Council on Energy, Environment and Water Integrated | International | Independent

Suggested Citation: Ganesan, Karthik, and Danwant Narayanaswamy. 2021. Coal Power’s Trilemma: Variable Cost, Efficiency, and Financial Solvency. New Delhi: Council on Energy, Environment and Water.

This study examines the thermal, financial and operational performance of the Indian coal fleet with a capacity of 194 GW over the course of 30 months (September 2017 – February 2020) leading up to the COVID-19 pandemic. It explores factors leading to under-utilisation of some of the new and efficient assets. The study assesses the factors driving the efficiency and variable costs of the coal fleet and proposes a counterfactual scenario which prioritises efficiency over variable costs in the dispatch mechanism.

It was a ‘lost-decade’ (2010–2020) for coal-based power generation in India. There was much promise at the beginning of the decade and generation capacity was added at a breakneck pace. Eventually, low economic growth and poor growth in power demand ended up bankrupting the sector that was already teetering on the brink. Today, non-performing assets (NPAs) abound in the sector and recovery of dues is a challenge throughout the value chain. We are at crossroad, where at the global stage, India is contemplating its net-zero emissions timelines, while the only strategy presented thus far has been increasing the installed capacity base of renewable energy (RE).

What about our thermal fleet then? The timelines for compliance with pollution norms have been repeatedly stretched, with plants now being asked to present affidavits of retirement deadlines, if they have any, and benefit from a more lenient treatment. While air pollution legislation has been given prominence, soil and water pollution emanating from millions of tons of ash pile up still goes unnoticed. The COVID-19 pandemic has also dented demand growth and many assets, which are in advanced stages on construction, are in a grip of uncertainty. Alongside, a new market-based economic dispatch (MBED) mechanism for procuring bulk power has been proposed to begin in April 2022. By dispatching power through a central clearing mechanism, MBED aims to reduce power procurement costs by INR 12,000 crore (MoP, 2021). All these developments point to an undercurrent of a storm brewing in the sector, and it is at this moment we ask the question—Can India rethink how it manages its coal-based power generation fleet from here on?

We began this study with an examination of the performance—thermal, financial, and operational—of nearly 194 GW of coal-based generation capacity over the course of 30 months leading up to the start of the COVID-19 pandemic in India. We explored how assets are being utilised and segment them by vintage and ownership. We observed that older plants are generating a disproportionate share of electricity and, unsurprisingly, private sector plants bear the brunt of under-utilisation challenge the sector is facing. When exploring the cost distribution of plants, we find that not only do older plants have low fixed costs but they also have low variable costs and outcompete younger plants in the merit order stack. Even in cases where plants incurring low variable costs are available, plants with higher variable costs are dispatched as they are contracted and preferred by utilities, given their lock-in clause in the contracts. The net impact of the current strategy of utilisation of assets is that the thermal efficiency of the generation fleet in India is an abysmal 29.7 per cent, which in turn points to regulators being lax about such poor technical performance.

Given the inefficient operations of the thermal fleet, we wanted to assess what exactly determines power plant efficiency and the variable costs of generation. Towards this end, we carried out a parametric regression assessment of these two metrics. We find that age, plant load factor (PLF), and the average size of units in a plant play an important role in determining how efficient a plant is. In the case of variable costs, we find that it is largely driven by the cost of delivered coal and to a lesser extent by operational characteristics of a plant such as station heat rate (SHR) and auxiliary consumption. These reinforce the theory that newer vintage plants if operated more consistently, would yield better outcomes to achieve system efficiency and possibly also lower variable costs. This in turn implies better environmental outcomes—lower greenhouse gas (GHG) emissions, reduced output of criteria pollutants, or lesser quantity of ash generated. But the financial implications of this proposition remain to be seen.

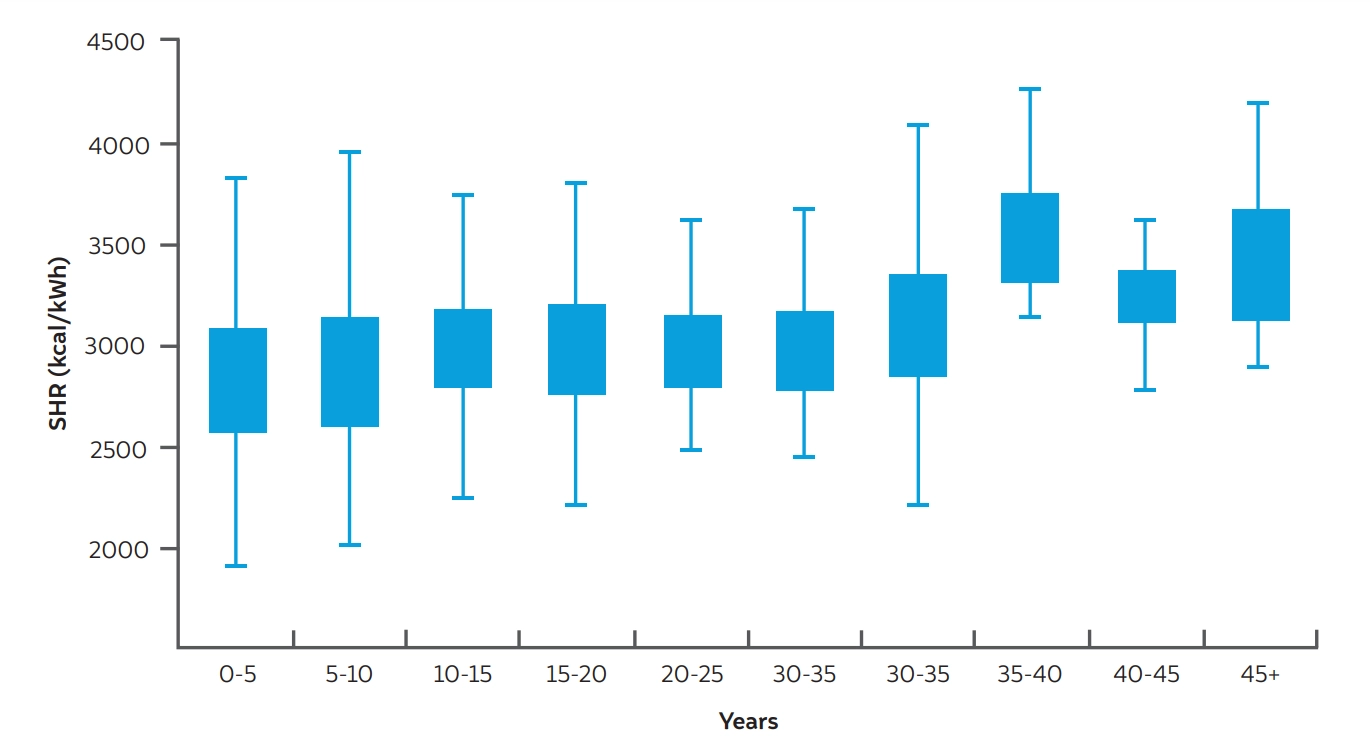

Figure ES1 Younger plants use lesser thermal energy to generate electricity

Source: Authors' analysis

In a bid to conceive of a system where efficiency is rewarded, we demonstrate an approach to dispatch power, based on an efficiency merit order and not the one based on stated variable costs. We chose efficiency as the criterion for dispatch because variable costs are distorted by fuel costs and fuel supply contracts, among others. The order based on variable costs does not mirror efficiency, as evident in our descriptive assessment of the system. As a first step in our approach, we assign higher PLFs to newer vintages, which is inherently a logical step—from operational and financial standpoints of the system. We order plants in an increasing order of estimated SHR, based on the parametric function we established in the first step. Generation schedules are assigned to plants at a daily resolution level, without factoring in spatial and temporal constraints in the movement of power but only providing for the energy demanded in a day. This is a significant limitation, but it is important to understand the nature of unconstrained opportunities existing in the Indian thermal fleet. If the proposed efficiency-based dispatch is employed, the Indian coal fleet would be able to cater to the average energy demanded from it (over the assessment period) at an improved thermal efficiency of 6 per cent over the baseline (the current scenario in action). This implies that the generation efficiency goes up to 31.6 per cent. As a corollary, we find that the reassignment results in an annual saving of nearly 42 MT of coal and a concomitant reduction in GHG and criteria pollutant emissions. The overall fleet also operates at a higher overall PLF of 78 per cent, with significant room for providing more generation should the system require it.

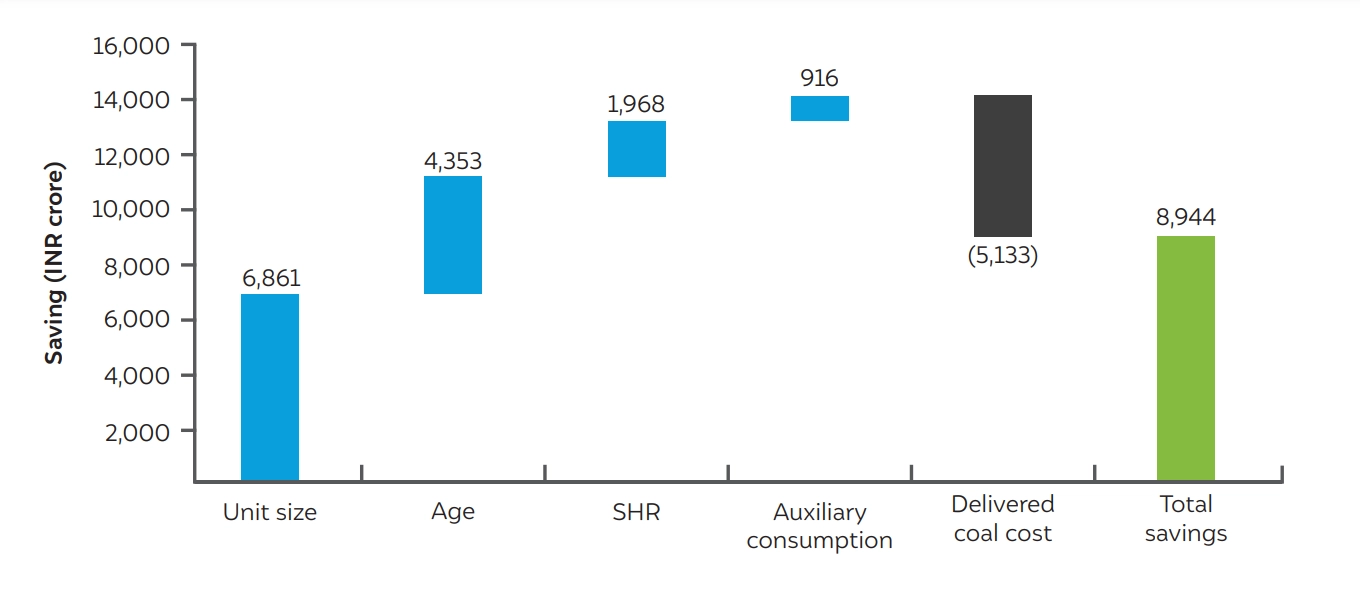

We have structured an efficient generation mix, but does it financially make sense? The drivers of overall variable costs are delivered cost of coal, SHR, auxiliary consumption, unit size and age. In our assessment, we find that the delivered cost of coal in the reassigned scenario increases the overall cost of generation, as 20 per cent of the pit-head plants do not generate in the reassigned scenario. However, plants consume less energy, operate at a higher load factor, and as a result there are significant savings on variable costs of generation. The total savings on variable costs in this reassigned scenario amounts to INR 8,944 crore. Against the overall cost of power procurement by discoms, this is a small fraction, though significant enough to give much needed breathing room for their finances.

Figure ES2 Most of the savings in the reassigned scenario is attributable to improved efficiency

Source: Authors' analysis

As a key outcome, we find that nearly 50 GW of capacity could be deemed as surplus to the requirements of the system, for the energy demand it caters to. Even when considering power delivered, the retained generation capacity could provide for the quantum of peak power required (143 GW in the analysis period) from the thermal fleet. We propose that 30 GW of the surplus capacity, which represents the older and some of the least efficient assets, be taken up for accelerated decommissioning as these have been identified in the National Electricity Plan (2018) for decommissioning during the course of this decade (2021-2030). Each passing year of delay increases the burden on us with a higher electricity bill and more air, water, and soil pollution to manage. It also results in a one-time saving of INR 10,200 crore in avoided pollution-control retrofits, which would otherwise be needed should some of these plants continue to operate. Nearly 20 GW of capacity can be considered for mothballing and based on a more rigorous assessment, it can be decided where they would be called upon to generate if contingencies are likely to arise. We also observe that the system has significant slack, outside of this assessed stock of plants, to manage contingencies and demand growth over the course of this decade. With nearly 36 GW of thermal power in various stages of construction, we find that meeting the electricity and power demand in later years of this decade should not be a matter for concern. Given some key limitations in terms of the spatial and temporal resolution in our study, there is a need to carry out a more rigorous assessment of the opportunities identified in this study. Equally, there is a need to assess electricity demand over the course of this decade and the prospects of RE materialising to the extent that it is currently anticipated in existing studies, in order to conclusively decide on decommissioning and its benefits.

The key contribution of our assessment has been clearly defining the performance metrics of the current thermal fleet in India in terms of both technical and financial aspects. As the data was hitherto not available easily in the public domain, it was compiled patiently and put together diligently for the purposes of the analysis. With data at our disposal, we propose a simple yet powerful way of viewing an alternative dispatch system. Some may consider the assessment incomplete as a result of the limitations stated earlier. However, in the planning horizon, the right set of policies and incentives can very much bring the outcomes envisaged in this study to life.

Despite the simplicity of our conclusions, the proposed reassignment of generation in favour of more efficient plants is far less likely to be operationalised. The Indian power system is mired in a rigid set of bilateral contracts for supply and taking away one to replace with another cannot be easily done. Our approach would leave the states with far lesser control on their sources of power, as many state-owned power generation stations are candidates for decommissioning. Given the challenges of payments for power procured and the broader political economy wielding ‘power’ over ‘owned’ generation assets, such a proposition is anathema to most actors. However, the future of the power system even as envisaged in recent white papers from the central regulator is moving towards a market-based system and does not bet on a bilateral scheduling between generators and discoms. Our proposed approach results in cost savings when viewed as a whole, but individual states are likely to see it only in terms of more costs and less flexibility for their operations.

We have two main recommendations for the Ministry of Power (MoP) and relevant actors as they look to establish the framework for MBED. First, we urge them to establish a set of key performance indicators (KPIs) for the thermal generation fleet, among which environmental footprint associated (as represented by thermal efficiency) with thermal power generation should be accorded priority. Individual legislations on water and criteria pollutants continue to languish, but bringing thermal efficiency to the centre of the debate could lower the costs. And second, we reiterate the need for consensusbuilding among states, in dialogue with central actors, to embrace the notion of a unified market. That the proposed MBED (starting in April 2022) is being carried out in two phases (MoP, 2021) is an indicator of uncertainty in the process. Beyond the implementation framework, we propose that an entity such a National Electricity Council be set up to oversee the concerns of states and central entities and allow for a seamless transition to the concept of ‘one nation, one market’. The challenges of this transition go well beyond the technical domain and must address the needs of state electricity utilities and key entities like Coal India Limited and Indian Railways, and what the future holds for them.

As stated earlier, despite the financial savings being relatively small, our proposed approach to prioritise efficiency opens up a window of opportunity to de-stress generation assets in the sector. By clearing out the stock of inefficient assets, we create fresh breathing room and make a case for more investment in the sector—in RE, energy storage, system upgrades, among others. With the sword of surplus not hanging over the sector anymore, cash flows for stressed assets could improve and, as a result, financial institutions saddled with NPAs could be relieved of their burden. Having gone past this preliminary hurdle, the power sector needs to address some critical issues before it, as it prepares for the larger energy transition.

How can India Create a Demand Flexibility Market?

Contracts for Difference for Flexible and Affordable Clean Power

Enabling Corporate India's Clean Energy Transition

Scaling Solar Power for Irrigation in India: