Council on Energy, Environment and Water Integrated | International | Independent

Odisha, also known as the aluminium capital of the country, is the largest producer of aluminium, steel, and stainless steel in the country. While concrete and steel comprise 90 per cent of offshore wind components, glass and aluminium account for 85 per cent of crystalline solar modules with aluminium capturing 99 per cent market share for frames (Garg and Jain, 2022). Thus, with a strong background in upstream industries, Odisha can generate immense economic value by supporting solar module and wind component manufacturing in the state.

Jobs overview

● 93,500 full time equivalent (FTE) jobs can be created through RE equipment manufacturing in the state of Odisha with 92,690 FTE jobs created through 35,650 MW of module manufacturing and 724 FTE jobs created through 500 MW of wind manufacturing capacity by 2030 1.

Market Opportunity

● INR 44,000 crore (USD 5,300 mn) is the market opportunity in terms of revenue generated from the sale of modules and wind components in 2030.

● Odisha is already looking to expand aluminium downstream industries in the Aluminium Park at Angul and Jharsuguda and steel downstream in the highly industrialised steel park in Kalinganagar. These regions can be districts of focus given features like infrastructure support, connectivity with airports, roadways, and railways, established logistics ecosystem, and assured 24/7 power in these regions (OdishaPlus 2020, Invest Odisha). The industrial park in Angul specifically has proximity to the port, an exclusive skill development centre, and a business centre as additional features whereas, with the development of the East Coast Economic Corridor (ECEC), Kalinganagar will have massive rail, road, and waterway connectivity alongside its natural advantage of proximity to major iron ore mines.

Investment Opportunity

● INR 65,000 crore (USD 8,000 mn) is the investment required to set up 35,650 MW and 500 MW of module and wind manufacturing facilities respectively by 2030.

1. RE equipment manufacturing is a potential downstream industry that can add value to the already existing mineral hubs and industries like aluminium, steel, and stainless steel. As per Odisha’s target of 50 per cent value addition to its base metal products by 2030 (Industries Department Odisha 2023), uptake of this rising sector of manufacturing comes as a perfect opportunity. This will also aid in making Odisha amongst the top three industrialised states in India given the rising momentum and interest from the private sector as well as the central government. This interest can be seen in solar PV equipment manufacturing whereas various measures at the national level have been introduced. These include Basic Customs Duty (BCD) of 25 per cent on imported cells and 40 per cent on imported solar modules effective April 2022 (PIB 2021), MNRE releasing the first Approved List of Models and Manufacturers (ALMM) for solar modules in 2021 (MNRE 2021), recent notification on adherence towards ALMM and support of INR 18,500 crore through the Production Linked Incentive (PLI) scheme for integrated solar manufacturing in 2021 (released in two tranches in 2021 and 2022) (MOP 2023). Further, module exports from China to India saw a 76 per cent year-on-year decline in 2023 (Hawkins, 2023), while India's solar cells and modules saw a 364 per cent jump in FY23 (Koundal and Singh, 2023). These measures show rising momentum in the module industry and an opportunity to capture the market.

2. Odisha can look to become a leader in the eastern deployment market and can become a significant supplier of downstream and midstream components to wind and solar sectors given its geographic advantages and massive potential in the eastern market since renewable energy in eastern states remains a fraction of its potential even after considering land constraints (Jaishankar D. 2023). Odisha is surrounded by water bodies and is among the top 5 states in India in terms of waterbody count with a 450 km coastline (Government of Odisha) providing access to the majority of the Eastern market. With the new Odisha Port Policy 2022, there is a further push for the integrated development of non-major ports and inland waterways of Odisha which can help reduce transportation costs, attract investment, and support additional deployment momentum in Odisha. Odisha also recently received an investment proposal worth INR 4,950 crore for the deployment of 575 MW of wind energy (PTI, 2023b) signaling rising interest in deployments.

3. In addition to capturing the domestic market, there is a wide opportunity to capture a sizable share of the international module and wind manufacturing market.

a. The wind industry is expecting record installations worldwide in both onshore and offshore markets with 680 GW of new capacity expected between 2022 - 2027 (Hutchinson et al. 2023). However, India currently only accounts for 7 per cent (~12GW) of global wind manufacturing capacity, with a major concentration in China of ~60 per cent (Lee et al. 2022). Worldwide, manufacturers are exploring newer markets to diversify the location of their manufacturing and secure future supply chains to reduce dependence on China. Further, with rising geopolitical concerns, the experience of Covid-19 supply chain disruptions and the increasing need for supply chain diversification, India can make use of the rising worldwide demand and establish itself as the major exporter of wind components internationally (Jain et al. 2023).

b. India is expected to become the second-largest solar module manufacturer in the world by 2025 (Kala 2023). In FY23, India exported $1 billion worth of PV modules to the USA, which accounted for 97 per cent of the total module exports from India. Given this rising momentum in the export market, Odisha can cater to the demand via a set of export facilitation measures, improving export infrastructure and logistics, and making use of its existing port advantage. However, it is also important to note that this market is not certain.

4. Given the labour-intensive nature of various components, RE equipment manufacturing can enable employment opportunities in the state and help arrest migration. Odisha can thus be the first such state with sustained focus on manufacturing and scaling of RE technologies, green equipment manufacturing in particular.

a. In addition to direct employment creation in these downstream sectors, there is a large opportunity for indirect employment creation and the creation of employment in supporting industries like inverters, mounting structures, etc. As per our analysis, a highly automated, large-scale module manufacturing facility generates roughly 30 indirect jobs per 100 MW4 in terms of drivers, facility guards, etc. Further, there is a large employment generation opportunity in supporting structures manufacturing like inverters, mounting structures, etc., and a whole ecosystem exists for supply and distribution. This can help arrest migration in the state in addition to offering additional investment in the state.

Adani Solar is looking to build India's first integrated solar manufacturing facility of 10 GW in Mundra, Gujarat, by 2027 (Adani Solar) with an expectation of creating over 13,000 jobs (PTI, 2023c). This will include the entire solar manufacturing ecosystem from metallurgical grade silicon to PV modules, including ancillaries and supporting utilities, which will be geographically co-located. Backward integration across the value chain (modules, cells, ingots, wafers, polysilicon, and ancillaries - EVA, backsheet, glass, aluminium frames, junction box, and tracker) will help boost India's position as a hub in module manufacturing and help reduce costs associated with the import of upstream components like wafer, ingot, etc (PTI, 2023c). Odisha can look to create such a hub for manufacturing and utilise the interest in the state from Waaree 5 , which is looking to build a 10 GW module manufacturing facility in the state (The New Indian Express, 2023). A similar setup in Odisha will help create an ecosystem of suppliers and growth of MSMEs, which will attract other manufacturers in the state.

1. Role of departments

a. Ministry of New and Renewable Energy:

i. The central ministry will play an essential role in ensuring the cost-effectiveness of solar modules and wind components, adopting indigenous products in India, and ensuring the quality of modules and wind components. Further, support in the form of incentives, technology upgradation may be given to wind component manufacturers to keep up domestic production in line with changing technologies (refer to technical/technological challenges section).

ii. MNRE could also encourage research and development (R&D) via industry-academia collaboration, and look to provide a 25 per cent capital expenditure subsidy for setting up R&D laboratories. Further, MNRE must also mandate minimum research expenditure for integrated solar manufacturers in the long term to spur technology innovation and establish cost competitiveness (Garg and Jain 2022).

b. Industries Department, Government of Odisha - To act as the nodal agency for the development of RE equipment manufacturing industries in Odisha and ensure the creation of an action plan/roadmap for attracting investment in the sector and enabling the setting up of industries. In addition to investment facilitation measures such as the introduction of GO SWIFT 2.0 single window system, unified payment mechanism, etc., the department is to look into coordination between different agents like Industrial Promotion and Investment Corporation of Odisha Ltd. (IPICOL), Industrial Development Corporation of Odisha (IDCO), and District Investment Promotion Agency (DIPA) to facilitate a coordinated approach to achieving a RE manufacturing hub in the state. In addition to ensuring synergies between different departments, it should also look into offering incentives and administrative support discussed in the challenges section such as financial incentives for waste minimisation, R&D incentives for industry, tax incentives, provide deemed approval of open-access renewable energy and remove net metering limits (Garg and Jain 2022), etc. Further, for wind components, the department should offer financial incentives to tackle technology risks in terms of technology upgradation grants/tax incentives / R&D grants and incentivise industry-led R&D and mandate R&D spending (Garg and Jain, 2022).

c. Industrial Promotion and Investment Corporation of Odisha Ltd. (IPICOL) and Department of Micro, Small & Medium Enterprise (MSME): IPICOL and MSME Department to help increase state visibility nationally and internationally (for export promotion) by participating in and organising events and international trade fairs, investor meets, workshops, etc. The scope of "Invest Odisha" is to be broadened with a sustained focus on attracting investment in RE component manufacturing. Further, IPICOL and MSME Department to work towards an investment promotion strategy and a roadmap for achieving certain manufacturing targets in the state with regular investor follow-up activities, assisting in marketing collaterals and presentations, etc.

d. Industrial Development Corporation of Odisha (IDCO) - As the nodal agency for providing industrial infrastructure and land for industrial development and infrastructure projects, it has an important role in mainstreaming the support parameters required for establishing low-cost manufacturing hubs in the state. This includes providing land acquisition services for industrial setup - identifying suitable land parcels with low leasing rates and high connectivity (Garg and Jain 2022), development of industrial complexes for supply chain integration of RE equipment manufacturing, etc.

e. District Investment Promotion Agency (DIPA) - Already in operation in Angul and Jharsuguda, this cell at the district level can be developed in other districts to ensure investment facilitation, project monitoring, and aftercare services 6 . This would include active planning on developing the supply chain ecosystem discussed later in this note. To strengthen the supply chain ecosystem, it is important to attract investment in different sectors of RE equipment manufacturing supply chain, logistics management, advocacy for industrial infrastructure development, and other general roles of DIPA (Invest Odisha).

f. Odisha Skill Development Authority - OSDA to play an important role to support labour requirements through skill training initiatives in material handling, software, mechanical and electrical skills, and STEM-related courses (required in wind component manufacturing). This will require close collaboration with industry, academia, and ITIs. It is important to address the skill-related challenges in the recommended manufacturing hubs to be able to operationalise supply chain integration and logistics ease.

2. Role of the private sector

a. Collaborate with academia for R&D and spur innovation via financing technology development initiatives.

b. Invest in large-scale production and make complete use of the capacity for large-scale economies of production. Increasing capacity utilisation of facilities from 50 per cent to 100 per cent is found to make India more cost-competitive with China with a reduction in price differential by 22 per cent (Jyoti 2021).

c. Collaborate with academia and OSDA to actively improve training modules for large-scale preparedness of the workforce. d. MSMEs have a very important role to play when it comes to complete supply chain integration (Shardul et al., 2022). It will become important for the private sector to establish this network of supply to be able to improve logistics access and uptake.

1. Technical / Technology related challenges and associated mitigants

a. Cost of technology is a major challenge to improve the uptake of Indian solar modules. Currently, Indian Mono PERC modules are ~103 per cent more expensive than their Chinese counterparts 7 . Further, Chinese module suppliers have an average profit income of 4.3 per cent while Indian manufacturers are at less than 3 per cent. (Jyoti 2021) These are due to factors like large-scale production in China, low import dependence, robust R&D, and complete supply chain integration. Increasing the capacity utilization of manufacturing facilities from 50 per cent to 100 per cent can lower the price differential to 22 per cent, making Indian modules more competitive (Jain et al., 2020).

b. Bill of Materials (BOM) which accounts for 50-60 per cent of production costs (Garg and Jain, 2022) is ~154 per cent more for Indian modules as compared to Chinese modules 8 . Thus, it is important to reduce the bill of materials cost to help reduce Indian module costs. Apart from solar cells, key BOM elements for solar modules include solar glass sheets, encapsulant films, backsheet, aluminium frame, and junction box (Garg and Jain, 2022). Odisha, with its large aluminium production and mineral ore reserve, can help indigenise production of these materials (Aluminium has over 99 per cent of the market share for frames and even a backsheet is typically of aluminium as per CEEW, 2023). Moreover, with players like Waaree who have already announced a 10GW integrated solar equipment manufacturing facility in Odisha, the momentum of localization and large scale of production, if maintained and improved on, can significantly reduce overall module costs (The New Indian Express 2023).

c. When it comes to Wind equipment manufacturing, India has already achieved 70-80 per cent indigenisation (MNRE, 2020) with high participation from MSMEs in midstream and upstream manufacturing which includes components like generators, gearbox, bearings, etc. However, wind turbine components are highly specialised, and with newer turbine models (Developers are moving towards 3MW+ turbine models), there is a large challenge of constant technology upgradation and keeping up local manufacturing. Based on our consultations with industry, it was realised that it is majorly the MSME sector that faces these challenges given their majority presence in component manufacturing. The unavailability of components like large castings, generators, etc., can lead to significant supply chain challenges and add to the cost difference in turbine components compared to China. These components contribute to ~55 per cent of total turbine cost, with a cost differential of INR 0.9 - 1 crore per MW between Indian and Chinese wind turbines (Jain et al., 2023) To be able to keep up with these technological improvements as well as push for 100 per cent indigenisation and building export capacity, the industry has been pushing for an extension of the Production Linked Incentive (PLI) scheme to wind energy component and sub-component manufacturers (PTI 2023a).

Introducing a PLI scheme for investments in casting, gearbox, and nacelle assembly will help vertical integration in domestic manufacturing, which is currently heavily reliant on China with 50 per cent dependence on hub castings and more than 90 per cent for gearbox castings in China (Jain et al. 2023). Further, monetary support can also take other forms like tax incentives, subsidy support, or other forms of technology upgradation support (for instance the Technology Upgradation Fund Scheme introduced in the textile and jute industry in 1999) which Odisha can look into in order to build a robust ecosystem of wind component manufacturing and become a state leader in the country for both indigenous and international demand.

d. Lastly, most of the technical challenges faced in RE equipment manufacturing are due to the country's lack of a robust research and development framework. 1-3 per cent of the gross revenue generated is utilised for R&D by Chinese players every year, whereas Indian players do not invest much in R&D (Jyoti 2021). There is a large gap in Indian R&D efforts, and to be able to scale effectively, domestic capacity and technological know-how need to be expanded.

Odisha can specifically contribute to R&D efforts when it comes to RE equipment manufacturing upgradation via its Renewable Energy Research Institute as notified in the Odisha Renewable Energy Policy 2022. The Institute can tie up with national and international institutes, private players, and academic institutions for the holistic improvement of manufacturing technologies. In addition to the R&D initiatives mentioned in the RE policy, a capital subsidy on equipment/machinery for supporting new R&D centres limited to the first few units in the state can also be explored.

2. Need for supply chain integration and establishment of RE equipment manufacturing hub in Odisha.

a. As has already been elaborated above briefly, a major challenge to solar module manufacturing is the high cost of modules which stems partially from the lack of adequate upstream and midstream capacity in the value chain. There is currently no polysilicon and wafer production in India and limited cell manufacturing due to which module production becomes more costly since the other components are imported. With the Tranche-II of PLI scheme for High Efficiency Solar PV Modules, there is rising momentum in India to capture the entire supply chain to be able to gain cost competitiveness in its domestic modules.

However, this will require significant capital investment with an estimated total of USD 198 million per GW of polysilicon, ingot and wafer, cell, and module manufacturing (Garg and Jain 2022). Measures like applying BCD (Basic Customs Duty) on polysilicon or wafer imports from 2026-27 can catapult indigenous capacity, while Odisha can specifically look to incentivise the setting up of integrated manufacturing facilities/upstream component manufacturing and become a leader in the country. To be able to do so, certain measures needed to set up a manufacturing hub and improve ease of doing business are elaborated below.

b. Further, steel is a major component in tower and nacelle (concrete and steel comprise 90 per cent of the material requirement for onshore wind farms as per Lee et al. 2022). However, a specific grade of steel (highly specialised to the wind sector) is required, which is currently imported from China due to low production volumes in India. Given Odisha's pioneering steel production (the largest producer of steel and stainless steel) in India, it can look to incentivise production of the particular steel plates required and thus, take a step towards supply chain integration.

c. A key component to becoming the leading state in manufacturing is ensuring the creation of a hub wherein different private players set up industries. There is an ecosystem of suppliers, a well-defined supply chain network with infrastructure and transportation ease, and other ease of doing business-related components. Such hubs or clusters enable the co-creation of an ecosystem of suppliers and manufacturers, ensuring that manufacturers across upstream, midstream, and downstream components are adequately placed in the hub to create and strengthen an integrated supply chain.

d. When it comes to PV manufacturing, Gujarat dominates the market with 53 per cent of India's module manufacturing capacity (Mercom 2023) and 57 per cent of upcoming manufacturing capacity (Jyoti 2023) as of 2024. The reason for such dominance is due to low industrial electricity prices and easy access to ports for imports and exports, alongside the presence of large players like Adani and Waaree. Thus, Odisha can capitalise on its port advantage and ensure the creation of an industrial hub by attracting large players to enter the geography with its 100 per cent exemption from payment of electricity duty and reimbursement of power tariff provisions under the Industrial Policy 2022, among various other provisions already in place. It can also provide additional incentives by ensuring creation of a robust logistic corridor, indexation of locally produced commodity prices in steel and aluminium to reduce commodity price shocks, etc. in order to promote module and wind manufacturing (Jain et al., 2023).

3. Skill-related challenges and opportunities

a. With higher capacity production, especially in module manufacturing, the requirement for highly skilled personnel increases. It was observed as per our analysis that in cases of high automation (~80 per cent) and large-scale production, 75 per cent of the individuals in the facility were high or semi-skilled. This figure decreases as automation reduces, with more low-to-medium skilled workers needed in the production/assembly line. This shows that as the sector and technology mature, there will be a rising need for semi to highly-skilled workers with an understanding of material handling, equipment processing, electrical and mechanical skills, software operation skills, etc. Given that a majority of these skills are also applicable to other industries, it is recommended that there is a focused strategy to upskill the youth of Odisha which can be routed via tie-ups of the Odisha Skill Development Authority with academic institutions, ITIs, independent institutes, etc.

b. In the case of wind component manufacturing, the requirement of science, technology, engineering, and mathematics (STEM) professionals is higher in the onshore wind sector as compared to solar PV (Lee et al. 2022). However, on the basis of our analysis, there seems to be no major pressing skill gap in the industry when it comes to the availability of a suitable workforce, either in the wind or module manufacturing sectors. Thus, there is a major challenge in ensuring that Odisha's local workforce is employed in manufacturing activities and there is no labour migration. It is recommended that the Odisha Skill Development Authority look to upskill local youth and that more ITIs be set up to ensure absorption into the upcoming jobs in the sector.

4. Lack of a sustained deployment trajectory and need for demand security

a. A major challenge to expanding manufacturing capacity, especially in the wind component sector, is the lack of a sustained trajectory for renewable energy deployment in the country (projects commissioned in CY 2022 met only 18-23 per cent of the annual required target 9 ). This leads to the risk of idle manufacturing capacity and low return to investment, which prevents manufacturers from undertaking large-scale production and thus, hurts the manufacturing sector's competitiveness.

Thus, it is recommended that GRIDCO Odisha notifies a trajectory for yearly solar and wind deployment and ensures adequate implementation to build a robust manufacturing ecosystem within the state, in addition to compliance with RPO. This is to be in line with a sustained trajectory that is maintained at the central level to ensure smooth production and demand in the country. This will also provide job security to those working in manufacturing plants and reduce the need for contractual labour, given the permanency of demand.

1. Technology risk

a. Changing technology (both in terms of machinery and equipment) and ensuring adaptation to new technologies is a key risk to manufacturing 10 . Manufacturers are not willing to make large investments in a particular technology if it is anticipated that newer and more efficient technology will arise, which is why the benefits of large-scale production cannot be utilised. Further, upgrading technology requires a large amount of capital and is a risk to current investment.

Mitigation: For wind components, since there is a constant change/upgradation in turbine models and ratings, it becomes important to offer financial incentives in terms of technology upgradation grants, tax incentives, and R&D grants, and incentivise industry-led R&D and mandate R&D spending.

b. The solar PV landscape has seen significant shifts in technologies from multi-Si to mono-Si and PERC (Garg and Jain 2022). There is an anticipated shift from p-type mono-Si wafers to n-type mono-Si wafers (displayed module efficiency above 22 per cent and cell efficiency above 25 per cent (Xiao 2021)). TOPCon is also expected to capture a major share of the module manufacturing market, with a reduced share of Mono PERC technology. Thus, it becomes important for the industry to be prepared for these changes in technology.

2. Import risk and need to consolidate supply chain - Given the dependence on China for major upstream and midstream components (polysilicon, wafer and ingot, cells (Raghavan 2023) and a few important wind components (Chandrasekaran, 2020), there is a large risk to downstream industries in India in terms of supply chain dependencies and the monopoly of China. India relies heavily on imports of wind components from Turkey and China for materials like castings, etc. which account for ~80 per cent of the total supply, and only 20 per cent of gearbox equipment are manufactured locally (Hazarika 2023).

3. Trade risk—Given that India may target the export market for RE equipment, there is a constant geopolitical trade risk dependent on the country's international relations and the policy of self-reliance followed by importing countries.

The wind and solar value chain consists of several segments: 1) mining, raw materials extraction and processing, 2) component manufacturing, 3) deployment, and 4) end-of-life-cycle management. In this note, the manufacturing process of the solar and wind value chain is covered.

For wind components, the scoping is limited to midstream components of blade, tower, nacelle and monitoring and control system whereas for solar, it is limited to the downstream components of modules (battery manufacturing is covered as part of the EV and battery manufacturing note).

Module manufacturing

Jobs estimation:

Total number of jobs that can be created through module manufacturing in Odisha by 2030 is calculated using employment factor per MW and potential market size.

Total FTE jobs through wind deployment = Employment factor per MW x potential market size (MW)

An employment factor of 2.6 per MW was applied as per Kuldeep et al., 2017.

Market sizing (in units):

Odisha has a current pipeline of upcoming projects of 12,500 MW11 .To be more ambitious, a comparison with the leading state is looked into. Gujarat currently has the highest amount of module manufacturing capacity capturing 53 per cent of the industry (Mercom, 2022). It has an upcoming pipeline of projects of 35,650 MW capacity (CII and EY, 2023) tendered post tranche II of the PLI scheme for solar manufacturing (MNRE 2021). This market scenario looks to match Gujarat’s upcoming pipeline of module manufacturing by 2030.

Wind manufacturing

Jobs estimation:

Total number of jobs that can be created through module manufacturing in Odisha by 2030 is calculated using employment factor per MW and potential market size.

Total FTE jobs through wind deployment = Employment factor per MW x potential market size (MW)

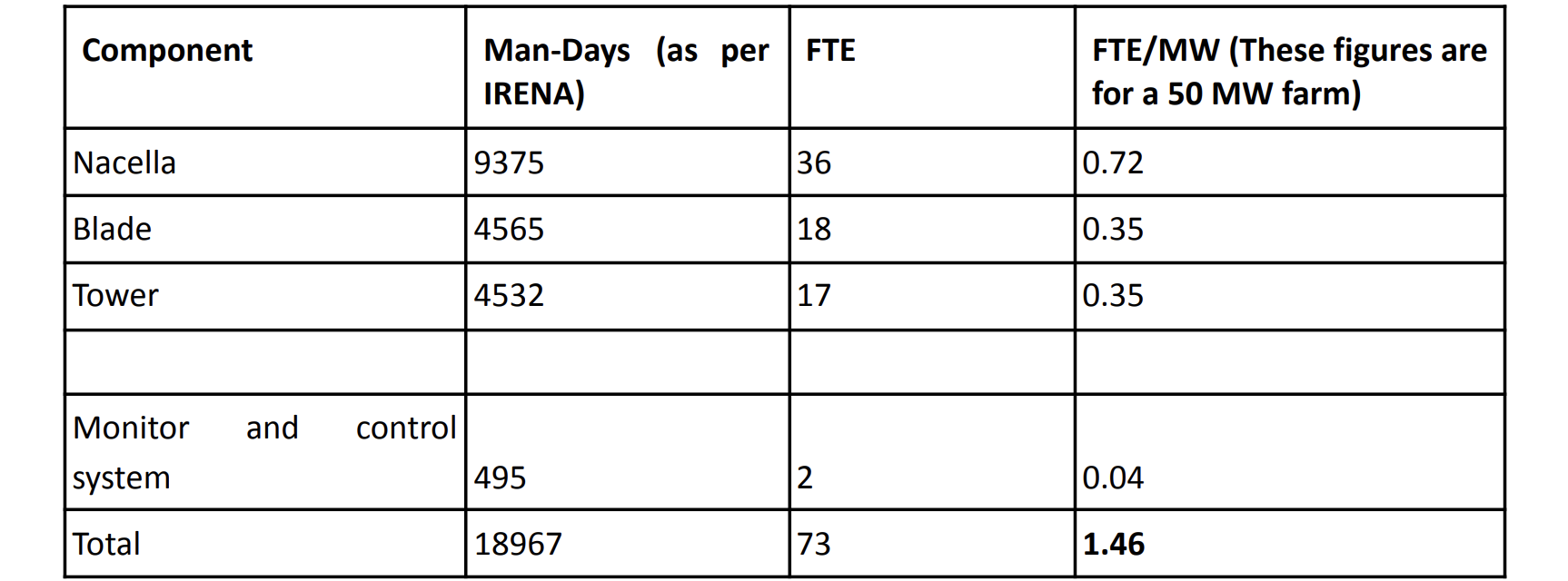

The manpower calculation for wind components by IRENA 2017 was directly adopted to develop an FTE for wind components (nacelle, blade, tower, monitor, and control system). The person-days were converted into full-time equivalent (FTE) by assuming a 260-day working year for a wind manufacturing facility using the following formula:

FTE per MW = (Person days required / Total number of working days in a year) / Total capacity (in MW))

Table 1

Source: IRENA, 2017

Market sizing (in units):

Currently, the wind manufacturing industry in India is facing low demand due to muted growth of the wind deployment sector. In 2022, out of 11.5 GW of installed manufacturing capacity, only 2 GW was utilised (Sidharth 2023). Most of the manufacturing capacity was underutilised due to lower volume in the domestic market and relatively low exports of nacelles from India. However, with a target of 1,041 MW of wind deployment for Odisha by 2030 (as per the target set in the wind deployment chapter), ~150 MW of annual wind deployment trajectory will help create domestic demand for wind components. Further, with increasing national efforts, RPO obligations, the wind industry witnessed a 56 per cent YoY increase in Q1 2024 and 109 per cent QoQ increase (Gupta 2024). Further, the rising opportunities for export to global markets will also help create the required demand for wind components.

For 2030, the goal for Odisha should be to help create a supportive ecosystem for wind component manufacturing in the state. Thus, a target of 500 MW, which is the minimum factory size 12 which can be set up to begin operations, is considered as the target for Odisha. It is important to note that it is the setting up of the required ecosystem that is to be given priority, with sustained deployments to ensure constancy of demand.

Note: The market opportunity here refers to the potential revenue accrued from the sale of total modules and wind components in 2030 only, once full capacity is realised. No proxy for the demand is taken given that the total opportunity is being looked into and it is assumed that the manufacturing plants are working at full capacity (taking into consideration a capacity utilization factor) and the entire manufactured component is sold.

Module manufacturing - The price (USD / W) of 0.18 is taken as the price of Indian modules as per Infolink Consulting. The capacity utilisation factor of 80 per cent was applied as per Rustagi, 2023 and then this was multiplied by the capacity by 2030 to get the market opportunity.

Wind manufacturing - Due to the unavailability of market price estimates for wind components, the methodology to calculate market opportunity is elaborated as follows:

● Wind turbines constitute 64 per cent of the cost breakup of an onshore wind farm as per IRENA 2017 (Similar estimates are taken as the industry standard).

● Thus, the capital cost per MW of an onshore wind farm is taken from the CEA, 2022 released by CEA, and the percentages mentioned above are applied, along with a capacity utilisation factor of 80 per cent in line with module manufacturing to get the cost/MW of wind manufacturing. This is then multiplied by the total capacity in 2030 to get the market opportunity.

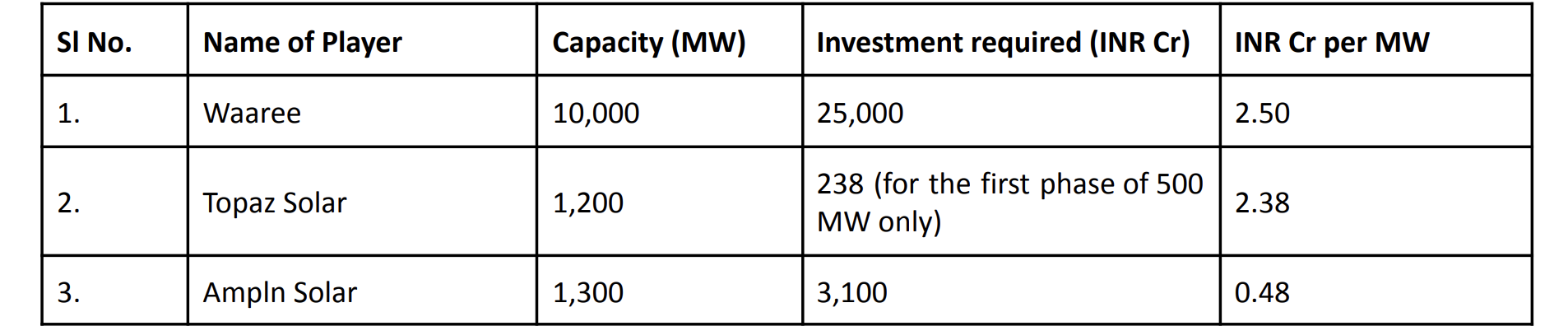

Module manufacturing - To calculate the investment opportunity, the investment required for the three upcoming module manufacturing facilities in Odisha was used. After calculating the investment required per MW for each project, an average investment required was derived Using this average and the estimated capacity target for Odisha by 2030, a total investment opportunity was calculated.

Note that the three capacities are fairly representative given a large plant by Waaree (10 GW), small plants by Topaz (the investment in the first phase of 500 MW installation was taken) and Ampln (1.3 GW). Upcoming module manufacturing facilities in Odisha as per industry reports:

Table 2

Source: The New Indian Express, 2023, Topaz Solar and Gupta, 2023

Wind manufacturing - The manufacturing facility investment cost required for a 600 MW blade manufacturing plant by Vestas (Sharma 2027) was taken to calculate the investment per MW. A major limitation faced was the lack of available and recent information on setting up wind manufacturing facilities in India, due to which the only available estimate was scaled up. Thus, the cost for setting up a blade manufacturing factory was taken to be the cost for setting up nacelle and tower manufacturing facilities, due to which the calculation was tripled. A limitation is that the benefits of cost integration with integrated facilities is not captured here. Further, a key assumption is that the cost of a blade manufacturing facility will be similar to nacelle assembly and tower manufacturing facilities.

Adani Solar AboutUS https://www.adanisolar.com/about-us

Amplus Solar. 2023 About 1 MW solar power plant specifications & price in India

https://amplussolar.com/blog/1mw-solar-power-plant/

By Our Bureau. 2018. “Topaz Solar plans to set up 500-MW module-making unit in Odisha.” BusinessLine.

https://www.thehindubusinessline.com/companies/topaz-solar-plans-to-set-...

CEEW. 2023. Developing Resilient Renewable Energy Supply Chains for Global Clean Energy Transition. New Delhi: Council on Energy, Environment and Water.

Chandrasekaran, K. 2020. “Duty concessions for wind turbine components may continue.” The Economic Times

https://economictimes.indiatimes.com/industry/energy/power/duty-concessi...

Central Electricity Authority (CEA). 2022. Indian Technology Catalogue, Generation and Storage of Electricity. Ministry of Power

https://cea.nic.in/wp-content/uploads/irp/2022/02/First_Indian_Technolog...

CII and EY. 2023. Global champions for advancing renewable energy innovation and manufacturing. In PIB.

https://static.pib.gov.in/WriteReadData/specificdocs/documents/2023/sep/...

David, Andrew. 2021. The Evolution of Global Onshore Wind Turbine Blade Production and Trade. US International Trade Commission

Garg, Shreyas and Rishabh Jain. 2022. Making India a Leader in Solar Manufacturing: Ways to Achieve Technology Leadership and Global Competitiveness. New Delhi: Council on Energy, Environment and Water.

Government of Odisha | Topography

https://odisha.gov.in/odisha-profile/topography#:~:text=It%20is%20bounde...

Gupta, U. 2023. “AmpIn Energy to build 1.3 GW solar cell, module factory in Odisha.” PV Magazine India.

https://www.pv-magazine-india.com/2023/11/24/ampin-energy-to-build-1-3-g...

Gupta, Urvashi, 2024. “India added 1.2 GW wind capacity in Q1 2024, 56% YoY increase”. Mercom India.

https://www.mercomindia.com/india-added-wind-capacity-yoy-increase

Hawkins, S. 2023. “Solar exports from China increase by a third.” Ember.

https://ember-energy.org/latest-insights/china-solar-exports/#supporting...

Hazarika, G. 2023. “Reasons behind the recent downturn in India’s wind sector and causes for hope.” Mercom India

https://www.mercomindia.com/reasons-behind-the-indias-wind-sector-and-ca...

Hutchinson Mark and Zhao Feng. 2023. Global Wind Report 2023. Global Wind Energy Council.

https://www.gwec.net/reports/globalwindreport/2023#:~:text=GWEC%20Market...

Industrial Policy 2020-2025 – Invest Karnataka. (n.d.).

https://investkarnataka.co.in/wp-content/uploads/2025/02/Booklet-final-.pdf

Industries Department, Odisha 2022-23 “Activities Report of Industries Department 2022-2023”.

https://industries.odisha.gov.in/sites/default/files/2023-09/ACTIVITY%20...

InfoLink Consulting. Spot price.

https://www.infolink-group.com/spot-price/

Invest Odisha “Aluminium Park Angul, Odisha India”

https://investodisha.gov.in/Application/uploadDocuments/Content/Aluminiu...

Invest Odisha, I. (n.d.-b). Investment opportunities in Odisha, India | Invest Odisha. Invest Odisha.

https://investodisha.gov.in/dipa/

IRENA, 2017. Renewable energy benefits: Leveraging local capacity for onshore wind. International Renewable Energy Agency, Abu Dhabi.

ITRPV. 2021. International Technology Roadmap for Photovoltaic: 2020 Results. Frankfurt: Verband Deutscher Maschinen- und Anlagenbau (VDMA).

Jain Sidharth, Srivastava Swarnim, Sodani Disha, Zhao Feng, Shardul Martand, Jayasurya Francis, Lathigara Anjali, and Lee Joyce. 2023.. From local wind power to global exhort hub: India Wind Energy Market Outlook 2023-2027. Global Wind Energy Council.

https://www.gwec.net/gwec-news/india-wind-energy-market-outlook-2023-202...

Jain, Rishabh, Arjun Dutt and Kanika Chawla, 2020. Scaling Up Solar Manufacturing to Enhance India’s Energy Security. New Delhi: Council on Energy, Environment and Water

Jaishankar, D. 2023. Transforming eastern India’s electricity sector to meet renewable energy goals — ORF America. ORF America.

https://orfamerica.org/newresearch/transform-eastern-india-electricity-s...

JMK Research. 2023. Q4 2022 India RE update (Oct-Dec 2022). JMK Research & Analytics.

https://jmkresearch.com/renewable-sector-published-reports/q4-2022-india...

Jyoti 2021. Viability Assessment of New Domestic Solar Module Manufacturing Units Can India Compete Against China in PV Production? IEEFA

https://ieefa.org/wp-content/uploads/2021/01/Viability-Assessment_New-Do...

Kala, B. R. R. 2023. “India likely to become second largest solar module manufacturer by 2025: Wood Mackenzie report.” Business Line.

https://www.thehindubusinessline.com/economy/india-likely-to-become-seco...

Koundal, A., and Singh, S. 2023. “Whopping 364 per cent jump in India’s solar exports within a year.“ ETEnergyWorld

https://energy.economictimes.indiatimes.com/news/renewable/tables-turnin...

Kuldeep, Neeraj, Kanika Chawla, Arunabha Ghosh, Anjali Jaiswal, Nehmat Kaur, Sameer Kwatra, Karan Chouksey. 2017 Greening India's Workforce: Gearing Up for Expansion of Solar and Wind Power in India. New Delhi: Council on Energy, Environment and Water and Natural Resources Defense Council

Lee Joyce and Zhao Feng. 2022. Global Wind Report 2022. Global Wind Energy Council.

https://www.gwec.net/gwec-news/global-wind-report-2022

Mercom 2022. State of solar PV manufacturing in India. Mercom India.

https://www.mercomindia.com/product/state-solar-manufacturing-india

MINISTRY OF NEW AND RENEWABLE ENERGY. Union Budget 2022-23.

https://www.indiabudget.gov.in/doc/eb/sbe71.pdf

Ministry of Power. 2023.

https://pib.gov.in/PressReleaseIframePage.aspx?PRID=1911380

MNRE: YEAR END REVIEW-2020. (n.d.).

https://www.pib.gov.in/PressReleseDetailm.aspx?PRID=168504®=3&lang=1

MNRE 2021 APPROVED LIST OF MODELS AND MANUFACTURERS (ALMM) | Ministry of New and Renewable Energy | India.

https://mnre.gov.in/en/approved-list-of-models-and-manufacturers-almm/

Odisha Renewable Energy Policy, 2022. Energy Department, Government of Odisha.

https://energy.odisha.gov.in/sites/default/files/2022-12/3354-Energy%20d...

OdishaPlus. 2020. Odisha Government to develop downstream cluster in Kalinga Nagar to boost steel production. Odisha Plus

https://www.odisha.plus/2020/01/odisha-government-to-develop-downstream-...

Odisha Port Policy 2022

https://ct.odisha.gov.in/sites/default/files/2022-12/Port%20Policy%20202...

PTI. 2023a. “Extend production linked incentive scheme for wind energy component makers, says expert.” ET Energyworld

https://energy.economictimes.indiatimes.com/news/renewable/extend-produc...

PTI 2023b. “Odisha gets investment proposals worth Rs 4,940 crore in wind energy sector.” Money Control

https://www.moneycontrol.com/news/business/odisha-gets-investment-propos...

PTI. 2023c. "Adani plans to build 10 GW integrated solar manufacturing capacity by 2027.” Business Standard

https://www.business-standard.com/companies/news/adani-plans-to-build-10...

Press Information Bureau (PIB), Government of India, ministry of New and Renewable Energy. 2021. Measures undertaken to promote local manufacturing of Solar Panels. (n.d.).

https://pib.gov.in/Pressreleaseshare.aspx?PRID=1779724

PV Insights. PV spot price. https://pvinsights.com/

Raghavan, T. S. 2023. “Curious case of India’s solar cell industry: Exports up 12x, but domestic power producers still import.” The Print.

https://theprint.in/india/curious-case-of-indias-solar-cell-industry-exp...

Ranjan, R. 2023. “Average cost of Large-Scale solar projects down for the first time in 11 quarters.” Mercom India.

https://www.mercomindia.com/average-cost-large-scale-solar-down-first-ti...

Rustagi, V. 2023. A peek into the future of solar manufacturing in India. BRIDGE TO INDIA.

https://bridgetoindia.com/a-peek-into-the-future-of-solar-manufacturing-...

Shardul Martand and Lee Joyce 2022. ACCELERATING ONSHORE WIND CAPACITY ADDITION IN INDIA TO ACHIEVE THE 2030 TARGET. Global Wind Energy Council

https://www.gwec.net/gwec-news/accelerating-onshore-wind-capacity-additi...

Shardul Martand and Arumugasamy Gurunathan. 2022. "India must leverage wind manufacturing and exports to become a multi-trillion-dollar economy.” ET Energyworld

https://energy.economictimes.indiatimes.com/news/renewable/india-must-le...

Sharma, S. N. 2017. “How Danish company Vestas built a Rs 500 crore blade factory near Ahmedabad in a record 15 months”. The Economic Times.

https://economictimes.indiatimes.com/industry/energy/power/how-vestas-bu...

The New Indian Express. 2023. “HLCA nod for Rs 25,000 crore solar equipment factory at Odisha's Dhenkanal district.” The New Indian Express.

https://www.newindianexpress.com/states/odisha/2023/Apr/02/hlca-nod-for-...

Topaz Solar https://www.topazsolar.net/indiaplant.html#:~:text=Topaz%20Solar%20is%20...(500MW%20and%20700MW)

Xiao, Carrie. 2021. “Next Generation Solar: How Topcon, Heterojunction And Other N-Type Technologies Are Striving For Market Share.” PV Tech.

https://www.pv-tech.org/next-generation-solar-how-topcon-heterojunction-...

Energy transition

Battery Energy Storage Systems

Battery Energy Storage Systems  Public Charging Stations for Electric Vehicles

Public Charging Stations for Electric Vehicles Electric Vehicle and Battery Manufacturing

Electric Vehicle and Battery Manufacturing  Biomass to Power

Biomass to Power Green Hydrogen and Electrolyser Manufacturing

Green Hydrogen and Electrolyser Manufacturing Rooftop Solar

Rooftop Solar Floating Solar Photovoltaic (FSPV)

Floating Solar Photovoltaic (FSPV) Solar Mini/Micro Grid

Solar Mini/Micro Grid Pumped Storage Hydropower (PSH)

Pumped Storage Hydropower (PSH) Renewable Energy Equipment Manufacturing

Renewable Energy Equipment Manufacturing Small Hydropower (SHP)

Small Hydropower (SHP) Utility-Scale Solar Deployment

Utility-Scale Solar Deployment Wind Deployment

Wind Deployment Decentralised Renewable Energy (DRE) Technologies for Livelihoods

Decentralised Renewable Energy (DRE) Technologies for Livelihoods