Council on Energy, Environment and Water Integrated | International | Independent

Suggested citation: Agrawal, Shalu, Disha Agarwal, Prateek Aggarwal, Dhruvak Aggarwal, Arushi Relan, Harsha V. Rao, Rashi Singh, et al. 2023. Policy Study on Energy Transition Roadmap 2030. Jaipur: CMRETAC, Government of Rajasthan.

India’s energy transition journey will be realised in its states and union territories. Rajasthan, bestowed with abundant renewable energy (RE) resources, has the opportunity to leverage the advantage to drive its own clean energy transition and support the nation’s transition. As Rajasthan pursues ambitious energy transition goals, it will be essential to enable cost-effective integration of RE at scale and increase the off-take of clean energy by state discoms. To achieve this, the state must address the key questions:

The Chief Minister's Rajasthan Economic Transformation Advisory Council (CMRETAC) commissioned the Council on Energy, Environment and Water (CEEW) to reflect on these questions and prepare a roadmap for the state’s power sector transition. CEEW undertook a study based on an in-depth analysis of the state’s power sector landscape and the emerging and potential challenges, using modelling tools, secondary research, and consultations with diverse stakeholders. The recommendations aim to assist all key state actors in undertaking timely and data-informed decisions on policy, regulatory, institutional, and financial reforms to help the state leverage its natural advantages of high clean energy potential.

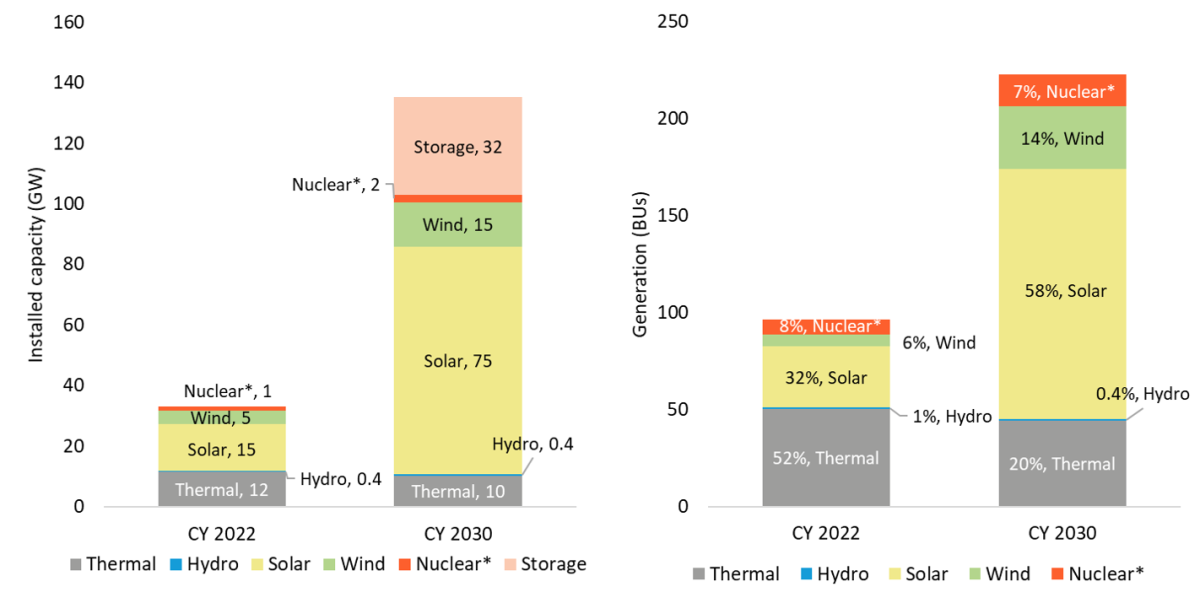

The transition required to meet India’s ambitious clean energy goals will take place in its states. By 2030, India aims that 50 per cent of its installed power generation capacity will be based on non- fossil energy sources, and its emissions intensity of GDP will reduce by 45 per cent (over 2005 levels). Rajasthan, with abundant renewable energy (RE) resources, is positioned to lead India’s energy transition to cleaner sources of energy. The state is already the largest producer of RE in the country with more than 23 GW of installed RE capacity in June 2023 (MNRE 2023). The Government of Rajasthan (GoR) aims to achieve 37.5 GW of RE capacity by 2025 (MNRE 2022), and ~90 GW by 2030 in line with enhanced national clean energy targets. However, an assessment of the state’s past efforts and current context shows that several challenges may impact the pace of this transition.

A holistic approach is needed to determine future transition pathways for Rajasthan’s power sector such that the transition is aligned with the state’s development aspirations, nation’s international commitments and the changing global context. An understanding of the long-term pathways should inform the state’s medium-term policy goals, which in turn should guide the state’s near-term strategies for sectoral transition. In this backdrop, the Chief Minister’s Rajasthan Economic Transformation Advisory Council (CMRETAC) commissioned CEEW to develop an Energy Transition Roadmap 2030 for the state’s power sector. This roadmap, developed by CEEW with support and guidance from CMRETAC, is based on an in-depth analysis of the state's power sector landscape, emerging and potential challenges, and use of suitable modelling tools and secondary research to answer the following key questions.

The underlying research and roadmap development has benefitted from multiple rounds of consultations with key actors in the state’s power sector. We hope that this Roadmap is able to assist and inform the Government of Rajasthan in its efforts to leverage its natural advantage of high RE potential to assume a pole position in India’s clean energy transition and ensuring universal access to clean, reliable and affordable energy for its people.

Our assessment of long-term transition pathways for Rajasthan suggests that aligning with the national aspirations of building a Net-Zero economy by 2070 would help the state retain its clean energy leadership while meeting its development aspirations.

Pursuing a Net-Zero pathway would present significant opportunities for the state’s power sector, as compared to a business-as-usual scenario, as depicted through the model results below.

To realise these opportunities, Rajasthan should consider enhancing its clean energy ambitions by:

https://www.ceew.in/small-hydropowerRise in share of variable RE (VRE) in Rajasthan’s generation mix would pose several challenges linked to variability and uncertainty in RE generation, surplus availability during low demand (leading to negative net load) and limited inertia or reactive power support available for secure grid operations. In view of these challenges, we assessed the flexibility needs of the state's power system using a national level and a state-level dispatch model.

Our assessment of all-India dispatch model results suggests that:

Figure ES1:With 90 GW of RE in Rajasthan, VRE share in generation would rise to 72 per cent

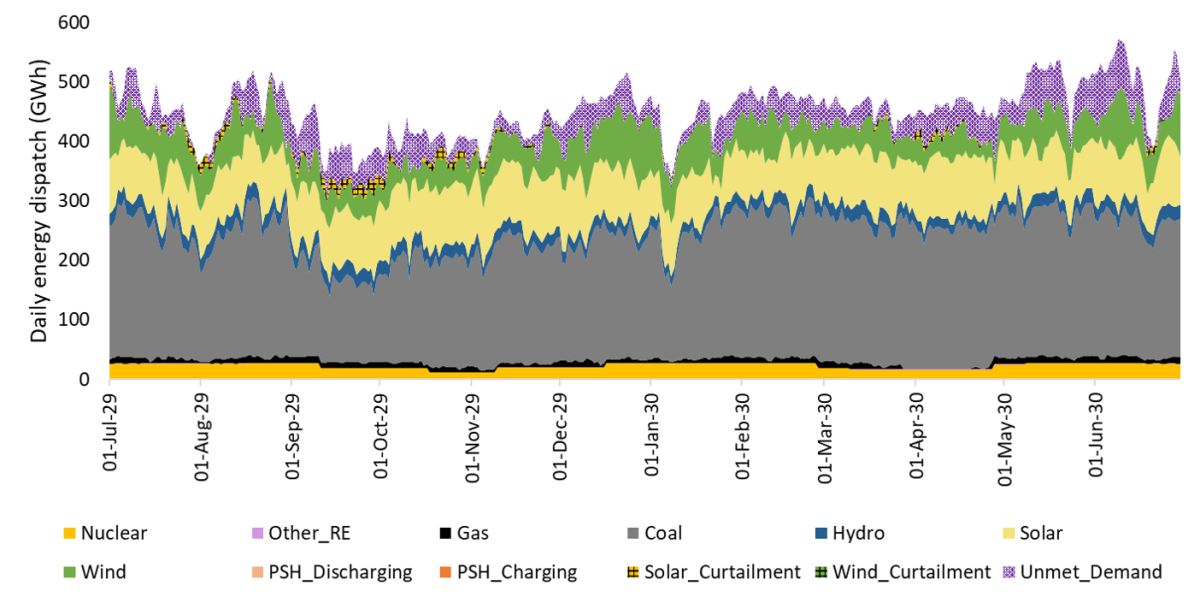

To meet their RPO targets, one-third of the 90 GW RE capacity installed within Rajasthan must be contracted by the state’s discoms. In this scenario, our assessment of the state-level dispatch model suggests that:

Figure ES2: With current and planned conventional generation capacities, 7 per cent of Rajasthan’s power demand would be unmet in 2030, indicating need for more resources

To manage load reliably in an RE-rich power system, flexibility can be enhanced by:

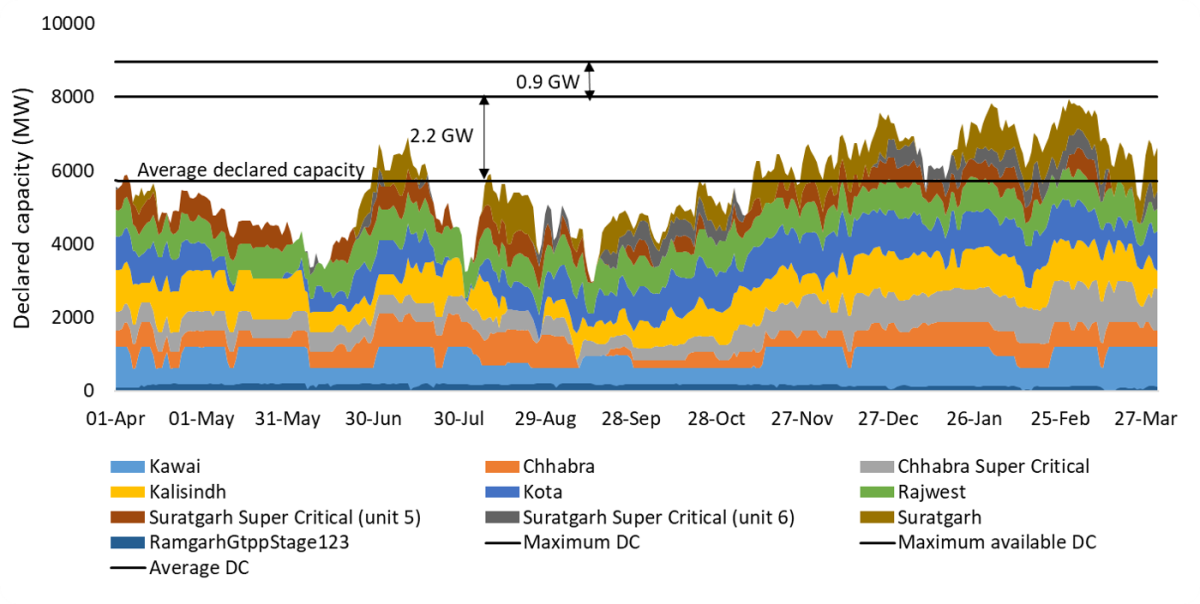

To ensure that the system runs at least cost, flexible operation of coal-based generating resources will have to be managed cost-efficiently. Currently, six state-owned and two privately-owned thermal power plants comprise nearly 40 per cent of Rajasthan’s total long-term contracted generation capacity and half of the annual energy procurement.

Our assessment of current operational trends suggests that:

Figure ES3: Higher declared capacity of the largest state thermal plants could improve peak generation availability by almost 1 GW

State entities can ensure that the coal fleet continues to operate cost-efficiently by:

Rajasthan’s discoms are in financial distress with aggregate technical and commercial (AT&C) losses of 17.5 per cent in FY22, accumulated losses of ~INR 90,000 crore (including regulatory assets worth ~INR 49,000 crore), total debt worth ~INR 66,000 crore, and a low debt-to-service-coverage ratio of 0.91. State discoms are in a vicious cycle of recurring losses, debt, delayed payment to generation companies, poor credit ratings, and high interest burden. Since discoms are the largest off-takers of clean energy, a perception of high off-taker risk is a key barrier to clean energy investments in the state.

Our assessment of the factors leading to loss accumulation suggests that disallowed costs by the state regulator during the true-up process are a major contributor to the accumulated losses of Rajasthan discoms. In FY22, RERC disallowed over INR 6,000 crore of the discoms’ claimed expense, 59 per cent of which pertained to power purchase owing to gaps in forecasting and discoms’ operational inefficiencies. Disallowed costs reflect as losses in the discoms balance sheet, affect cash flows, and add debt and interest costs.

To break out of the vicious circle, Rajasthan discoms must undertake measures to:

We propose a detailed Energy Transition Roadmap until 2030 for Rajasthan based on our assessment of system requirements and the various aspects of power sector operation. The Roadmap (refer to Chapter 6) has been made after multiple rounds of stakeholder consultations and is based on the current understanding of technologies and institutional capacities. The proposed timelines may vary based on the pace of technological developments and momentum of

implementation.

We also propose a two-tier institutional framework that draws from the institutional arrangements under existing policies in the state, such as the Rajasthan Solar Energy Policy, 2019 (Government of Rajasthan, 2019a) and the Rajasthan Wind and Hybrid Energy Policy, 2019 (Government of Rajasthan, 2019b).

“An action-oriented detailed roadmap helps all actors in state to prioritise on timely interventions, which are essential for a smooth energy transition in the state. India’s energy transition journey will be realised in its states and union territories. Rajasthan with its bestowed RE potential is positioned to lead the transition. The roadmap is the first of many steps for the state’s and national journey towards achieving net zero emissions by 2070.”

“Rajasthan is likely to be one of the leading states in achieving national energy transition. With 90 GW of RE capacity installed in the state, it will supply heavy quantums of clean energy to nearby states. Along with this, the state will also share its flexible resources such as energy storage and flexibility from its thermal fleet.”

“Every state has its unique set of challenges and opportunities. The states must identify the growing energy needs of the state’s economy, to identify the clean energy targets for themselves. Some interventions such as having integrated resource planning activities and expanding and modernising the network capacity are essential and common across all states for enabling cost-effective integration of RE. The state must identify and prioritise the interventions to solve the challenges and leverage their strengths.”

“Rajasthan’s energy transition roadmap focuses on state’s journey towards net zero, by (i) identifying short, medium and long term clean energy targets; (ii) preparing the state’s grid to enable cost-effective RE integration; and (iii) improving financial health of discoms, such that they become enabler of this clean energy transition. The roadmap also defines short, medium interventions and roles to be played by the state regulator, energy department, discoms, power procurement company, load despatch centres, state generating company and state’s transmission utility.”

How can India Create a Demand Flexibility Market?

Contracts for Difference for Flexible and Affordable Clean Power

Enabling Corporate India's Clean Energy Transition

Scaling Solar Power for Irrigation in India: