Council on Energy, Environment and Water Integrated | International | Independent

Suggested Citation: Singh, Rashi, Disha Agarwal, and Vishal Tripathi. 2026. Contracts for Difference for Flexible and Affordable Clean Power: India’s Pilot and Path to Scale. Council on Energy, Environment and Water.

India’s power system is entering a new phase of transition. The challenge is no longer only to add renewable energy capacity, but to ensure that clean power is available at affordable prices when the system needs it most. As peak demand rises, renewable energy integration deepens, and storage becomes increasingly important, India will need market-linked instruments that can balance investor certainty with flexible, cost-effective procurement.

This issue brief examines India’s first Contract-for-Difference (CfD) pilot for renewable energy and storage, approved by the Ministry of New and Renewable Energy in 2026 and implemented by the Solar Energy Corporation of India. The pilot marks an important shift from long-term, capacity-based procurement towards market-linked procurement of clean power during evening peak-demand hours.

CfDs can help de-risk investments in merchant renewable energy and storage by providing developers with partial revenue certainty while retaining exposure to wholesale market prices, dispatch signals, and buyer preferences. The brief analyses the pilot’s design, its implications for wholesale power markets, and the market architecture required to scale CfDs in India.

The study also draws lessons from Global markets, including the United Kingdom, European markets, Japan, China, and Australia, to identify how India can strengthen pricing benchmarks, manage long-term price risk, attract buyers, build self-sustaining settlement mechanisms, and enable aggregators and traders to support market participation.

Over the last decade, countries have attracted investment in renewable energy (RE) through feed-in-tariffs, premiums and competitive auctions, resulting in longterm assured offtake contracts. However, with the rapid ingress of solar and wind across grids and changing electricity demand patterns, these routes are no longer sufficient to ensure an affordable supply mix. Marketlinked revenue mechanisms are becoming important. The International Energy Agency (IEA) estimates that merchant capacities, corporate contracts, and utility contracts could account for nearly 30 per cent of global RE growth until 2030.

Our analysis suggests that India’s first Contract-forDifference (CfD) pilot tender, launched in April 2026, can help de-risk investments in merchant renewable energy and storage and enable utilities to procure clean power during evening peak-demand hours. CfD, a financial contract that guarantees a generator an agreed strike price, helps manage this transition by giving clean-power developers partial revenue certainty while still exposing them to market prices, dispatch signals, and buyer preferences. It will also help increase volumes in the wholesale power market, which is essential for cost-effective RE integration.

To scale market-based transactions, India must strengthen price discovery for short-term procurement, expand buyer participation in wholesale markets, develop financial products to manage risk for merchant power developers, and rethink market design to reward capacities for being available and flexible. India’s pilot holds relevance for other developing power markets, where renewable energy procurement is still dominated by long-term bilateral contracts, wholesale markets remain shallow, and governments are seeking ways to procure clean, flexible power without assuming openended fiscal liabilities.

Power systems across the world are entering a new phase of transition. The challenge has shifted from adding more renewable energy capacity to ensuring clean power is available at reasonable costs when the system needs it most (IEA 2024). This is particularly relevant for developing and emerging and developing economies (EMDEs) experiencing rapid electrification, industrial growth, rising cooling demand, and increasing variable renewable energy output, all of which require highly flexible power systems (IEA 2025a; IEA 2025b). Countries are now being forced to rethink electricity procurement frameworks that were primarily designed for conventional firm power generators, such as coal and nuclear, or must-run solar and wind.

India offers an important case study in this transition. Its peak power demand exceeded a record 270 GW in May 2026, 8 per cent higher than the previous peak (according to Ministry of Power data). In many of its large states, the peak power demand has grown faster than total annual energy demand, according to the Bureau of Energy Efficiency (BEE)’s analysis of the Central Electricity Authority (CEA)’s data (Bureau of Energy Efficiency 2024). The challenge is the widening gap between this growing peak and average demand, compounded by intra-day and seasonal variations in RE generation. Firm or inflexible capacity built to meet short periods of high demand sits underutilised for most of the year, raising system costs and, ultimately, consumer tariffs.

In the last two decades, India has quadrupled its installed power generation capacity to fuel a rapidly growing economy (CEA 2025; Ministry of Power 2025). This expansion was enabled largely through long-term power purchase agreements (PPAs), which provided assured payments and reduced investment risk for coal-based plants. In the renewables sector, competitive auctions with 25-year PPAs led to sharp tariff declines and rapid capacity additions (Kanika Chawla et al. 2019). However, while this model was effective for scaling supply, it is less suited to today’s dynamic demand patterns. Long-term PPAs lock in generation capacity for decades regardless of when electricity is actually needed. They are designed to meet expected baseload demand, not respond flexibly to short-term peaks or increasing uncertainty in consumption patterns.

This is where the Government of India’s push towards Contracts-for-Difference (CfDs) for RE and storage in March 2026 becomes significant (MNRE 2026). Complementing traditional long-term PPAs, India’s CfD design can channel flexible, demand-responsive clean power into wholesale markets. It will provide revenue visibility for clean energy generators in the absence of assured offtake contracts, while enabling utilities and corporates to buy power at competitive, market-reflective prices on power exchange platforms.

Several mature power markets, including the United Kingdom (UK) and parts of Europe, adopted CfDs as instruments to attract investment in renewables starting in 2013-2014, when the technology was nascent, and costs were high (Oxford Institute for Energy Studies 2024). This issue brief examines the innovative design and prospects of India’s first CfD pilot. It also draws lessons for other evolving power markets facing similar constraints, such as limited short-term procurement avenues, heavy reliance on long-term contracts, and the need to scale clean, flexible power without open-ended fiscal exposure.

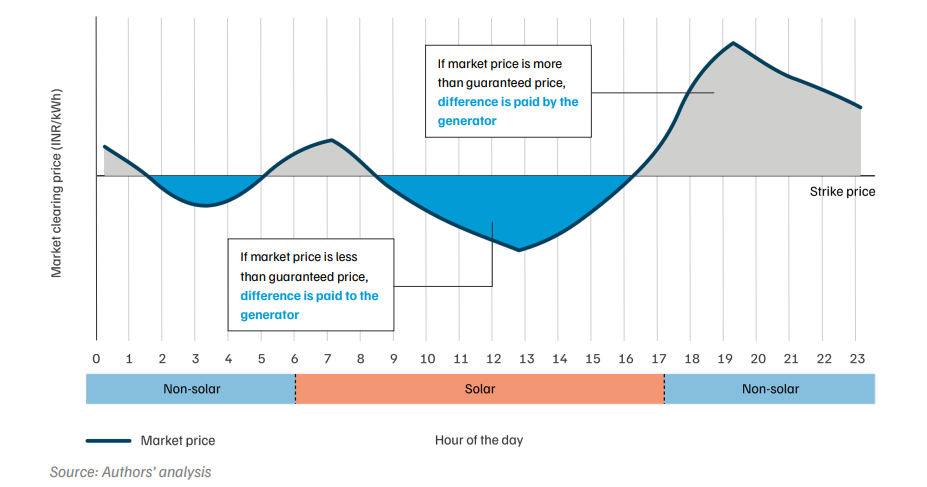

A CfD is a financial instrument designed to manage the risk of revenue uncertainty for generators selling electricity exclusively on market platforms (called merchant plants), where electricity prices fluctuate based on real-time demand and supply.

In advanced power markets, CfDs provide revenue stability by guaranteeing a fixed benchmark, known as the strike price (SP), which is typically determined through competitive bidding and reflects the generator’s cost to supply. The contract then settles the difference between this strike price and the prevailing market or reference price.

In a two-way CfD (Figure 1):

Figure 1. How do two-sided Contracts-for-Difference (CfDs) work?

This structure protects generators from low-price periods while preventing windfall gains during highprice periods. In countries such as the UK and Germany, where CfDs are used as part of renewable energy market design, payments are typically managed through government-owned or designated counterparties and financial settlement mechanisms (Department for Energy Security and Net Zero 2025; Simon Malleret et al. 2024). However, unlike mature European markets, where CfDs are layered on relatively liquid wholesale and forward markets, India is testing the instrument in a market where participation in wholesale markets remains limited and long-term PPAs dominate. This makes the pilot important not only as a renewable energy support mechanism but also as a market-building intervention.

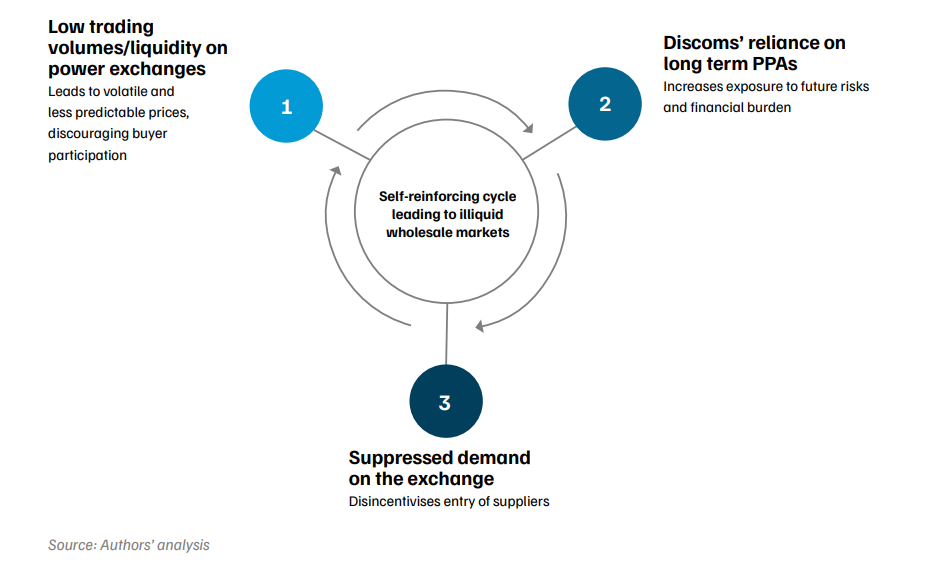

India’s wholesale electricity markets remain thin. Despite nearly 17 years of formal operation, power exchanges— platforms where electricity is bought and sold for shortterm horizons—account for only about seven per cent of total electricity generation, functioning largely as a last resort for buyers (CERC 2025a). The primary cause is the dominance of legacy long-term PPAs, which lock most distribution companies into fixed procurement arrangements. This creates a self-reinforcing cycle: low trading volumes lead to price volatility, which discourages buyers such as distribution utilities from participating. Weak demand, in turn, deters suppliers from entering the market, further constraining market depth (Figure 2).

Figure 2. The self-reinforcing cycle of why India’s power exchanges remain small and underused

However, merchant renewable energy plants face risks operating in illiquid markets. These risks are difficult to quantify and, in many cases, still poorly understood. Without instruments to discover and manage these risks, investment in market-based capacity remains constrained and wholesale market liquidity remains weak. This is the structural gap that India’s pilot CfD is designed to fill: by stabilising revenues sufficiently to attract investment while preserving enough market exposure to drive competitive behaviour.

In this sense, CfDs can help power markets move beyond the traditional choice between long-term contracts and full merchant risk. They can provide enough revenue visibility to make market-linked renewable energy and storage bankable, while still exposing generators to wholesale market prices. For evolving power markets, this creates a practical transition path from contracting capacity for decades to procuring clean power more flexibly, in the shorter term.

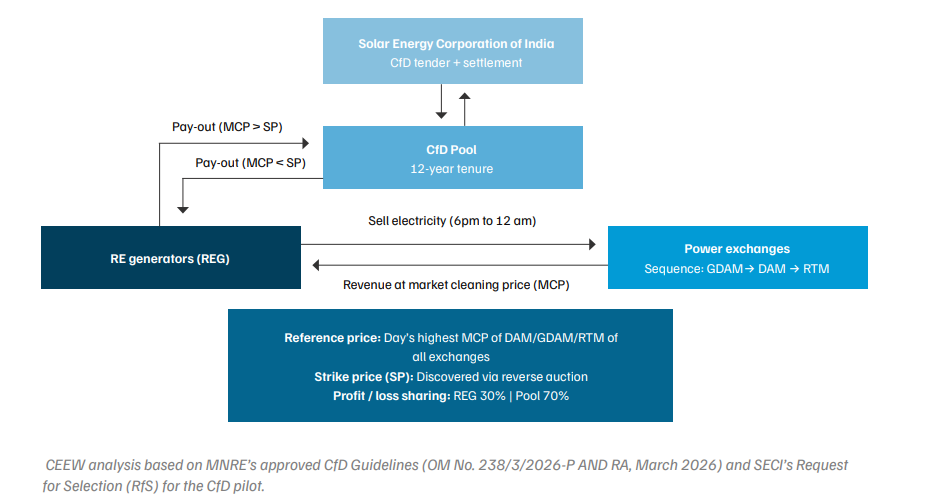

In March 2026, India’s Ministry of New and Renewable Energy (MNRE) approved a pilot CfD scheme for 500 MW of renewable energy capacity, making India one of the first developing economies to formally adopt a CfD instrument for clean power. The Solar Energy Corporation of India (SECI), the nodal implementation agency, has since issued a tender that gives concrete shape to the framework (SECI 2026).

The pilot is built around a two-way, financially settled CfD contract model. SECI, as a counterparty, manages a dedicated stabilisation fund, seeded with INR 76 crore (approximately USD 8 million) , to pay developers when market prices fall below the strike price. The fund gets replenished when market prices exceed the strike price (Figure 3). The design serves three broad objectives: (i) speeding up the deployment and offtake of renewable energy and battery storage; (ii) facilitating clean energy availability during critical evening peak-demand (nonsolar) hours; and (iii) stabilising market prices to attract a wider set of buyers and sellers.

Figure 3. India’s CfD pilot mechanism flow

The Government of India has already signalled the need for such market-linked instruments. The Ministry of Power’s Report of the Group on Development of Electricity Market in India and the Draft National Electricity Policy 2026 both call for instruments that increase efficiency in power procurement (Ministry of Power 2023, Ministry of Power 2026).

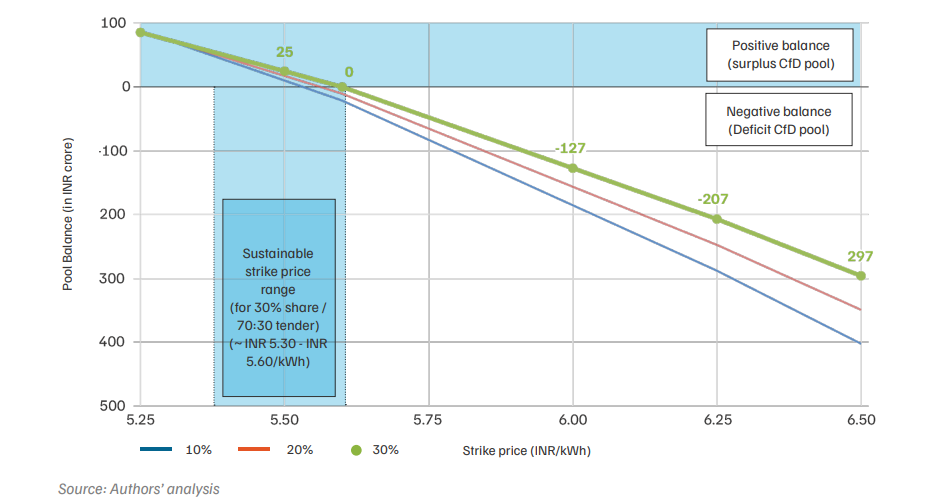

At the same time, the adequacy of the CfD pool is highly sensitive to strike prices. Our analysis shows that the pool reaches break-even at a strike price of approximately INR 5.5–5.6/kWh (or 5.76–5.86 cents/kWh) under the 70:30 profit-loss sharing ratio (Figure 4).

Figure 4. The CfD pool remains financially sustainable at strike prices of approximately INR 5.5– 5.6/kWh

However, its greater value lies in the shift it could trigger among renewable energy developers that are traditionally reliant on long-term PPAs. By requiring them to participate in power exchanges, the pilot can help build market-facing capabilities and confidence in merchant operations, gradually supporting deeper market participation.

The pilot establishes a strong foundation for catalysing innovation. However, five design challenges will determine whether CfDs can fulfil their potential to deepen wholesale markets, de-risk clean energy investment, and support cost-effective peak power procurement. These challenges are not unique to India.

They reflect the broader design frontier for CfDs in developing power markets: how to anchor settlement to credible prices, keep support pools solvent, manage long-term investor risk, and ensure that market-linked renewable supply is matched by sufficient buyer participation.

The CfD settles payments based on prices discovered on the power exchanges. But these platforms handle only about seven per cent of India’s total electricity trade. When the volume of power traded on exchanges is low, prices can swing sharply from day to day. The pilot’s risk-sharing ratio partially mitigates this by giving generators a meaningful stake in maximising market revenues. But as CfD volumes grow, more stable pricing benchmarks, such as dedicated settlement indices, will be needed to reduce the impact of day-to-day price swings on settlement outcomes.

International experience shows that reference-price design for electricity evolves with market maturity.

Source: Author's Analysis

While CfDs settle against day-ahead/real-time prices, strike prices reflect a 10–12 year revenue expectation. This mismatch creates residual risk for both developers and the settlement pool. In mature markets, generators can manage this uncertainty through electricity derivatives, which are contracts that allow them to lock in electricity prices months or years before delivery. As India’s derivatives market develops, its interaction with CfDs will be critical in improving bankability and investor confidence.

International experience shows that CfDs and electricity derivatives perform different but complementary functions.

Source: Author's Analysis

The Indian pilot focuses on de-risking supply-side generators and brings new supply to exchanges. But as CfD-backed capacity grows, concentrated supply in similar time blocks could depress prices in precisely those hours. This is known as cannibalisation, where new supply erodes the market prices on which it depends for revenue. This increases pool payouts and weakens the market signals that CfDs are meant to preserve. The key risk, therefore, is not supply-side participation alone, but whether additional market-linked supply is matched by sufficient buyer-side demand. Without mechanisms that also draw distribution utilities and corporate consumers to procure through exchanges, the supply-demand imbalance will persist.

Global evidence underscores the necessity of buyer-side mandates and intentional demand-building strategies.

Managing supply concentration

Source: Author's Analysis

Scaling market mechanisms beyond the CfD pilot will require broader structural reforms. These include reviewing exchange price ceilings, unlocking new market-based revenue streams through ancillary services and carbon pricing, and introducing capacity markets. It will also require a clearer risk-sharing architecture so that downside protection does not depend only on periodic budgetary support. Without such interventions, the need for budgetary support will continue.

International practice suggests that market-linked support schemes must be embedded within wider market reforms.

Source: Author's Analysis

CfD-backed projects will need to participate across multiple exchange segments and manage forecasting and deviation risks. Larger developers may be able to do this through internal trading desks, but smaller developers could face higher transaction costs. Licensed traders or aggregators can pool projects, optimise bidding across markets, and manage deviations at the portfolio level, improving participation and making strike-price discovery more competitive.

What can India learn from global markets on aggregation?

European wholesale markets rely on balancing responsible parties, aggregators, traders, and portfolio managers to reduce the operational burden on individual generators (European Commission 2024).

Source: Author's Analysis

The Government of India’s pilot tender marks a decisive move from viewing CfDs as a policy idea to deploying them as a market instrument. It reflects a careful balancing act: de-risking investments to attract capital while preserving enough market signals to drive competitive behaviour and build exchange liquidity. The value of the pilot lies in the market intelligence it generates: on investor appetite, on price formation dynamics, and on the structural reforms needed to design sophisticated market instruments.

India should use the contracts-for-difference pilot as the first step towards a broader market framework, rather than as a stand-alone procurement exercise. Four immediate actions are critical to the success of CfDs.

These steps would align India’s CfD pathway with global experience, in which revenue-support instruments are usually embedded within broader market reforms, including credible benchmarks, demand-side participation, hedging tools, flexibility markets, and transparent settlement governance. If sequenced well, India’s CfD pilot can become more than a domestic procurement experiment: it can offer a learning architecture for other developing power markets seeking to procure clean, flexible power while deepening wholesale markets and limiting fiscal exposure.

A Contract-for-Difference, or CfD, is a financial contract that helps manage revenue uncertainty for generators selling electricity in the market. It guarantees a generator an agreed strike price. If the market price falls below the strike price, the generator receives a payment to cover part of the shortfall. If the market price rises above the strike price, the generator pays back part of the excess revenue.

India’s renewable energy procurement has largely relied on long-term power purchase agreements. While these contracts helped scale solar and wind, they are less suited to a power system where demand varies sharply by time of day and clean power is needed during specific high-demand hours. CfDs can help make merchant renewable energy and storage projects bankable while keeping them exposed to market signals.

India’s first CfD pilot is a 500 MW renewable energy and storage tender. Developers must sell electricity on power exchanges between 6 pm and midnight. The strike price is discovered through a reverse auction, while the reference price is based on market prices across exchange segments. SECI manages a dedicated CfD pool that pays developers when market prices fall below the strike price and is replenished when market prices exceed it.

CfDs can help utilities procure clean power during peak-demand hours without locking into long-term inflexible contracts. If designed well, they can reduce reliance on expensive short-term power, support renewable energy integration, and create more transparent market-based procurement options. Two-way CfDs can also prevent windfall gains during high-price periods by returning part of the upside to the settlement pool.

CfDs will succeed only if India builds the supporting market architecture around them. This includes credible reference-price indices, stronger buyer participation from C&I consumers and utilities, time-of-day pricing signals, deeper forward markets, flexible contracts, self-sustaining settlement mechanisms, and aggregators or traders that can support developer participation in wholesale markets.

Many developing power markets still rely heavily on long-term bilateral contracts, have shallow wholesale markets, and face growing demand for clean and flexible power. India’s CfD pilot offers an early example of how emerging economies can de-risk renewable energy and storage investments while building market depth and limiting open-ended fiscal exposure.

How can India Create a Demand Flexibility Market?

Enabling Corporate India's Clean Energy Transition

Scaling Solar Power for Irrigation in India:

Solarising Agricultural Power Demand by 2030