Council on Energy, Environment and Water Integrated | International | Independent

Context: India and the US signed a Critical Minerals Agreement in May 2026 to strengthen cooperation across mining, processing, recycling, and investment in critical minerals.

CEEW analysis: Both countries face similar vulnerabilities in processed critical minerals and remain heavily dependent on concentrated global supply chains for processing technologies, equipment, and inputs.

Recommendation: The India-US partnership should prioritise joint R&D, commercialisation financing, and public-private processing facilities to build resilient processing capabilities.

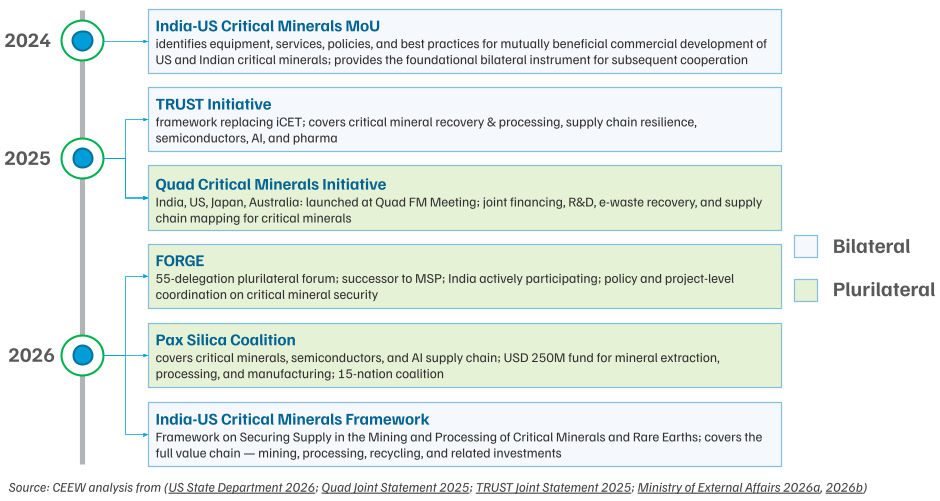

India and the United States (US) have built a cohesive diplomatic architecture around critical minerals in recent times. The bilateral Critical Minerals Agreement (CMA), signed in May 2026, on the sidelines of the Quad Foreign Ministers' Meeting in New Delhi, formalises cooperation across the critical mineral value chain, from mining and processing to recycling and investments. It follows India’s endorsement of the Forum on Resource, Geostrategic Engagement (FORGE), a 55-country successor to the Mineral Security Partnership, and sits alongside multilateral initiatives such as Pax Silica and the Quad Critical Minerals Initiative (Figure 1).

Figure 1: India-US cooperation reveals a mature diplomatic relationship around critical minerals

India has vast raw mineral endowments, particularly rare earths, graphite, and titanium. The US, too, has substantial reserves of copper, lithium, and beryllium, among others. However, upstream mining projects — from exploration to mining and then processing — tend to take 10–12 years to reach maturity. Meanwhile, what manufacturing industries need are refined and processed, or industry-grade, mineral products. The challenge, as well as the opportunity, for India and the US goes beyond securing raw mineral supply for the future, to generating industrial demand for processed minerals currently.

For this partnership to see significant success, it would help both India and the US to consolidate their resources in the midstream of the mineral supply chain. In practice, such prioritisation would involve creating an ecosystem for producing processed minerals by increasing technical capabilities to foster innovation, supporting the commercialisation of locally-developed processing technologies, and co-financing public-private processing facilities.

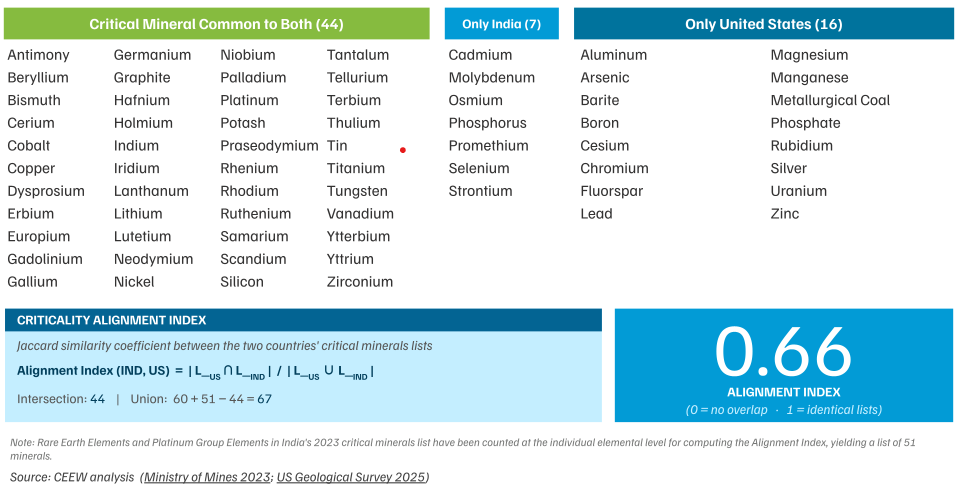

Both India and the US are heavily dependent on imported processed critical minerals for industries central to their economic and strategic interests: semiconductors, defence, and clean energy infrastructure. Their exposure to risk is structurally similar. Analysis by the Council on Energy, Environment and Water (CEEW) reveals a Criticality Alignment Index of 0.66 between the two countries, reflecting the fact that 44 of 67 unique minerals on their respective critical minerals’ lists are mutually classified as critical (Figure 2).

Figure 2: 44 of 67 unique minerals are mutually critical to India and the US

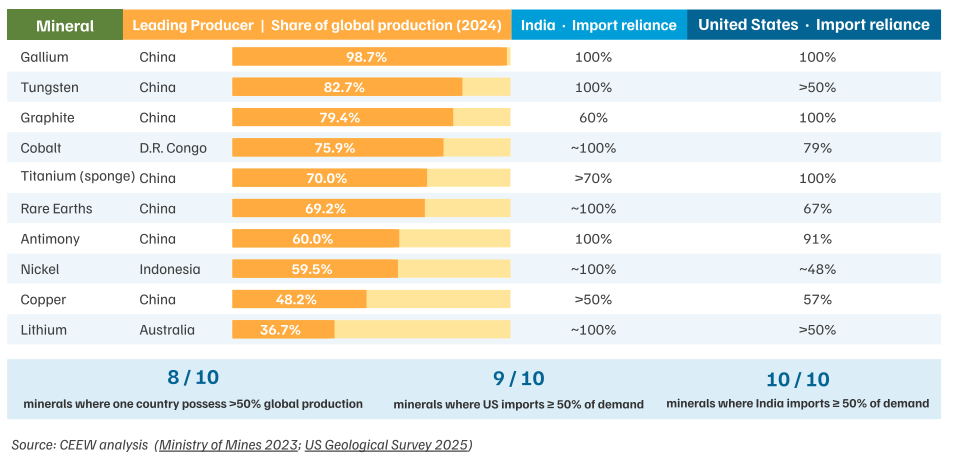

Both countries also lack the midstream capabilities to process critical minerals independently. Specialised mineral processing equipment, chemical reagents, and separation technologies are themselves heavily import-dependent and concentrated. China, for instance, controls over 60 per cent of global production of gallium, graphite, and rare earths (Figure 3). India predominantly sources high-precision analytical and processing instruments from China, alongside Japan, Germany, and the US, with commercial procurement facing long lead times and elevated operational costs. The US imports the same from these suppliers as well as from Nordic countries like Finland, Sweden, and Denmark.

The fragility of this arrangement was made visible in October 2025, when China imposed export controls on rare earth processing equipment and magnet-manufacturing technology. These controls are currently suspended, but the legal authority for their re-imposition remains intact. For supply chain planners in both countries, the episode highlighted that midstream capability vulnerabilities require immediate addressing.

Figure 3: Both India and the US import at least half their demand for 9 of 10 mutually critical minerals, mostly from a single producer

India's National Critical Mineral Mission (NCMM) has a combined financial outlay of INR 34,300 crore to support projects across the value chain, including refining and processing, over seven years. Meanwhile, the US has rolled out over USD 30 billion through direct equity, public procurement, and stockpiling mechanisms, alongside an Executive Order integrating import adjustments of processed minerals with domestic industrial requirements. These instruments are complementary. The 2026 CMA creates the institutional basis to align them. Three priorities can make that alignment operational.

Since production of refined rare earth metal and platinum group elements at a commercial scale is largely absent in both countries, a bilateral R&D programme structured across two tracks — frontier research and consolidation pilots — could address both the knowledge gap and the issue of scaling up.

The frontier track, anchored through TRUST (Transforming the Relationship Utilizing Strategic Technology), an initiative steered by the National Security advisors of both countries to stabilise AI supply chains, could focus on acquiring AI-related minerals where global leadership has yet to emerge. This includes research on processing efficiency and technologies that are still evolving, such as material substitution of compounds — Silicon carbide and Gallium nitride — used to manufacture semiconductors.

The track could also focus on lanthanum-cerium-based magnets, which require light rare earths that are abundant in India. These could be an alternative to the risk-prone supply chain of rare earth permanent magnets (REPMs). Such projects can also include sodium-ion formulations and other alternative battery chemistries that reduce exposure to constrained lithium and cobalt supply.

The consolidation track could focus on taking frontier-track outputs to pilot scale, testing their commercial viability under realistic production conditions. Circular economy applications, particularly advanced recovery technologies for complex alloys at the end-of-life stage, are a strong candidate for early consolidation pilots, since both countries have in-use stocks of critical minerals embedded in power grids, vehicles, and electronics that will require managed recovery. Joint in-use stock modelling, to estimate the scale and timing of these secondary flows, could also strengthen both countries’ long-term structural planning.

The critical minerals processing technologies face a commercialisation problem that private capital cannot resolve on its own. The ramp-up from pilot to commercial typically takes one to three years, during which predictable downstream demand and standardised production specifications allow investors to absorb stabilisation risk, in the case of bulk minerals processing. Critical mineral processing offers no such predictability. Specifications for battery-grade lithium chemicals and high-purity rare earth outputs continue to evolve; commercial-scale know-how is scarce; and demand uptake is structurally uncertain given global mineral pricing. The result is a financing gap that blocks technically viable projects from reaching commercial operation.

The Lynas Rare Earths — Australia-owned, US-funded — example illustrates how effectively designed state interventions can bridge this gap. The Lynas processing facility in Kuantan, Malaysia, took close to three years to reach 75 per cent of its capacity, requiring additional convertible bond financing during the ramp-up itself. Building on this experience, the US has since increased its support for Lynas for its heavy rare earth expansion at Seadrift, Texas, poised to produce Neodymium-Praseodymium (NdPr) oxide, the key input material in REPMs. By funding construction, guaranteeing a USD 110/kg floor price, and entering into an offtake agreement, the US is removing revenue uncertainty and ensuring demand. This is precisely the bundle of stabilisation guarantees that allows a facility to operate through the ramp-up period without private financiers exiting. The US-MP Materials deal is another example of the US focusing on building domestic midstream capacity.

A joint India-US financing mechanism should be structured to absorb such stabilisation risks for first-of-its-kind processing facilities with ensured demand. It can draw on the US’s critical minerals financing and India’s NCMM capital. The mechanism could be fiscally bound and tied to clear performance benchmarks — output volume, purity specifications, and ramp-up timelines — to prevent open-ended public exposure.

The sustenance of processing facilities depends on reliable input supply chains. Chemical reagents, such as the acids, solvents, and extractants used in hydrometallurgical processing, are themselves heavily imported. The global mining chemical market is projected to grow from USD 8.2 billion to USD 11.1 billion by 2034, and increasing capacity in co-manufacturing these chemicals and reagents alongside processing facilities would enable both countries to benefit from this market.

The CMA provides a framework to structure such joint public-private projects. The US has already operationalised this model through various CMAs with Ukraine, Malaysia, Japan, Australia, and the European Union. The Alcoa-JAGA gallium project in Western Australia — projected to account for 10 per cent of global gallium supply — demonstrates that such arrangements can rapidly move from agreement to operation. From the signing of the Joint Development Agreement in August 2025 to government financing commitments by October 2025, the project advanced through key milestones in under three months. Australia has committed USD 200 million in concessional finance. The US, through a joint special purpose construction vehicle, and JAGA, a Japanese government and Sojitz Corporation joint venture, will fund and build the facility. A final investment decision and production commencement are both targeted for 2026. While the project is yet to reach commercial operation, the speed of its multilateral structuring, driven by shared urgency around China's gallium export controls, is itself the instructive precedent.

India can amplify the reach of bilateral projects by leveraging its membership in US-led multilateral platforms. The USD 250 million Pax Silica Fund, which covers critical minerals extraction, processing, infrastructure, and manufacturing assets, is directly relevant to co-processing facilities. Configurations through the Quad Critical Minerals Initiative, harnessing Japan’s processing technologies and Australia’s resource base, would extend India’s effective partnership network beyond what a purely bilateral framework could offer.

Neeraja Kulkarni is a Research Analyst, and Sunil Kumar is a Programme Associate at the Council on Energy, Environment and Water (CEEW). Send your comments to [email protected].

Add new comment