Council on Energy, Environment and Water Integrated | International | Independent

Shaily Jha, Sasmita Patnaik, Abhishek Jain

September 2019 | Energy Transitions, Sustainable Livelihoods

Suggested citation: Jha, Shaily, Sasmita Patnaik, and Abhishek Jain. 2019. Financing Solar-powered Livelihoods in India: Evidence from Micro Enterprises. New Delhi: Council on Energy, Environment and Water.

This report, in collaboration with the SELCO Foundation and supported by the Good Energies Foundation, analyses the financiers’ perspective in lending for solar-powered livelihood appliances in India. It generates evidence on the impact of solar-powered productive-use technologies on the net incomes of end-users and their loan repayments. This helps financiers understand the economic viability of these technologies. It also assesses the prevailing policy solutions and provides recommendations for the private sector, policymakers and donors to improve access to finance for end-users of such products.

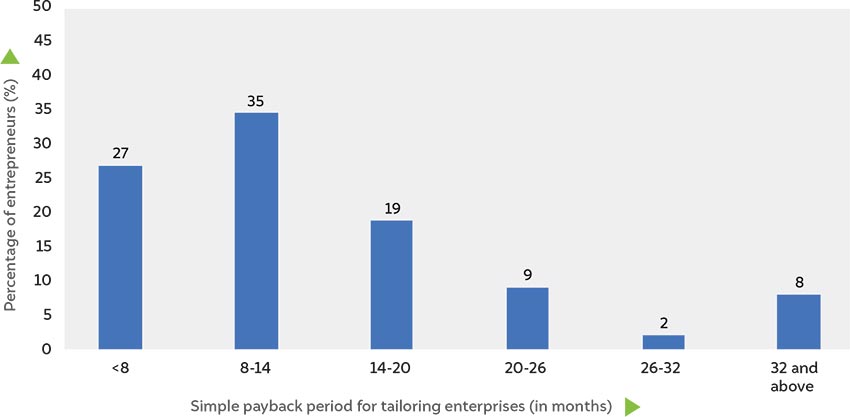

The findings are based on interviews with bankers at the state and national level, civil society organisations and other financiers. To understand the economic viability of solar-powered livelihood appliances, the report also analyses the data on income, revenue, cash flow and loan repayment of 300 micro enterprises for two specific technologies supported by SELCO Foundation – sewing machines and digital service centres called Lok Seva Kendras (LSKs).

Source: Author's analysis

Key Findings

Maximising Rooftop Solar Performance by Enabling a Robust O&M Ecosystem

What Drives Rooftop Solar Installation Decisions in Indian Homes?

Building a People-centric Energy Future:

Roadmap of the methodology to assess the climate co-benefits of the SUP ban in Tamil Nadu