Council on Energy, Environment and Water Integrated | International | Independent

Suggested Citation: Aggarwal, Prateek, Vishal Tripathi, and Harsha V. Rao. 2026. Enabling Corporate India's Clean Energy Transition: Reforming Open Access Framework and Tariff Design for the Next Decade. New Delhi. Council on Energy, Environment and Water.

A manufacturing-led economic transformation, anchored by emerging sectors such as AI-enabled digital infrastructure and green hydrogen, is one of the pillars of India's Viksit Bharat 2047 ambition. Manufacturing’s share of GDP is targeted to rise from around 17 per cent today to 25 per cent by 2047. Achieving this goal will depend on the ability of Indian businesses to remain competitive in both domestic and global markets. Yet, in an increasingly volatile geopolitical environment, businesses are becoming more vulnerable to energy supply disruptions and price volatility, with significant implications for their competitiveness.

The need to enhance competitiveness has driven Commercial and Industrial (C&I) consumers to widen their renewable energy (RE) procurement choices beyond distribution companies (discoms). Discoms and non-discom RE routes accounted for ~23 per cent of C&I electricity consumption in 2025. Three structural shifts are now redefining corporate RE procurement. First, the sharp decline in storage costs is enabling reliable, dispatchable renewable power to emerge as a cost-competitive and domestically available solution. Second, evolving global standards are placing increasing pressure on companies to decarbonise their operations and supply chains. Third, ongoing regulatory and retail tariff reforms are pushing towards mechanisms that ensure C&I consumers fairly compensate discoms for the services they provide. Together, these trends are transforming both the economics and architecture of corporate clean energy procurement, while the existing open access framework has yet to evolve in step with these changes.

Against this backdrop, this report analyses the interaction between the ongoing tariff rationalisation efforts and the open access charges framework and how the two remain disconnected. We studied six open access (OA) charges that govern this market: cross-subsidy surcharge (CSS), additional surcharge (AS), standby charge, banking charge, parallel operation charge (POC), and wheeling charge. We examine how each charge is designed, where and why it fails, and what specific reforms are needed to create a level playing field across the discom and non-discom routes.

A manufacturing-led economic transformation, supported by the rise of sunrise sectors such as AI-driven digital infrastructure and green hydrogen, is one of the pillars of India's Viksit Bharat 2047 ambitions. Manufacturing's share of GDP should rise from around 17 per cent today to 25 per cent by 2047 (Jha 2025), a shift also central to capitalising on the China+1 opportunity as global supply chains diversify away from concentrated manufacturing bases (Debroy and Sinha 2024). Realising this ambition rests on Indian businesses being competitive across domestic and international markets. But in a geopolitically uncertain world, corporates are increasingly exposed to energy supply and price shocks that put their competitiveness at risk. Industrial investment decisions, with 20–25 year horizons, require long-term electricity price certainty and revenue visibility. Clean, firm, and competitively priced power is now a precondition for attracting this investment, not a sustainability overlay on top of it.

This is already changing how large electricity consumers think about clean energy procurement. The need to enhance competitiveness has driven commercial and industrial (C&I) consumers to widen their renewable energy (RE) procurement choices beyond distribution companies (discoms). Non-discom RE routes, including third-party open access (OA) and captive arrangements, accounted for around 10 per cent of C&I electricity consumption in 2025. When combined with grid-embedded RE supplied through discoms, renewables meet approximately 23 per cent of C&I electricity demand.1 Three megatrends are now shaping how corporates source power. First, the rapidly falling cost of storage is making on-demand, dispatchable RE, a competitive and indigenously available option. Second, global frameworks are increasingly enforcing stringent standards on the carbon footprint of corporate operations and supply chains. Third, regulatory and retail tariff reforms require migrating C&I consumers to fairly compensate discoms for the services they provide. Together, these forces are reshaping not only what corporations procure, but also how they procure.

Recent actions by the central government including the four-year sunset provision for the additional surcharge under the Electricity Amendment Rules 2024 (MoP 2024a), the draft Electricity (Amendment) Bill 2025's proposal to phase out cross-subsidy for manufacturing, Indian Railways, and metro rail within five years (MoP 2025a), and the simplification of groupcaptive proportionality requirements under the Electricity Amendment Rules 2026 (MoP 2026), have begun to address parts of the problem. At the state level, Karnataka has set a trajectory to raise fixed-cost recovery from 19 to 38 per cent by FY2028 (KERC 2025). These are material developments, however, they do not completely address the underlying problem of discoms' cost underrecovery and a conducive framework for OA. Our analysis examines some of these developments, and recommendations set out in this report are meant to complement these ongoing efforts.

India's OA framework for corporate RE procurement is caught between two countervailing pressures. On one hand, tariff reforms across states are correcting long-standing distortions in electricity pricing. In many states, C&I consumers have historically cross-subsidised other consumer categories through higher tariffs. OA-based RE procurement allowed these consumers to procure RE at significantly lower rate than than grid power. As states rationalise tariffs and revise OA charges, the cost arbitrage is narrowing. On the other hand, decarbonisation pressures on Indian corporates are intensifying rapidly. Regulatory mandates, global carbon border adjustment mechanisms, investor-driven environmental, social, and governance (ESG) requirements, and supply-chain pressures from multinational buyers are turning RE procurement into a compliance necessity rather than a cost-driven choice.

Positioned at the intersection of these two shifts, the current OA charges framework is no longer adequate for the decade ahead. It undercompensates discoms for some of their legitimate costs and exposes C&I consumers to unpredictable, litigation-prone OA charge levies. Yet in CY2025 alone, solar OA additions reached 7.8 GW. Overall, C&I consumers contracted over 36 GW of RE capacity, with 45 GW more under development, and a further 100+ GW of procurement expected over 2030–35 that will need to include firming and storage technologies suited to a high-RE grid (Kothamasu 2025; Mercom India 2025). Table ES1 provides a diagnostic summary of how the six OA charges undermine discom cost recovery and distort the price signals for C&I consumers.

Table ES1. How OA charges undermine discom recovery and distort consumer signals

| Charge | How discoms under-recover | How it distorts consumer signals | Root failure |

|---|---|---|---|

| Cross-subsidy surcharge (CSS) | On the one hand, captive and group-captive consumers are exempt from CSS, leading to a loss of cross-subsidy revenue. On the other hand, in several states, CSS levels exceed the actual cross-subsidies paid by C&I consumers. | CSS is not calibrated to the actual cross-subsidy embedded in tariffs. Even as tariff reforms reduce cross-subsidies, consumers continue to pay elevated CSS due to the disconnect between the Average Cost of Supply and the Voltage-wise Cost of Supply (ACoS–VCoS) and CSS methodology. | Tariff design |

| Additional surcharge (AS) | Fixed costs are largely recovered through energy charges. When consumers migrate, discoms lose the embedded fixed-cost recovery that AS cannot fully offset. In Karnataka, a 5 MW OA consumer contributes to a 6–14% fixed-cost under-recovery despite the AS levy. | AS is not consistently linked to demonstrable stranded capacity. In practice, it is applied under broad assumptions, leading to contested, non-causal pricing. | Tariff design |

| Standby charges | Most states recover only a fraction of the fixed cost of maintaining backup capacity, as charges are based on energy drawal rather than capacity reservation. Punjab’s two-part structure recovers only 21% of the estimated fixed-capacity costs. | The absence of a two-part tariff means consumers do not bear the true cost of maintaining standby capacity. Backup is effectively under-priced and socialised across the system. | Design and data gap |

| Banking charges | Discoms incur back-down costs and peak procurement premiums that are not fully recovered under capped banking charges. | The regulatory cap on banking charges prevents cost-reflective pricing. States respond by restricting banking volumes instead of pricing the service appropriately, undermining procurement certainty. | Design and data gap |

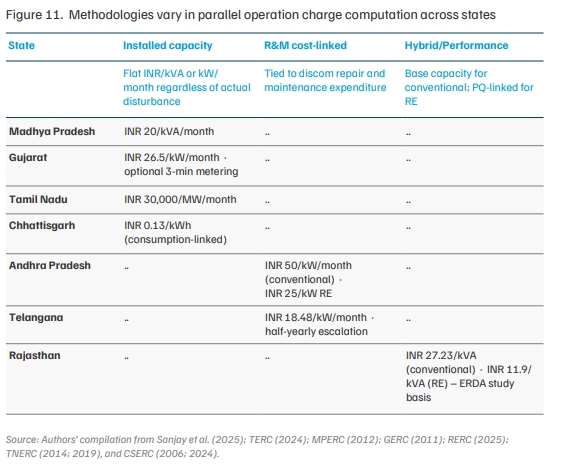

| Parallel operation charges (POC) |

Charges are based on limited studies and lack empirical grounding across the large captive fleet. No state publishes a cost justification. | POC is not linked to the actual impact on power quality. Uniform or presumptive charges apply regardless of technology, overstating costs for RE-based captive plants. | Data deficit |

| Wheeling charges | Network costs are allocated using proxies due to incomplete asset and loss data, leading to approximations in cost recovery. | Consumers face averaged, non-granular charges that do not reflect voltage-wise or locational network costs, limiting their ability to make efficient procurement decisions. | Data deficit |

Source: Authors’ analysis

Note: ACoS (Average Cost of Supply) is the discom's total approved expenditure divided by total energy sold, yielding a single system-wide per-unit cost. VCoS (Voltage-wise Cost of Supply) disaggregates this cost by the voltage level at which consumers are connected, reflecting that serving consumers at higher voltages involves fewer distribution assets and lower losses, and therefore costs less than the system average.

In parallel, decarbonisation pressures are becoming more binding. Domestic policies such as renewable consumption obligations and the Carbon Credit Trading Scheme are introducing compliance requirements for industrial consumers. International mechanisms such as the EU’s CBAM will penalise carbon-intensive exports of steel, cement, aluminium, and fertilisers from the late 2020s (Singh et al. 2025). The Securities and Exchange Board of India’s (SEBI) Business Responsibility and Sustainability Reporting framework mandates emissions disclosures and assurance for top-listed companies. Sustainability-linked loans now tie borrowing costs directly to emission reduction targets (Climate Bonds Initiative 2025). Apple’s commitment to a 100 per cent carbon-neutral supply chain has driven over 250 suppliers across 28 countries, including India, to adopt verified renewable procurement (Apple 2023). These developments are not voluntary signals but contractual, regulatory, and commercial obligations with direct financial consequences.

This report analyses six OA charges–cross-subsidy surcharge (CSS), additional surcharge (AS), standby charges, banking charges, parallel operation charges (POCs), and wheeling charges–in terms of purpose, reform drivers, and actionable recommendations. Across all six, a common cluster of problems recurs, which can be distilled into three structural failures.

Only 15–20 per cent of discom revenue comes from fixed charges, despite fixed costs comprising nearly half of discoms’ total expenditure. When consumers migrate to OA, discoms lose the contribution toward fixed costs embedded in energy charges–a loss that the compensatory additional surcharge cannot fully offset. An illustrative analysis of a 5 MW Karnataka consumer shows that, even with AS levies, the discom faces a 6 per cent fixed-cost under-recovery in case of third-party OA, which rises to 14 per cent for captive arrangements (which are exempt from AS). Cross-subsidy surcharges further compound the distortion: in Karnataka, the CSS is set at INR 1.82/kWh, 11–14 times higher than the actual cross-subsidy contribution of high tension (HT) industrial consumers under the proposed FY2027–28 trajectory. The root problem is not the surcharge rate; it is the inefficient tariff design.

Studies on POCs cover fewer than 10 plants, despite there being ~73 GW of captive capacity. In four of six states, wheeling charges rely on ratio-based asset splits because updated fixed-asset registers are unavailable. Several discoms lack metering at intermediate voltage levels, leading regulators to adopt benchmark or historical loss percentages from earlier orders. Banking cost studies are largely absent. In the absence of such data, OA charges that are precise in form but approximate in substance.

Standby frameworks range from Maharashtra’s four-tier commitment structure to no provisions at all in Tamil Nadu and Rajasthan. Rates for POC vary by more than a factor of 10 across states that use the same nominal methodology. Banking rules have been revised retroactively in Maharashtra. For C&I consumers making 15–25 year investment decisions, this level of regulatory unpredictability is a material barrier to procurement at scale.

Corporate RE procurement in India is undergoing a structural shift, from volume-based annual energy accounting to reliability-centric portfolio design measured in 15-minute time blocks. Leading C&I consumers, such as Hindustan Zinc, have contracted 530 MW of firm RE with battery storage, securing assured delivery in every 15-minute time block. Hindalco and ArcelorMittal have each signed round-the-clock (RTC) RE agreements backed by long-duration pumped-hydro storage. UltraTech Cement has deployed co-located solar, wind, and battery storage to enhance on-site operational resilience. These are not pilot projects but reflect a procurement transformation already underway. Table ES2 maps the evolution of the C&I RE procurement model and its direction.

This transformation requires a fundamentally different regulatory foundation: one that supports procurement models that combine RE with storage, flexibility, and market-based balancing, rather than one built around administratively determined charges and limited data transparency.

Table ES2. C&I renewable energy procurement is shifting from cost arbitrage to reliability driven strategic procurement

| Typical coverage | Balancing mechanism | Delivery metric | |

|---|---|---|---|

| Cost arbitrage era: Plain solar–cost-driven procurement | |||

| Driver: Lower tariff vs grid supply | 30–50% of annual demand | Annual banking with generous OA provisions | Annual energy volume (MU) |

| Hybrid scale-up era: Solar–wind hybrid–expanded demand coverage | |||

| Driver: Cost savings combined with greater RE displacement | 50–65% of annual demand | Monthly banking with increasing Time of Day (ToD) alignment | Annual energy with seasonal profiling |

| Reliability and compliance era: Firm RE with storage–assured delivery | |||

| Driver: Compliance requirements (ESG mandates, CBAM, RCOs) and tightening banking restrictions are pushing consumers toward assured delivery. The GHG Protocol Scope 2 revision proposes hourly matching for reporting, making grid-level emission optimisation essential to substantiate corporate sustainability claims. | Near-100%, including peak hours | Battery energy storage systems (BESSs), pumped hydro, and portfolio-based dispatch | Assured supply at 15-minute intervals |

Source: Authors’ compilation based on stakeholder consultations and Hindustan Zinc (2025); Greenko Group (2022); Hindalco (2022); ArcelorMittal (2025); Gentari (2025), and UltraTech Cement (2025).

The report's recommendations are organised around addressing four challenges: first, correct the tariff distortions that make compensatory surcharges redundant; second, build the evidence base required for rationalising charges accurately; third, redesign charges to reflect the costs they are intended to recover; and fourth, strengthen market mechanisms that can, over time, replace administrative charges. Without progress on the first challenge, the remaining three can only partially succeed. Each recommendation is mapped to a specific charge, a responsible institutional actor, a timeframe, and an expected outcome (Table ES3).

Table ES3. Reform requires sequenced action across four themes

| Charge | Stakeholder | Recommendation | Timeframe |

|---|---|---|---|

|

Theme 1: Correct structural tariff distortions

CSS and AS exist partly because tariffs are not cost-reflective, and fixed costs are bundled into energy charges. Reforming tariff structures reduces the need for compensatory surcharges.

|

|||

| CSS | SERCs and state governments | Publish a time-bound trajectory for ABR–ACoS alignment across consumer categories. Implement a trajectory to align consumer tariffs within a ±20 per cent band of ACoS, protecting vulnerable consumers through direct budgetary transfers rather than embedded cross-subsidies. | 1 year |

| CSS | SERCs and state governments | Undertake structural tariff reforms to progressively eliminate cross-subsidies from tariff design. Any support for vulnerable consumers should be through direct budgetary transfers, not tariff cross-subsidies, so that CSS becomes redundant. | 2–4 years |

| AS | SERCs | Implement phased tariff rebalancing by progressively increasing fixed charges and reducing energy charges, beginning with C&I categories. Introduce sunset provisions for AS in states where rebalancing substantially improves fixed-cost recovery. | 2–4 years |

| Banking | MoP and SERCs | The current 8% cap incentivises volume restrictions rather than cost-reflective pricing. Revise the GEOA Rules 2022 to allow for cost-reflective floor and ceiling anchored to independently estimated injection–withdrawal mismatch costs. | 2–4 years |

|

Theme 2: Build the transparency and evidence base

Accurate charges require data that does not yet exist in most states. These actions establish the foundation on which all subsequent reforms depend.

|

|||

| AS | Discoms and SERCs | Publish quarterly, block-wise data on stranded capacity, OA drawal volumes, curtailment events, and scheduling deviations. Data must be publicly available on discom and SERC websites. | 1 year |

| Standby | Discoms | Publish quarterly data on standby capacity contracted, standby power drawn, and associated revenues. | 1 year |

| AS | SERCs | Require discoms to demonstrate a direct link between OA transactions and specific stranded capacity before levying AS. Exclude curtailment arising from demand-forecasting errors or avoidable RE backdown. | 1 year |

| Charge | Stakeholder | Recommendation | Timeframe |

|---|---|---|---|

|

Theme 2: Build the transparency and evidence base

Accurate charges require data that does not yet exist in most states. These actions establish the foundation on which all subsequent reforms depend. |

|||

| Banking | SERCs and discoms | Commission independent studies to quantify the actual system costs of banking, including discom back-down costs and peak procurement premiums. Conduct a structured stakeholder consultation before revising banking provisions. | 1 year |

| POC | SERCs, SLDCs, and discoms | Commission large-sample harmonic studies stratified by fuel type. Publish results and make them available for public comment before use in charge-setting. | 1 year |

| Wheeling | Discoms | Leverage RDSS to prioritise feeder- and distribution-transformer-level metering, enabling voltage-wise loss assessment and network-cost segregation. | 1 year |

|

Theme 3: Align charges with actual costs Most charges are set using outdated proxies or methodologies that no longer reflect the costs they are meant to recover. These actions correct the design

|

|||

| CSS | MoP and SERCs | Review the CSS methodology and notify of a revised methodology after consultation with the states. Align CSS computation with the actual cross-subsidy embedded in consumer tariffs rather than the ACoS– VCoS divergence. | 1 year |

| Standby | SERCs and discoms | Mandate two-part standby tariffs separating capacity reservation from energy components. Require mandatory standby commitment agreements for all consumers above a threshold load, drawing on Maharashtra’s four-tier framework. | 1 year |

| Charge | Stakeholder | Recommendation | Timeframe |

|---|---|---|---|

|

Theme 4: Strengthen market mechanisms and planning Administrative charges are a second-best substitute for market signals. These actions build the systems that can replace them over time.

|

|||

| Standby | SERCs and discoms | Integrate standby commitments into resource adequacy assessments and power-procurement planning. Contracted standby capacity should be treated as a known load to reduce the risk of stranded capacity. | 2–4 years |

| Standby | CERC, SERCs, and market institutions | Enable standby services to be procured through ancillary services and balancing markets, allowing reserve capacity to be sourced competitively rather than through administrative tariffs. | 2–4 years |

| Banking | SERCs and discoms | Develop regulatory frameworks and technical standards for gridconnected BESSs for C&I consumers, covering grid connectivity, scheduling protocols, and metering. | 1 year |

| Banking | SERCs and discoms | Develop a transition pathway from banking-dependent RE procurement to market-based balancing, integrating access to the day-ahead market (DAM) or real-time market (RTM) for C&I consumers and hybrid procurement structures. Publish state-level timelines so C&I consumers can plan contract structures accordingly. | 2–4 years |

Source: Authors’ analysis

India’s commercial and industrial (C&I) sector is at an inflection point in its relationship with renewable energy (RE). What began as a cost-arbitrage play in this sector–procuring solar or wind power because it was cheaper than grid supply–is rapidly becoming a strategic necessity, driven by environmental, social, and governance (ESG) mandates, carbon border levies, investor scrutiny, and supply-chain pressures from global buyers.

Consumers in the C&I sector directly contracted over 36 GW of renewable capacity by December 2025, with solar open access (OA) accounting for the bulk at over 30 GW (Climate Group RE100 2023; Mercom India 2025). Solar OA additions reached 7.8 GW in CY2025 alone, nearly double the 3.9 GW added in CY2023 (Kothamasu 2025; Mercom India 2025). The OA market remains heavily concentrated: Karnataka, Maharashtra, and Rajasthan together account for over 60 per cent of new solar OA installations in CY2025 (Mercom India 2025), while most states see negligible activity. An additional 45 GW of solar OA projects are in various stages of development as of the end of 2025, and the pace is accelerating (Mercom India 2025). India’s C&I segment accounts for nearly half of the country’s total power demand (MoSPI 2025). How this segment procures energy over the next decade will determine whether India’s industrial economy decarbonises at the pace its climate commitments demand.

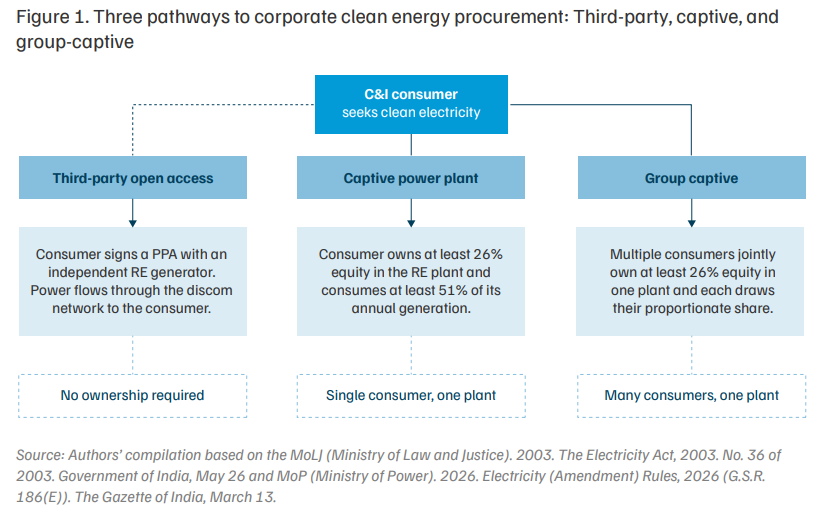

Open access has been the primary instrument enabling this shift (see Figure 1). By allowing C&I consumers to buy power directly from RE generators, OA has created a market-led pathway for decarbonisation. For consumers, it enables ESG compliance, hedges against rising grid tariffs, and supports long-term energy planning. For RE developers, it provides a bankable demand base that attracts private investment and drives competition.

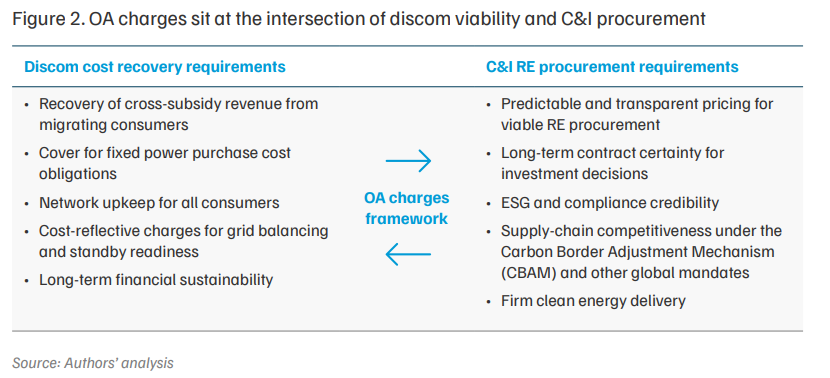

Yet RE meets only ~23 per cent1 of C&I electricity demand today, through a combination of discom supply and direct OA procurement, far short of what the sector must deliver for India to meet its decarbonisation commitments. This gap is not due to a lack of demand or supply; rather, it reflects the limitations of a regulatory framework that has not kept pace with the evolving economics and requirements of corporate clean energy procurement (see Figure 2). Developers and consumers of RE report facing high and unpredictable surcharges, restrictive banking and standby rules, and prolonged administrative delays. These frictions weaken price signals and undermine the competitiveness of clean power (Sethi et al. 2020).

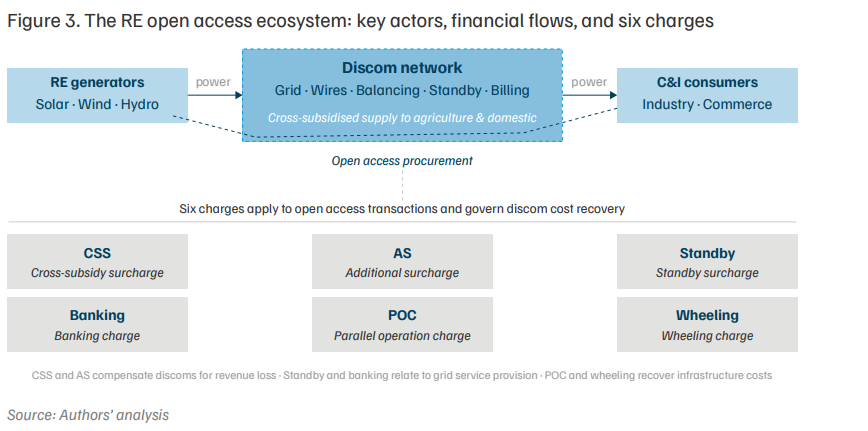

When C&I consumers migrate to OA, discoms face legitimate financial pressures. They lose their highest-paying customers–the same consumers who cross-subsidise agricultural and domestic tariffs. The migration triggers a cascade of under-recovery risks, including fixed-cost liabilities from power purchase agreements (PPAs), stranded network investments, additional costs for grid balancing, and increased administrative burdens (MoP 2017). India’s regulatory architecture addresses these pressures through a set of compensatory charges: CSS, AS, standby charges, banking charges, POC, and wheeling charges (see Figure 3).

In principle, each OA charge has a clear rationale. However, in practice, all six charges are affected by a common set of problems, including methodologies that are not cost-reflective, data systems that are too weak to support rigorous computation, and inconsistent application across states. The result is a framework that simultaneously undercompensates discoms and overcharges consumers. This misalignment is more urgent now than it was five years ago, as the nature of corporate clean energy demand is changing. A combination of ESG disclosure requirements, the EU’s CBAM, granular greenhouse gas (GHG) accounting standards, and supply-chain mandates from global buyers is pushing Indian companies towards a higher share of clean energy procurement. Leading C&I consumers are now contracting firm, round-the-clock (RTC) power with delivery measured in 15-minute time blocks. Procurement at scale will remain constrained if the regulatory framework governing OA remains unpredictable, litigation-prone, and economically distorting for both discoms and consumers.

Several reforms are already underway. The GEOA Rules 2022 standardised banking provisions, streamlined approval process, and lowered the OA eligibility threshold to 100 kW. The Electricity Amendment Rules, 2024, introduced sunset provisions for an additional surcharge. The draft Electricity (Amendment) Bill, 2025, proposes to phase out cross-subsidy for manufacturing, metro rail, and Indian railways, and to exempt discoms from supply obligations for consumers above 1 MW (Ministry of Power 2025a). Radical proposals, such as reclassifying all HTconnected users as OA consumers, signal meaningful shifts (Prayas Energy Group 2025). However, these reforms will take years to design, enact, and implement. The charges that currently govern OA will shape investment decisions, procurement structures, and discom finances long before any of these proposals take full effect.

Chapter 3 examines each OA charge through a consistent analytical lens–its purpose and legal basis, the drivers for reform, and the specific actions required by regulators, discoms, and policymakers to correct the current misalignment. Chapter 4 situates this regulatory analysis within the broader shift in corporate clean energy strategy, demonstrating why reforming OA charges is not merely a technical regulatory matter but a prerequisite for India’s next phase of industrial decarbonisation. The report’s recommendations are directed at specific actors– the Ministry of Power (MoP), state electricity regulatory commissions (SERCs), the Forum of Regulators (FoR), state load dispatch centres (SLDCs), discoms, and C&I consumers–with clear timeframes and expected outcomes.

India has the RE potential, policy architecture, and corporate demand to build a deep and reliable market for industrial clean energy. What it currently lacks is a robust, cost-reflective regulatory framework for OA that is methodologically transparent and consistent across jurisdictions. This report maps the path from where the framework is to where it needs to be.

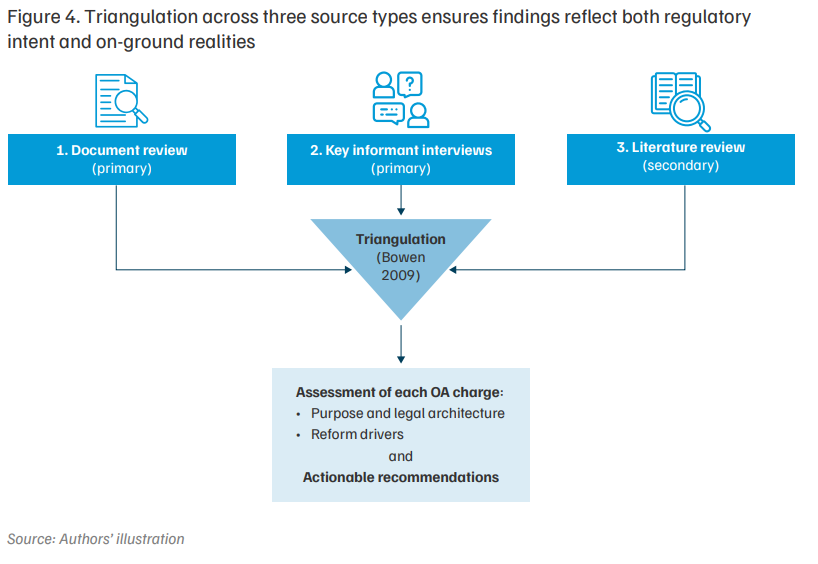

This study employs a qualitative research design (Creswell 2009), drawing on extensive document review and long-form stakeholder interviews to explain how OA charges are conceptualised, calculated, and implemented across Indian states. This approach is appropriate when the research objective is not to test causal hypotheses, but to explain how complex regulatory mechanisms operate in practice, why they vary across jurisdictions, and how institutional actors interpret and respond to them. It is therefore well suited to analysing regulatory environments that are legally complex, institutionally embedded, and unevenly implemented across jurisdictions. The research began with a systematic review of primary regulatory and policy documents, including the following:

• SERC tariff orders, tariff regulations, OA regulations, and petitions

• FoR reports and model regulations

• CEA, CERC, and MoP discussion papers, draft rules, and notifications

• State government policies on RE, captive generation, and electricity duty notifications

• Judicial and quasi-judicial decisions, including APTEL judgements and relevant high court and Supreme Court rulings

These documents provided foundational insight into the statutory intent and computational logic behind each charge, as well as the state-wise methodologies. To supplement this review, we examined secondary literature–including reports by sectoral think tanks, academic papers, and analytical studies–to capture expert interpretations and contextualise how state-level OA charges have been designed, adapted, and applied in practice under varying regulatory, data, and system conditions. While primarily qualitative, this study incorporates descriptive statistics from regulatory sources to contextualise and validate qualitative insights. These quantitative insights strengthen the assessment by grounding our arguments in observed trends and sectorlevel evidence.

Alongside this desk research, the study incorporates insights from conversations with renewable developers, C&I consumers, electricity traders, over-the-counter (OTC) platforms, consultants, and sectoral experts. These interviews serve as key-informant consultations, validating the assumptions underlying tariff orders, surfacing implementation challenges that are invisible in regulatory documents, and capturing expectations around how charges may evolve under future reform scenarios.

This study adopts triangulation across document analysis and long-form interviews, consistent with the approach outlined by Bowen (2009), in which multiple qualitative sources are combined to enhance analytical depth and validity. We do this through:

• Document triangulation: Cross-checking tariff orders against electricity regulatory commission (ERC) regulations, FoR recommendations, and MoP guidance

• Case triangulation: Comparing similar charges across states to identify outliers, gaps, and best practices

• Stakeholder triangulation: Integrating regulatory analysis with stakeholder narratives to enrich, contextualise, and interrogate how charges operate in practice

This iterative process ensures that the final analysis reflects both doctrinal accuracy and onground realities, resulting in a holistic understanding of how these charges shape corporate renewable procurement in India.

Each charge is analysed using a consistent three-part structure: its purpose and legal basis; the regulatory, financial, and structural drivers calling for reform; and specific, timeframebound recommendations directed at named institutional actors. This structure enables direct comparison across the six charges while maintaining a focus on actionable outcomes.

Limitations of the study

• Stakeholder consultations are qualitative and not statistically representative of all market participants. Participant views may reflect organisational positions or limited experiential scope.

• Triangulation partially normalises cross-state comparison; however, inherent regional and regulatory heterogeneity limits the generalisability of findings across all Indian states.

• Limited access to granular administrative data, such as load curves, banking transaction records, and voltage-wise cost components, constrains deeper quantitative validation of several charge methodologies.

• Several regulatory provisions are ambiguously drafted. Where computational steps are not fully specified in tariff orders, interpretive judgement has been applied and noted.

• The analysis reflects the regulatory landscape up to FY2024–25. Subsequent tariff orders, court rulings, or policy changes may alter specific charge methodologies.

• Some recommendations have cross-cutting implications for other charges. These interlinkages are noted where relevant and would benefit from system-wide regulatory review.

Open access has emerged as a key pathway for C&I consumers to transition to RE. The pace of RE uptake, however, depends not only on enabling OA provisions but also on how various OA charges are structured and applied. These charges include the CSS, AS, standby charges, banking charges, wheeling charges, and POCs. Each charge serves a distinct purpose, ranging from compensating discoms for revenue loss to payment against services such as wheeling of power, banking, and standby power.

This chapter examines each of these OA charges through a common analytical lens. First, we analyse their purpose, statutory basis, and prevailing methodologies; then, we identify key regulatory and policy shifts driving reform; and finally, we set out a coherent set of actionable recommendations.

3.1 Cross-subsidy surcharge

Purpose, legal basis, and design

Cross-subsidy has long been a central feature of India’s electricity tariff design framework. Commercial and industrial consumers pay tariffs above the discom’s average cost of supply (ACoS), enabling below-cost tariffs for agricultural and low-income domestic users. An assessment of 60 discoms for 2019 found that C&I consumers overpay by an average of INR 2.46/kWh and INR 1.35/kWh for C&I categories, respectively (Tyagi and Tongia 2023).

The CSS is anchored in Section 42(2) of the Electricity Act, 2003 (MoLJ 2003). It compensates discoms for the loss of cross-subsidy revenue when higher-tariff C&I consumers migrate to OA. It applies only to third-party OA transactions; captive and group-captive consumers are exempt under the Electricity Act. In practice, CSS constitutes the largest single component of OA charges and plays a decisive role in shaping both discom revenues and the economics of RE procurement (Gambhir et al. 2020). The act specifies that CSS should reflect the current level of cross-subsidy within the discom’s area of supply–a requirement that, as the analysis will show, is systematically violated in practice.

Apart from the Electricity Act, 2003, the design and application of CSS are governed by multiple regulatory instruments, including the policy guidance under the National Tariff Policy, 2006 (NTP) and its subsequent amendments in 2008 and 2016 (MoP 2016), as well as subordinate legislations, such as the Electricity Amendment Rules, 2022 and the Electricity (Promoting Renewable Energy Through Green Energy Open Access) Rules, 2022 (MoP 2022b). The NTP 2016 provides the operational guidance that CSS should neither stifle competition nor undermine discom viability. It also specifies that CSS should not exceed 20 per cent of the applicable consumer tariff and requires state electricity regulatory commissions (SERCs) to establish a trajectory for reducing cross-subsidies, gradually bringing tariffs for all consumer categories within ±20 per cent of the ACoS.

Subsequently, the Electricity (Amendment) Rules, 2022, capped CSS at 20 per cent of the ACoS (MoP 2022a), which differs from the provision under the NTP 2016. The GEOA Rules 2022 introduced additional provisions governing the CSS for green energy OA (MoP 2022b). The GEOA Rules specify that the CSS shall not increase by more than 50 per cent of the surcharge fixed in the year OA was granted, for a period of twelve years from the commissioning of the generating plant. Despite these overarching provisions, states continue to apply varying methodologies and interpretations in determining CSS, resulting in a lack of uniformity across jurisdictions.

Further, the recently notified Electricity (Amendment) Rules, 2026 (MoP 2026), simplified proportionality requirements for group-captive projects and clarified verification and appeals, thereby reducing litigation and compliance uncertainty. These changes are likely to improve the viability and scalability of captive-based renewable procurement for C&I consumers.

CSS should reflect the current level of cross-subsidy within the discom’s area of supply, violated in practice.

Drivers for reform

A series of regulatory, financial, and structural changes in India’s power sector are beginning to alter the relevance and effectiveness of the current CSS framework. These developments could prompt policymakers and regulators to reassess both the methodology for CSS and its role in an evolving electricity market.

Tariff rationalisation and solarisation of domestic and agricultural demand is leading to a reduction of cros subsidy requirement.

A. Declining cross-subsidy requirements

Impact of tariff rationalisation measures: One of the most significant developments in recent years is the gradual reduction in cross-subsidy requirements across states. The regulatory framework mandates the progressive alignment of the average billing rate (ABR) with the ACoS within a ±20 per cent band across consumer categories. As of FY2024–25, domestic tariffs in Bihar, Madhya Pradesh, Maharashtra, Tamil Nadu, and Karnataka are already above 90 per cent of ACoS. For agriculture, Bihar and Madhya Pradesh have met the ±20 per cent threshold (ETPI 2024). Karnataka has gone the furthest, establishing a trajectory to nearly eliminate crosssubsidy from tariff design by FY2027–28. These developments suggest that state governments are increasingly bearing a larger share of the subsidy burden through direct budgetary transfers rather than embedding it within tariff structures (Tripathi and Aggarwal 2025).

Impact of solarisation programmes: Central government schemes, such as Pradhan Mantri Kisan Urja Surakshaevam Utthaan Mahabhiyan Yojana (PM-KUSUM) and PM Surya Ghar: Muft Bijli Yojana, along with several state initiatives, aim to meet a substantial share of agricultural and household electricity demand through decentralised solar generation. PM-KUSUM targets the solarisation of 35 GW of agricultural demand by March 2026, while PM Surya Ghar aims to deploy 30 GW of rooftop solar for residential consumers by March 2027. These initiatives are expected to reduce both subsidy requirements and cross-subsidy burdens embedded within tariffs. For instance, Maharashtra estimates that feeder-level solarisation could reduce its annual subsidy outlay by around 45 per cent (from INR 10,000 crore to INR 5,500 crore), lower the cost of supply and reduce cross-subsidy requirements. This could potentially lower C&I tariffs by INR 1.0–1.5/kWh, making solarisation an attractive pathway for tariff rationalisation (MAHAVITARAN 2025; MAHAPREIT 2025).

Misalignment between cross-subsidy levels, CSS methodology, and intent under the Electricity Act, 2003: Cross-subsidy requirements are declining; however, CSS has not followed. Karnataka illustrates this divergence clearly: the cross-subsidy contribution of industrial (HT-2a) and commercial (HT-2b) consumers under the proposed FY2027–28 tariff trajectory is INR 0.17/kWh and INR 0.13/kWh, respectively. In contrast, the CSS approved by the regulator is INR 1.82/kWh, 11–14 times higher than the actual cross-subsidy contribution. Similar patterns are observed in Gujarat, Madhya Pradesh, Uttar Pradesh, and Rajasthan.

This divergence has a structural basis. Regulators compute CSS using voltage-wise cost parameters, while cross-subsidy contributions are assessed against the ACoS. Consumer tariffs are set with reference to ACoS rather than the voltage-wise cost of supply (VCoS). Therefore, CSS is anchored to voltage-level cost parameters, while the cross-subsidy embedded in tariffs is determined using average system costs–and the two routinely diverge (see Box 1). Our consultations indicate that SERCs are complying with the provisions of the NTP, which require CSS to be determined at the relevant voltage level, resulting in structural inconsistency.

Gujarat's VCoS and tariff data for FY2021 make the structural problem concrete. For the HT industrial category, the VCoS is computed at INR 5.67/kWh, notably lower than the ACoS of INR 6.34/kWh—indicating that the actual cost of serving industrial consumers at high voltage is lower than the system average. However, because tariffs are set on an ACoS basis, the industrial tariff (ABR) is INR 7.35/kWh, implying a cross-subsidy contribution of INR 1.01/kWh relative to ACoS. The CSS, computed at 20 per cent of ABR, is INR 1.47/kWh, which is INR 0.46/kWh higher than the actual cross-subsidy contribution.

To demonstrate our hypothesis that the current ACoS–VCoS disconnect causes CSS to systematically overcharge third-party OA consumers relative to the actual cross-subsidy they contribute within the discom's area of supply, we present two scenarios:

| Category/ Unit |

Scenario 1: ACoS-aligned tariffs | Scenario 2: VCoS-aligned tariffs | |||||

|---|---|---|---|---|---|---|---|

| ACoS (INR/kWh) |

ABR @ ACoS (INR/kWh) |

CS @ ABR-ACoS |

CSS – 20% of ABR (INR/kWh) |

VCoS (INR/kWh) |

ABR @ VCoS (INR/kWh) |

CS @ VCoS-ABR |

|

| Low tension | |||||||

| Domestic | 6.34 | 6.34 | 0 | NA | 6.98 | 6.98 | 0 |

| Non-Domestic | 6.34 | 6.34 | 0 | NA | 7.25 | 7.25 | 0 |

| Low Tension Industry | 6.34 | 6.34 | 0 | NA | 6.88 | 6.88 | 0 |

| Public Water Works (PWW) | 6.34 | 6.34 | 0 | NA | 5.07 | 5.07 | 0 |

| Agriculture | 6.34 | 6.34 | 0 | NA | 6.80 | 6.80 | 0 |

| High tension (HT) | |||||||

| Industry | 6.34 | 6.34 | 0 | 1.27 | 5.67 | 5.67 | 0 |

| CSS under scenario 1: VCoS – ABR @ACoS (Industry, INR/kWh) |

-0.67 | Summary | |||||

| CSS under scenario 2: VCoS – ABR @VCoS (Industry, INR/kWh) |

0.00 | ||||||

Scenario 1—ACoS-aligned tariffs: If the ABR of all categories is aligned with the ACoS, the industrial ABR falls to INR 6.34/kWh (from INR 7.35/kWh). Under this scenario, the ACoS-based cross-subsidy contribution reduces to zero. However, CSS under the current formula remains INR 1.27/kWh, as it is computed on ABR rather than actual cross-subsidy. The VCoS-implied cross-subsidy for the HT industry is INR 0.67/kWh (the gap between ACoS and VCoS: 6.34–5.67). Therefore, CSS overcharges by approximately 47 per cent relative to the VCoS estimate of the actual cross-subsidy. A consumer whose tariff reform has eliminated their cross-subsidy contribution is still paying CSS.

Scenario 2—VCoS-aligned tariffs: If tariffs are set equal to VCoS, the industrial billing rate becomes INR 5.67/kWh. Both the cross-subsidy embedded in tariffs and the CSS payable on migration to OA fall to zero. The charge disappears precisely because the underlying distortion, the gap between average and voltage-level costs, has been eliminated. Table 1 shows both scenarios across all consumer categories.

The conclusion is direct: the current CSS formula is not calibrated to the actual cross-subsidy. It is calibrated to ABR, which inflates the charge regardless of what cross-subsidy actually exists. Several discoms have indicated that they lack the granular data required to compute VCoS reliably, which is why ACoS-based tariff determination persists across all states. However, data limitations do not justify a formula that systematically over-recovers. Even within an ACoS-based tariff framework, the CSS methodology requires revision.

Source: Authors' analysis based on GERC (Gujarat Electricity Regulatory Commission). 2022. Tariff Order: Truing up for FY 2020–21 and Determination of Tariff for FY 2022–23 for Paschim Gujarat Vij Company Limited (Case No. 2031 of 2021). Gujarat Electricity Regulatory Commission, and PGVCL (Paschim Gujarat Vij Company Limited). 2021. Category Wise Cost of Service Study for Paschim Gujarat Vij Company Limited (FY 2020–21). Paschim Gujarat Vij Company Limited.

Note: VCoS-based numbers were available only for FY21; therefore, we used them for the analysis. The industry (HT) row is highlighted to underscore the ACoS–VCoS divergence. Summary rows show the gaps between ACoS, VCoS, and ABR for each scenario in the HT industry category.

Further, a review of financial disclosures from several large discoms suggests that CSS collections remain modest compared with the discoms’ overall revenue base. In many cases, annual CSS collections range between INR 200–300 crore, representing less than 0.5 per cent of the annual revenue requirement. Yet the administrative burden of verifying captive status for CSS exemptions is substantial, creating compliance costs for discoms, regulators, consumers, and generators alike.

These observations indicate that the policy objectives under the Electricity Act, 2003, and NTP 2016 have not been implemented in tandem. The NTP calls for progressive reduction of cross-subsidies in tariffs, while the Electricity Act requires CSS to reflect the current level of cross-subsidy. These two mandates should reinforce each other; however, in practice, the CSS formula has not tracked the decline in cross-subsidies, resulting in systematic over-recovery and highlighting the need to review it.

B. Discoms under-recovery due to CSS exemptions for captive consumption

Under the Electricity Act, 2003, CSS applies only to third-party OA transactions, while captive consumption remains exempt. As a result, when C&I consumers migrate to captive arrangements, discoms lose the cross-subsidy revenue embedded in tariffs and do not receive compensation through CSS. In practice, this financial loss should reflect the foregone crosssubsidy contribution rather than CSS receipts. To partially offset this impact, several states levy electricity duties on captive consumption, which can moderate the net revenue loss for discoms (Kokate and Josey 2022).

As tariff reforms progressively align consumer ABRs with ACoS, the cross-subsidy embedded in C&I tariffs will shrink, and with it, the revenue discoms stand to lose when those consumers migrate to captive arrangements. In the long run, as tariffs become fully cost-reflective, the rationale for cross-subsidy disappears entirely, and CSS loses its purpose. Reform is therefore self-reinforcing, and every step towards ACoS alignment reduces the distortion that CSS was designed to address. Policy discussions are already moving in this direction. For instance, the draft Electricity (Amendment) Bill, 2025, proposes to phase out CSS for manufacturing enterprises, Indian Railways, and metro railways within five years. Once cross-subsidy is eliminated from tariff design, the distinction between captive and third-party OA also becomes redundant.

Implementing these reforms will require navigating significant political and institutional constraints. Tariff rationalisation often involves difficult trade-offs for state governments and regulators including balancing cost-reflective pricing with consumer affordability, improving discom finances while preserving C&I competitiveness, and introducing efficient price signals without undermining renewable investment certainty. Policymakers will therefore need to pursue these changes gradually while protecting vulnerable consumers and strengthening coordination between regulatory and fiscal institutions. Recognising these constraints is essential to ensure that reforms remain both practical and implementable.

Recommendations

Declining cross-subsidy requirements, potential over-recovery under the existing CSS methodology, and revenue risks for discoms arising from captive exemptions together warrant a reassessment of how CSS is computed and applied. The recommendations here propose immediate regulatory actions and longer-term structural reforms, organised by timeframe and responsible actor. Some actions may also affect other OA charges and will therefore require coordinated regulatory attention to ensure consistency across the broader tariff framework.

MoP must review the CSS methodology and, after consultation with states, notify a new framework.

| Timeframe | Stakeholder | Recommendation | Expected outcomes |

|---|---|---|---|

| Short (1 year) |

MoP and SERCs | MoP must review the CSS methodology and, after consultation with states, notify a new framework. SERCs must align with the revised CSS formula. | Prevent potential over-compensation to discoms and reduce pricing distortions in OA markets. |

| SERCs | Publish a consultation or white paper that sets out a time-bound trajectory for ABR–ACoS alignment across consumer categories. | Establish a transparent roadmap for tariff rationalisation and signal the gradual reduction of cross-subsidy dependence. | |

| SERCs and state governments | Implement a time-bound trajectory for aligning consumer tariffs within a ±20 per cent band of the ACoS, while safeguarding vulnerable consumers through direct budgetary transfers. | Reduce cross-subsidy levels embedded in tariffs and limit the revenue impact of captive exemptions. | |

| Medium (2–4 years) |

SERCs, state governments, and discoms | Undertake structural tariff reforms to progressively eliminate cross-subsidies from tariff design and eventually phase out CSS. Any support to vulnerable consumers should be through direct budgetary transfers. | Create cost-reflective tariffs, improve transparency in electricity pricing, and reduce reliance on CSS over the long term. |

3.2 Additional surcharge

Purpose, legal basis, and design

The AS is levied under Section 42(4) of the Electricity Act, 2003. When C&I consumers procure electricity through OA, discoms may remain obligated to pay fixed charges under long-term PPAs that were originally contracted to serve those consumers. The AS enables discoms to recover unavoidable fixed costs arising from such stranded power purchase commitments. The AS applies only to third-party OA transactions, while captive and group-captive users are exempt. This distinction has been upheld in several Appellate Tribunal for Electricity (APTEL) and court judgments, including JSW Steel Ltd & Others vs Maharashtra Electricity Regulatory Commission & Others (2019).

The design and application of AS are governed by multiple regulatory instruments, including the NTP 2006 and subsequent amendments, the Electricity (Promoting Renewable Energy Through Green Energy Open Access) Rules, 2022, and the Electricity Amendment Rules, 2024. The NTP 2016 broadly establishes that AS should reflect only the actual stranded fixed costs arising from discoms’ power purchase commitments and should not undermine the viability of OA. It further clarifies that AS is distinct from network-related charges, which are recovered separately through wheeling and transmission tariffs.

Subsequent regulatory provisions have further refined the scope of AS. The GEOA Rules 2022 specify that AS shall not apply to green energy OA consumers if they continue to pay fixed charges to the discom. The Electricity Amendment Rules, 2024, also cap AS at the per-unit fixed cost of the discom’s power purchase. In addition, the rules introduce a sunset mechanism under which the surcharge must be reduced linearly from the level applicable in the year in which OA or general network access is granted and eliminated within four years. Despite these overarching provisions, states continue to apply varying methodologies and interpretations when determining AS, resulting in limited consistency across jurisdictions.

Drivers for reform

Several structural and regulatory factors limit the effectiveness of the current AS framework, including issues related to tariff design, stranded capacity attribution, and the treatment of certain OA transactions. The following subsections examine these challenges in detail.

A. Discom under-recovery due to captive exemptions

Under the Electricity Rules, 2005, captive and group-captive consumers are exempt from AS. Discoms challenged this exemption for several years; however, the Hon’ble Supreme Court recently upheld the legal position in Dakshin Gujarat Vij Company Limited vs Gayatri Shakti Paper & Board Limited and Another (2023). The exemption has significantly reduced AS-related revenues and has financial consequences for discoms. For instance, in Maharashtra, AS revenues declined by more than 80 per cent, from INR 575 crore in FY2017–18 to INR 109 crore in FY2023–24, following courts’ clarification that AS does not apply to group-captive projects (MSEDCL vs JSW Steel and Others 2021).

Renewable energy developers frequently structure projects as captive or group-captive arrangements by transferring the minimum required equity to consumers. This structure allows consumers to access OA power while avoiding both AS and CSS. Even where such transactions leave discoms with genuinely stranded contracted capacity, the current framework provides no compensatory mechanism. Several states levy electricity duties on captive consumption to partially offset this gap; however, these duties are state-specific and do not systematically address the underlying structural shortfall (Kokate and Josey 2022).

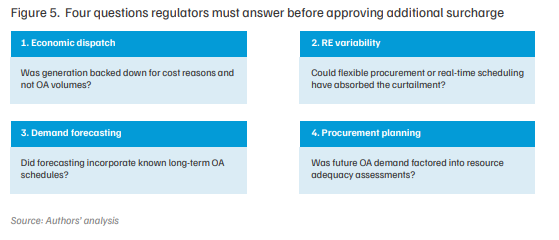

B. Inadequate assessment of curtailment reasons

Additional surcharge is justified only where OA transactions directly cause discoms to strand contracted capacity. In practice, however, regulators and discoms routinely attribute curtailment to OA volumes without adequately examining alternative causes, such as economic dispatch decisions (where discoms back down costlier power when cheaper sources are available), RE variability management, demand forecasting errors, or grid outages. Renewable energy developers and OA consumers have consistently contested this assumption, arguing that several factors unrelated to OA transactions also contribute to power curtailment.

In recent times, courts and tribunals have already scrutinised this assumption. In Lord Chloro Alkali Limited vs Rajasthan Electricity Regulatory Commission & Others (2025), the APTEL overturned Rajasthan’s regulator’s AS levy for FY2015–16, finding that the state had failed to establish a clear link between power curtailment and actual OA volumes. The ruling highlights the need for discoms to demonstrate that OA transactions directly result in stranded capacity before seeking compensation. To ensure that AS reflects genuine OA impacts, regulators should examine the underlying reasons for curtailment before attributing stranded costs to OA consumers. Figure 5 sets out key questions.

Regulators should examine the underlying reasons for curtailment before attributing stranded costs to OA consumers.

C. Discom under‑recover fixed cost due to inefficient tariff design

Regulatory proceedings across several states show that commissions apply varying methodologies to determine AS, a practice that RE developers and OA consumers frequently contest. Regulators and discoms often justify these approaches by arguing that discoms underrecover fixed costs due to the inherent design of electricity tariffs, and that AS is therefore required to compensate for the resulting revenue gap. Therefore, the strongest driver of AS is not OA itself, but the structural mismatch between how discoms incur costs and how tariffs recover them.

Discoms incur two types of costs: fixed costs associated with long-term power purchases, transmission, and distribution networks, and variable costs linked to the energy consumed from generators. Although fixed costs account for nearly half of a discom’s total expenses, fixed charges typically contribute only 15–20 per cent of total revenue (KERC 2025). The remaining 30–35 per cent of fixed costs is recovered through energy charges, creating a structural mismatch between cost recovery and tariff design. State-level data confirms the scale of this issue. In Delhi, regulators bundle more than 60 per cent of fixed costs into energy charges (DERC 2025). In Maharashtra, fixed charges account for only about 19 per cent of revenue, even though fixed costs represent nearly 57 per cent of total costs (MERC 2025). As a result, when consumers shift to OA and reduce their energy drawal from the discom, a significant share of fixed costs remains unrecovered, strengthening the regulatory justification for levying the AS.

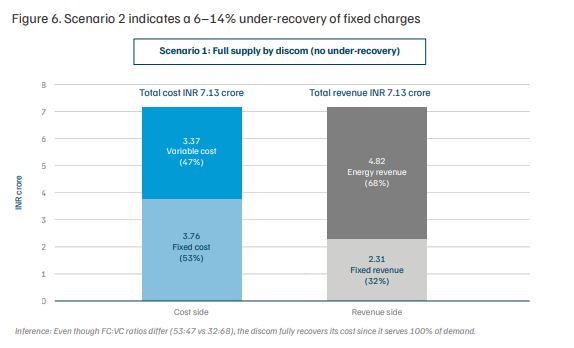

An illustrative analysis of a 5 MW industrial consumer in Karnataka demonstrates how fixedcost recovery operates under discoms and OA-based power procurement. Table 2 summarises the assumptions and calculations used in this illustrative analysis, while Figure 6 presents the findings across scenarios.

In Scenario 1, the discom supplies the consumer’s entire demand. Despite the tariff structure recovering only 32 per cent of fixed costs through fixed charges, full fixed-cost recovery is achieved because the consumer pays energy charges on all units drawn, and energy charges carry the embedded fixed-cost component.

In Scenario 2, the consumer migrates 55 per cent of demand to third-party OA. The discom loses energy charge revenue on these units. The discom applies all applicable charges, including fixed charges on sanctioned load, wheeling charges, transmission charges, and AS. Even after applying these charges, a 6 per cent fixed cost remains unrecovered. For captive transactions, which are exempt from AS, the under-recovery increases to about 14 per cent.

Scenario 3 demonstrates that the entire issue can be addressed through tariff redesign. If fixed charges are increased by 41 per cent (from INR 385/kVA to INR 543/kVA) and energy charges are reduced by 20 per cent (from INR 6.47/kWh to INR 5.18/kWh), fixed costs are fully recovered through the fixed component of the tariff. When a consumer migrates to OA, the discom no longer loses fixed-cost recovery along with energy revenue, because fixed costs are no longer embedded in energy charges. As a result, AS becomes unnecessary, and the distinction between captive and third-party transactions becomes redundant.

This approach also aligns with the GEOA Rules 2022 and several state regulations, which specify that AS should not apply if a consumer pays the full fixed cost through tariffs. The assumption is that fixed charges are set at cost-reflective levels. Several states have begun moving in this direction. Karnataka has set a trajectory to increase fixed-cost recovery from 19 per cent to 38 per cent over FY2024–28. Maharashtra and Rajasthan have initiated similar, though more gradual, adjustments. Table 3 presents Karnataka’s trajectory across consumer categories. The analysis, therefore, shows that prudent tariff design alone can protect discom revenues while providing consumers greater price transparency. Once tariff rationalisation ensures adequate recovery of fixed costs, the rationale for levying AS weakens significantly.

| S no | Parameter | Description |

|---|---|---|

| Key Parameters and Assumptions | ||

| 1. | Consumer profile | HT industrial consumer Contract demand = 5 MW Load factor = 0.17 Power factor = 1 Karnataka discom tariffs used as reference |

| 2. | Annual energy consumption | 7.45 million kWh/year (~7.45 MU annually) |

| 3. | Cost side (discom expenditure) | Fixed cost = INR 5.05/bWh; variable cost = INR 4.52/kWh; ACoS = INR 9.57/kWh → Annual fixed cost (expected) = INR 3.76 crore |

| 4. | Revenue side (tariff design) | Fixed charge = INR 385/kVA; energy charge = INR 6.47/kWh, ABR = INR 9.57/kWh → Assumed cost-reflective tariffs → Annual fixed cost (recovered) = INR 2.31 crore |

| 5. | OA charges and quantum | OA quantum = 55% of annual demand Wheeling charge = INR 0.40/kWh Transmission charge = INR 0.28/kWh Additional Surcharge = INR 0.70/kWh |

| 6. | Cost–revenue ratio misalignment | FC:VC on cost side = 53:47 vs FC:VC on revenue side = 32:68 |

| Findings | ||

| 7. | Fixed cost recovery with consumer getting full supply from discom | Full recovery of fixed cost (INR 3.76 crore) |

| 8. | Fixed cost recovery as consumer procures 55% from third-party OA and 45% from discom | ~94% recovery of fixed cost (INR 3.53 crore) 6% under-recovered fixed cost |

| 9. | Fixed cost recovery as consumer procures 55% from captive OA and 45% from discom | ~86% recovery of fixed cost (INR 3.22 crore) 14% under-recovered fixed cost |

These tariff changes will also alter the economics of OA procurement. As fixed charges rise and energy charges decline, C&I consumers will reassess their contract demand requirements and load-optimisation strategies. Such adjustments could encourage consumers to reduce contracted demand and invest in alternative supply options, such as solar and storage, particularly as technology costs continue to fall. Discoms therefore face a delicate transition: while higher fixed charges improve cost recovery, large and abrupt increases could accelerate migration away from discom supply

| Particulars | Vikram Solar expenditure (USD million /GW) |

Premier Energies expenditure (USD million /GW) |

|---|---|---|

| Land and site development | 0.8 | 0 |

| Building and civil works | 5.3 | 4.1 |

| Plant, machinery, equipment, and utilities | 59.8 | 55.6 |

| Miscellaneous (fixed assets, pre-operative expenses) | 1.8 | 1.9 |

| Design, engineering, and project management | 0 | 0.7 |

| Interest during construction | 2.0 | 6.2 |

| Contingency cost | 1.4 | 1.4 |

| Total | 71.1 | 70.0 |

Recommendations

A rational AS framework must balance the legitimate cost-recovery needs of discoms with the predictability and fairness required by OA consumers. The following recommendations propose a phased pathway to improve transparency, strengthen methodological rigour, and gradually phase out AS where tariff reforms reduce the need for stranded cost recovery.

| Tariff category | Fixed-charge change (FY26–28) (INR/kW or kVA) |

Energy-charge change (FY26–28) (paisa/kWh) |

|---|---|---|

| LT domestic | +INR 25, +INR 5, +INR 10 per kW | −10p, −10p, −5p |

| LT commercial | +INR 5 per kW each year | −100p, −20p, −20p |

| LT industrial | +INR 10 per kW each year | −160p, −10p, −10p |

| LT irrigation <10HP | - | +90p, +26p, +43p |

| HT industrial | +INR 5 per kVA each year | −30p, 0, −10p |

| HT commercial | +INR 55 per kVA each year | −205p, −25p, −30p |

Source: Authors' compilation from KERC (Karnataka Electricity Regulatory Commission). 2025. Combined Tariff Order 2025. Karnataka Electricity Regulatory Commission.

Note: Positive (+) figure indicates cross-subsidy provided by that category, while negative (−) indicates cross-subsidy received.

3.3 Standby charge

Purpose, legal basis, and design

Standby charges apply when OA consumers rely on the discom for backup supply–during generator outages, transmission constraints, or force majeure events. The discom steps in to ensure continuity of service. Standby charges compensate the discom for maintaining the reserve capacity and operational readiness required to provide backup.

Unlike CSS and the AS, standby charges are payments for a service rather than compensation for revenue loss. The discom acts as the supplier of last resort, maintaining the ability to meet sudden demand when the consumer’s primary power source fails.

The Electricity Act, 2003, does not explicitly define standby charges. State electricity regulatory commissions derive their authority to design such charges from their broader tariff-setting powers under the act. Policy guidance is also available through the NTP 2016 and the GEOA Rules 2022. The NTP states that when the generator supplying an OA consumer trips, the discom should provide a temporary supply at a tariff not exceeding 125 per cent of the applicable retail tariff. The GEOA Rules state that standby charges should not apply when the consumer provides at least 24 hours’ advance notice of the standby requirement, and, where levied, such charges should not exceed 10 per cent of the energy charges applicable to the relevant consumer tariff category.

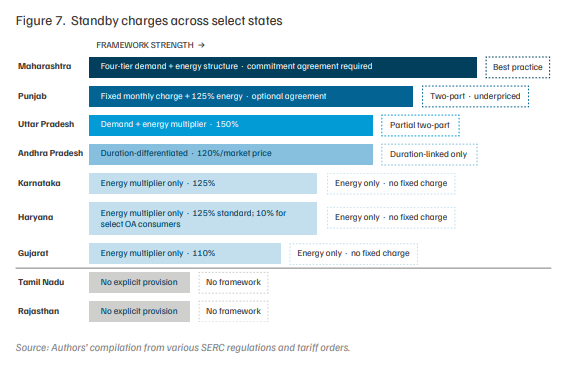

Despite these guiding provisions, states have adopted widely different approaches to standby arrangements. The variation is substantial–it ranges from structured four-tier frameworks to no provisions at all.

Drivers for reform

Standby charges are a critical but underdeveloped component of the regulatory landscape. Most states lack a cost-reflective design, leading to significant under-recovery for discoms and weak economic signals for consumers.

A. Discom stand-by services are not cost-reflective, leading to cost under-recovery

Standby supply involves two distinct cost components. The first is capacity reservation cost–the fixed cost of maintaining generation capacity and system readiness regardless of whether backup power is drawn. The second is variable procurement cost–the cost of actually sourcing electricity when a consumer calls on standby. A cost-reflective standby framework recovers both through a two-part tariff: a fixed charge for capacity reservation and an energy charge for actual drawal. The MoP’s 2017 Consultation Paper on Open Access recommended exactly this structure (MoP 2017).

Although there is limited quantitative evidence on the extent of discom under-recovery from standby charges, insights can be drawn from the current design of standby charges and their linkage with fixed-cost recovery, as discussed in Section 3.2 on AS. In practice, most states lack a structured and cost-reflective framework. As shown in Figure 7, standby charge mechanisms vary widely across states. Some states apply a simple multiplier to energy charges (such as Karnataka, Haryana, and Gujarat), while others combine demand and energy charges (such as Maharashtra and Punjab). A few states, including Tamil Nadu and Rajasthan, lack an explicit framework, leading to ad hoc and non-transparent practices. The variation across states highlights the absence of a consistent regulatory framework for valuing backup capacity and recovering associated system costs.

Punjab provides a clear illustration of the limitations of even relatively advanced frameworks. The state has a formal two-part structure–one of only two states in Figure 7 do so. However, the capacity reservation charge of INR 50–60/kVA per month recovers only about 21 per cent of the estimated monthly fixed cost of INR 280/kVA (PSERC 2025). An energy charge of 125 per cent of the applicable tariff for actual drawal is also applicable. A 5 MW consumer contracting standby without drawing power pays approximately INR 3 lakh per month, leaving an estimated fixed-cost gap of INR 11 lakh per month, which is approximately INR 1.3 crore annually. In the absence of cost-reflective standby charges, discoms socialise these backup costs across all consumers or resort to ad hoc surcharges.

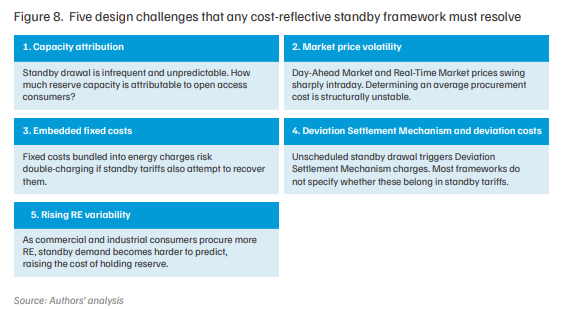

B. Designing cost-reflective standby charges is challenging

Designing fair and cost-reflective standby charges is not straightforward. Discoms and regulators face several structural challenges in pricing standby services appropriately (Figure 8).

Challenge 3 is directly linked to the tariff rebalancing argument presented in the AS section. As states correct the fixed–variable cost bundling problem, standby pricing becomes simultaneously easier to implement, because the risk of embedded fixed-cost double-charging diminishes.

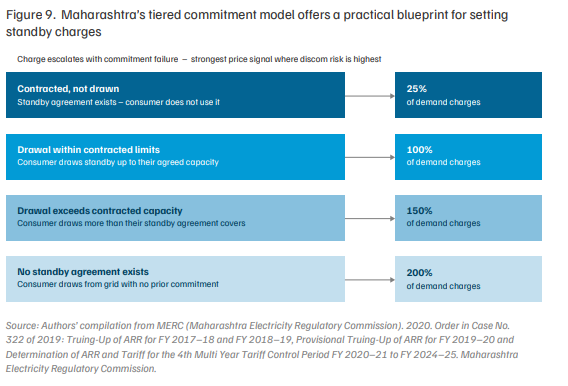

Given these challenges, regulators require a structured and transparent approach to standby provisioning. Maharashtra demonstrates that a workable solution exists despite these challenges. Its four-tier commitment framework resolves Challenge 1 (capacity attribution) through contractual commitments, and Challenges 2 and 4 (market pricing and DSM [deviation settlement mechanism]) by anchoring charges to demand rates rather than spot prices. Figure 9 illustrates this structure.

The framework has three key advantages. First, advance commitments allow discoms to estimate reserve requirements, directly addressing Challenge 1. Second, the escalating penalty structure creates strong price signals against unplanned drawal, reducing the exposure to market price volatility from Challenge 2 (Kokate and Josey 2025). Third, anchoring charges to demand rates rather than energy rates keeps the framework compatible with tariff rebalancing–as fixed charges rise, standby charges increase proportionally without double-counting.

Looking ahead, two structural shifts could transform how standby services are priced. The growth of ancillary services and balancing markets may enable reserve capacity to be procured competitively rather than through administrative tariffs. In parallel, digitalisation and advanced metering may enable real-time standby pricing linked to grid conditions, allowing consumers to manage standby risk through storage or third-party flexibility providers.

Recommendations

A rational standby charge framework must balance two objectives: enabling discoms to recover the cost of maintaining reserve capacity while ensuring predictability and fairness for OA consumers. At present, many state-level mechanisms remain ad hoc or poorly aligned with the underlying cost drivers of standby supply. The following recommendations set out a phased roadmap to improve transparency, strengthen tariff design, and integrate standby provisioning into broader system planning.

| Timeframe | Stakeholder | Recommendation | Expected outcomes |

|---|---|---|---|

| Short (1 year) |

Discoms and SERCs | Publish quarterly block-wise data on stranded capacity, including OA drawal, scheduling deviations, and reasons such as curtailment, outages, or economic dispatch. Data must be publicly available on discom and SERC websites. | Improve transparency and allow stakeholders to independently verify AS calculations. |

| SERCs | Require discoms to demonstrate a clear causal link between OA transactions and generator back-down before approving AS. Exclude RE curtailment, demand forecasting errors, and other operational causes from AS computation. | Ensure AS reflects genuine stranded capacity and reduce regulatory disputes and litigation. | |

| Discoms and SERCs | Integrate OA demand trends into power-procurement planning and resource adequacy assessments. | Reduce the risk of future stranded capacity and improve long-term procurement efficiency. | |

| Medium (2–4 years) |

SERCs | Implement phased tariff rebalancing by progressively increasing fixed charges and reducing energy charges, beginning with C&I categories. Protect low-consumption domestic consumers through targeted support rather than suppressed fixed charges. | Improve recovery of fixed costs through tariffs and reduce reliance on AS. |

| SERCs | Introduce sunset provisions for AS in states where tariff rebalancing substantially improves fixed-cost recovery. Once fixed charges cover their intended cost base, the rationale for AS disappears, and the charge should be phased out. | Phase out AS where it no longer serves a meaningful cost-recovery function. |

3.4 Banking charge

Purpose, legal basis, and design

Renewable energy banking allows generators to inject surplus electricity into the grid and withdraw an equivalent amount later when their own generation declines. The grid temporarily absorbs the surplus and returns energy when required. Like standby charges, banking is a payment for a grid-balancing service rather than compensation for revenue loss. By enabling temporal adjustment between generation and consumption, banking helps consumers manage renewable variability and improves the utilisation of intermittent resources.

India introduced RE banking in 1986 in Tamil Nadu for wind generators as a promotional mechanism to support early RE deployment. States such as Maharashtra and Karnataka allowed annual banking with minimal or no charges, enabling generators to bank most of their surplus RE and withdraw it within the settlement period. These policies were instrumental in scaling renewable capacity when technology costs were high and grid integration frameworks were still being developed.

As RE costs fell from approximately INR 14.5/kWh in 2010 to below INR 3/kWh today, the economics of banking changed (Casey 2024). States now apply banking charges typically in the range of 8–10 per cent of the banked energy, with settlement timelines varying across states, including intraday, monthly, and annual adjustments, depending on regulatory frameworks.

To harmonise banking provisions across states, the central government notified the GEOA Rules 2022. The rules state that banking, where permitted, should be settled at least monthly and capped at 8 per cent of banked energy. The rules also specify that states should allow banking of RE up to 30 per cent of the consumer’s total electricity consumption in a month, subject to regulatory approval.

Drivers for reform

Banking originally functioned as a promotional instrument but has increasingly become a source of operational and financial pressure for discoms, particularly as solar penetration created large midday surpluses that consumers banked and then withdrew during evening peak hours at the discom’s cost. The following factors explain why several states are revisiting their banking frameworks.

A. Banking services are often not cost-reflective

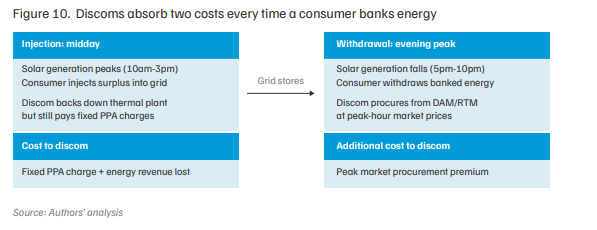

When consumers bank energy, discoms incur two distinct costs. The first is a back-down cost: surplus RE injected during midday forces discoms to curtail contracted thermal generation while continuing to pay fixed-capacity charges. The second is a peak procurement premium: when consumers withdraw banked energy, typically during evening peak hours, discoms must source replacement power from short-term markets at prices substantially higher than what they would have paid from their contracted portfolio. Figure 10 shows why this mismatch is structural rather than incidental.

When consumers bank energy, discoms incur two distinct costs: back down cost and peak procurement premium.

Discoms, therefore, argue that banking effectively forces them to absorb the cost of balancing renewable variability for OA consumers (UPPCL 2024). For instance, an assessment of Karnataka’s banking framework estimated that discoms incurred losses of INR 0.50–0.70/kWh due to banking provisions in FY2020–21, amounting to approximately INR 253–350 crore for around 5,000 MU of OA consumption (Dixit et al. 2022). Such experiences have prompted regulators to reassess whether existing banking charges adequately reflect underlying system costs.

B. States are tightening banking provisions and moving towards a de facto ‘no banking’ regime

Several states have begun modifying banking rules to better align withdrawals with evolving system conditions (Gulia et al. 2021)

In Maharashtra, recent regulatory changes have linked banking withdrawals more closely with time-of-day (ToD) scheduling (MERC 2025). These changes were made to reflect the state’s evolving supply profile, where growing solar capacity is expected to create substantial midday generation surplus. Under the revised framework, the ability to shift large volumes of low-cost daytime solar generation to high-value other periods is significantly constrained. As a result, the effective substitution of discom supply through OA renewable procurement may decline from now 50–65 per cent of a consumer’s demand to around 30–40 per cent, depending on project configuration. Although elements of this framework have faced legal challenges and remain under review, the regulatory direction indicates increasing scrutiny of banking arrangements (Deshpande 2025).

Rajasthan has retained annual banking but introduced several restrictions. The state now limits banking primarily to captive renewable projects and excludes third-party OA transactions. It also caps the banked quantum at 25 per cent of monthly injected energy or 30 per cent of the consumer’s monthly consumption, whichever is higher (RERC 2023).

Gujarat continues to permit banking but levies one of the highest charges in the country, currently around INR 1.50/kWh (Mathew 2026). The regulator has also commissioned a study to assess appropriate banking charges under different renewable penetration scenarios (Kumar 2023). Although the status of this study remains unclear, the approach indicates a shift towards cost-reflective pricing of banking services.

C. Banking may be a transitional instrument as alternative balancing mechanisms mature

Battery storage costs have fallen from approximately INR 13,860/kWh in 2020 to around INR 8,400/kWh in 2025 and are projected to decline further (Chojkiewicz et al. 2025). The day-ahead market and real-time market have expanded significantly, creating new flexibility mechanisms for managing short-term imbalances (Jarbratt et al. 2023; Das and Rodrigues 2025). Green hydrogen and hybrid renewable-plus-storage procurement are emerging as additional alternatives. As storage costs decline and market mechanisms mature, the role of banking is becoming increasingly redundant. The question is therefore shifting from whether banking should continue in its current form to how and at what pace states should transition from banking-dependent procurement to market-based balancing mechanisms.

Recommendations

A reformed banking framework must balance grid reliability, discom cost recovery, and operational flexibility for RE consumers. As renewable penetration increases and alternative balancing mechanisms emerge, regulators will need to gradually transition banking from a promotional policy instrument to a priced grid-balancing service. The following recommendations outline a phased pathway to support this transition while minimising regulatory uncertainty for market participants.

| Timeframe | Stakeholder | Recommendation | Expected outcomes |

|---|---|---|---|