Council on Energy, Environment and Water Integrated | International | Independent

India currently has 11 GW of rooftop solar (RTS) installed, which is around 8 per cent of the total renewable energy installed (MNRE 2023). The deployments are largely driven by commercial and industrial (C&I) consumers who account for 70-80 per cent of the country’s rooftop installation. C&I consumers consume around 49 per cent of electricity produced, but renewable energy (including rooftop solar) constitutes only 3.5 per cent of C&I procurement (JMK Research). At the same time, Indian households consume a fourth of the electricity sold annually, and the consumption of this segment is projected to double by 2030 but their share in RTS installation remains minuscule (Zachariah et al. 2023). According to a CEEW study (Zachariah et al. 2023), the technical potential of rooftop solar in the residential sector in Odisha taking into account rooftop area and energy need and consumption is 4 GW. With the PM Surya Ghar Muft Bijlee Yojana, the increased capital subsidy would further boost deployment 1 . Rooftop solar thus has a huge potential across C&I and residential consumers whilst offering the co-benefit of employment generation and decarbonisation of the power sector.

Jobs overview

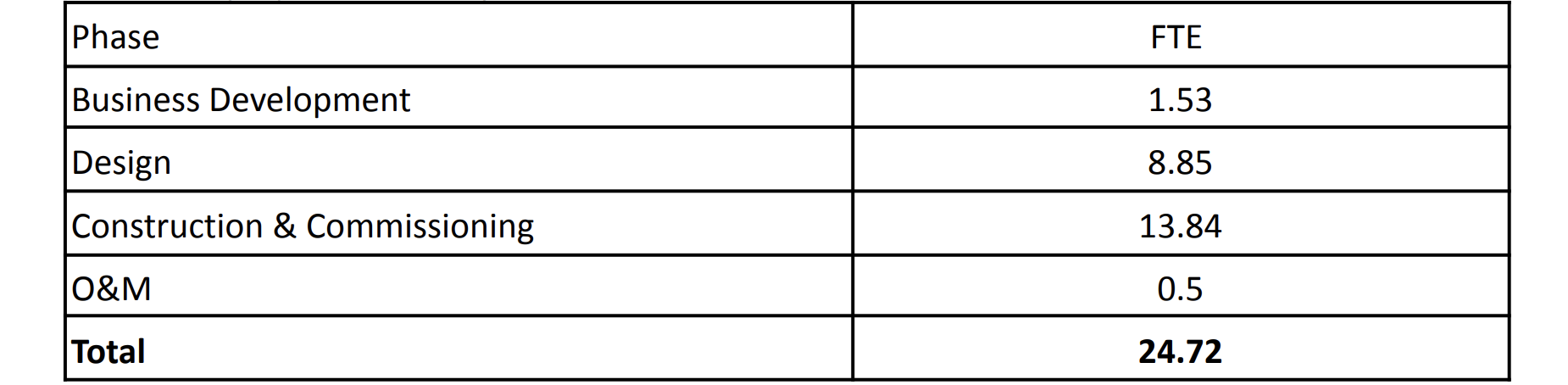

● Solar rooftop deployment is labour intensive with activities including business development, design, construction, and commissioning, and employs around 24 full-time equivalent (FTE) employees per MW deployed. A total of 26,000 FTE jobs would be generated to develop, design, construct, operate and maintain 1.2 GW RTS by 2030.

Market Opportunity

● The market opportunity in terms of electricity being generated for rooftop would be INR 400 crore (USD 50 million) in 2030.

Investment Opportunity

● The investment required to reach 1 GW of RTS by 2030 would be INR 5,000 crore (USD 600 million).

1. Benefits to the DISCOMs: Based on the study on valuing grid-connected rooftop solar (Kuldeep et al. 2019), DISCOMs benefit in the following ways from RTS:

a. Daytime peak load is better managed if RTS systems are installed. DISCOMs source from the open market at higher prices to meet peak load. With the penetration of RTS, this is mitigated.

b. DISCOMs procure power through long-term power purchase agreements (PPA). Since consumers have decentralised systems of generation, there is lower demand, and the need for new PPAs would decrease thus the benefit of avoided generation cost.

c. With the deployment of rooftop systems, the actual cost paid by DISCOMs to generators will reduce. While there is a fixed amount to be paid to generators, the variable amount on the actual electricity procured may reduce, resulting in avoided power purchase costs.

d. There would also be avoided transmission charges, as DISCOMs have to pay for the share of the transmission network used.

e. Since grid interactive rooftop solar generation contributes to RPO targets to be met by DISCOMs, facilitating and encouraging rooftop solar can lead to DISCOMs reducing the need to purchase renewable energy certificates (REC).

f. Since RTS is decentralised and decongests the grid, the deployment of such systems reduces the maintenance costs of the grid for decongestion and reduces the investments needed in additional components to decongest the grid.

g. Due to the above reasons and the revenues from sale of electricity through RTS, working capital needs for the DISCOM are reduced, thus resulting in a lower debt servicing obligation.

2. Reduction of state power subsidies: Of the 36 states and union territories, 27 provide power subsidies to consumers (Goswami 2022). These subsidies are provided via DISCOMs. With the move to decentralised RTS, where generation is at point of consumption, the state government will no longer need to provide electricity subsidies to consumers, thus reducing the quantum of money spent on the same.

3. Other benefits:

a. Overcoming land constraints – Utility-scale solar and ground-mounted solar are constrained by the availability of land and face challenges such as land acquisition and land procurement leading to both time and cost overruns. By leveraging existing roof space, consumers, especially in cities and urban areas, who also have high energy consumption can generate and use renewable energy without dependence on large scale solar and also reduce their electricity bills.

b. Conventionally, diesel generators are used as the back-up option in case of power outages. If these are replaced with rooftop solar plus storage, households and industries would enjoy uninterrupted electricity and reduce the impact of outages. An added advantage is that DISCOMs can utilise the decentralised rooftop and storage facilities as required (Rutter & Pulipaka 2023).

CEEW Partnered with BSES Yamuna Power Limited (BYPL) and PV Diagnostics to evaluate performance of RTS systems of a sample of 61 sites in Delhi in the BYPL area. Purposive sampling taking into account location, age of plant, consumer category, MNRE and non-MNRE projects, CAPEX vs RESCO, system size and plant performance was done. Desk research and site visits identified hotspots 3 and visible trails and cracks as key reasons for underperformance. Operations and maintenance (O&M)-specific factors include shadow of objects falling on the panel restricting sunlight, deposition of dust and bird droppings, cable damage due to maintenance issues, uneven orientation of the panels due to poor installation, roof limitations and non-functioning inverter causing the system to shut down. It was also found that the quality of air and water impacts the performance of the RTS system. Thus, proper maintenance and cleaning is key to ensuring performance is not affected. Onsite cleaning improves performance by at least 10 per cent and results in a reduction of dependence on the grid, leading to prosumer savings (Tyagi et al., 2023).

1. Role of departments:

a. OREDA and Department of Energy:

i. Nodal agency: OREDA is the nodal for distributed RE in Odisha and currently facilitates demand aggregation and deployment of rooftop solar on government buildings.

ii. Target new segments: OREDA may go beyond government buildings, and work towards targeting large C&I consumers as well as residential societies to encourage the uptake of rooftop solar through demand aggregation campaigns. Similarly, OREDA may work with the Rural Development Department to build awareness and facilitate uptake in rural areas.

iii. Innovative business models: OREDA may experiment with other business models in the state such as solar partner, peer-to-peer trading and DISCOM owned community solar especially for low energy consumers who may not have any incentive to move towards RTS due to highly subsidised electricity.

iv. Targets: OREDA and the Department of energy may jointly set targets, either yearly or for every five years in accordance with the state renewable energy policy, to ensure progress is measured against certain targets and to set the ambition, thereby signally a supportive environment to industry and vendors.

v. Financial incentives: OREDA may also look to develop financial incentives or subsidies (over and above central subsidies) to kickstart the rooftop solar revolution and phase down the subsidy after five years.

b. DISCOMs: DISCOMs facilitate the connection to the grid, meter the export/import of power, and bill the consumers. DISCOMs should provide timely net metering services to consumers and ensure mechanisms of consumer grievance redressal. CEEW research has shown that DISCOMs are trusted by consumers, and provide familiarity in campaigns to increase uptake of rooftop solar. DISCOMs play an important role in creating awareness under RTS phase II and can ensure RTS deployment guidelines are well communicated to consumers as consumers are more likely to trust DISCOMS (Gupta et al. 2022). This will ensure information is openly shared and will push vendors to ensure customer satisfaction.

c. Odisha Electricity Regulatory Commission (OERC): The role of OERC is critical to issue enabling regulations to facilitate the innovative business model, feed-in tariff rates, metering regulations.

2. Role of the private sector:

a. Developers: Developers may take responsibility to ensure vendors are provided training and SOPs. While most developers already provide certification, they may go a step further and provide annual maintenance checks to the prosumers.

b. Channel partners and entrepreneurs: Channel partners are key players who aid in raising awareness, educating prosumers, ensuring maintenance onsite. Since vendors/channel partners are most connected to the consumer, they may go a step ahead and link up financial institutions and consumers to ensure the upfront cost does not become a deterrent in the uptake of solar.

3. Role of civil society organisations (CSOs): India still lags behind in solar rooftop as compared to other countries. CSOs can play a role in organising awareness campaigns along with DISCOMs to persuade residential consumers to adopt or at least consider solar rooftop. CSOs can work to understand demand potential, impact on DISCOMs, identify innovative business models specific to Odisha, and garner and assess consumer interest.

1. Challenges in the deployment of RTS on ground: Based on interviews with vendors 4 in Bhubaneswar, the key challenges faced include delayed installation of net metering, lack of grievance redressal mechanism by DISCOMs, lack of mechanism to check the status of the application, delay in disbursement of subsidy amount to the developers. Due to the delay in subsidy, many vendors have refused to take up installation of residential rooftop systems. While non-compliance is a risk as highlighted above, it is also a challenge to scale RTS.

OREDA may convene with DISCOMs to ensure they fulfil their responsibility in boosting rooftop solar in Odisha. DISCOMs may constitute a cell specifically for RTS, including assistance in tracking of application, grievance redressal, etc. Routing the subsidy through the national portal, where the subsidy comes directly to the consumers, is critical to ensure reduced complexities between consumers, channel partners and developers.

2. High upfront cost: Learnings from a pilot campaign in Delhi revealed that for the residential segment, even after the subsidies provided at the national level, the upfront costs of capital investment were too high (Gupta et al. 2022).

To overcome this, residential consumers would need access to affordable financial solutions such as dedicated solar loans, reduced interest rates on loans for solar installation, lines of credit for solar, easily usable non-bank financial apps, etc.

3. Lack of awareness: In Odisha, among residential consumers, only 68 per cent of consumers in urban areas and 48 per cent of consumers in rural areas knew about solar home systems (Zachariah et al. 2023). Further, a large number of households have low energy consumption per sq. ft. (Zachariah et al. 2023). Nudging low energy consumers to RTS would require targeted policy focus.

Based on past CEEW research, it was found that DISCOMs are trusted by the community, and awareness campaigns jointly by CSOs and DISCOMs can add credibility to awareness campaigns through various methods as simple as SMS, lending their name and support to CSOs, etc. (Gupta 2022). Campaigns can ensure influences, and that consumers have beginning to end support, with cities such as Bhubaneswar, Cuttack leading campaigns and creating a central repository of resources/guidelines for all campaigners (Gupta 2022). A one-stop platform with information for consumers in the lowest energy consumption bracket to C&I consumers with easy-to-access reliable and compelling information about various business models, available subsidies, and credible information would be beneficial across all categories.

4. Lack of incentive to move: Currently, there is no incentive for consumers to shift to rooftop solar as electricity is subsidised.

The state may introduce attractive feed-in tariffs for RTS to incentivise consumers to generate electricity and contribute to decarbonising the power sector.

5. Maintenance issues: As highlighted in the case study, maintenance is critical for the proper functioning of a RTS system.

Knowledge transfer to consumers, creating standard SOPs, having ratings for vendors/channel partners done by the developer, ensuring annual maintenance checks are critical to mitigate the challenge of non-performance due to issues such as bird dropping, soiling and dust, etc (Tyagi et al. 2023).

1. Rise in solar waste: Solar waste after the lifetime of panels is bound to increase. This coupled with panels damaged due to maintenance or other issues would add to the pile of solar and other related waste. According to the IEA, solar waste could amount to 78 million tonnes worldwide by 2050 (Atasu et al. 2021). If not managed properly, there is a risk of panels ending up in landfills.

Mitigation: Producers of solar cells and modules should establish waste collection and storage centres to fulfil their obligations under the E-Waste Management Rules 2022 (MNRE and CEEW 2024).

2. Non-compliance of DISCOMs: For DISCOMs, the shift to RTS by their customers reduces the revenue from those customers. Many DISCOMs may not assess the benefits of RTS, such as lower T&D losses, grid decongestion, etc. which would be cost savers for them.

Mitigation: It is integral to have DISCOMs on board to ensure facilitation of RTS is done in a smooth manner. DISCOM-owned community solar is one model that can help meet renewable energy targets, where DISCOMs could provide cheap electricity to highly subsidised consumers, avoid T&D losses, and avoid power purchase costs (Tyagi & Kuldeep 2023).

The rooftop solar value chain covered includes:

● Deployment phase: This stage involves all activities encompassing the direct application of the designated product towards its desired end-use activity. For example, in rooftop solar deployment, this includes site selection, project design, procurement of components such as solar panels, construction, commissioning and O&M.

Jobs estimation:

Employment coefficients across each phase have been taken from Kuldeep et al. 2017

Table 1 Employment across phases

Source: Kuldeep et al. 2017

A linear trajectory of deployment is assumed and given the short-term nature of jobs in business development, design and pre-construction and construction and commissioning, it is assumed that the workforce employed in one year will be re-absorbed in the deployment of rooftop solar in the next year.

Market sizing (in units):

● As already elaborated above, the ‘market’ looked at is deployment, and other aspects like component manufacturing, end-of-life management, etc., are not considered in this Note.

● The methodology to develop market scenarios are as follows:

○ The scenarios have been formulated ambitiously to create a vision for the state and unlock the value of high deployment via generating evidence on employment, market, and investment opportunities. The rationale for the development of the market scenario for rooftop solar deployment is as follows:

■ PM Surya Ghar Yogana envisions 30 GW to be the 2026 deployment of residential Rooftop Solar (MNREa 2024).

■ Cumulative installed capacity of solar as on May 2024 is 84,277 MW (MNREb 2024). Target for 2030 is 292566 MW (MNRE 2023). In order to achieve this target, a yearly CAGR of 19.46 per cent would need to be achieved in terms of installations.

■ Assuming that the 2030 target is achieved only from utility-scale solar and rooftop solar, the proportion of the two is developed as follows:

● Based on the CAGR of 19.46 per cent utility-scale solar, projections were made till 2030.

● Thus, in 2026, total solar is expected to reach 143 GW in India out of which RTS is 30 GW.

● Thus, using this ratio, the 2030 RTS India target is estimated to be ~60 GW (Total 2030 solar target is ~292 GW).

● In order to arrive at Odisha’s target, the MNRE state rooftop solar allocation 2022 was taken and Odisha’s share was 1.9 per cent. This was then applied to the India 2030 estimated number to get a market potential of 1,161 MW.

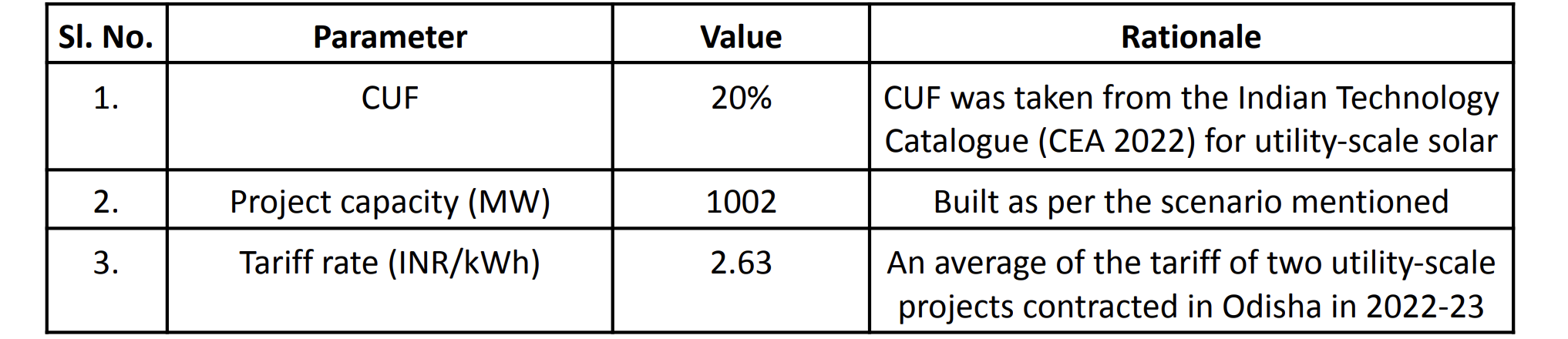

To find yearly revenue potential from sale of power, the following formula was used to calculate injected energy (MWh) from project capacity (MW):

Capacity Utilisation Factor (CUF) = [Injected energy (MWh)/(Project capacity (MW) * 8766)]* 100

Revenue potential = Tariff rate (USD/kWh) * Injected energy (kWh)

Further, a degradation rate of 0.7 per cent and a performance ratio of 80 per cent (taken as per the Indian Technology Catalogue) have also been applied to account for generation losses.

Table 2 The values taken and rationale for each parameter to calculate market opportunity

Source: Author’s analysis

As per the Indian Technology Catalogue (CEA, 2022), the capital cost per MW of rooftop solar systems is INR 39 Mn as on 2020.

This INR Mn/MW figure was then multiplied with the total additional capacity to be installed to get the total investment required.

AE Admin. 2023. “What Are Hot Spots and How They Affect Solar Panels.” AESOLAR, February 9, 2023.

https://ae-solar.com/what-are-hot-spots-and-how-they-affect-solar-panels

Central Electricity Authority (CEA). 2022. Indian Technology Catalogue, Generation and Storage of Electricity. Ministry of Power

https://cea.nic.in/wp-content/uploads/irp/2022/02/First_Indian_Technolog...

Rutter, Alexander Hogeveen, Pulipaka, Subrahmanyam and ET EnergyWorld. 2023. “OPINION: Make Solar Rooftop Great Again.” ET Energy World, December 29, 2023.

https://energy.economictimes.indiatimes.com/news/renewable/opinion-make-...

Goswami, Shweta. 2022. “27 states providing power subsidy, MP, Rajasthan and Karnataka top list”. Hindustan Times, August 8, 2022.

https://www.hindustantimes.com/india-news/27-states-providing-power-subs...

Gupta, Akash Som, Bhawna Tyagi, Neeraj Kuldeep and Selna Saji. 2022. Unlocking Demand for Residential Rooftop Solar in India: Learnings from Solarise Delhi Campaigns. New Delhi: Council on Energy, Environment and Water

Atasau, Atalay, Duran, Serasu, Wassenhove, Luk N. Van. 2021. “The Dark Side of Solar Power,” Harvard Business Review, Jun18, 2021.

https://hbr.org/2021/06/the-dark-side-of-solar-power

IEA and CEEW. 2019. Women working in the rooftop solar sector. Paris: International Energy Agency.

JMK Research & Analytics. “C&I Rooftop Solar Market Assessment India.” JMK Research & Analytics. Accessed January 15, 2024

https://jmkresearch.com/renewable-sector-published-reports/powering-up-s...

Kuldeep, Neeraj, Kumaresh Ramesh, Akanksha Tyagi, and Selna Saji. 2019. Valuing grid-connected rooftop solar: A framework to assess cost and benefits of rooftop solar to Discoms. New Delhi: Council on Energy, Environment and Water.

Kuldeep, Neeraj, Kanika Chawla, Arunabha Ghosh, Anjali Jaiswal, Nehmat Kaur, Sameer Kwatra, Karan Chouksey. 2017 Greening India's Workforce: Gearing Up for Expansion of Solar and Wind Power in India. New Delhi: Council on Energy, Environment and Water and Natural Resources Defense Council Ministry of Power, Central Electricity Authority. 2022. ”Report on twentieth Electric Power Survey of India (Volume 1),”

https://cea.nic.in/wp-content/uploads/ps___lf/2022/11/20th_EPS____Report...

MNRE. 2023. “Government is committed to provide Energy and Food Security: Union MoS Shri Bhagwanth Khuba” Press Information Bureau

https://pib.gov.in/PressReleaseIframePage.aspx?PRID=1944075#:~:text=By%2...

MNRE and CEEW. 2024. Enabling a Circular Economy in India’s Solar Industry: Assessing the Solar Waste Quantum. New Delhi: Council on Energy, Environment and Water

Ministry of New and Renewable Energy (MNREa), 2024. “PM Surya Ghar: Muft Bijli Yojana - Redefining Solar Power and Energy Access” Press Information Bureau

https://www.pib.gov.in/PressNoteDetails.aspx?NoteId=152016&ModuleId=3&re...

MNRE. “FAQ: Grid Connected Solar Rooftop System,” n.d.

https://solarrooftop.gov.in/pdf/faq%20new.pdf

Ministry of New and Renewable Energy (MNREa), 2024. “PM Surya Ghar: Muft Bijli Yojana - Redefining Solar Power and Energy Access” Press Information Bureau

https://www.pib.gov.in/PressNoteDetails.aspx?NoteId=152016&ModuleId=3&re...

MNREb. 2024. Physical Achievements. Ministry of New and Renewable Energy.

https://mnre.gov.in/en/year-wise-achievement/

Singh, Mandvi, Chaudhuri Ritwik Ray, Mukherjee Arpo. 2023. Renewable Energy Potential in Odisha. IFOREST - International Forum for Environment, Sustainability & Technology.

https://iforest.global/people/team/ritwik-ray-chaudhuri/

Tyagi, Bhawna, Neeraj Kuldeep. 2023 . Community Solar for Advancing Power Sector Reforms and the Net-Zero. New Delhi: Council on Energy, Environment and Water.

https://www.ceew.in/sites/default/files/scaling-community-solar-for-net-...

Tyagi, Bhawna, Sachin Zachariah, Neeraj Kuldeep, Deepak Singh Chouhan, Shailendra Singh Chouhan, Aayush Mahajan, and Atul Kumar Jain. 2023. kWh from kW: Achieving Optimum Energy Generation from Rooftop Solar Systems -Insights from field visits in Delhi. New Delhi: Council on Energy, Environment and Water.

Tyagi, Akanksha, Akanksha Golchha, Deepak Rai, Arvind Poswal, Charu Lata, Sameer Kwatra, and Praveen Saxena. 2023. India's Expanding Clean Energy Workforce 2022 Update . Council on Energy, Environment and Water, Natural Resources Defense Council, and Skill Council for Green Jobs.

https://www.ceew.in/publications/indias-expanding-clean-energy-workforce...

World Bank. n.d. "Leveraging Climate Opportunities - Sembcorp Tengeh Floating Solar Farm." World Bank. Accessed November 6, 2023.

https://ppp.worldbank.org/public-private-partnership/leveraging-climate-...

Zachariah, Sachin, Bhawna Tyagi, and Neeraj Kuldeep. 2023. Mapping India’s residential rooftop solar potential A bottom up assessment using primary data. New Delhi: Council on Energy, Environment and Water.

https://www.ceew.in/publications/residential-rooftop-solar-market-potent...

Energy transition

Battery Energy Storage Systems

Battery Energy Storage Systems  Public Charging Stations for Electric Vehicles

Public Charging Stations for Electric Vehicles Electric Vehicle and Battery Manufacturing

Electric Vehicle and Battery Manufacturing  Biomass to Power

Biomass to Power Green Hydrogen and Electrolyser Manufacturing

Green Hydrogen and Electrolyser Manufacturing Rooftop Solar

Rooftop Solar Floating Solar Photovoltaic (FSPV)

Floating Solar Photovoltaic (FSPV) Solar Mini/Micro Grid

Solar Mini/Micro Grid Pumped Storage Hydropower (PSH)

Pumped Storage Hydropower (PSH) Renewable Energy Equipment Manufacturing

Renewable Energy Equipment Manufacturing Small Hydropower (SHP)

Small Hydropower (SHP) Utility-Scale Solar Deployment

Utility-Scale Solar Deployment Wind Deployment

Wind Deployment Decentralised Renewable Energy (DRE) Technologies for Livelihoods

Decentralised Renewable Energy (DRE) Technologies for Livelihoods