Council on Energy, Environment and Water Integrated | International | Independent

Context: India achieved 20 per cent ethanol blending in petrol in March 2025, five years ahead of target. The Ministry of Road Transport and Highways (MoRTH) is now considering E85 and E100 flex-fuel vehicles.

CEEW analysis: Public spending on ethanol production extends well beyond what oil marketing companies pay for procurement; production costs differ substantially by feedstock; and petrol demand is expected to peak and then decline sooner as electric vehicle adoption grows.

Recommendation: As blending volumes grow, the programme’s next phase can be strengthened by publishing annual estimates of its total public expenditure, planning ethanol capacity in step with petrol demand and electric-vehicle adoption, and periodically reassessing feedstock incentives against food security, water use, and fiscal objectives.

India reached 20 per cent ethanol blending in petrol five years ahead of schedule. This is a major energy security milestone. Since 2014, the Ethanol Blending Programme (EBP) has mixed ethanol, an alcohol made from crops like sugarcane and maize, into petrol so that part of the petrol sold is homegrown and not imported. This has helped the government in its attempt to build a domestic fuel source and has created an additional market for agricultural produce such as sugarcane, maize, and surplus rice. Countries like Brazil and the United States have long relied on high ethanol blending mandates of up to E85 (85 per cent ethanol) and E100 (nearly pure ethanol). So far, according to the Indian government, the EBP has substituted ~270 lakh metric tonnes of imported crude oil, saved roughly INR 1.59 lakh crore in foreign exchange, and paid INR 1.18 lakh crore to farmers across states like Uttar Pradesh, Maharashtra, and Karnataka.

But the next phase is not more of the same. In April 2026, the Ministry of Road Transport and Highways (MoRTH) released a draft notification to recognise flex-fuel vehicles running on E85 (85 per cent ethanol) and E100 (nearly pure ethanol), and ~48 retail outlets of public oil marketing companies started rolling out E85 fuel in June 2026. Existing E20-compatible vehicles cannot run on E100 without changes to engine calibration and fuel-system components. Higher blends, therefore, require dedicated flex-fuel vehicles, new consumer demand, and a larger ethanol supply base. Analysis by the Council on Energy, Environment and Water (CEEW) in this blog considers financing, resource implications, and market viability to identify four issues that merit closer examination.

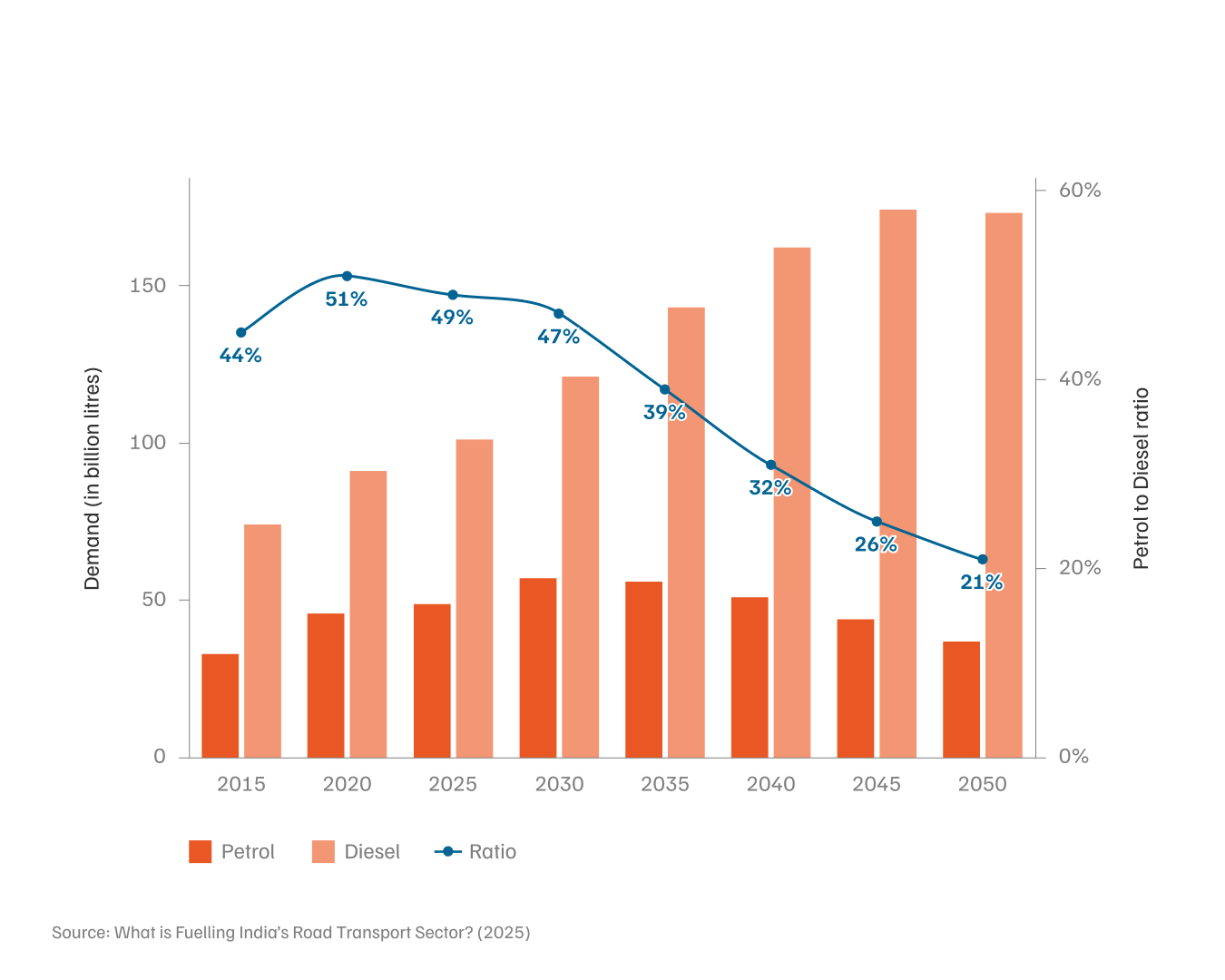

If E20 blending continues and flex-fuel vehicles account for even 20 per cent of new vehicle registrations by 2028, India’s ethanol demand could rise from around 1,016 crore litres in 2025 to about 1,600 crore litres by 2028 — an increase of more than 50 per cent. India’s installed ethanol production capacity, currently ~1,700 crore litres, could theoretically meet this demand in the near term.

But the longer-term outlook is more uncertain. CEEW’s transport fuel modelling suggests that petrol demand could peak at ~5,700 crore litres by 2032 before falling to 3,700 crore litres by 2050, as two- and four-wheelers shift towards electric vehicles, which are cheaper to own and operate. Ethanol plants are long-lived assets with operating lives of 20 to 30 years. Capacity additions made now could face a shrinking market within a decade, creating the risk of stranded investments.

To mitigate this risk, the government has proposed blending isobutanol — a derivative of ethanol — with diesel to extend the programme’s relevance to heavy-duty vehicles, which may continue running on diesel till the 2040s. This proposal is still early-stage: long-term trials have yet to establish its performance and reliability in heavy-duty use, and, because isobutanol requires further processing of ethanol, it is likely to carry a higher per-unit cost than existing blends.

Figure 1: Falling petrol demand can leave ethanol plants stranded with excess capacity

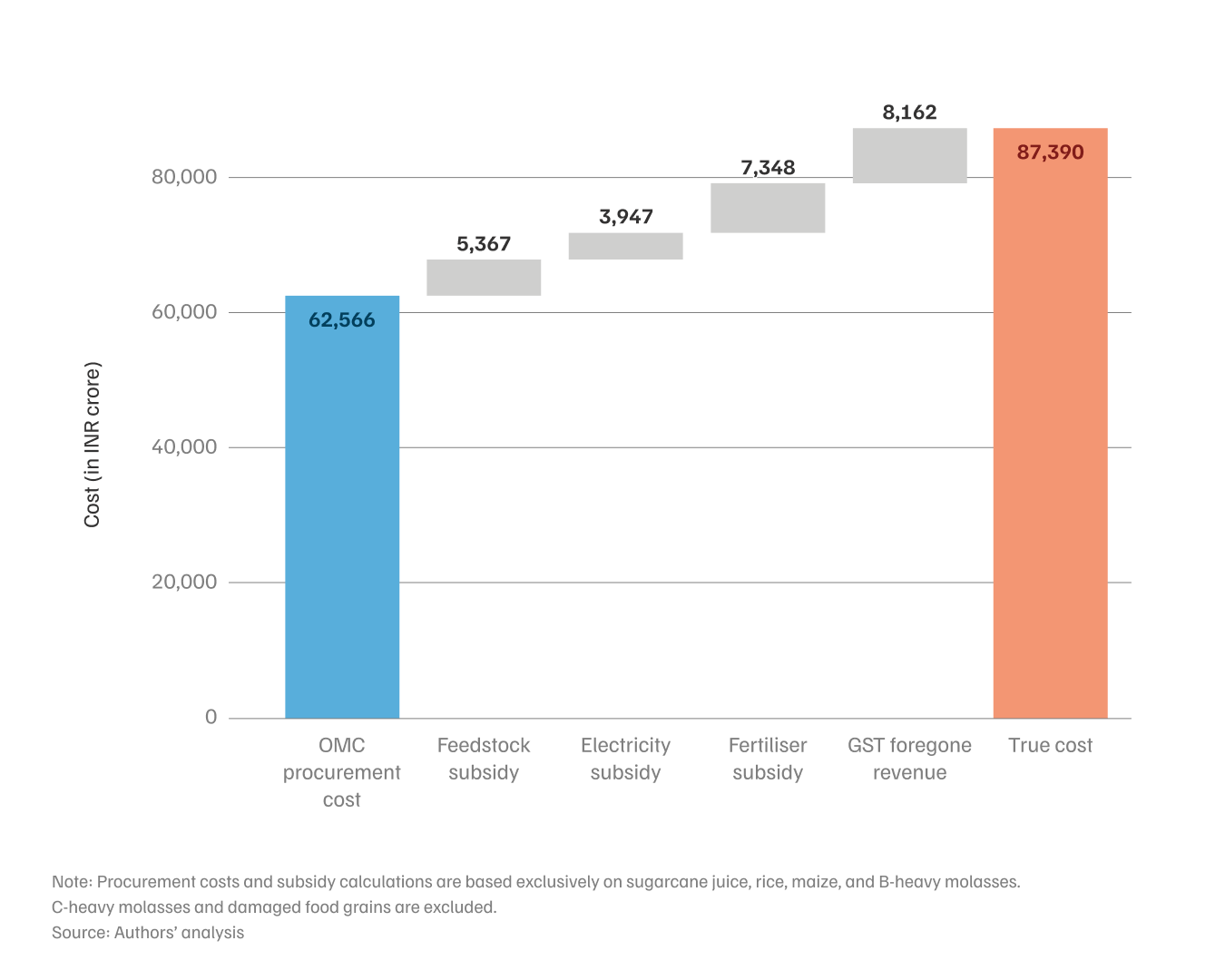

The OMC (oil marketing companies) procurement price of ethanol does not capture the full fiscal cost of the programme. When feedstock subsidies, electricity subsidies, fertiliser subsidies, and foregone GST revenue are aggregated, the true cost of ethanol procurement in ESY 2024–25 was approximately INR 87,390 crore, as compared to the OMC procurement cost of INR 62,566 crore. The gap of approximately ~24,824 crore represents additional public expenditure or foregone revenues, with fertiliser and electricity subsidies accounting for approximately 46 per cent of this additional outlay. Therefore, an increase in ethanol demand to 1,600 crore litres by 2028 (as projected) would lead to an even higher public expenditure/foregone revenues amounting to ⁓INR 38,226 crore (notwithstanding any future increases in procurement cost).

Note that, while the effective retail selling price of ethanol is the same as petrol (as it is blended), this additional fiscal expenditure is only partly recovered by the government through the 5 per cent GST levied on the price of ethanol (and smaller recoveries from freight, etc.).

Figure 2: True cost of ethanol procurement, ESY 2024–25 (INR crore)

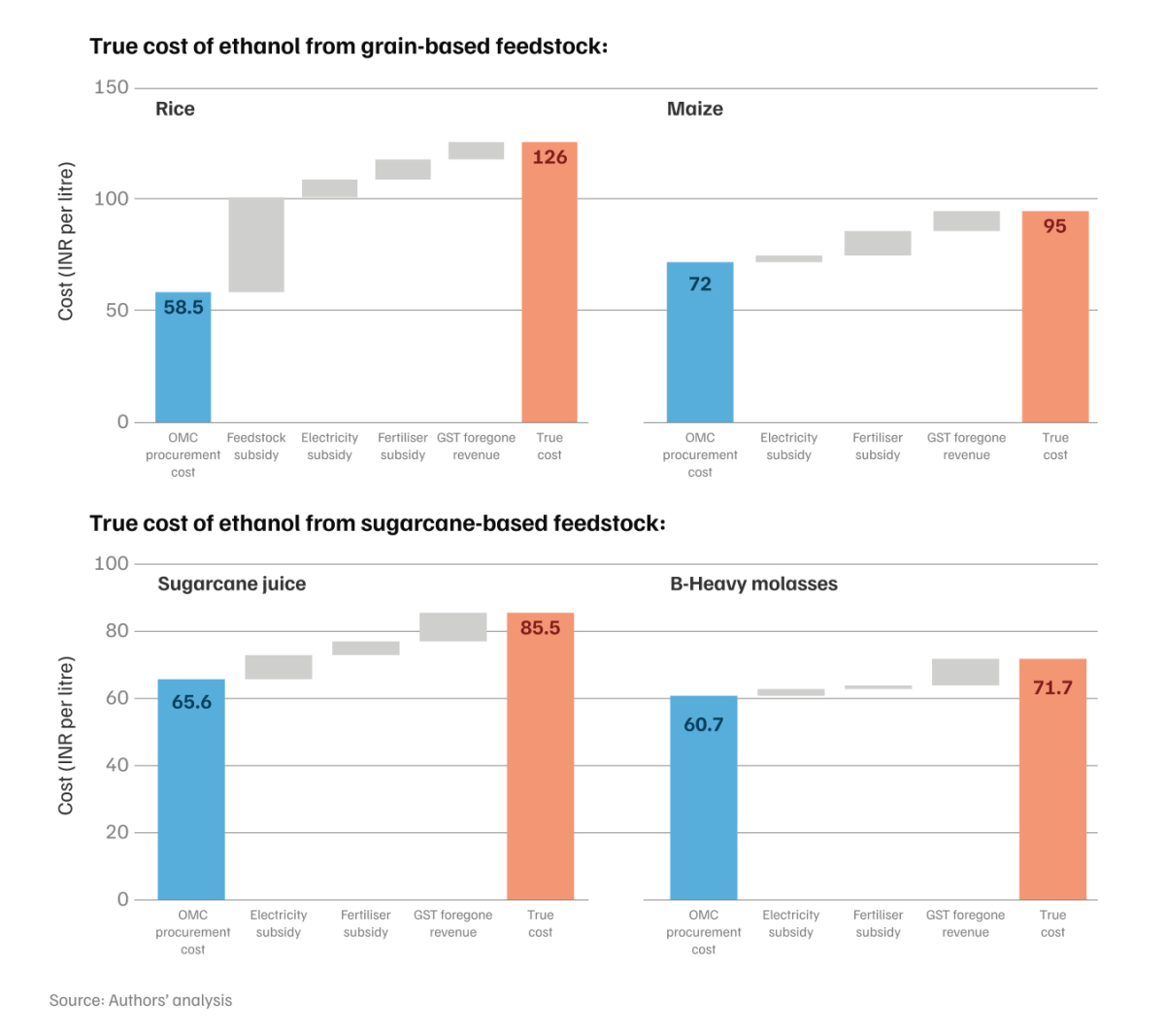

Feedstock choice shapes this cost sharply. For instance, rice-based ethanol has a true cost of ~INR 126 per litre, more than twice the oil marketing company procurement price of INR 60 per litre. Maize-based ethanol costs ~INR 95 per litre. Sugarcane juice and B-heavy molasses remain the lowest-cost options at INR 85.5 per litre and INR 71.7 per litre respectively.

Yet India’s feedstock mix has shifted towards grains in recent years. That shift has direct implications for the programme’s fiscal footprint.

Figure 3: A shifting feedstock mix has material implications on fiscal footprint

Flex-fuel vehicles—vehicles designed to run on more than one type of fuel using a single fuel tank and engine—are unlikely to be cost-competitive without additional support.

Ethanol has ~28 per cent lower gross calorific value than petrol. Although ethanol’s higher octane rating allows engines designed for it to operate more efficiently and resist engine knocking, this efficiency gain does not fully offset its lower energy content. As a result, vehicles running on ethanol typically deliver 20–25 per cent lower fuel economy per litre, raising the effective fuel cost per kilometre despite any pump-price advantage. CEEW’s total cost of ownership (TCO) analysis for four-wheelers in 2028 tested three pricing scenarios across six states. At current retail prices, petrol is 2 to 14 per cent cheaper than flex-fuel (E100). At OMC procurement prices, petrol is ~15 per cent cheaper. At the true cost, petrol is 15 to 25 per cent cheaper than ethanol.

For flex-fuel vehicles to reach parity with petrol, ethanol would need to retail at ~INR 52 to ~INR 73 per litre across states. This is well below the production cost of any commercially viable feedstock assessed. Reaching a 20 per cent market share for flex-fuel vehicles in the petrol segment could require an additional INR 3,500 crore to bring their Total Cost of Ownership (TCO) on par with standard petrol cars.

Electric vehicles offer a useful comparison. They already have lower running costs across passenger categories and could deliver higher CO₂ savings per rupee of public expenditure. This does not eliminate ethanol’s role, especially in segments (like heavy-duty transport) where electrification may take longer, but it does mean ethanol capacity should be planned alongside other clean mobility pathways.

India’s ethanol programme relies almost entirely on first-generation (1G) feedstocks such as sugarcane, rice, and maize. Expanding to higher blends could intensify pressure on food systems, land use, and water resources.

In the Ethanol Supply Year 2024–25, the government allocated ~52 lakh metric tonnes of surplus Food Corporation of India rice, released below the minimum support price, for ethanol production. Rice remains central to India’s food security and is a staple for lower-income households. Continued diversion at this scale risks affecting prices and availability.

Maize is also seeing stronger demand signals. In the 2025–26 kharif season, maize cultivation rose by ~9 lakh hectares, while oilseed area declined. Higher maize-based ethanol prices (which grew at 11.7 per cent annually between 2022 and 2025) could pull farmers away from pulses and oilseeds, deepening import dependence and complicating India’s crop diversification goals.

Feedstock choices also have implications on water available for agriculture. Paddy cultivation remains a primary driver of groundwater depletion in Punjab and Haryana, both regions identified as critical in India’s National Water Mission. Sugarcane and maize are also water-intensive feedstocks, requiring ~210 litres and ~500 litres of water per kilogram of feedstock, respectively. This matters for states like Maharashtra, where sugarcane cultivation is expanding in regions with varying water availability across districts. Scaling up rice-based ethanol for higher blends without accounting for regional water stress could therefore exacerbate scarcity in already vulnerable districts.

Ethanol blending has delivered real gains for energy security and rural incomes. But its next phase should be planned with clearer accounting and sharper trade-off analysis before further expansion:

India’s Ethanol Blending Programme has been a genuine success in energy security and rural economic development. Its next phase deserves the same care that brought the first phase its credibility, anchored in a clear-eyed view of what ethanol really costs and how that sits alongside India’s clean energy transitions.

With inputs from Sabarish Elango, Shalu Agrawal, Karthik Ganesan, Hemant Mallya and Chandan Jha.

Dharshan Siddarth Mohan is a Programme Associate, Aishwarya Joshi is a Programme Associate, and Kushi Naidu is a Consultant at the Council on Energy, Environment and Water (CEEW). Send your comments to [email protected].

Add new comment