Council on Energy, Environment and Water Integrated | International | Independent

Suggested Citation: Khan, Adeel, Srishti Mishra, Rahul Das, and Priyanka Singh. 2026. Organic Waste Circular Economy for Viksit Bharat: Jobs, Investment, and Emissions Pathways to 2047. New Delhi: Council on Energy, Environment and Water.

India aims to become a Viksit Bharat by 2047, with an economy valued at USD 30 trillion. As urbanisation accelerates, Indian cities are expected to generate approximately 435 million tonnes of municipal solid waste (MSW) by 2050. The organic fraction of MSW (OFMSW), which includes kitchen waste, market waste, and horticulture waste, accounts for about half of all MSW generated in India. Mismanaged organic waste contributes to methane emissions, air pollution, and biodiversity loss. When managed properly, this waste stream has the potential to unlock a wealth of resources, including clean energy (biogas and biomethane) and nutrient-rich compost, creating green jobs and driving economic growth.

This report provides a strategic roadmap for India to achieve circularity in organic waste management in support of the Viksit Bharat vision. It assesses three scenarios – the business-as-usual (BAU) scenario, the accelerated policy scenario (APS), and the ambitious green transition scenario (AGTS) – to quantify investment needs, market opportunities, employment potential, and emissions reductions by 2047.

The study draws insights from multiple expert interviews and stakeholder consultations across policymakers, private sector actors, academic institutions, financial institutions, and civil society. The study maps systemic barriers and enablers across six themes: policy and governance, infrastructure and technology, financial viability and business models, human resources and capacity building, data and information, and awareness and behaviour change.

India aims to become a Viksit Bharat by 2047, with an economy valued at USD 30 trillion (Ministry of External Affairs 2024). Cities in India are currently the engines of this growth, contributing about 60 per cent of the country’s gross domestic product (GDP) (NITI Aayog and Asian Development Bank 2022). India is also expected to undergo one of the largest urbanisations globally, with more than 416 million people projected to move to cities by 2050 (García 2023). As urbanisation accelerates and lifestyles change, Indian cities are expected to generate approximately 435 million tonnes of municipal solid waste (MSW) by 2050 (Khan et al. 2025). In the absence of effective waste management systems, and under the prevailing ‘take– make–waste’ model, this growth in waste generation can exacerbate several local and global challenges, including pollution, urban flooding, biodiversity loss, and climate change.

A transition to a circular economy is therefore both urgent and imperative, and it provides a pathway to effectively utilise resources, reduce pollution, and create green jobs for the future. Given their extensive resource use and concentrated populations, cities play a crucial role in embedding and scaling circular economy principles. Advancing circularity in cities will be pivotal to India’s growth trajectory and to building liveable, clean, and resilient urban centres.

The organic fraction of municipal solid waste (OFMSW), which includes kitchen waste, market waste (vegetables, meat, fruits, and flowers), and horticulture waste, accounts for about half of the total MSW generation in India (MoHUA 2022). Embedded within OFMSW are valuable resources, such as water, nutrients, and clean energy, which can be recovered through processes such as composting and biomethanation (Ddiba et al. 2022). When harnessed effectively, these processes generate nutrient-rich compost that can substitute for chemical fertilisers, while biogas or biomethane can contribute to clean energy and reduce energy imports. Further, the valorisation of OFMSW can reduce methane emissions and prevent contamination of recyclable materials, such as paper, cardboard, and plastics.

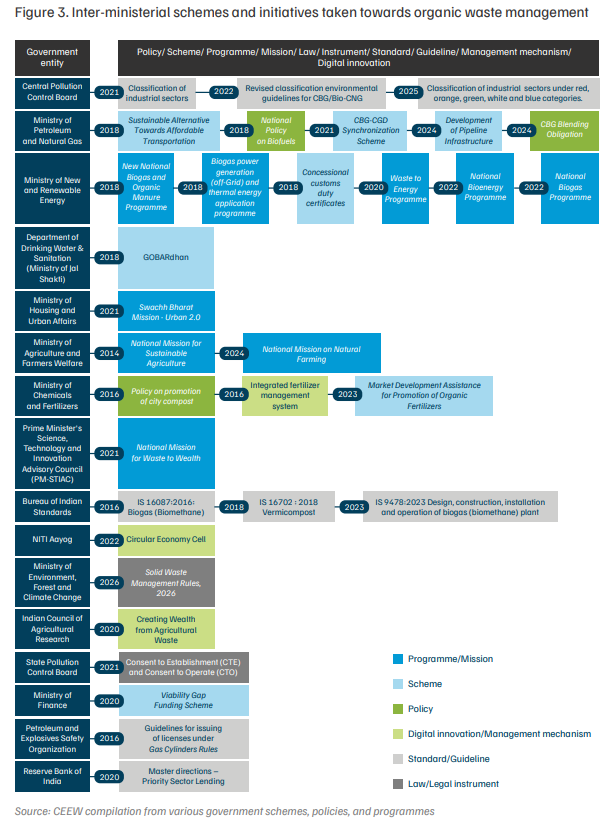

Our review reveals that approximately 16 ministries and government bodies are involved in promoting and implementing multiple organic waste management initiatives, encompassing 9 programmes, 3 policy guidelines, and 7 schemes. Flagship initiatives, such as Swachh Bharat Mission–Urban (SBM-U), the National Bioenergy Programme, and Galvanising Organic Bio-Agro Resources Dhan (GOBARdhan), among others, have begun shifting the focus from waste disposal towards resource recovery. We also found that there has been a concerted push to create a favourable environment for biomethanation.

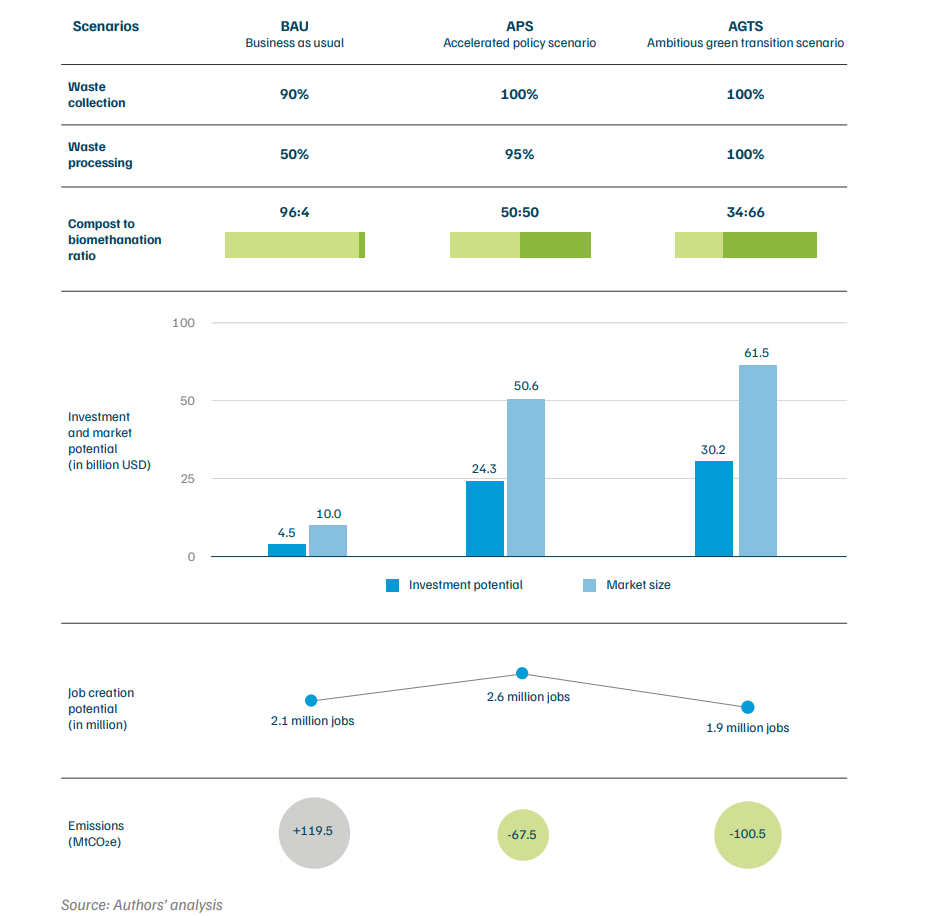

This study addresses a key research gap by assessing how different approaches to organic waste management, including shifts in the treatment mix from composting towards biomethanation, can support India’s Viksit Bharat vision, and what ecosystem levers are needed to enable this scale-up. To address this, we developed a strategic roadmap for organic waste circularity and assessed three scenarios using sigmoid curve modelling: the business-as usual (BAU) scenario, the accelerated policy scenario (APS), and the ambitious green transition scenario (AGTS). These scenarios set targets based on the rate of collection and processing of organic waste with varied allocations of treatment capacities for biomethanation and composting by 2047. For each scenario, we quantified the investment required to establish the facilities, the market opportunity for the end products, the job creation potential, and the emissions reduction potential.

We conducted expert interviews and stakeholder consultations with diverse stakeholders, including policymakers, private-sector actors, academia, financial institutions, and domain experts, to identify current gaps in the ecosystem that must be addressed to unlock this potential. Insights from these consultations can provide strategic foresight to policymakers across ministries, such as the MoHUA, the Ministry of New and Renewable Energy (MNRE), and the Ministry of Petroleum and Natural Gas (MoPNG), as well as for business and city leaders seeking to harness organic waste as a driver of India’s circular economy transition.

Currently, biomethanation and composting are the two most widely adopted organic waste processing techniques in India, accounting for approximately 4 per cent and 96 per cent of treatment capacity, respectively (MoHUA n.d.). Beyond these two dominant techniques, other waste processing options, such as black soldier fly and briquetting, are available, but their uptake remains limited. Figure ES1 presents the economic and environmental potential of integrating circularity into OFMSW management across three scenarios.

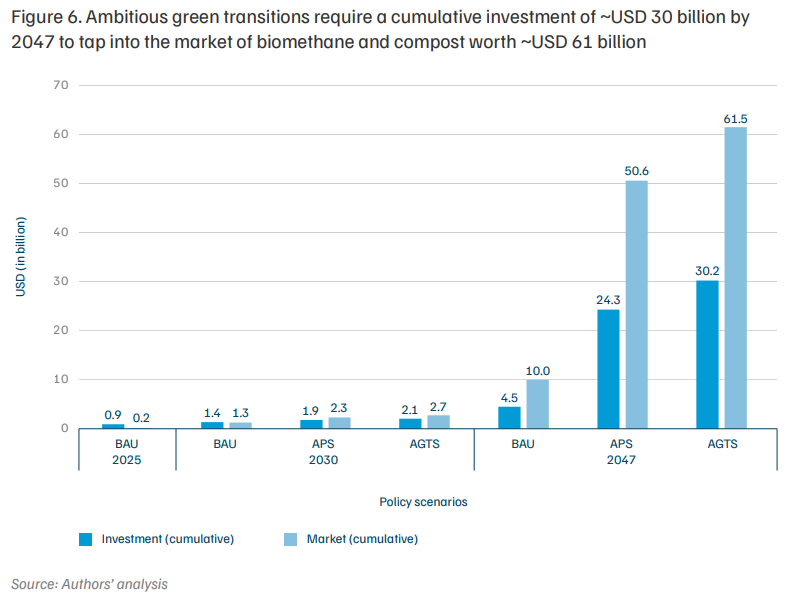

Investment potential: Under a BAU scenario, current investments in waste processing are projected to increase to USD 4.5 billion by 2047, up from the current baseline of USD 0.9, with around half of the waste remaining untreated. In contrast, under the APS and AGTS, investment opportunities would increase significantly, reaching USD 24.3 billion and USD 30.2 billion, respectively, by 2047.

Market potential: The market size for end products reflects this shift. From USD 10.0 billion under the BAU scenario, the market could expand fivefold to USD 50.6 billion under APS and further to USD 61.5 billion under AGTS by 2047.

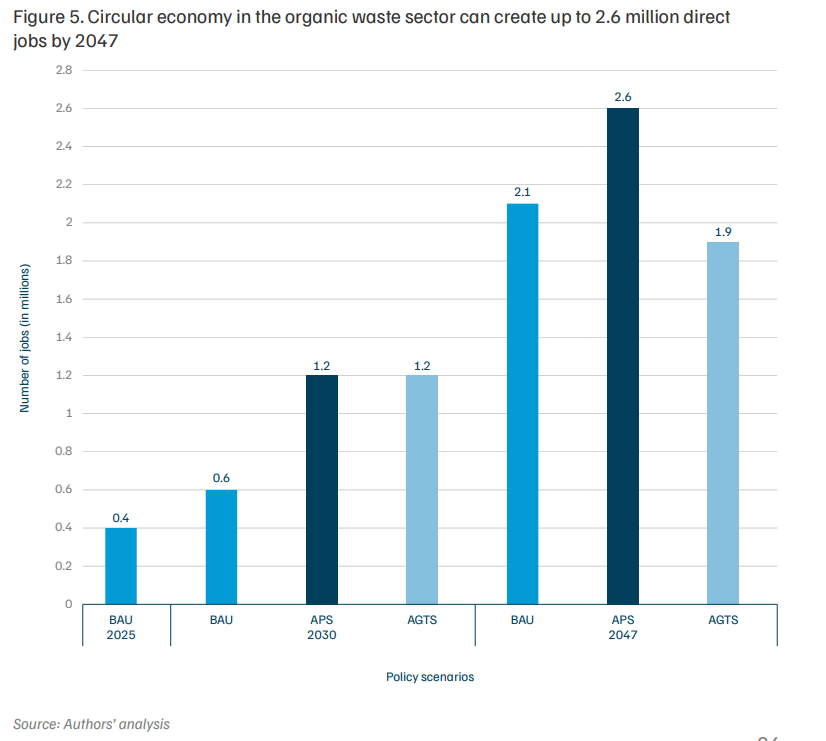

Job growth: India’s strides in organic waste management are expected to shape job creation over the coming decades. Under APS, the sector could potentially create 2.6 million jobs by 2047. Under AGTS, direct job creation is estimated at 1.9 million, slightly lower due to the greater contribution of biomethanation, which is characterised by higher levels of mechanisation than composting.

Emissions reduction: Waste has been one of the fastest-growing contributors to India’s emissions, increasing by 226 per cent between 1994 and 2020 (MoEFCC 2024). Under the BAU scenario, emissions from the sector could reach 119.5 MtCO₂e by 2047. Under the APS and AGTS, emissions from the waste sector are reduced, while the use of end products in sectors such as agriculture, transport, and industry enables additional emissions offsets of 67.5 MtCO₂e and 100.5 MtCO₂e, respectively. Together, these outcomes position OFMSW management as a key lever for driving low-carbon growth and supporting India’s net-zero ambitions.

Figure ES1. USD 60 billion+ market opportunity can be unlocked by scaling organic waste treatment in India by 2047

Note: Under AGTS the number of jobs reduce due to a shift towards biomethanation, which is more automated and capital-intensive than composting. Negative emissions in the APS and AGTS scenarios arise from diverting waste from dumpsites and using end products across agriculture, transport, and industry to displace fossil fuels and chemical fertilisers.

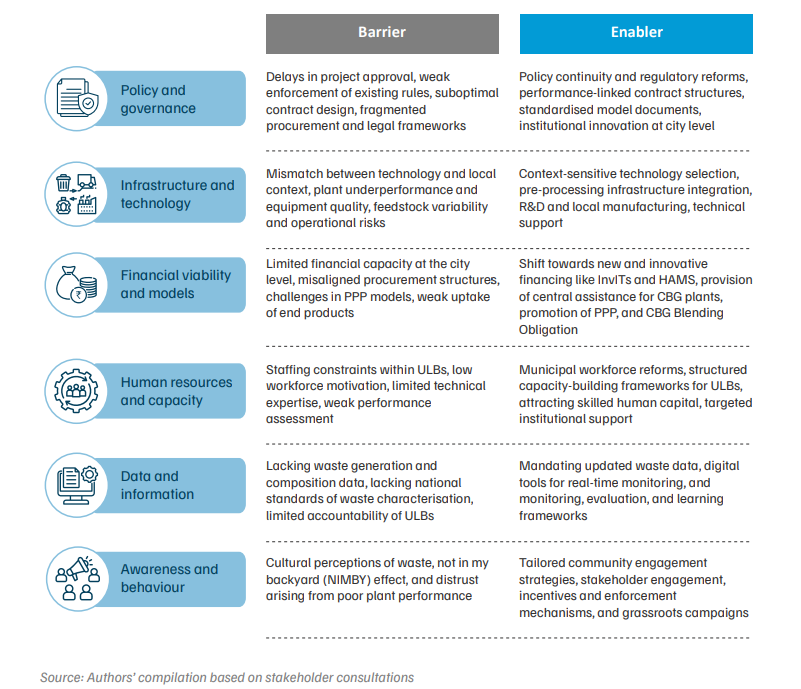

There is significant potential for a circular economy in OFMSW to drive economic growth, create millions of green jobs, provide a low-carbon pathway, and support cleaner cities. However, unlocking these opportunities requires a holistic, multi-stakeholder approach that accounts for the range of challenges and levers. Drawing on our analysis and insights from stakeholder consultations, we identified certain barriers, including delays in project approvals, weak enforcement of waste management rules, variability in feedstock quality and quantity, competition for end products, limited local capacity, lack of data on generation and composition, and low levels of awareness. At the same time, we identified certain enablers, including policy continuity, research promotion, local manufacturing, innovative financing mechanisms, digital public infrastructure, and targeted capacity building and training initiatives. We have mapped these barriers and enablers across six different themes and provided a summary in Figure ES2.

Figure ES2. Barriers and enablers associated with organic waste management across different themes

Note: R&D – Research and Development; CBG – Compressed Biogas; PPP – Public–Private Partnership;

ULB – Urban Local Body; InvITs – Infrastructure Investment Trusts, and HAMs – Hybrid Annuity Models

Translating this potential into reality will require coordinated action from stakeholders across governments, private enterprises, academic institutions, multilateral banks, and civil society to address systemic barriers and translate enabling levers into policies, infrastructure, markets, and mindsets. As India prepares to host the World Economy Forum in 2026, it has a unique opportunity to showcase progress in the sector and strengthen international collaboration to advance the circular economy agenda as a pathway for climate action. To support this transition, we propose the following seven action points:

India has emerged as the fastest-growing major economy and is projected to become the thirdlargest globally, with its GDP expected to reach USD 7.3 trillion by 2030 (PIB, 2025). Over the past three decades, the country’s economy has increased tenfold, and the government has set a target of becoming a Viksit Bharat by 2047, with an economy valued at USD 30 trillion (NITI Aayog 2024). Rising urbanisation and industrial transformation are among the critical drivers of this economic growth. Over the last half-century, India has witnessed a six-fold increase in material consumption, from 1.18 billion tonnes in 1970 to about 7 billion tonnes in 2015 (Sarma et al. 2023), and this figure is projected to reach 14.2 billion tonnes by 2030. However, less than 20 per cent of materials are currently recycled (Sarma et al. 2023). This overexploitation of limited natural resources and the underutilisation of resource recovery place a constraint on India’s long-term growth trajectory.

The prevailing growth paradigm, based on linear economic growth, is likely to aggravate existing concerns around wasteful resource use and the breach of planetary boundaries (CEEW 2022). Waste generation in major Indian cities has almost doubled over the past two decades, and projections indicate that Indian cities will generate 435 million tonnes of waste by 2050 (Khan et al. 2025). The widening gap between waste generation and its proper management threatens to disrupt civic services, leading to open dumping and burning of waste, which exacerbates the twin problems of air pollution and climate change. With more than 877 million people expected to live in cities by 2050, effective waste management is critical to building resilient and healthy cities for the Viksit Bharat vision (MoHUA 2024).

1.1 Embracing a circular economy approach to meet national and international commitments

As Michael Thompson defined in Rubbish Theory, waste is nothing but a misplaced resource (Thompson 2017). A circular economy approach seeks to reintegrate these misplaced resources back into the economy, ensuring that materials and products never become waste. In doing so, the quality and integrity remain intact, which promotes the sustainable use of natural resources while also reducing emissions.

Boosting the economy and creating green jobs

According to the Ministry of Environment, Forest and Climate Change (MoEFCC), advancing circular economy principles could add up to USD 2 trillion to India’s economy and create more than 10 million jobs by 2030 (MoEFCC 2025). A CEEW study focused on the state of Odisha highlights that a green economy could create approximately 10 lakh new full-time equivalent (FTE) jobs and attract investments worth 3.5 lakh crore (~USD 42 billion) by 2030, representing an additional 20 per cent investment for the state (Jain et al. 2025).

Cleaner cities with lower emissions

Open waste burning contributes about 10 per cent of PM2.5 emissions in Indian cities and could become one of the most significant contributors to air pollution in the coming decade (Khan et al. 2025). A World Bank study highlights that addressing the municipal solid waste (MSW) sector is among the most cost-effective interventions for reducing air pollution in the Indo-Gangetic Plain (World Bank 2023). Similarly, the Global Methane Assessment identifies the waste sector in India as offering one of the highest and most cost-effective opportunities for methane mitigation (UNEP 2021).

Pathway for sustainable development

India’s vision of becoming a developed country closely aligns with promoting sustainable development through inclusive economic growth and social welfare. The theme of India’s G20 was ‘Vasudhaiva Kutumbakam’ (‘One Earth, One Family, One Future’), emphasising a unified approach towards addressing global challenges such as climate change. The Delhi Declaration, adopted under India’s G20 presidency, acknowledges the need for a circular economy and reaffirms the country’s commitment to reducing waste and advancing its scientific treatment (MEA 2023). Overall, the circular economy approach can act as a catalyst for achieving India’s net-zero commitments and multiple Sustainable Development Goals (SDGs) (Selvaraj et al. 2024). Lifestyle changes and energy efficiency could result in some of the most significant long-term emissions reductions (Das et al. 2025).

Addressing waste management is one of the most cost-effective pathways to reduce air pollution and methane emissions in India.

Pivotal moment and emerging global leadership in circularity

India has demonstrated its ability not only to set ambitious targets but also to deliver on them. This is evident through its achievement of sourcing 50 per cent of its installed electricity capacity from non–fossil fuel sources five years ahead of the target set under its Nationally Determined Contributions (NDCs) (MNRE 2025; PIB 2025). Further, India has also successfully achieved 20 per cent ethanol blending in petrol by 2025, well ahead of its original 2030 target (MoPNG 2025).

At a time when global circularity has declined from 8.6 per cent in 2020 to 6.9 per cent in 2025 (Sutherland 2025), India is signalling a strong commitment to advancing a circular economy both domestically and globally through its announcement of C-3 and its proposal to host the World Circular Economy Forum in 2026 (MoHUA 2025a). These efforts could position India to become a forerunner and provide a pathway to unlocking the circular economy across sectors. This will be instrumental in achieving the vision of a Viksit Bharat and will also offer lessons and strategies for countries to achieve a sustainable and resilient future.

1.2 Current scenario of solid waste management in India

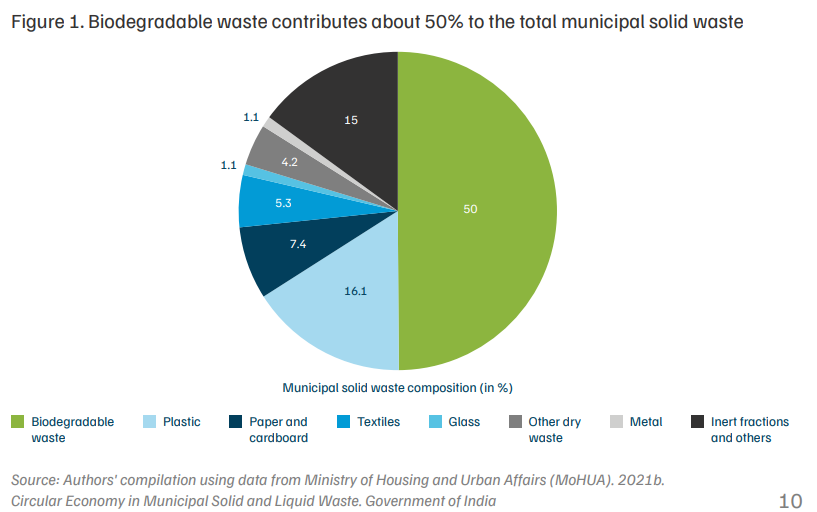

In FY 2022–23, Indian cities generated about 1,70,900 tonnes of municipal solid waste daily, of which about 61 per cent was treated, 24 per cent was landfilled, and the remaining 17 per cent was unaccounted for due to leakages across the supply chain (CPCB 2023). The precise composition of solid waste varies significantly based on factors such as geographical location, season, income levels, and consumption patterns. However, at the national level, about 50 per cent is biodegradable waste, 35 per cent is non-biodegradable, and the remaining 15 per cent comprises inert and other waste, as shown in Figure 1 (MoHUA 2022).

Addressing biodegradable or organic waste is crucial, as effective management of this fraction could immediately halve the overall waste burden on society. Further, diverting and prioritising the organic waste can help improve resource recovery of other recyclable waste, such as paper, metal, and plastic, which are often contaminated when mixed with organic waste. Additionally, the decomposition of organic waste generates odour and releases methane, which has a global warming potential of 84–87 over a 20-year time frame.

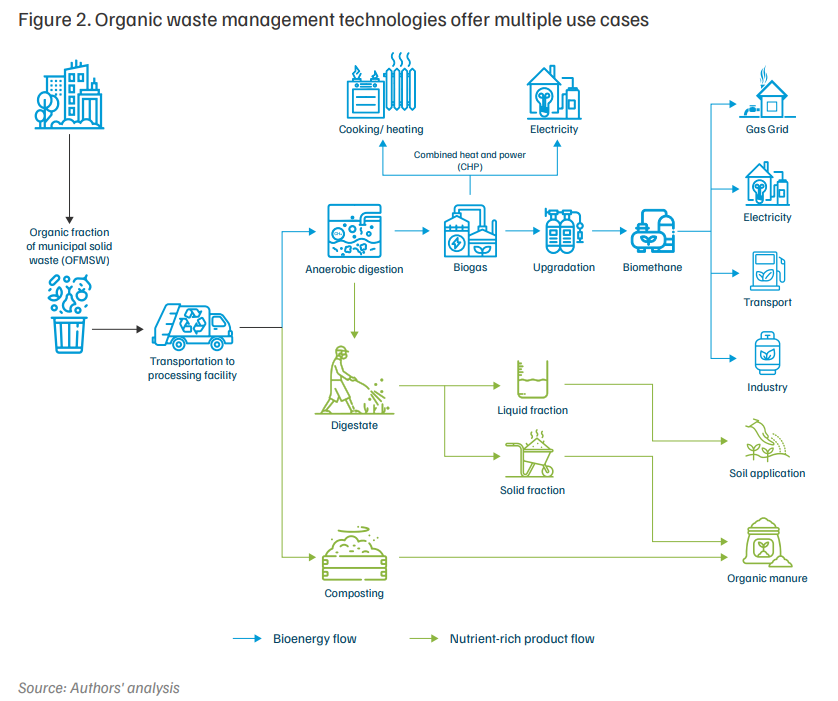

Composting and biomethanation are the primary methods used to treat the organic fraction of municipal solid waste (OFMSW) in India. Composting can be aerobic (e.g. windrow) or anaerobic (e.g. pit composting). Modern composting predominantly favours aerobic methods due to faster processing, reduced odour and methane emissions, reduced space requirements, and a limited need for additional inputs. Biomethanation, in contrast, is an anaerobic process that produces biogas or biomanure. When biogas is further purified through desulphurisation, upgradation, and compression, it is referred to as compressed biogas (CBG) or bio-compressed natural gas (bio-CNG). The final processed gas is comparable to natural gas in terms of composition and properties. Figure 2 summarises the key process steps and final offtake for organic waste management.

Both composting and biomethanation are technologically proven and economically viable methods for managing organic waste. Each presents distinct benefits depending on available resources, market demand, and waste management objectives. In addition, emerging technologies, such as briquetting and pyrolysis, are gaining traction. However, these options currently require more time to become widely and stably available and to be recognised as a preferred mode of organic waste treatment.

1.3 India’s key initiatives and policies for organic waste management

The circular economy has been a cornerstone of India’s policy initiatives, particularly in the context of waste management (Sarma et al. 2023). Spearheading the circular economy principle of ‘cradle to cradle’, India’s organic waste management efforts have significantly evolved its policy landscape to support the management, treatment, and offtake of products derived from organic waste.

These efforts are characterised by cross-sectoral interactions among various ministers and departments involving numerous policies, programmes, schemes, and guidelines (Sarma et al. 2023). Our review indicates that almost 16 distinct ministries and government bodies are involved in the promotion and implementation of a range of initiatives at various roles and capacities, as illustrated in Figure 3.

Collectively, these ministries and departments oversee the implementation of 9 programmes, 3 policy guidelines, and 7 schemes that are currently active in advancing organic waste management in India. This institutional ecosystem underscores the cross-cutting nature of organic waste management and inter-ministerial coordination. A detailed breakdown of these programmes, policies, and schemes, along with key highlights from various ministries and departments, is provided in Annexure 1.

Organic waste treatment strengthens energy security and soil health while improving the recovery of recyclables often contaminated in mixed waste.

India’s net-zero ambition positions biogas as a clean alternative fuel, with the potential to reduce methane emissions from landfills while ensuring energy security (Shrivastava 2022). Existing policies and programmes, such as the National Bioenergy Programme and GOBARdhan, have contributed to creating a favourable environment for biogas as a sustainable technology (MNRE 2025; MoJS 2024).

In addition to regulatory support, India’s policy landscape includes direct economic incentives structured around financial incentives, market development assistance, and favourable financial conditions to improve the bankability and viability of biogas plants. One key economic incentive is the Central Financial Assistance (CFA) being provided by MNRE to support the installation of biogas plants (MNRE 2022). Beyond direct subsidies, economic assistance schemes such as SATAT, GOBARdhan, and Market Development Assistance (MDA) for organic fertilisers do not provide direct grants but instead create an enabling policy environment that fosters favourable market conditions and linkages (IFC 2025; MoJS 2024; MoPNG 2023).

Further, the government has introduced several complementary measures concerning loans and other broader financial mechanisms, such as Priority Sector Lending (PSL), Agri-Infra Fund (AIF), excise duty exemptions for CBG blended in CNG, the Direct Pipeline Infrastructure scheme, and concessional customs duty certificates for machinery imported for CBG plants, to bolster financial viability and incentivise private sector participation (Reserve Bank of India (RBI) 2020; MoJS 2024; MNRE 2021).

For India to achieve its 2047 Viksit Bharat vision of becoming a developed nation, a transformative approach to organic waste management is crucial to maximising resource efficiency, aligning with environmental priorities, generating livelihoods, and ensuring energy access and nutrient security. Developing a solid waste grid that covers urban and rural households, as well as other settlements, is critical to ensuring a comprehensive solid waste collection system (Virmani 2024). Accordingly, targeted initiatives that strengthen other levels of the supply chain, such as generation, collection, and logistics/transportation, will ensure the long-term sustainability of the existing initiatives for the treatment of organic waste and for better-quality end products.

1.4 Global and national overview of the potential and market for organic waste products

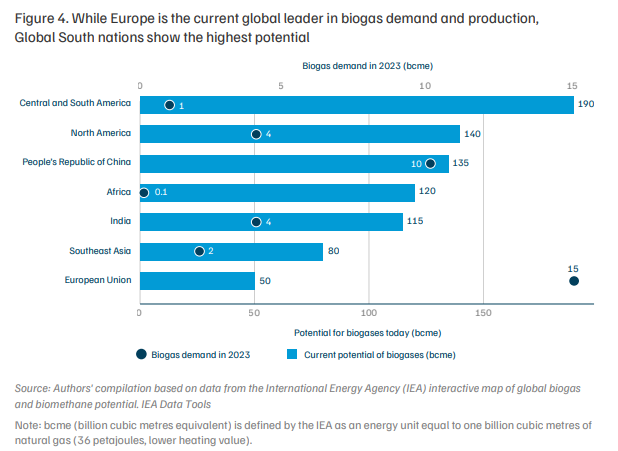

A global study by the International Energy Agency (IEA) indicates that the technical potential for the sustainable production of biogas and biomethane is vast and remains largely untapped. In 2018, actual production represented only a fraction of the estimated overall potential. Full utilisation of this sustainable potential could cover roughly 20 per cent of today’s global gas demand (IEA 2020).

Further, the global potential for biogas production is projected to increase by over 50 per cent by 2040, with costs declining gradually over time, thereby improving competitiveness with natural gas prices (IEA 2020). Data from the IEA indicate that global biogas production will increase fourfold by 2050 (IEA 2024a and IEA 2024b). The primary drivers of this expansion are the established markets in the European Union (EU), the United Kingdom (UK), and the United States (US), which are expected to account for the largest share of new production. Along with these regions, the Asia-Pacific region, including Southeast Asia, represents one of the strongest opportunities for biogas and biomethane production (IEA 2024b).

Europe, especially the EU, has emerged as a global frontrunner in biogas and biomethane due to the convergence of several strategic drivers. The region accounts for around 50 per cent of global biogas production (IEA 2024c). Following Russia's invasion of Ukraine and the subsequent energy crisis, biogas gained traction as an alternative and sustainable energy source capable of reducing dependence on natural gas imports while ensuring energy security (IEA 2024c). To further support this, the EU launched the REPowerEU plan in May 2022, setting a target of producing 35 billion cubic metres (bcm) of biomethane by 2030 (EBA 2022), supported by an investment injection of EUR 37 billion for scaling the initiative (European Commission 2023). Further, in 2024, the EU's Gas Package introduced additional support for grid upgrades.

Of the 50 per cent of biogas production in Europe, Germany alone accounted for nearly 20 per cent in 2024 (IEA 2024c). However, as of 2025, France has overtaken Germany in biomethane production, achieving production levels around 21 per cent higher and operating three times as many plants (EBA 2025). This has been due to recent stagnation in the UK and Germany caused by regulatory uncertainties. Despite recent headwinds, Germany remains among the earliest adopters of supportive biogas production policies, followed by Denmark, Sweden, and Finland (Pelkmans 2024).

Along with major policy shifts, there is also an overall supporting environment. This includes (a) a strong emphasis on promoting an agri-residue management system, (b) the use of digestate to improve crop quality, (c) efforts to reduce import expenses on chemical fertilisers, and (d) the introduction of several directives and guidelines. A range of regulatory instruments has helped create an enabling environment for biogas development in Europe. These include the EU Landfill Waste Directive and the EU Urban Wastewater Treatment Directive, as well as national policy frameworks such as England's Waste and Resources Strategy and the 'Biogas Done Right' guidelines developed in Italy (IEA 2020, 2023b, 2024c). Together, these measures have provided the regulatory backing required to accelerate the transition towards greater energy independence, including in countries such as Germany.

Asia-Pacific: Immense opportunity, but uneven progress

While Europe has emerged as a leader in biogas deployment, there is vast untapped potential, especially in the Asia-Pacific region. At present, aggregate biogas generation in Asia is disproportionately concentrated in China, with China’s market share disproportionately high (Amin et al. 2022). During the early 2000s, Asia experienced robust growth in biogas production; between 2001 and 2009, average growth was close to 25 per cent per year, driven by pro-biogas policies (Amin et al. 2022). However, due to institutional bottlenecks and low policy push, this reduced to just 2.6 per cent between 2010 and 2017 (Amin et al. 2022). Most recently, renewed political interest and increasing pressure to manage waste and reduce emissions have prompted countries to explore biogas more actively as both an alternative fuel and a pathway to managing waste and promoting a circular economy.

India’s push for bioenergy and compost: Aligning with energy independence and net zero

India, with its large agricultural base and increasing MSW, possesses immense and crucial potential for bioenergy. This potential aligns closely with national priorities, including achieving its NDCs by 2030, energy independence by 2047, and a net-zero economy by 2070 (Joshi and Hughes 2023). The IEA forecasts India to be the fastest-growing renewable energy market among large economies through 2030 (IEA 2024c). The CBG potential alone is estimated at 87 billion cubic metres per year, while existing installed capacity represents less than 1 per cent of this potential (IEA India Gas Market Report 2025). This volume, if generated, would meet around 8 per cent of India’s primary energy consumption, based on India's 2024 primary energy consumption of 11,336 terawatt hours (Ritchie et al. 2020).

The other organic waste products that could support India’s circular economy pathway are compost and liquid fermented organic manure (LFOM). According to the Compost Market Report, 2025, the global compost market is expected to reach USD 8.9 billion by the end of 2025, growing at a compound annual growth rate (CAGR) of 8.7 per cent from USD 8.2 billion in 2024 (The Business Research Company 2025).

As highlighted in the preceding sections, a circular economy is pivotal for aligning India’s economic growth with sustainability, particularly within the organic waste sector. India is well positioned to advance this transition, with proven technologies ranging from tradiational composting to advancement in the biogas sector, which is backed by growing policy and regulatory push. At the same time, there is a growing domestic and international markets for key end products such as compost and bio-CNG, creating a strong commercial foundation for scaling circular solutions.

Against this backdrop, in this study, we aim to develop a strategic roadmap for India to achieve circularity in organic waste management that supports the Viksit Bharat vision for 2047. To this end, we assess current and projected trends in organic waste, explore different technological pathways and scenarios under different collection and treatment efficiencies and processing mix. For each parthway, we aim quantify associated financing needs, market opportunities, workforce requirements, and environmental benefits. The study also identifies key levers to unlock the ecosystem and explores policy and regulatory frameworks, technological innovations, financial measures, collaborative partnerships, and business models essential for scaling circularity in this sector.

This research aims to study the potential of the OFMSW to build a roadmap for India’s Viksit Bharat 2047 economy. We employed a mixed-methods approach based on scenario and secondary data analysis to project waste generation, employment potential, investment requirements, and market opportunities. We have also estimated potential emissions reductions from improved OFMSW management based on the relevant emission factors from the literature. In addition, primary insights were gathered through semi-structured expert interviews and stakeholder consultations, supported by semi-structured questionnaires. The following subsections detail the methodology used in the study’s research process.

2.1 Projections for jobs, market, and investment

In the study, we first projected MSW generation through 2047, which formed the basis for subsequent estimates of infrastructure requirements, job potential, and market opportunities. The MSW was calculated as the product of the projected urban population and per capita waste generation (PCWG). Growth rates for waste generation were derived from PCWG data from the Central Pollution Control Board (CPCB) between FY 2015–16 and FY 2021–22 and used to further project the PCWG for the years 2023–47. These calculations served as the basis for estimating the total MSW generation and, subsequently, the organic fraction, which was assumed to constitute 50 per cent of the total MSW. Finally, the projected waste generation value was cross-validated against estimates from other reports and modelling studies for consistency and reliability.

Scenario-based modelling was conducted to estimate the collection and treatment of OFMSW under three scenarios: the business-as-usual (BAU) scenario, the accelerated policy scenario (APS), and the ambitious green transition scenario (AGTS). The three scenarios, presented in Table 1, were devised based on the status quo of solid waste management, current policies, and India’s circular economy objectives for 2047. Hence, assumptions related to collection efficiency, treatment levels, scale (centralised and decentralised), and technology type (biogas and composting) were informed by available data from CPCB, Swachh Survekshan, government websites, and relevant research studies. The percentage targets for waste collection and processing for the APS and AGTS were estimated using CAGR. Meanwhile, estimations for the percentage of waste treated by composting and biomethanation for APS and AGTS are projected using the S-curve (Speelman and Numata 2022). The detailed assumptions and calculations for the waste generation projections, scenario development, and estimates of employment, market size, and investment requirements are provided in Annexure II.

| Scenario | Description | ||

|---|---|---|---|

| Waste collection by 2047 | Waste processing by 2047 | Compost to biomethanation ratio by 2047 | |

| Business-as-usual (BAU) | 90% | 50% | 96:4 |

| Accelerated policy scenario (APS) | 100% | 95% | 50:50 |

| Ambitious green transition scenario (AGTS) | 100% | 100% | 34:66 |

Source: Authors' analysis

For employment opportunities, we considered only the workforce directly engaged in the day-today processing and operational activities of OFMSW management. Market opportunities were assessed based on the potential output of biogas and compost, derived using process yields and recovery rates. The revenue estimates for biogas and composting accounted for the production of CBG and fermented organic manure (FOM), as well as the sale of compost. The corresponding market rates used to calculate total revenues were based on recent government notifications. Investment in infrastructure was limited to land and machinery and was determined by the unit capital costs of the centralised and decentralised plants. The inflation rates were not factored into either market or investment calculations. These projections provide an understanding of the potential of improved OFMSW management to advance India’s circular economy vision.

2.2 Emissions calculation

This study estimated greenhouse gas (GHG) emissions avoided by diverting waste from dumpsites to composting and biomethanation facilities using process-specific emission factors. A lifecycle-based approach was adopted, incorporating process-specific emission factors and yields, rather than applying fixed per-tonne values, to more accurately reflect energy recovery and resource substitution effects. All assumptions and emission factors were derived from secondary data, including peer-reviewed literature, government reports, and sectoral studies.

For composting, emissions were calculated based on process-level methane and nitrous oxide releases, while avoided emissions were derived from the displacement of chemical fertilisers. Net reductions were estimated as the difference between these two values. Similarly, for biomethanation, emissions reduction was quantified through the recovery of biogas for energy use and slurry recovery, which displaces chemical fertiliser. We have provided detailed key assumptions, calculation steps, and relevant emissions factors in Annexure II.

2.3 Questionnaire

A semi-structured questionnaire was developed in English and framed around key thematic areas, such as data, digitisation, waste generation, waste collection, waste treatment, markets, investment and finance, capacity building, technology, R&D, clearances and contracts, policies, plant operations and maintenance, and global partnerships. To ensure relevance, the questions were customised to align with the specific domain expertise of the stakeholders, including academia and research, industry, policymakers, financial institutions, and civil society organisations. Each interview was designed to last 60–90 minutes, allowing sufficient time to gain insights from the stakeholders. The questionnaire is attached in Annexure III.

2.4 Stakeholder consultation

To understand the on-ground implementation barriers and enablers for driving a circular economy in OFMSW, relevant stakeholders were identified and mapped across key domains, such as academia, research organisations, industry players, policymakers, financial institutions, and civil society organisations.

We conducted the stakeholder consultations in two stages. In the first stage, a total of 16 key informants participated in in-depth, semi-structured interviews conducted through both online and offline modes. These informants represented a diverse range of stakeholder groups, as summarised in Annexure IV. All the interviews were anonymised, and prior informed consent was obtained before each interaction. We analysed the qualitative data to identify recurring barriers, enablers, and actionable interventions for OFMSW management.

In the second stage, we convened a multi-stakeholder consultation to validate and inform the interview findings. A total of 35 experts participated in the stakeholder consultation, provided feedback, and helped prioritise feasible solutions. We systematically integrated the feedback into the final research findings to strengthen the reliability and credibility of the recommendations. This two-step process for primary data collection ensured that the findings were both evidence-based and grounded in the insights from practitioners and policymakers across the waste management ecosystem.

2.5 Thematic analysis

To gain insights into the barriers and enablers of circular organic waste management, a thematic analysis was conducted using data gathered from semi-structured expert interviews and multi-stakeholder consultations. All the interview notes were transcribed using Gemini notes. Subsequently, NotebookLM was employed to identify recurring themes and emerging patterns across interview transcripts. The analysis then categorised these findings into the following key themes: policy, governance and institutional frameworks; infrastructure and technology; data and information; financial viability and business models; human resources and capacity building; and awareness, behaviour change, and social acceptance. This approach enabled a systematic understanding of the on-ground challenges, initiatives, processes, and innovations that helped synthesise the findings and recommendations of this study.

2.6 Scope and limitations of the study

This study focuses on OFMSW and does not consider the waste generated in rural areas and other waste streams, including hazardous waste, construction and demolition waste, biomedical waste, and e-waste. While the exact waste composition varies based on multiple factors, such as geography, climate, and other factors, we assumed, based on existing literature and government data, that at the national level, on average, 50 per cent of the waste generated is organic (MoHUA 2022). We also assume that the share of organic waste in MSW remains broadly constant over the study period. The population projections used in the study are based on India’s household-level projections, given the absence of an updated national census, which may affect the accuracy of estimates of waste generation and urban–rural distribution.

Projections for various factors are based on CAGR and secondary market reports focused on the organic waste sector, which differs geographically, rather than specifically on OFMSW. Additionally, all projections in the study are based on current prices and do not account for inflation, changes in operating expenses (OPEX) and maintenance costs, or future technological advancements. The estimates for jobs and investment are based on capital expenditure (CAPEX), while OPEX values are variable and dependent on technology and operational efficiency. The focus of this study is to provide a vision for opportunities in better waste management to inform policy design and set achievable targets, aligning with the Viksit Bharat 2047 vision, rather than to serve as an economic forecast.

In the future, integrated modelling tools, such as Greenhouse Gas and Air Pollution Interactions and Synergies (GAINS) or Global Change Assessment Model (GCAM) and Life Cycle Analysis (LCA), could be used to enhance emissions and economic assessments that can capture the interlinkages of waste with energy, industry, transport, agriculture, and other sectors. Despite these limitations, the study offers insights into the evolving dynamics of India’s waste sector and provides pathways and associated trade-offs for circular economy transformation.

Sustainable development is central to India’s Viksit Bharat vision. This vision prioritises the adoption of green technologies, renewable energy sources, and the promotion of circular economy principles and eco-friendly practices across industries to reduce environmental footprints (Ghosh et al. 2020; Sarma et al. 2023).

India’s OFMSW presents a significant opportunity within this vision. India is projected to generate around 208 million tonnes of OFMSW per annum by 2047 (Jain, and Jhunjhunwala, et al. 2025). If managed efficiently, OFMSW can unlock substantial economic value, particularly in terms of jobs, investment, and market potential.

The sector offers direct employment opportunities across the treatment or processing of OFMSW, spanning technical, managerial, and support functions. A typical 100-tonne-perday (TPD) biomethanation plant requires a workforce of around 31 personnel, including a plant manager, operators, technicians, chemists (laboratory), feedstock management staff, administrative and logistics support personnel, security staff, and unskilled workers (MoHUA 2021a). In comparison, a 100 TPD composting plant employs approximately 28 personnel across various roles and requirements, including plant and assistant managers, supervisors, foremen, plant operators, skilled and unskilled workers, chemists, store and weighbridge operators, drivers, security staff, and support staff (MoHUA 2025a).

Our analysis estimates that under the BAU scenario, direct jobs in the OFMSW sector are projected to grow from 0.4 million in 2025 to 2.1 million by 2047, as shown in Figure 5. Under the APS, total direct jobs could reach approximately 2.6 million by 2047. In contrast, the AGTS shows job attrition by 2047, driven by the greater contribution of biomethanation relative to composting. Scaling OFMSW processing infrastructure would thus create a substantial number of direct jobs, as well as indirect employment in input supply, transport, marketing, retail, etc.

Investment is a key enabler for unlocking the economic potential of the circular economy transition. Under the APS and AGTS, urban areas shift from process improvement (i.e. no gaps in OFMSW generation, collection, and treatment percentages) towards the systematic scaling of processing infrastructure. As a result, investment needs to rise significantly compared to the BAU scenario. The market potential of OFMSW products, i.e., CBG, FOM, and compost, is projected to expand alongside higher investment, as shown in Figure 6.

The study estimates that under the BAU scenario, investment and market size are estimated to grow from USD 0.2 billion and USD 0.9 billion in 2025, respectively, to USD 4.5 billion and USD 10.0 billion by 2047. Under the APS scenario, scaling waste-processing infrastructure would require a cumulative capital investment of approximately USD 24.3 billion. This expansion is expected to unlock a market opportunity of around USD 50.6 billion by 2047.) Further, AGTS could mobilise a cumulative capital investment of USD 30.2 billion to scale waste-processing infrastructure, especially biomethanation plants, which can generate a market opportunity of USD 61.5 billion by 2047.

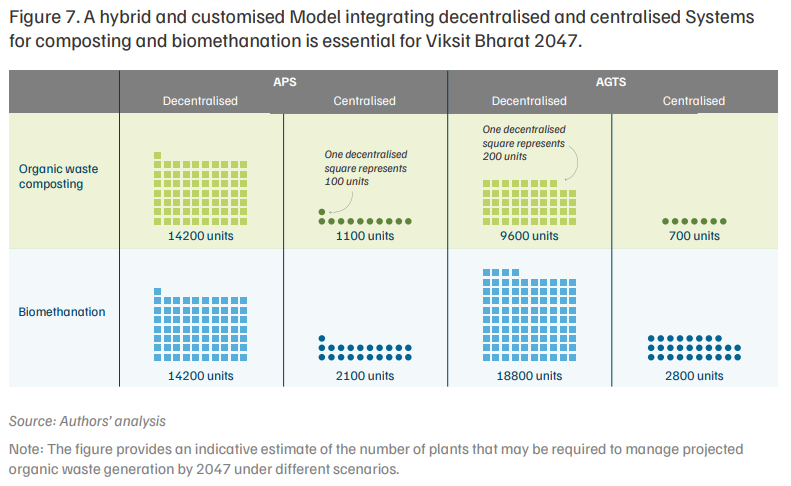

A circular waste economy must diversify, relying on a combination of solutions/technologies like composting and biomethanation across both decentralised and centralised scales, as explained in Figure 7.

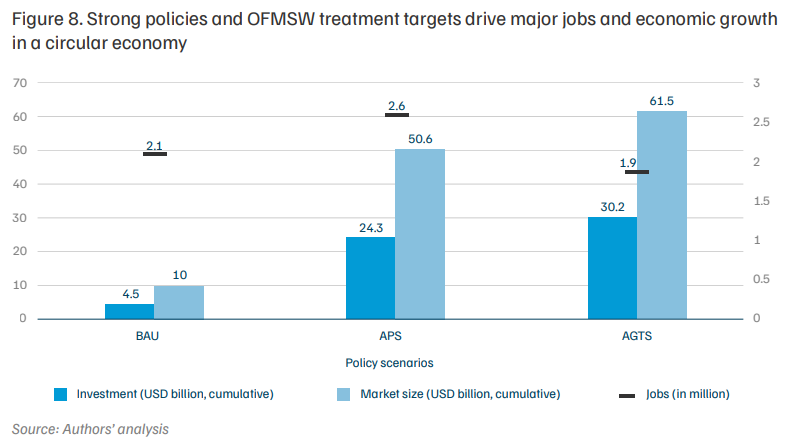

Figure 8 provides a comparative outlook for jobs, investment, and market opportunities of all three scenarios for 2047. The data show that BAU offers a modest gain, with significant job creation but limited investment and market size. At the same time, APS, with its transitional policy pathway, offers better opportunities in all three dimensions of employment, markets, and investment. By contrast, AGTS, which favours biogas technology, looks promising in terms of investment and market opportunities, but it creates fewer direct jobs than APS. These different scenarios demonstrate the economic potential of integrating sustainability with OFMSW management.

India’s total GHG emissions have been rising steadily, with waste now representing the fourthlargest contributor to national emissions (NIUA 2025). According to the latest Biennial Update Report, emissions from the waste sector grew by nearly 226 per cent during 1994–2020, driven largely by rapid urbanisation, population growth, and industrialisation (MoEFCC 2024). Lack of source segregation, open dumping and burning, inefficient waste collection, and unscientific disposal are major contributors.

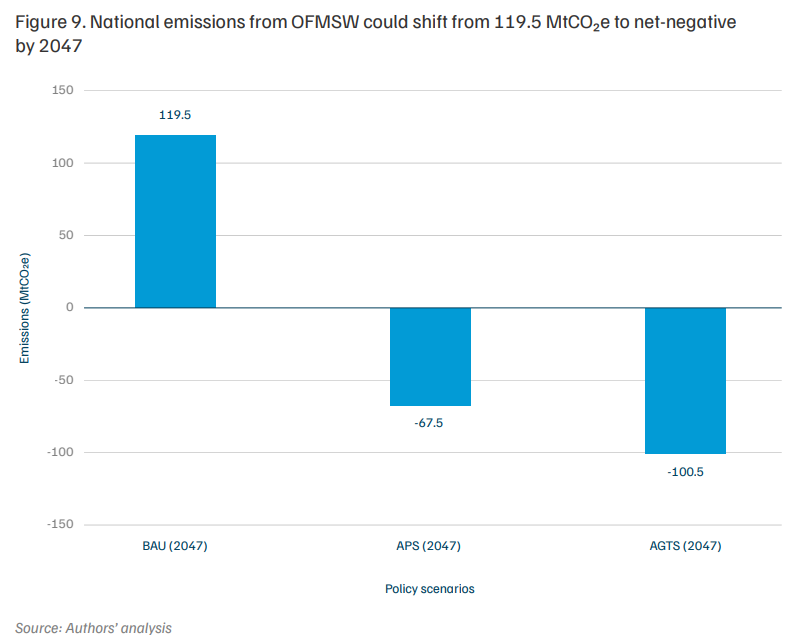

Methane, a potent GHG with a higher global warming potential than carbon dioxide, is primarily generated from waste treatment and disposal facilities. Figure 9 presents emissions across different scenarios, highlighting the significant mitigation potential of effective waste management. Under the BAU scenario, emissions from the waste sector are projected to reach 119.5 MTCO₂e by 2047. In contrast, increasing the share of waste processed through biomethanation and composting, diverting waste away from dumpsites, and utilising end products across sectors such as agriculture, transport, and industry can reduce emissions from its own sector while also displacing fossil fuels and producing bio-fertilisers. Our analysis indicates that, under the APS and the AGTS, these effects could result in negative emissions of 67.5 MTCO₂e and 100.5 MTCO₂e, respectively. This underscores the potential of the circular transition in organic waste management to deliver transformative climate benefits while aligning emissions mitigation with economic growth, green job creation, and the development of sustainable livelihoods.

Managing OFMSW through a circular economy offers significant opportunities for economic growth, energy security, job creation, and emissions reduction. However, despite this potential, adoption could face multiple challenges. Drawing on a review of the literature, expert interviews, and stakeholder consultations, we have captured the barriers and enablers for its transformation across various themes.

4.1 Policy, governance, and institutional framework

This thematic area highlights how sectoral responsibilities are defined, decisions are made, and accountability is enforced across different levels of government. In India, while policies and regulations exist, on-ground implementation and enforcement face multiple challenges.

a. The Solid Waste Management Rules have been in place since 2000, yet enforcement remains inconsistent across cities. While some ULBs have introduced penalties for non-segregation and open dumping, widespread compliance and implementation remain limited.

b. Project implementation is delayed on the ground due to multiple hierarchical processes, which require approval and adherence to regulations across several departments. Further, delays in clearances and land acquisition are among the most significant hurdles.

c. ULBs rely heavily on central grants and often face challenges in effectively utilising them. While central grants primarily focus on providing CAPEX, cities struggle with improper OPEX and weak revenue mobilisation to sustain it.

d. Inadequately designed contracts for private concessionaires often attract opportunistic entities, making it challenging for genuinely committed entities to operate profitably.

e. A key barrier within the legal and regulatory framework of request for proposals (RfPs) and contracts is the absence of a comprehensive procurement act in India, which leads to multiple interpretations and inconsistencies across bidding documents (Hazarika and Jena 2017; Bajpai and Malviya 2024).

“Policies and rules exist for segregation, enforcement remains difficult. Successful examples like Indore or Ambikapur are often due to strong administrative leadership rather than widespread compliance.”

– Urban practioner and policy advisor (Interviewee, anonymised)

Despite these barriers, policy continuity and regulatory reforms provide a solid foundation for accelerating change. Flagship programmes such as the SBM and recent regulatory updates, including the Solid Waste Management Rules, 2026 and blending mandates for CBG are creating stronger compliance mechanisms, clear mandates, and more predictable investment conditions (MoEFCC 2026).

a. Empowering and strengthening the capacity of frontline workers at the city level, such as sanitary inspectors and waste workers, through clearly defined responsibilities and accountability mechanisms can strengthen the enforcement of waste management rules.

b. Structuring contracts with clearly defined key performance indicators (KPIs) that link concessionaire payments to both the quantity and quality of waste provided. Shifting toward product-based mechanisms, where payments are tied to output quality (like compost or biogas), will incentivise segregation and improve performance.

c. Adopt model concession agreements and RfPs developed by the MoHUA to provide stakeholders with standardised documents that offer flexible revenue structures, clear eligibility and qualification criteria, and risk mitigation through payment security (MoHUA 2022).

d. Establishing city investment cells to attract private investment for waste infrastructure projects, along with enabling city-level diplomacy through initiatives such as sister-city partnerships and the C-3, can facilitate knowledge exchange, investment mobilisation, and collaborative partnerships.

4.2 Infrastructure and technology

This theme explores the physical and technical aspects underpinning organic waste management, which face several barriers.

a. A critical challenge is the deployment of technologies that are poorly suited to specific local contexts. Many imported solutions are expensive and difficult to maintain, undermining long-term viability. At the same time, innovation and adoption of indigenous technologies remain limited.

b. A significant number of plants underperform or become defunct over time due to weak adherence to standard operating procedures (SOPs) or reliance on cheaper, substandard equipment. This leads to issues such as odour, leachate leakage, and fires, which not only disrupt plant operations but also raise health and safety concerns.

c. Plant underperformance is further exacerbated by high variability in feedstock quality arising from poor source segregation, which impacts the treatment plants’ overall operational and economic viability.

“Urban local bodies are hesitant to invest public funds in untested indigenous technologies, as there are significant questions and scrutiny for risks taken, but little reward for success.”

– Policy researcher on urban sanitation (Interviewee, anonymised)

Several enablers can significantly enhance the infrastructure and technology landscape for waste management, including:

a. Developing a context-specific approach to technology selection that can ensure that solutions are tailored to a city’s size, waste quality and quantity, financial capacity, and climatic conditions.

b. Incorporating pre-processing infrastructure, such as shredders and drying units, can improve consistency and quality of waste before the actual treatment. This can support more efficient composting and biogas generation, while also reducing equipment wear and downtime.

c. Promoting R&D, collaboration, and local manufacturing to develop cost-effective and scalable solutions suited to varied Indian conditions. Additionally, building an ecosystem with industry collaboration and technology exchange, such as the International Trade Fair for Water, Sewage, Solid Waste and Recycling (IFAT), where foreign companies with worldclass technologies can partner with Indian cities and manufacturers.

d. Developing clear SOPs, providing comprehensive operator training, and ensuring long-term technical support are essential to sustaining the efficient operation of plants.

4.3 Financial viability and business models

The long-term success of an organic waste management system depends not only on policy support and technology but also on economic viability, investability, and scalability. Private players are likely to be attracted to the sector if clear business models and revenue streams are in place. However, several financial and market-related barriers continue to constrain investment and scale-up:

a. ULBs often lack the overall institutional capacity to effectively and efficiently use financial instruments, including green bonds.

b. Concessionaire payment structures are typically based on the volume of waste transported rather than the quality of waste, which can disincentivise waste segregation. Further, current procurement systems often rely on L1 selection (lowest cost), which can compromise quality (Das Gupta 2021).

c. PPP projects face protracted delays in obtaining essential clearances from various authorities, alongside financial issues that impact viability, such as overly optimistic revenue projections, difficulties in mobilising long-term debt, and insufficient user charges (Mamami and Nath 2025; Reddy and Sharma 2017).

d. Heavily subsidised alternatives, such as chemical fertilisers and liquified petroleum gas (LPG), constrain market uptake of end products from organic waste plants. Further, this overuse has led to a rising government expenditure on chemical fertiliser subsidies, which stood at INR 1.6 trillion in 2024 (Ministry of Chemicals and Fertilisers 2024).

e. The establishment and maintenance of plants, especially CBG facilities, are capital-intensive and involve high operational costs, which can deter investment from small private players.

“If the selection of the contract is solely based on the lowest bid after technical qualification, it often compromises quality. Many times, agencies quote absurdly low prices just to get the contract, but are unable to deliver properly.”

– Urban practioner and policy advisor (Interviewee, anonymised)

a. To address these barriers, a shift towards bankable projects and innovative financing models is crucial. Concepts such as Urban Infrastructure Investment Trusts (InvITs) are proposed to bundle waste management infrastructure and attract investment through public trading. Enhanced risk-sharing mechanisms, such as Hybrid Annuity Models (HAMs) in PPPs, are advocated to ensure a steady revenue stream for private investors and reduce upfront capital burdens on cities. Table 2 highlights some of these models along with examples.

| Financing mechanism | How it works | Key benefits | Best suited for | Examples |

|---|---|---|---|---|

| Blended finance models | This model combines funding from the following sources: commercial debt/equity (for CAPEX), philanthropic grants (for technical advisory), and a revolving credit facility (for OPEX) from a commercial bank (Blended Finance Task Force and Systemiq 2023). |

|

Projects requiring a mix of capital for different phases (e.g. CAPEX, technical assistance, OPEX). | Sistema.bio used grants (Shell Foundation), debt (Triodos Bank), and crowdfunding to finance biodigesters for small farmers. They also collaborated with corporates, such as Amul and Nestle (Convergence 2021). |

| Urban Infrastructure Investment Trusts (InvITs) | Pools funds from retail and institutional investors to fund a bundle of infrastructure projects (e.g. waste-to-energy, bio-CNG plants). These trusts are then traded on the stock market. |

|

Large, capital-intensive infrastructure, particularly in Tier-2 and Tier-3 cities, where municipal revenues may be insufficient (Sharma 2013). | While new to waste management, this model has been successful in the highways and real estate sectors, demonstrating its potential (Construction World 2025). |

| Integrated utility billing | Consolidates various municipal service charges (such as waste management, water, and sewerage) into a single bill, often linked to an existing, high-compliance bill similar to electricity. |

|

Municipalities that are struggling with low collection rates for user fees and seeking to establish a more reliable revenue stream. | In Johannesburg, residents typically receive a single monthly bill that includes property rates, water, sanitation (sewerage), electricity, and refuse removal (Joburg n.d.). |

| Hybrid Annuity Model (HAM) | PPP model where the government provides 40 per cent of the initial capital during construction (CEPT 2018). The private partner arranges the remaining 60 per cent and manages the project for a concession period. The government repays the private partner in fixed annuities. |

|

Large-scale, capital-intensive projects where user charge collection can be efficiently managed and guaranteed by the government. | The Namami Gange Programme used the model to finance sewage treatment plants in cities such as Varanasi and Haridwar (MoJS 2025; Mehta et al. 2018). |

Source: Authors' analysis

b. The National Bioenergy Programme acts as a significant financial catalyst by providing substantial CFA to ULBs. By offering grants that can reach up to INR 10 crore per plant, the programme drastically reduces the initial capital burden of setting up biogas/ CBG units (MNRE 2023b).

c. The mandate of CBG Blending Obligation (CBO) at 3 per cent for 2026-27 of total CNG/ PNG consumption (MoPNG 2024), (which is increasing to 4 per cent next year) is a transformative policy shift that provides investment certainty for production infrastructure.

d. The government has been promoting natural farming through programmes, such as the Paramparagat Krishi Vikas Yojana, the Mission Organic Value Chain Development for the Northeastern Region, and the National Food Security Mission (Joshi and Hughes 2023).

e. Schemes such as the Market Development Assistance (MDA), introduced in 2023, offer support for marketing biofertilisers and partially offset the costs of processing and distributing digestate-based fertilisers (MCF 2023). These schemes, when coupled with a strengthened quality control infrastructure, would provide sufficient incentive for farmers to increase usage.

4.4 Human resources and capacity building

The success of waste management initiatives is directly linked to the motivation and capabilities of the personnel involved. Without addressing human resource constraints, even financially viable projects supported by appropriate technology are likely to underperform or fail. Several challenges related to human resources and capacity building persist, including the following:

a. ULBs are often understaffed relative to the increasing volume and complexity of waste management and often lack sufficient officers and sanitary inspectors to carry out the work required (Singh 2020).

b. Worker motivations remain low, as their work tends to be reactive and involves daily firefighting with municipal operations rather than proactive planning and management. Municipal staff are often primarily concerned with avoiding escalations or career repercussions, which discourages initiative, risk-taking, and long-term planning.

c. Lack of technical expertise and local capacity within ULBs leads to officials being inadequately equipped to understand and address the operational and technological nuances of waste management systems.

d. Absence of structured workforce planning and performance assessment mechanisms could result in duplicate or unclear responsibilities, leading to inefficient operations.

“If you have skilled human resources who understand the topic, the mechanisms, structures and processes, then they can set up or formulate projects which can become bankable.”

– Organic waste expert (Interviewee, anonymised)

Mission Karmayogi–the National Programme for Civil Services Capacity Building (NPCSCB), aims to promote citizen-centred governance in India. Central to this mission is an emphasis on competency-driven capacity building and human resource management, with a focus on enabling role-based capacity building that empowers government officials to take ownership of their professional development (ISTM 2021). To oversee this transformation, the Capacity Building Commission (CBC) was established to foster a shared understanding and promote coordinated functioning across departments as a unified system (CBC 2026; ISTM 2021). Additional drivers that can strengthen capacity and support sector-wide development include the following:

a. Municipal reforms that can include detailed organisational analyses to determine workforce requirements and identify the skills required, alongside strategies for upskilling or crossskilling existing staff.

b. ULBs need to augment capacity across organisational, institutional, and individual levels. Annual Capacity Building Plans (ACBPs) provides a bottom-up framework for identifying skills gaps and training needs assessment (CBC 2026). Further, platforms such as Integrated Government Online Training (iGOT) platform, onboarding of training institutes, and immersive learning sessions enable a structured training ecosystem and capacity development across departments and ULBs (CBC 2023).

c. Empowering frontline staff, including sanitary inspectors and waste workers, would grant them the power and support to enforce compliance. For instance, local staff could be authorised to reject unsegregated waste from different generators. Non-governmental organisations such as Stree Mukti Sanghatana have demonstrated models that support livelihood creation and the inclusion of waste pickers (Mhapsekar n.d.).

d. Attracting young, skilled workers to ULBs and the waste management field can help build long-term institutional and technical capacity.

e. Targeted training programmes and knowledge-sharing initiatives on various aspects can support municipalities and private entities. Government bodies such as RCUESs can play a crucial role in evaluating city-level data and conditions, conducting training, providing support in developing strategies and action plans, organising stakeholder meetings and workshops, and compiling the necessary documents for validation (AIILSG 2020). Further, eight BDTCs have also been established at recognised technical institutions to provide entrepreneurship education programmes to motivate beneficiaries and impart biogas technology for self-entrepreneurship (MNRE 2023a).

4.5 Data and information

In the changing waste scenario, data and information systems play an essential role in empowering policymakers, private players, and other key stakeholders to take data-driven decisions. The baseline data are crucial for planning infrastructure and deploying tailored technology in the region.

a. Many Indian cities lack access to accurate waste generation and composition data. Municipalities often rely on outdated surveys, sometimes decades old, or on broad assumptions, such as PCWG estimates or fixed wet-to-dry ratios (for example, 60:40), which may not reflect local realities.

b. The lack of national standards and methodologies for conducting waste characterisation studies for MSW leads to inconsistent or incomparable datasets.

c. ULBs frequently operate with limited monitoring and accountability mechanisms, which can affect the long-term maintenance of waste management infrastructure. This can lead to some of the assets being underutilised, poorly maintained, or unsustainable over time.

“Many cities issue tenders for compressed biogas (CBG) plants with either no data or very outdated waste characterisation data for cities.”

– Technology provider to urban local bodies (Interviewee, anonymised)

Various enablers are crucial to addressing data- and information-related challenges, many of which the government and different stakeholders are already undertaking. The MoHUA has conducted the Swachh Survekshan–the world’s largest urban sanitation survey–for the past nine years. In addition, the government has developed dashboards and digital portals to track the progress of programmes such as SBM and GOBARdhan. The iGOT platform under Mission Karmayogi also hosts a course on ‘Data-Driven Decision Making for Government’, which aims to build capacity among government officials and enable them to make informed, data-driven decisions, hence strengthening public service delivery (Karmayogi Bharat 2023).

a. Mandating up-to-date waste generation and characterisation studies as a precondition for waste programme implementation and fund disbursal can enable stakeholders to build and maintain waste data systems.

b. Leveraging geographic information system (GIS) tools and real-time data dashboards at the city level can improve waste tracking and flow management, allowing transparency and management at the hyperlocal level.

c. Developing a robust monitoring, evaluation, and learning (MEL) framework and templates, supported by clear KPIs, can help track and improve waste management outcomes.

4.6 Awareness, behaviour change and social acceptance

Public participation plays a critical role in sustaining effective waste management. Without strong public support, waste remains mixed, leading to the underperformance of facilities and the loss of both economic and environmental value.

a. A cultural context associated with waste, influenced by the notion of pollution and purity, shapes citizens’ attitudes towards waste. Many citizens perceive waste handling as solely the responsibility of municipalities or informal waste workers.

b. Citizens often do not perceive the direct value or benefits of source segregation and face minimal to no penalties for non-compliance, resulting in low motivation and frequent mixing of waste.

c. The ‘not in my backyard’ (NIMBY) sentiment is another significant barrier to establishing waste processing plants, even in locations where land availability and odour concerns are minimal. Additionally, consumer awareness of end products, such as biofertilisers produced by organic waste processing plants, remains limited.

d. Inefficient operations and inadequate technical expertise in running waste treatment plants have led to poorly performing plants, leading to distrust in the reliability of the technology (Mittal et al. 2018).

“Effective awareness means going beyond messaging to direct engagement; visiting every household, securing a commitment to segregate, spending 10 minutes on day one, and following up consistently for 15 days to drive real change.”

– Organic waste expert (Interviewee, anonymised)

Under the SBM-U, IEC and BCC interventions have played a critical role in raising awareness, changing attitudes, and inculcating sustained behaviour change in waste segregation (MoHUA 2022). In addition to these efforts, the government is also addressing research gaps to strengthen the implementation outcomes.

Addressing these barriers required tailored, targeted, activity-based outreach programmes. The first phase of the SBM’s success was driven by its conceptualisation as a ‘Jan Andolan’ or a public movement towards sanitation. The Swachhata Hi Seva campaign is another key initiative that aims to popularise cleanliness as a shared responsibility.

a. Designing specific engagement strategies tailored to different groups within a community, such as housekeeping staff, schoolchildren, spiritual leaders, retired employees, and safai mitras, can ensure broader engagement and understanding of waste management practices.

b. Stakeholder consultations and building local trust that allows transparency are crucial for continuous engagement and collective decision-making. Additionally, grievance redressal mechanisms, including through applications such as Swachhta, can bring municipal services closer to citizens and enable public engagement.

c. Cities need to incentivise positive behaviours and penalise negative ones. This can be done by piloting and implementing systems such as pay-as-you-throw (PaYT), in which higher waste generation results in higher charges. Further, it can be supported through the provision of incentives for segregated waste, such as the reduction of user charges, which can encourage and enable responsible waste management behaviours.

d. Establishing well-managed demonstration projects can help build local community trust and improve understanding of technology viability. These efforts can be complemented by grassroots-level IEC and BCC campaigns to promote waste segregation and other multifaceted barriers to adoption (Mittal et al. 2018).

Biogas and composting each have their own benefits and challenges. Accordingly, decisions on whether to establish a biogas or composting unit should be based on a careful assessment of the specific resources available to a ULB, existing infrastructure potential, and broader sustainability goals. Further, the efficient function of both composting and biogas facilities depends on several key factors, including feedstock quality, operational efficiency, and the availability of welltrained personnel.

To develop a comprehensive understanding of the organic waste management landscape and the range of waste management techniques currently in use, this study examines multiple case studies across different scales of operation.

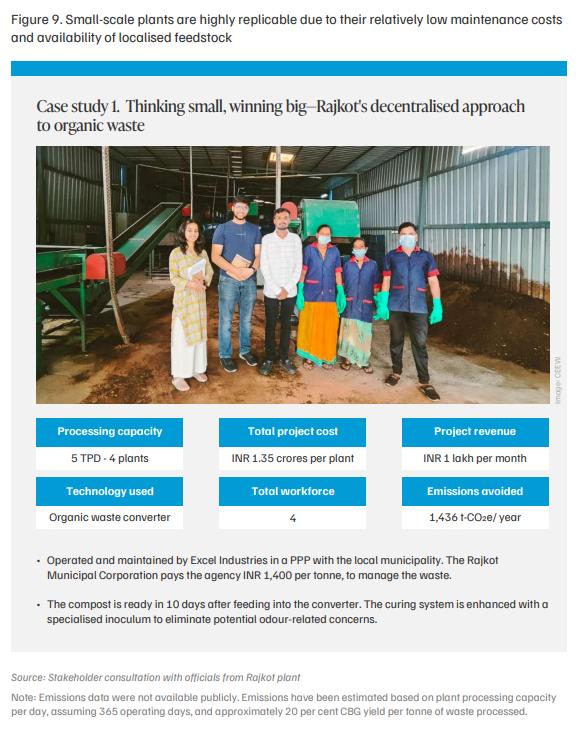

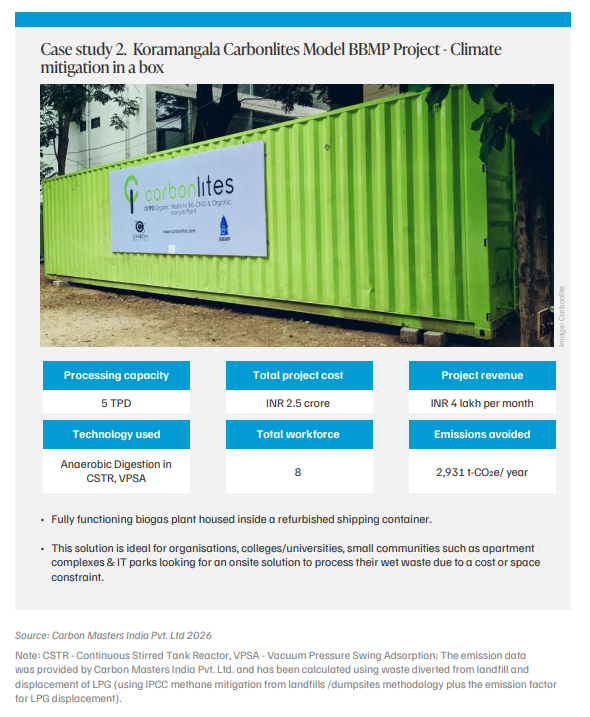

5.1 Small-scale plants

Small-scale decentralised plants are commonly implemented in Indian residential societies, institutions, and at the household level. These plants are of capacity up to 5 TPD and usually do not require detailed permissions and approvals during establishment.

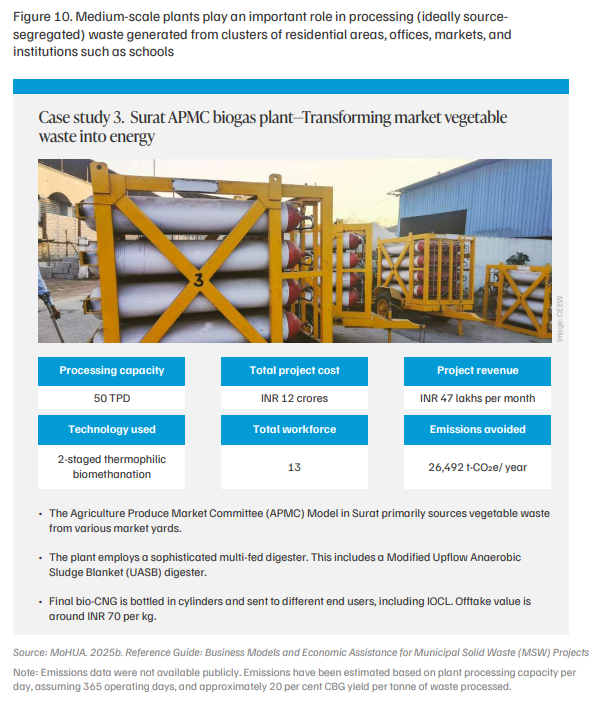

5.2 Medium-scale plants

Medium-scale plants are typically up to 100 TPD range and include ward- or zone-specific solutions. They can also reduce the burden of processing on city landfills and lower transportation costs.

A prime example is the Akshar Biotech plant at the Surat Agricultural Produce Market Committee (APMC) market, which effectively converts large quantities of market waste into biogas.

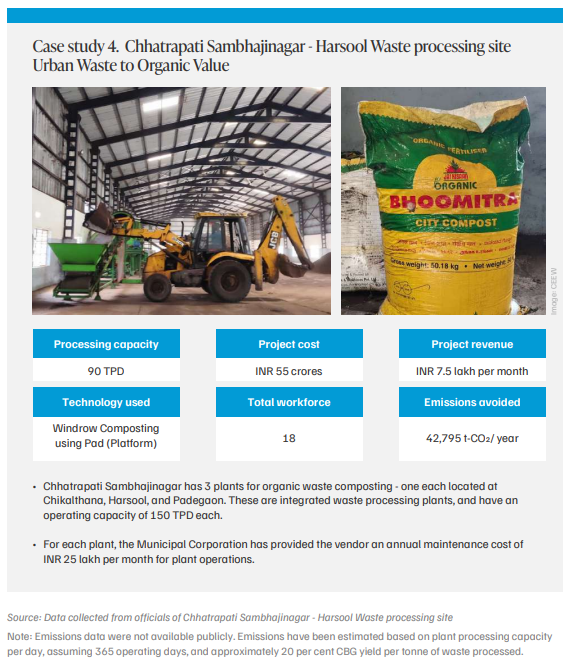

5.3 Large-scale plants (city-wide)

City-wide projects are typically large projects managing over 100 TPD. Most of these plants are usually located on the outskirts of cities to control odour and reduce traffic.

Most of these plants also use advanced and high-cost technologies. However, some of these projects still face significant challenges; for example, in Solapur, the use of the Dry Anaerobic Digestion (DRYAD) technology creates a strong dependency on a very small pool of external specialists for operations and maintenance.

Based on the analysis of the various cases, a key insight that emerged relates to the long-term feasibility of different organic waste processing technologies at scale. While composting is highly effective and replicable in small-scale, decentralised settings (as shown previously), maintaining it at larger scales may prove significantly more challenging, although a few successful examples do exist. Consequently, for managing city-wide projects, especially over 50–100 TPD, CBG or waste-to-energy technologies offer more valuable, scalable, and manageable solutions, as they are better positioned to manage high volumes of waste.

To unlock the full potential of India’s circular economy, coordinated action across various stakeholders is essential to bridge existing systemic gaps. The following strategic recommendations outline key pathways for transforming organic waste into a driver of sustainable urban growth.

6.1 Ensuring optimum quantity and quality of feedstock for plant operations and sustainability

The viability and success of organic waste processing plants depend directly on the availability of high-quality, source-segregated feedstock. Inadequate waste quality and quantities often lead to operational difficulties, underutilisation of capacity, and overall financial non-viability. Addressing persistent challenges of source segregation in cities, therefore, requires coordinated, multistakeholder action. To ensure that organic waste processing plants receive the optimum quantity and quality of feedstock, the following measures are recommended:

Policy makers, particularly the MoHUA, have already developed model contracts, guidelines, and advisories for waste processing plants. These should be disseminated widely with clear feedstock responsibility metrics and KPIs. Further, MoHUA could work with the line ministries to develop sector specific guidelines like with the Ministry of Fisheries, Animal Husbandry and Dairying on food waste use in piggeries, and with the Ministry of Tourism and Culture on floral and temple waste.

Urban local bodies should incorporate and integrate feedstock quality KPIs into their RFPs and concessionaire agreements for organic waste management. These KPIs should also be reflected in servicelevel agreements across the supply chain, including door-to-door collection, transportation, and processing, and should be supported by performance-linked incentives and penalties.

Industry players should mandatorily invest in pre-treatment facilities and flexible multi-feeder technologies capable of handling a diverse range of organic waste.

Civil society organisations and NGOs, working in close partnership with ULBs, should develop tailored IEC interventions, particularly at the household level, to encourage consistent source segregation. This would require door-to-door outreach, community feedback loops, and sustained monitoring, which can then build behaviour among residents and waste collectors.

Assured access to high-quality, segregated feedstock is critical to plant performance.

6.2 Creating an up-to-date database of waste quantification and characterisation and leveraging digital infrastructure for monitoring, evaluation, and optimisation

Data plays multiple critical roles in waste management, including infrastructure planning, technology selection, monitoring, and evaluation. However, many cities continue to lack up-todate foundational data on waste generation and composition. To drive data-driven decisionmaking, we recommend the following actions for the key stakeholders:

Policymakers from MoHUA have already undertaken multiple initiatives to strengthen data-driven planning, from conducting the world’s largest urban sanitation survey through Swachh Survekshan to developing the Management Information System (MIS) dashboard on the progress of the SBM-U. Building on these efforts, MoHUA can take the lead by mandating periodic waste characterisation studies, conducted through bodies like NABLaccredited laboratories or other qualified agencies using standardised protocols, as one ofthe preconditions for project approvals or fund disbursement. For instance, waste management projects under the City Investments to Innovate, Integrate, and Sustain (CITIIS) 2.0 mandate new waste characterisation, which can then be extended to other initiatives, including the recently announced Urban Challenge Fund.

Municipalities should recognise the importance of establishing and maintaining a comprehensive baseline of waste data. This necessitates collaboration with subject matter experts and specialised firms to conduct feasibility assessments and waste characterisation studies. Moreover, cities should leverage digital infrastructure, such as integrated command and control centres (ICCCs), which were developed under the Smart Cities Mission (SCM) for multiple waste management applications, including tracking waste generation and segregation, monitoring collection vehicles in real time, and addressing citizen grievances.

Private sector entities should invest in advanced monitoring tools, such as IoT-enabled collection systems and real-time analytics from BioCNG facilities, to track and optimise operations.

Regulatory bodies, such as CPCB, and academic institutions, such as NEERI or the IITs, should collaborate and standardise characterisation methodologies nationwide. This would enable data consistency and comparability. Additionally, these institutions should develop training modules and courses to build local technical capacity on data management and emerging technologies.

Academia and CSOs collect granular datasets through field surveys, which can play a crucial role in capacity building, community involvement, and the dissemination of best practices for utilising datasets.

6.3 Building workforce capacities, expanding training centres, and having a responsibility matrix

Capacity building should go beyond technological aspects to include competencies in governance, financing, planning, regulatory compliance, and service delivery (CPHEEO 2016).

Digital capacity-building platforms, such as iGOT-Karmayogi under Mission Karmyogi, should introduce more courses to upskill and build the competencies of government officials in the waste management sector (MoHUA 2024). Evaluation of these courses by assessing the number of people completing the course, also feedback should be taken to improve the content.

Industry associations, including the Federation of Indian Chambers of Commerce and Industry (FICCI ), the Confederation of Indian Industry (CII), the Compressed Biogas Producer Forum (CBPF), the Indian Biogas Association (IBA), and others, play a crucial role in providing platforms for dialogue, facilitating growth, and advocating for the sector.

The geographical coverage of BDTC centres is limited and should be expanded across more regions to ensure equitable access to training. Leveraging R&D institutions, such as the Council of Scientific and Industrial Research, BARC, IITs, and other technical institutions, can play a crucial role in research, innovation, technical guidance, co-development of training modules, and the preparation of SOPs for organic waste treatment technologies. Sardar Swaran Singh National Institute of Bio-Energy (SSS-NIBE) could be designated as a nodal agency to guide and coordinate BDTC expansion and oversee curriculum development.

Civil society organisations and NGOs should actively engage in training and providing employment opportunities for SHGs and informal sector workers, thereby promoting inclusive growth and strengthening the workforce across the waste management value chain.

6.4 Strengthening procurement and compliance systems to encourage investment and improve project delivery and performance