Council on Energy, Environment and Water Integrated | International | Independent

Suggested Citation: Tripathi, Vishal, Debanjan Bagui, Prateek Aggarwal, Peter Hulshof, Arushi Chopra, Daksh Jain, and Avantika Vashishtha. 2026. Scaling India’s Data Centre Ecosystem: Stakeholder perspectives on Infrastructure, Energy, and Resilience. Council on Energy, Environment and Water and SYSTEMIQ.

India's digital economy is entering a new phase. Digitalisation is no longer peripheral to growth; it is now embedded in how productivity, competitiveness, and service delivery are being reimagined across sectors. Artificial intelligence (AI) is being embedded across search, payments, logistics, healthcare, education, and public service delivery, marking the next phase of this transition and reshaping how digital systems operate across the economy. What often goes unnoticed is that this digital layer is powered by a very physical backbone, i.e. data centres that operate around the clock.

Installed data centre capacity has nearly tripled since 2020, reaching ~1.5 GW, and is projected to reach around 6.5 GW by 2030. Total committed investments between 2019 and 2025 reached approximately USD 95 billion, underscoring the scale and capital intensity of the sector.

This rapid expansion carries substantial implications for land, energy, and water. In 2025, data centres account for ~0.5 per cent of national electricity consumption and approximately ~150 billion litres of annual water use, both expected to more than double by 2030. Decisions taken today on siting, power sourcing, and cooling technologies will shape India’s long-term environmental and infrastructure footprint.

Against this backdrop, this white paper examines how prepared India’s data centre ecosystem is to absorb this scale of growth, and whether current market practices, policies, and regulatory frameworks align with long-term resilience. We do so through a review of global and Indian literature and semi-structured consultations with key stakeholders across the data centre ecosystem, including data centre operators, cloud service providers, renewable energy (RE) developers, policymakers, and domain experts.

India’s data centre growth reflects a structural digital transition

Amid the global data centre boom, India is emerging as one of the fastest-growing markets. Rapid expansion of digital services, accelerating cloud adoption, rising AI workloads, and supportive policy frameworks are driving large, capital-intensive data centre investments. Installed capacity has nearly tripled from about 520 MW in 2020 to almost 1.5 GW (JM Financial 2025, CBRE 2025) by mid-2025 and is projected to reach 4.5-6.5 GW by 2030 (Colliers 2025, S&P Global 2025) Over the past few years (2019–25), total committed investments have reached approximately USD 95 billion (CBRE 2025), and are expected to exceed USD 100 billion by 2027.

Land, water, and energy footprint of India’s data centres

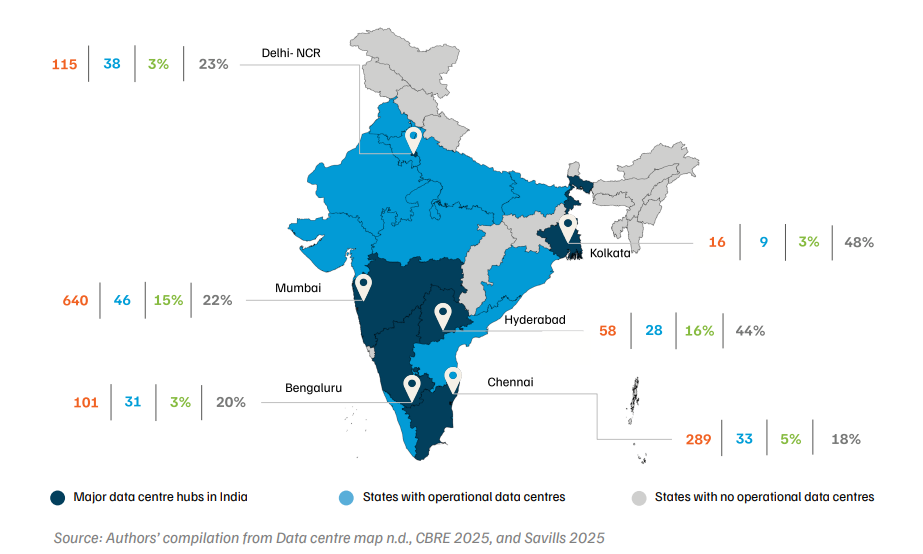

As India seizes this unprecedented opportunity, it must also strike a fine balance between growth and sustainability. Decisions being taken now on siting, power sourcing, and cooling technologies will lock in land, energy, and water impacts for decades. In 2024, data centres accounted for around 0.5 per cent (Cornell 2025) of national electricity consumption and approximately 150 billion litres (Mordor Intelligence 2025) of water use, both figures projected to more than double by 2030. As of January 2026, India hosts ~271 data centres1 (Data centre map n.d.), occupying ~23 million square metres (CBRE 2025) of land. With nearly a quarter of the total data centres, Mumbai leads the market, followed by Chennai, Hyderabad, and Bengaluru.

A hybrid approach to assess the data centre ecosystem

This white paper examines how prepared India’s data centre ecosystem is to absorb this scale of growth, and whether current market practices, policies, and regulatory frameworks align with long-term resilience. We do so through a review of global and Indian literature and semi-structured consultations with 24 key stakeholders across the data centre ecosystem, including data centre operators, cloud service providers, renewable energy (RE) developers, policymakers, and domain experts.

States have led data centre policy development

India does not yet have a binding national policy framework for data centre development, and state governments have taken the lead in shaping the sector’s growth. This trajectory mirrors other sunrise sectors, such as green hydrogen (Pal, et al. 2025), where early state-level incentive and promotion policies preceded the articulation of a national mission. At the central level, support for data centres has been provided through targeted enabling measures, including the grant of infrastructure status (The Hindu 2025) and the 2026 Budget announcement of a long-term tax holiday (PIB 2026) extending to 2047. In parallel, 15 states have already notified dedicated data centre policies or used IT/ industrial policies to attract data centre investment.

Figure ES1. Each stakeholder plays a distinct role in the data centre ecosystem

Manage and maintain physical data centre infrastructure

Utilise data centre facilities to run their IT infrastructure and deliver services

Provide sustainable energy solutions for data centres

Shape frameworks, reforms, and governance for the data centre ecosystem

Offer analytical insights on policy, sustainability, and market evolution

Source: Authors’ analysis

The table presents key stakeholder insights across the market, infrastructure, energy, and policy dimensions that are collectively and rapidly shaping the evolution of India’s data centre sector.

Table ES1. Sustaining data centre growth will require better alignment of infrastructure, energy, and policy

| S. No. | Theme | Insight |

|---|---|---|

| 1 | Market growth outlook | Hyperscaler and colocation facilities are expected to dominate India's data centre market over the next decade. |

| 2 | Drivers of data centre expansion | Growth in demand for cloud services, expansion of AI/ML2 workloads, and data localisation requirements are the primary drivers of data centre growth. |

| 3 | Siting considerations | Stakeholders increasingly factor climate risk assessments, including heat stress, flooding, and seismic risk, into data centre siting decisions. |

| 4 | Power backup requirements | Diesel generator (DG) sets remain an indispensable asset for meeting uptime and reliability requirements. |

| 5 | Primary water source for cooling | Small-scale data centre operators (<5 MW) primarily rely on municipal water supply for cooling. |

| 6 | Water risk perception | Most stakeholders currently perceive water availability risks to be low to medium. |

| 7 | Renewable energy feasibility | Renewable energy developers indicate that up to ~80 per cent renewable supply is feasible through geographically diversified solar–wind portfolios combined with battery storage. |

| 8 | Renewable energy adoption incentives | Power-sector incentives are the most influential policy lever across states, with the majority of stakeholders identifying them as critical for accelerating renewable energy adoption by data centres. |

| 9 | Sustainability provisions in state policies | Only 5 out of 15 state policies explicitly embed sustainability-related provisions for data centre development. |

| 10 | Policy implementation challenges | Despite single-window clearance provisions, stakeholders report delays in practice, particularly in land acquisition, building approvals, grid connectivity, and fire safety clearances, slowing deployment timelines. |

| 11 | Role of state policies | State policies are a major driver of data centre investments and capacity build-out in India. |

| 12 | Land–water–energy nexus planning | Stakeholders strongly endorse the need for an integrated land–water–energy nexus framework to guide siting and improve long-term resilience of data centres. |

| 13 | National–state policy alignment | The majority of stakeholders support the coexistence of a national green data centre framework alongside state policies. |

Source: Authors’ compilation

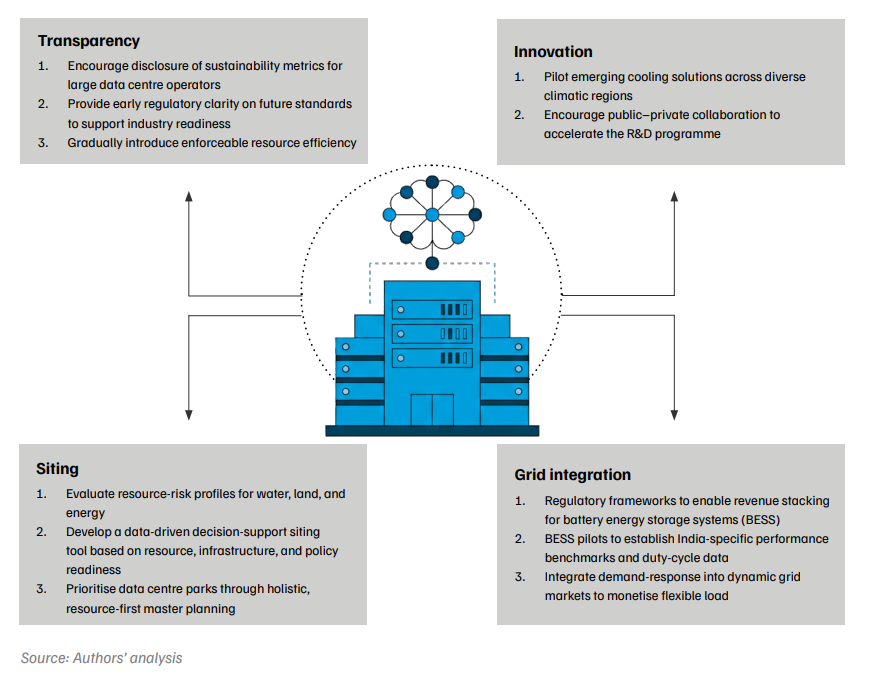

Stakeholder consultations suggest that India’s data centre sector is at an inflexion point. While growth prospects are strong, the scale, pace, and siting of expansion must align with system readiness across power, water, and land. This is particularly relevant in the context of India’s emerging “frugal AI”3 (Economic Survey 2026) pathway, which prioritises application-led, resource-efficient deployment over compute-intensive frontier models. Such an approach places greater emphasis on efficient, shared, and flexible compute infrastructure, underscoring the need for phased growth and early coordination across enabling systems. The way forward, therefore, lies in coordinated action across transparency, innovation, siting, and grid integration, as outlined in Figure ES2.

Figure ES2. Four levers to align data centre growth with sustainability and resilience

In an era where data is considered the new oil and a strategic global currency, data centres act as refineries powering the digital economy. The rise of artificial intelligence (AI) is intensifying the global race to build advanced data and computing infrastructure. As nations scale up digital capacity, integrating sustainability into infrastructure development is becoming essential to ensure long-term responsible growth.

The global AI race is accelerating demand for compute-intensive infrastructure

India is positioning itself as an emerging data centre and AI hub

The domestic data centre ecosystem is undergoing a significant transformation, driven by strong demand, expanding geographic footprints, and accelerating investment flows. The evolving market landscape is being shaped by both domestic and global players, reflecting the sector’s growing strategic importance.

Factors accelerating domestic data centre infrastructure

Figure 1. Core enablers of India’s digital transition

The evolving geopolitical landscape and heightened national security priorities are expected to prompt more sectors to implement data-localisation (CSIS 2021) mandates10 . Together, these measures reflect India’s broader push toward data sovereignty, thereby accelerating nationwide demand for data centre infrastructure.

Regional footprint and capacity expansion

Investment trends and distribution across states

In comparison, the global data-centre market is witnessing similarly strong momentum. More than USD ~60 bn (CNBC 2025) has reportedly flowed into the sector in 2025 alone, underscoring sustained investor confidence worldwide. Looking ahead, cumulative global investments in data-centre infrastructure are expected to reach up to USD 3 trillion (JLL 2025) during the 2026– 2030 period, driven by hyperscale expansion, cloud adoption, and AI-led demand. Insights from stakeholder consultations also indicate that investment is expected to increase significantly over the next few years, globally and in India.

Figure 2. More than ~65% of data centres are located in six regions

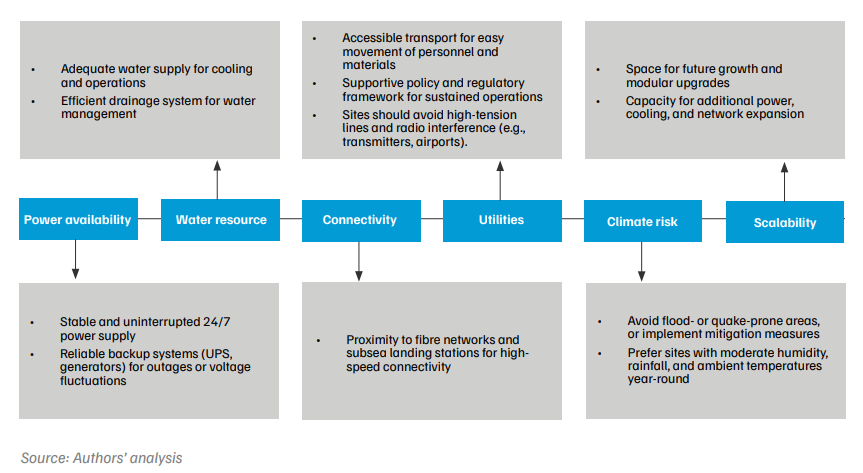

Power and water availability, along with the climate risk profile, are the primary parameters considered when selecting a site for a data centre. Beyond these factors, several additional operational and logistical parameters must also be considered (Figure 3). Given that data centres are designed for long operational lifecycles, it is essential to carefully evaluate all these parameters to ensure operational reliability, cost efficiency, and longterm performance.

Figure 3: Critical factors that define data centre site selection

Access to reliable power is the primary siting criterion

Water availability influences data centre planning

Climate risks increasingly affect operational resilience

In addition to the aforementioned parameters, land availability, the policy and regulatory landscape, and permitting and approval processes frequently determine project viability and development timelines. Connectivity-related factors such as access to optical fibre networks, proximity to subsea cable landing stations, and latency requirements are also critical to ensuring high-speed, low-latency operations. The relative importance of these parameters, however, varies significantly depending on the intended function of the facility, whether hyperscale, colocation, or edge (refer to the Annexure).

Data centre sustainability rests on six levers spanning power systems, cooling, IT equipment, construction, and materials. While all influence outcomes, stakeholder evidence shows that electricity and cooling-related water use dominate delivery risk and long-term lock-in. This chapter, therefore, focuses on how Indian stakeholders navigate these two trade-offs in practice.

Power procurement strategies reflect cost, reliability, and regulatory risk

Overall, stakeholder insights suggest that although data centre operators are pursuing more diversified and cleaner electricity sourcing strategies, these efforts remain bound by physical grid constraints. They highlighted evacuation and capacity limitations in major data centre clusters. However, such grid congestion challenges are not unique to data centres, but mirror those encountered by other large electricity consumers seeking to increase RE procurement.

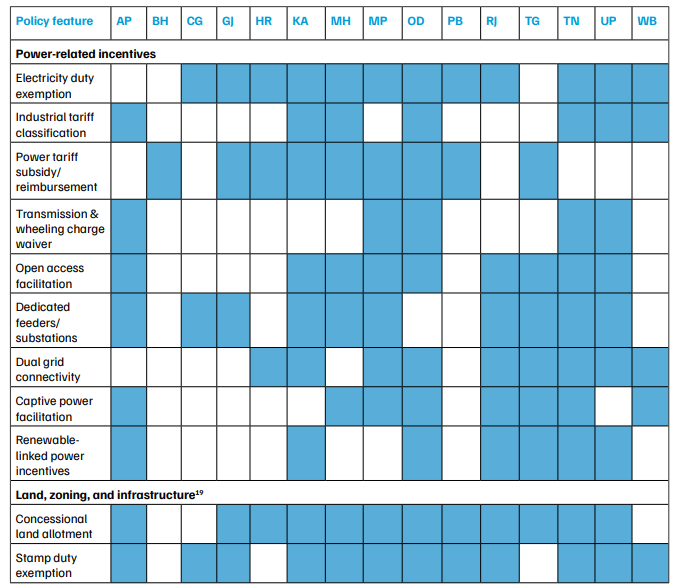

India does not yet have a national policy framework specifically governing data centre development. A Draft National Data Centre Policy (MeitY 2020) circulated by the Ministry of Electronics and Information Technology (MeitY) in 2020 was not notified; instead, central support has been provided through enabling measures such as according infrastructure status (The Hindu 2025) to data centres above 5 MW in 2022 and the announcement of a long-term tax holiday (PIB 2026) for data centre and cloud investments (extending up to 2047) in the Union Budget 2026. In the absence of a binding national framework and with national guidance largely limited to an early compilation of energy-efficiency best practices, (BEE 2010), state governments have taken the lead. Currently, 15 states support data centres through dedicated policies or through IT/ITeS and industrial policies (see Figure 4).

Table 1. Comprehensive comparative matrix of the policy levers across states

Source: Authors’ compilation from 15 states’ policies

As hyperscale capacity expands, future policy leadership will depend less on fiscal generosity and more on systemic integration of energy, water, land, and climate resilience. Rajasthan, Odisha, Karnataka, Tamil Nadu, and Andhra Pradesh offer early templates for such nextgeneration policy frameworks.

Compared to these jurisdictions, India’s regulatory approach remains largely incentive-driven and nonprescriptive, relying on state-level industrial policies, general environmental compliance, and renewable procurement mechanisms. This highlights a growing gap between India’s investment-led data centre expansion and global shifts towards performance-based sustainability regulation.

Rapid digitisation and data localisation requirements have positioned data centres as critical national infrastructure. While there is a broad consensus on India’s long-term demand potential, consultations reveal divergent views on the pace, scale, and conditions required for sustainable growth. This signals the need for a more coordinated and evidence-based approach to sector development. Table 2 outlines indicative pathways for each focus area, reflecting how targeted actions across these domains can reinforce one another and guide the sector’s transition towards more resilient, efficient growth.

Table 2. Structuring the pathways to sustainable data centre growth

| Focus area | Critical questions | Potential pathways | Long-term sectoral benefits |

|---|---|---|---|

| Transparency | How can transparency and evidence become the foundation for sustainable data centre growth? |

|

|

| Innovation | How can innovation be aligned with long-term sustainability outcomes? |

|

|

| Siting | How can siting decisions move from project-level approvals to system-level planning? |

|

|

| Grid integration | How can data centres be integrated into power systems as flexible infrastructure rather than passive loads? |

|

|

Source: Authors’ analysis

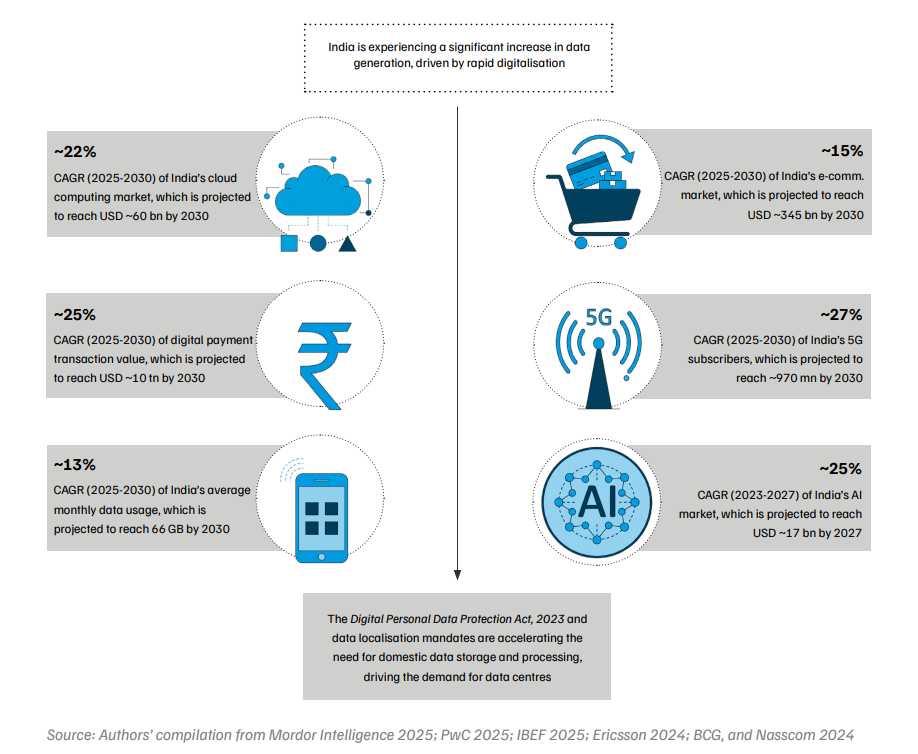

The Digital India initiative, the rapid growth of quick commerce and e-commerce, internet and 5G penetration, the expansion of public digital infrastructure, digital payments, and increasing AI adoption have significantly accelerated data generation. In addition, regulatory developments, such as the Digital Personal Data Protection Act and data localisation mandates from regulators like SEBI and RBI, are further strengthening the case for expanding domestic data centre capacity.

AI adoption is increasing at an unprecedented pace, both globally and in India. Approximately 1 in 6 people worldwide use gen-AI for learning or work-related purposes. More than 80% of organisations globally, and a similarly high proportion in India, are actively using AI in some capacity.

India’s installed data centre capacity stands at approximately 1.5 GW as of 2025 and is projected to grow to 4.5–6.5 GW by 2030. In comparison, global data centre capacity is expected to reach around 200 GW by 2030. Mumbai leads India’s data centre market, accounting for roughly 25% of total facilities, followed by Chennai, Hyderabad, and Bengaluru.

While India does not currently have a binding national-level policy specifically for data centres, state governments have taken the lead in driving sector growth. 15 states have introduced dedicated data centre policies or leveraged existing IT and industrial frameworks to attract investment and facilitate data centre development.

How can India Create a Demand Flexibility Market?

Contracts for Difference for Flexible and Affordable Clean Power

Enabling Corporate India's Clean Energy Transition

Scaling Solar Power for Irrigation in India: