delays, which may discourage project developers from pursuing cross-border refrigerant movement for reclamation or destruction. Thus, there is a need to streamline regulations that classify recovered refrigerants as ‘waste’ or ‘hazardous waste’ and establish a formal LRM implementation mechanism that aligns with the goals of the Montreal Protocol, Paris Agreement, and Basel Convention.

Refrigerant management cess —also known as the HFC tax11, levy12 or advance stewardship fee13 —is a policy mechanism to secure funds for financing and incentivising LRM infrastructure and operations (AHRI 2018). It involves levying an extra cess on refrigerants. The cess rate is either based on the GWP of refrigerants (e.g., Norway) or is a fixed flat rate per unit weight of regulated refrigerants (e.g., Canada). Typically, it is charged upstream —levied on high-GWP refrigerant manufacturers and importers – and is eventually passed on to the end consumer. Some countries, such as Norway and Australia, have implemented the cess as a mandatory requirement. Others, such as Canada, allow industries to adopt it on a voluntary basis.

The refrigerant management cess model offers several advantages that make it an effective and practical approach to address the concerns posed by high-GWP refrigerants.

I. Funding for LRM initiatives

Revenue from the collected cess can help support operations and finance the infrastructure required by LRM initiatives. These funds can also be used to manage refrigerant banks that have accumulated during the different stages of ongoing HCFC phase-out (2013-2030).

II. High enforceability and implementation

In this model, refrigerant manufacturers and importers are legally obligated to comply with cess requirements, ensuring high enforceability. Robust MRV mechanisms, and a dedicated administrative entity to govern implementation, will further strengthen this model’s enforceability, ensuring effective LRM implementation and emissions reduction.

III. Supporting the transition to low-GWP and natural refrigerants

The revenue generated by this cess model can play a significant role in facilitating the transition towards low-GWP or natural refrigerants. In turn, this can help India achieve its HFC phase-down target. By providing financial support and incentives, the model can encourage organisations to adopt alternative technologies, promote research and development efforts, and support the phase-down of high-GWP refrigerants in line with the Montreal Protocol’s 2016 Kigali Amendment.

In 2003, Norway began taxing the import and production of HFCs and perfluorocarbons (PFCs) based on their GWP. In 2004, this scheme was amended to include a refund scheme. The Tax and Refund Scheme is specifically designed to finance and incentivise refrigerant management operations.

This tax is levied on businesses that import these gases, since Norway does not produce HFC or PFC. In 2024, the tax rate was set at 1,176 Norwegian krone14 (approximately INR 9,129) per tonne of refrigerant imported, multiplied by its GWP (NTA 2024). The scheme is administered by the Norwegian Environment Agency (NEA), a government agency under the Ministry of Climate and Environment. The NEA ensures that companies that safely refrigerants using approved destruction facilities and technologies with the required documentation are refunded. The refund amount is equal to the tax amount.

The Norwegian Foundation for Refrigerant Recovery (SRG) is the only company that can collect and destroy refrigerants. Through agreements with refrigerant distributors, the SRG has established a refrigerant collection system featuring more than 60 collection centres across the country. The SRG collects waste refrigerants from electronic and vehicle waste handlers and servicing enterprises. To transport used refrigerants to the collection centres, Isovator – an SRG subsidiary – rents refillable cylinders to waste handlers and servicing companies.

Once these companies deposit refrigerants in collection centres, they are sent to the SRG’s centralised facility, where all the cylinders are emptied, and the gases are transferred to a big tank measuring 25 m3 (Asphjell et al. 2023). When this tank reaches a certain weight, the SRG requests the NEA to audit its contents.

To qualify for a refund, companies must ensure that the waste refrigerants are analysed by an independent and accredited laboratory using standardised methods. Isovator is Norway’s only such laboratory. It analyses a waste refrigerant sample from different sources and issues a report on its type, composition, and purity. Once the analysis is completed, the SRG transports the tank to an approved destruction facility in France.

Next, the SRG applies to the NEA for a refund. The refund application includes documentation for each cylinder of gas that was transferred to the tank and destroyed. Upon due diligence, the NEA refunds the tax amount to the SRG. After deducting the costs incurred in aggregating, testing, and transporting waste refrigerants and administrative expenses, the SRG credits the remaining amount to the individuals or companies that recovered the gases and sent them to the collection centres. As of 2022, SRG refunded individuals or companies NOK 300 per tonne of gas (Asphjell et al. 2023).

In principle, any company or person can apply for a refund. However, given the extensive logistics and documentation requirements, only the SRG applies for the refund.

Norway’s Tax and Refund Scheme, Denmark’s HFC Tax, Canada’s Refrigerant Management Canada, and Australia’s Synthetic Greenhouse Gas Levy are a few examples of countryspecific initiatives to impose a cess on refrigerants and use it to finance LRM efforts (AHRI 2018; CCAC 2022).

Generally, the cess is imposed on all refrigerants entering the market, whether in bulk or contained in products. The framework to implement a refrigerant management cess consists of certain steps.

Step 1: Cess rate determination

The cess rate is primarily determined and imposed in two ways.

The cess is charged along with other applicable taxes when refrigerants enter the market.

Step 2: Cess collection and its administration

The administration of the collected cess varies by country. In Norway, for example, customs authorities collect the cess, and the NEA refunds individuals or businesses that have destroyed refrigerants after due diligence. In Canada, it is industry associations that operate the refrigerant cess management scheme (AHRI 2018).

Step 3: Cess utilisation

Regardless of the administering body, it is their responsibility to ensure that the cess is utilised for funding and incentivising refrigerant management efforts and supporting the reverse supply chain of refrigerants. However, countries fulfill this responsibility in different ways. In Norway, the NEA is only responsible for refunding individuals or businesses that provide evidence of the safe destruction of refrigerants using approved destruction facilities and technologies. In Canada and Australia, the administering agency not only collects the cess and but also works with the industry to reclaim or destroy the recovered used refrigerants (RMC 2024). Australia also offers partial refunds to individuals and businesses that recover refrigerants and send them for reclamation or destruction (AHRI 2018).

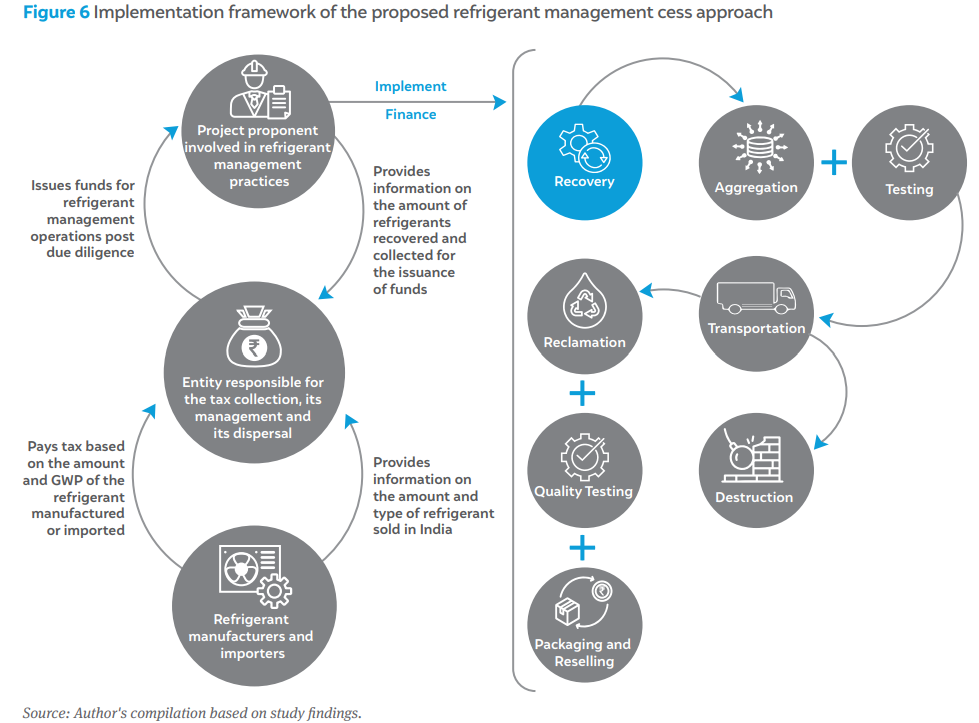

In this section, we propose a refrigerant management cess framework for India by drawing from international examples. Our framework involves three key stakeholders – refrigerant manufacturers or importers, an administrative body, and project proponents – that play a distinct role in the framework’s implementation. This section outlines the specific modalities governing their interactions and responsibilities.

The proposed cess framework require stakeholders to collaborate closely with each other. This section details their distinct responsibilities and interactions.

I. Refrigerant manufacturers/importers

Entities producing or importing refrigerants in India will be subject to a cess determined by the administrative entity. This cess could be calculated based on the GWP of the regulated refrigerant or it could be a flat fee. Manufacturers and importers will be mandated to report their production or import volumes and remit the corresponding cess amount, which will be managed by the administrative entity.

II. Administrative entity

A designated agency under the government or authorised by it will serve as the administrative entity responsible for implementing the refrigerant management cess. This entity will maintain accurate records of the funds collected from manufacturers and importers. It will establish guidelines, regulations, and monitoring mechanisms to ensure compliance and proper reporting by industry stakeholders. The administrative entity will also disburse the collected funds to approved project proponents so that they can implement LRM initiatives. This involves evaluating the project proposals submitted by proponents, ensuring alignment with the LRM programme’s objectives, and allocating funds to eligible proposals.

III. Project proponents

Any individual or company that handles refrigerants can act as a project proponent. Their responsibility is to propose and execute refrigerant management operations. A project proponent can be a servicing technician or enterprise or an e-waste management facility – anyone who has recovered and reclaimed or destroyed used refrigerants that are unfit for reuse. A project proponent may also be a third party hired to assist servicing technicians, e-waste handlers, and servicing enterprises with the logistics, documentation, reclamation, and destruction of refrigerants.

Project proponents must submit detailed proposals and documentation to the administrative entity with the following information:

Upon the administrative entity’s evaluation and approval, project proponents will be eligible for funds to implement their refrigerant management projects.

We identified several challenges in implementing a refrigerant management cess model based on our literature review and stakeholder consultations. To address these challenges, we recommend establishing certain key enablers.

Our recommendations encompass various aspects such as legal and regulatory support, administrative capacity and governance, stakeholder collaboration, incentives and technical support mechanisms, and policy integration. Implementing these enablers is crucial for a conducive ecosystem and long-term sustainability of the proposed refrigerant management cess model.

I. Draft legislations that mandate a cess on high-GWP refrigerants

Legislations must mandate the imposition of a cess on the production, import, or consumption of high-GWP refrigerants. Legislations must outline implementation guidelines and the responsibilities of key stakeholders clearly. This should include defining the scope of the cess – e.g., the types of refrigerants covered – and the basis for determining the cess rate, e.g., GWP, revenue targets, or CO2-equivalent emissions reduction targets. The legislation should also explicitly state that funds collected from the cess must be utilised to finance LRM operations and related initiatives only. This measure is essential to prevent fund misallocation, as witnessed in the case of the National Clean Energy and Environment Fund (launched in 2010), where funds from the coal cess were diverted for purposes other than clean energy initiatives after 2016-17 (SSEF 2018; IISD 2018).

Robust MRV mechanisms must be established as part of the regulatory framework to ensure compliance and accurate data collection from refrigerant manufacturers and importers.

II. Designate an administrative entity for cess allocation and governance

A capable administrative entity with adequate resources, expertise, and authority to manage and administer the refrigerant management cess is essential. This authority should be accountable for administering the cess, maintaining a central registry, and disbursing funds to project proponents for their LRM initiatives.

III. Develop and publish guidelines and standards

Clear guidelines and standards must be developed by the designated government authority in consultation with the Ozone Cell and industry experts. This is critical to ensure that refrigerants are recovered, aggregated, transported, tested, and reclaimed or destroyed safely. These guidelines are also needed to help stakeholders furnish the documents required to comply with the regulations.

IV. Build the capacity of stakeholders

Under this model, only personnel or businesses that are licensed and possess the skills to handle LRM operations will be permitted to carry out such initiatives. Therefore, training programmes must be designed to enhance the technical expertise and capacity of e-waste handlers, servicing individuals, and other project proponents. These programmes will enable them to carry out LRM operations safely and effectively, while adhering to implementation guidelines and standards. They will ensure that LRM operations adhere to guidelines and that all documentation is credible and trustworthy.

V. Harmonise the cess model with existing policies

It is essential to align the cess model with existing policies, laws, and regulations on emissions reduction efforts, potent refrigerants, and tax systems in India. These include the country’s Nationally Determined Contributions, Central Goods and Services Tax Act, 2017, Ozone Depleting Substances (Regulation and Control) Rules, 2000, and E-waste (Management) Rules, 2022. Further, relevant government agencies and industry associations must collaborate closely with each other. These include the Refrigerant Gas Manufacturers’ Association and the Refrigeration and Air-conditioning Manufacturers’ Association.

VI. Foster the buy-in of refrigerant industries and LRM project proponents

India is one of the world’s largest manufacturers and exporters of refrigerants. Manufacturers and importers will be financially impacted by an additional cess. It is also expected to impact OEMs and other industry stakeholders. It is necessary to address their concerns and foster their buy-in with the cess model. It is equally essential to foster collaboration with project proponents such as waste management and LRM entities. We recommend educating stakeholders about the environmental impact of refrigerants and the importance of responsible management practices.

VII. Incentivise compliance with the cess

We recommend providing manufacturers, importers, and OEMS with financial incentives to encourage their compliance with the cess model. These incentives could include tax rebates, technical assistance, or funds to access alternative technologies. Offering financial or technical support to project proponents could catalyse the development of the infrastructure required to reclaim or destroy refrigerants. This is essential to effectively implement LRM initiatives in India.

Securing finance is crucial to addressing the harmful impact of refrigerant emissions. To address this issue, this report explores three promising financing approaches to establish a refrigerant management ecosystem in the country: EPR, the carbon market offset–based mechanism, and a refrigerant management cess. All three financing approaches can potentially finance businesses and stakeholders involved in LRM practices. A viable business model that combines these financing approaches can create a sustainable source of revenue for them.

In addition to implementing a financing mechanism, it is necessary to draft policies to standardise processes, build technical capacity, develop infrastructure and market linkages, and foster awareness among stakeholders – including consumers. In addition, it is essential to harmonise the chosen financing approach with existing regulations relevant to LRM, such as the Ozone Depleting Substances (Regulation and Control) Rules, 2000, E-Waste (Management) Rules, 2022, and Draft End-of-Life Vehicles (Management) Rules 2024.

These measures will enable smooth coordination among stakeholders and effective implementation of LRM practices.

A summary of each financing approach is compared in Table 2.

Table 2: Summary of financing approaches for EOL refrigerant management in India

| Parameter | Carbon market offset mechanism | EPR | Refrigerant management cess |

|---|---|---|---|

| Eligible gases | CFC HCFC after the phase-out target year (2030) |

All types of gases: CFC, HCFC, HFC | All types of gases: CFC, HCFC, HFC |

| Eligible refrigerant sources | Stockpiled, banned gases: CFCs and HCFCs EOL gases Gases recovered during maintenance |

EOL gases from decommissioned cooling systems | Stockpiled, banned gases: CFCs and HCFCs EOL gases Gases recovered during maintenance |

| Ease of implementation | Depends on the voluntary actions and interest of the project developers based on the potential market for used refrigerants and the regulatory ecosystem | Existing e-waste and vehicle recycling and administrative infrastructure can be leveraged to ease and regulate implementation | Extensive process: requires introducing and passing a bill and creating an administrative body to overlook the scheme |

| Government involvement | Low, since it comprises—in most cases—private firms interested in purchasing carbon offsets, voluntary project developers, and a private carbon market registry | Moderate, since government agencies role is to monitor and enforce compliance while the implementation will be done mostly by the private sector. | High, since government departments that administer taxes, import of refrigerants, and pollution must collaborate to implement the scheme |

| Funding | Companies willing to reduce their carbon emissions by purchasing carbon offsets | Equipment manufacturers when they purchase EPR certificates | Cess levied on refrigerant import and production |

| Stakeholders | Project developers E-waste handlers Servicing enterprises Carbon credit purchasers |

E-waste handlers CPCB Equipment manufacturers Servicing enterprises |

Refrigerant importers and producers E-waste handlers Servicing enterprises Government administrative entities |

| Incentive mechanism | Project developers and stakeholders are eligible for carbon credits when they take up LRM initiatives | Recyclers are eligible for EPR certificates EPR targets drive producers to optimise refrigerant usage, invest in anti-leakage technologies, and explore low-GWP alternatives |

Incentivises companies and individuals willing to reclaim or destroy refrigerants after its recovery |

| Enforceability | Low, since the government is not involved | High, since producers are obligated by law to purchase EPR certificates in proportion to their annual recycling targets | Moderate to high, based on the other supporting policies mandating refrigerant management at EOL, e-waste, and ODS |

Source: Author's compilation.

It is important to note that any financing approach should prioritise incentivising servicing technicians and waste handlers – key stakeholders responsible for refrigerant recovery at the ground level. Providing them with training, equipment, and financial incentives can significantly improve recovery rates and reduce intentional venting.

In conclusion, addressing the challenge of refrigerant management in India requires a comprehensive and multifaceted approach. By adopting such an approach, India can not only mitigate the environmental impact of refrigerant banks but also contribute to the global effort to combat climate change and protect the ozone layer.

Building a Climate Conscious India: Scalable Solutions for a low carbon built environment

Activating Circular Economy for Sustainable Cooling

Activating Circular Economy for Sustainable Cooling

Activating Circular Economy for Sustainable Cooling