Council on Energy, Environment and Water Integrated | International | Independent

Lithium-ion batteries (LIBs) are promising battery technologies widely used in consumer electronics, electric vehicles (EV) and stationary storage applications. LIB recycling is the recycling of batteries that have reached their end of life, to recover intrinsic materials, preferably to bring back into the manufacturing supply chain. Recycling these batteries is a multistage process including steps such as collection, sorting, dismantling, physical separation and refining to recover intrinsic materials. Some of these materials are classified as critical or strategic for the Indian manufacturing industry, and their recovery can help alleviate supply chain risks and reduce import dependency. We estimate that Odisha could generate about 6.6 kilotonnes of cumulative LIB waste by 2030, driven primarily by the uptake of electric vehicles and stationary storage applications such as telecom towers, and consumer electronics. To give more context, as per our analysis, approximately 100 tonnes of lithium can be recovered from this LIB waste. A single car lithium-ion battery pack (of an NMC532) could contain around 8 kg of lithium (Castelvecchi 2021); therefore, 100 tonnes of lithium from this waste can theoretically power 12,500 car battery backs.

Jobs overview

● A total of 200 cumulative direct FTE jobs can be generated from LIB recycling of 7 kilo tonnes of cumulative LIB waste in Odisha between 2024 to 2030 in an ambitious scenario. This scenario assumes a high penetration of EVs across the vehicle segments; specifically, the share of EVs in new sales will reach 80 per cent for 2-wheelers and 3-wheelers, and 50 per cent for 4-wheelers by 2030. Furthermore, it will reach 40 per cent for buses by 2030. It also assumes a complete recycling (100 per cent recycling rate) of all types of LIB waste by 2030. This scenario covers waste generated within Odisha during the evaluation period.

Market opportunity

● 10 million USD is the revenue potential from recycling 3 kilo tonnes of LIB waste in Odisha in 2030 under the ambitious scenario.

Investment opportunity

● 14 million USD is the investment potential (or capital expenditure 6 ) to set up LIB waste recycling capacities of approximately 3 kilo tonnes per annum in Odisha under the ambitious scenario.

● Domestic supplier of critical materials: The government of India has set ambitious deployment targets for EV and RE technologies, which will increase the demand for LIBs. Consequently, the LIB waste quantum will increase significantly in India from current levels. By creating a conducive environment, Odisha can potentially be a hub for LIB recycling in India and a supplier of key materials. The supply of these key raw materials to domestic manufacturing industries will reduce import dependence and build local mineral supply chains (Warrior, Tyagi and Jain 2023). This will allow the building of a regional battery ecosystem with the growing LIB component manufacturing industry setting up units in the State (Mercom 2023) wherein recycled raw materials can be supplied.

● Reduced migration of semi-skilled workforce: The functions of battery waste handling, testing, and repair can be performed by ITI (Industrial Training Institute) graduates upskilled in the battery sector. Scaling LIB recycling will create employment opportunities for such a semi-skilled workforce within the state in the long run and reduce out-of-state migration.

● Enhanced environmental safety and reduced contamination: Battery components such as heavy metals like nickel and cobalt can leak from the casing of LIB if left untreated and contaminate soil and groundwater. Further, discarded batteries with residual charge are a safety threat and can lead to fires. Responsible management of battery waste will help overcome these critical issues. Moreover, circularity in the supply chain of critical minerals will reduce the demand for mining them and save the corresponding carbon footprint (Kumar, Mulukutla and Pai 2023).

Lohum Cleantech Private Limited is India’s first integrated used LIB treatment facility, performing repurposing, recycling and refining. Operational since 2018, they have 300 MWh refurbishing and 10,000 tonnes per annum recycling facility. The used batteries from electric vehicles are repurposed and reused in stationary storage applications or recycled to recover raw materials. The facility is capable of recovering all major minerals, including lithium, cobalt, nickel and manganese, which can be used in the manufacturing of new battery cells and can be recycled endlessly (Lohum n.d.).

1. Role of departments

● Odisha State Pollution Control Board (OSPCB) to ensure stricter enforcement of Battery Waste Management Rules, 2022 (BWM Rules). It should work closely with the Forest, Environment and Climate Change Department of Odisha to specify guidelines for the safe transportation of waste LIBs till the time the Central Pollution Control Board (CPCB) issues them at a national level. The OSPCB to tackle the potential issue of paper trail recyclers (not undertaking actual operations) in the state as exists for e-waste dismantlers 8 by undertaking audits/checks on registered entities for any malpractices such as incorrect reporting and material balance. In addition, the existing EPR (extended producer responsibility) Portal for Battery Waste Management may be leveraged, and producers may be required to add the quantity of the battery waste generated within the state. OSPCB may recommend to the CPCB to amend the portal in this respect. This data will help build capacities and infrastructure to manage the state’s domestic waste and plan to expand its capacity for the LIB waste generated by the neighbouring states.

● The Industries Department, in consultation with the Forest, Environment and Climate Change Department and OSPCB, as per the Odisha EV Policy 2021, to notify a comprehensive policy to encourage recyclers. The policy could focus on creating recycling clusters to bring economies of scale for battery recycling, introduce various fiscal and non-fiscal incentives, promote the uptake of refurbished products, and create markets for reusing recovered materials.

● Local bodies to tie up with authorised producers and recyclers and hand over the collected battery waste separately or ensure its channelisation to these authorised entities. Being a relatively new stream, it should facilitate awareness drives and programmes about it. Local bodies should have conditions in their agreements with e-waste recyclers to channelise battery waste, which is a part of e-waste, to authorised recyclers/refurbishers. Further, local bodies could work with OSPCB to build capacities for the waste management staff and the informal sector to ensure the safe handling, transportation, sorting, and storage of battery waste. The OSPCB may facilitate the development of capacity-building modules in consultation with the recyclers.

● Odisha Skill Development Authority (OSDA) to create short-term modules to upskill existing ITI graduates and include battery chemistry and battery waste recycling as a part of their courses.

● The Skill Development and Technical Education Department, in conjunction with the State Council for Technical Education and Vocational Training (collectively “Skilling bodies”) to facilitate the inclusion of battery chemistries and battery waste management expertise as a part of the ITI curriculum. These courses must be developed in consultation with the recycling industry to meet their requirements and have an internship component to give field exposure to the trainees.

2. Potential role of the private sector:

● Battery ‘producers’, as defined in BWM Rules, must lead the creation of an efficient battery recycling ecosystem. Some immediate priorities include:

○ Reducing waste leakages: producers can explore innovative business models such as ‘battery as a service' or introduce incentives such as a deposit refund scheme to ensure the handover of waste batteries for safe treatment. This can also be done by creating a strategic network of collection centres, EV battery replacement, or scrapping centres in cooperation with the recyclers. The private sector involved in the operations and maintenance of stationary storage should tie up with the recyclers for the collection of end-of-life LIBs to close the loop and bring the critical materials back to the LIB production supply chain.

○ Channelling waste to authorised recyclers: producers can leverage the EPR portal introduced by CPCB, have direct tie-ups with recyclers, or enter long-term contracts with recyclers. This shall also mitigate recyclers' waste supply issues and secure recycling investments.

○ Disclosing battery chemistry and composition: producers can adopt ‘Battery Passport’ to share battery-related information across users in the value chain. This shall ensure efficient sorting and recycling by dismantlers and recyclers.

● In the medium term, battery manufacturers or original equipment manufacturers (OEMs) should adopt strategies such as circular design and standardisation of battery packs for similar applications that can ease and scale the dismantling and recycling process of battery waste. Regular dialogues among OEMs and recyclers would help design effective solutions.

● Waste management entities such as dismantlers and recyclers should collaborate with the OSDA and state Skilling bodies to update the respective courses and curriculum with practical skills on testing and discharging batteries, knowledge of chemistries, operating relevant machineries, etc.

● Recyclers can also collaborate with local bodies or the Housing and Urban Development Department (H&UDD) to communicate any minimum sorting requirement of battery waste that can be potentially undertaken at the level of the local bodies.

● Low levels of LIB waste aggregation: Most of the collection of LIB waste found in e-waste (such as mobiles and laptops) remains in the unorganised/informal sector. This sector has a better reach for waste generators and offers competitive salvage value to formal channels, leading to supply-related challenges for formal waste management entities. Furthermore, as the informal sector does not process waste efficiently and safely, there is limited resource recovery and significant environmental degradation. Additionally, due to the lesser quantity of LIB waste generation in other applications from EVs and stationary storage, currently, aggregation of LIB waste is a challenge. Hence, efficient reverse logistics of batteries is urgently needed to tap the battery recycling market opportunity.

Way forward:

1. Awareness among consumers: Targeted awareness campaigns should be undertaken for registered vehicle scrapping facilities and entities engaged in operations and maintenance of stationary storage batteries to ensure that the batteries are channelised to authorised recycling facilities. They should also be made aware of the regulatory and environmental implications of mismanagement of such batteries to ensure fulfilment of this requirement. The local bodies can facilitate awareness drives and programmes, both for citizens and groups/associations of dealers, the informal sector, etc., to highlight the provisions of the BWM Rules and the roles and responsibilities of the different stakeholders. These can be coupled with the existing awareness drives for waste segregation to guide the deposition of battery waste with either e-waste or domestic hazardous waste or separately.

2. Integration of the informal sector: The BWM Rules can draw parallels from E-waste (Management) Rules, 2022, to recognise informal workers and facilitate the formation of groups to set up facilities for primary activities such as sorting batteries, which can then be channelised to registered processing units. The OSDA can organise skill, health, and safety training for the workforce, both formal and informal, performing such activities.

3. Proactiveness by local bodies and OSPCB: The local bodies can tie up with authorised producers and recyclers to channelise the battery waste, either sorted in existing municipal facilities or dedicated battery waste facilities as set forth above, to create a more formal supply chain. Further, they can create a separate empanelment process for private entities who intend to collect, sort, and channel battery waste to authorised processing units for accountability and compliance with the BWM Rules.

● Low availability of skilled workforce: The existing workforce in waste management sectors lacks knowledge of various battery chemistries (to handle and prepare the waste for processing) and operation of the relevant machinery. The limited skillset of the workforce is a huge impediment to the battery recycling industry.

Way forward: The OSDA to create short-term modules to upskill existing ITI graduates and the curriculum with such topics. It should leverage battery training programmes run by other institutions, such as MEiTY, to customize the curriculum for this sector (MEiTY n.d.).

Further, the state Skilling bodies can facilitate the inclusion of battery chemistries and battery waste management expertise in the ITI curriculum, including practical training and visits to battery recycling facilities. These can be undertaken at different levels depending on the aptitude, experience, and qualifications of the students. Given its hazardous nature, such training will make the workforce aware of the requisite safety measures.

● Flammability of LIBs: LIBs are highly flammable, and due to high residual charge, the transportation of battery waste is likely to cause fire hazards. Hence, it is a huge safety challenge.

Way forward: In this regard, it is important for the CPCB (and/or OSPCB) to specify guidelines, standards or other compliance requirements for the safe collection and packaging, labelling, transportation, and storage of battery waste, as have been issued for hazardous waste management (NPC 2019). The SPCBs enforce these guidelines. The guidelines should be supplemented with awareness and skills development (discharging, sorting) for all workers engaged in collection and transportation activities.

● Environmental risks: Battery recycling is a complex process and could potentially lead to severe environmental footprint if the spent chemicals used in recycling or the unprocessable waste is not disposed properly. OSPCB to ensure, through audits or inspections, that all certified waste management entities adhere to all safety and environmental norms to avoid any impact on the local surroundings, including disposing of unprocessable waste in authorised treatment, storage, and disposal facilities (TSDF).

● Risks in investment and volatility in commodity prices: With the battery manufacturers being more cognisant of supply chain risks in various battery materials, there are visible trends of technology evolution to reduce the content of these materials. For instance, cobalt-free batteries such as lithium-ferro phosphate (LFP) are gaining traction over lithium nickel manganese cobalt oxide (NMC) (IEA 2023). These technology shifts will reduce the economic benefits of recycling. Hence, an obsolescence risk of current battery technologies can impact investments in today’s recycling infrastructure. Additionally, there is a risk that the relatively lower-value batteries, such as LFP, will not be recycled as much due to relatively lower profits (Willing 2023). Hence, these patterns should be identified to ensure that such LIBs are not disposed of without proper management, and recycling is encouraged through mechanisms such as financial incentives or subsidies.

The battery waste recycling infrastructure requires significant capital investment. The commodity prices of materials recovered from battery waste are volatile as they depend on the demand and supply of materials from the industries it caters to. For instance, slowing demand for EVs for a short period compared to the production targets can cause a drop in LIB prices and potentially risk the return on investments made overall. Recyclers must stack multiple revenue streams to secure returns on their investments.

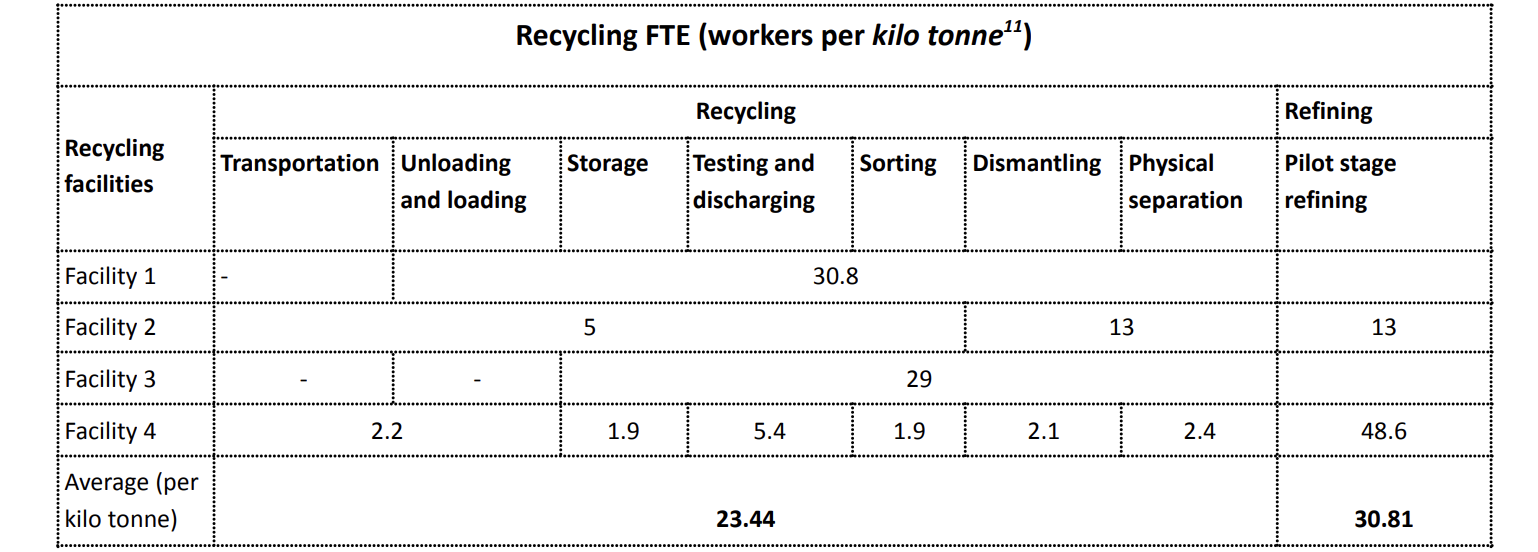

The scope of the LIB waste recycling value chain is limited to jobs generated from recycling operations that include partial secondary transportation to the recycling facilities 9 , sorting, testing and discharging, recycling (dismantling and physical separation) and refining 10 undertaken at the recycling facility. These jobs are created at or by a recycling plant.

Activities prior to recycling, which include primary collection and aggregation, are not included in the scope of the current analysis due to data unavailability. The scope excludes corporate functions of the recyclers, such as accounts, human resources, legal, etc., and ancillary activities related to insurance, banking, chartered accountants, etc. These functions are not directly linked to the operational capacity of the recycler. Hence, only direct jobs from recycling operations are estimated in this analysis.

● Direct jobs are converted to a full-time equivalent (FTE). The full-time equivalent or job year is defined as simply a ratio of the time spent by an employee on a particular task/project in a given year to the standard total working hours in that particular year. The FTE formula translates short-term or one-time employment into a full-time equivalent or job-year (Tyagi et al. 2022).

● In this analysis, FTE for recycling operations is the number of workers engaged in the recycling operations in a year divided by the quantity of waste recycled in a year.

● Key informant interviews (KIIs) were conducted with identified players in the LIB waste recycling ecosystem in order to arrive at the FTE. The interviews focused on the number of people employed for LIB recycling operations, average capacity utilisation, challenges and risks for the ecosystem, skilling requirements, etc.

● The market opportunity is estimated as the revenue accrued by selling recovered materials from recycling LIB.

● Investment opportunity refers to the capital expenditure to be incurred in setting up the LIB waste recycling facilities. This includes the cost of land, building, and machinery.

Two scenarios were developed for estimating the market, investment, and employment opportunity: policy and ambition. These differ in the quantum of waste and recycling targets.

KIIs were conducted with identified players to calculate the LIB waste recycling FTE and estimate the jobs.

● A mix of purposive and convenience sampling strategies was used to identify the stakeholders for KIIs.

● Six KIIs were conducted with recyclers, of which four recyclers' data have been obtained and considered for analysis. The recyclers’ activities included partial waste transportation to the recycling facilities, storage, testing and discharging, sorting, recycling (dismantling and physical separation), and refining at a pilot stage. The annual recycling capacity of these facilities ranges from 350 to 3,600 tonnes.

● Questionnaires were used to gather information and data from the respondents. The broad heads under the questionnaire included specifications of the recycling plants such as capacity, personnel deployed for overall recycling operations, etc., and stages of recycling. There were also qualitative questions on skill requirements at different stages of recycling, risks associated with the recycling ecosystem, prevalent challenges in the ecosystem, and interventions that can potentially solve them.

Annual FTE for LIB waste recycling is computed as:

Full time equivalent (per Kilo tonnes) = Total number of worker employed for recycling and refining operations /

Total waste recycled and refined in the year (in kilo tonnes)

Table 1: Annual FTE calculated using data received from the KIIs

Source: Authors’ analysis based on stakeholder consultations

● It should be noted that this analysis does not consider any reduction in employment due to increased automation of various recycling operations.

The market opportunity has been estimated from the sale of materials recovered from LIB waste within or outside Odisha. The following methodology was used to calculate the market opportunity across the two scenarios: policy and ambitious.

● First, the LIB waste generated in Odisha from 2024-2030 12 was projected under three product categories: electric vehicles (EVs), stationary storage (from telecom towers), and consumer electronics (mobiles and laptops/computers). The sections below discuss this in detail. Next, the LIB waste was characterised (battery type and composition) based on the product categories. Thereafter, recycling rates as per the extended producer responsibility (EPR) targets under the Battery Waste Management Rules, 2022, were applied to the waste projected to calculate the LIB waste to be recycled. Recovery rates for hydrometallurgy recycling were used to arrive at the quantum of recovered materials from recycled waste. Lastly, it was multiplied with the market price of the materials to estimate the revenue from recycling. The market opportunity is, therefore, a summation of the quantum of product and price of all recoverable materials from LIB waste:

Market opportunity (USD) = ∑(Recovered material from LIB waste (Kg) ) *(market price (USD/Kg)) i indicates the recoveraboe materials from the LIB waste USD to INR = 83

● The following sections detail these stages:

i. Composition of different battery types:

The LIB waste is bifurcated into different types of batteries based on the type of vehicle or product. Thereafter, the composition of materials for different batteries by weight is used to calculate the quantum of different materials in the LIB waste.

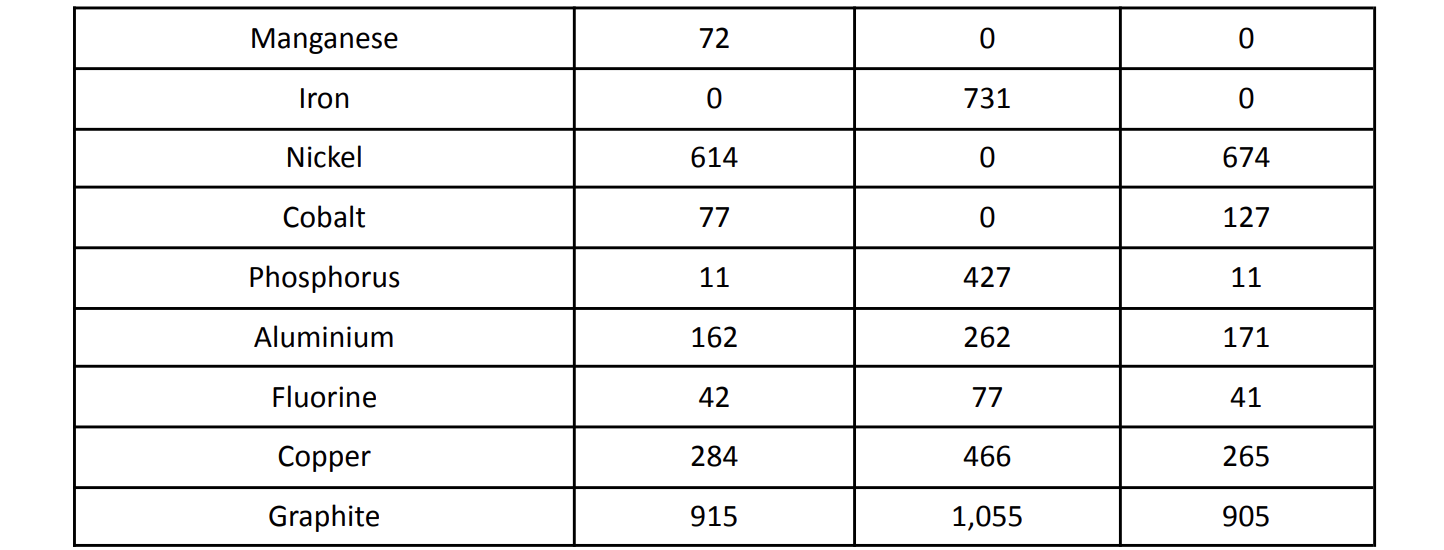

Table 2: Composition of different battery types

Source: Niti Aayog 2022

Source: Niti Aayog 2022

ii. Recovery rates

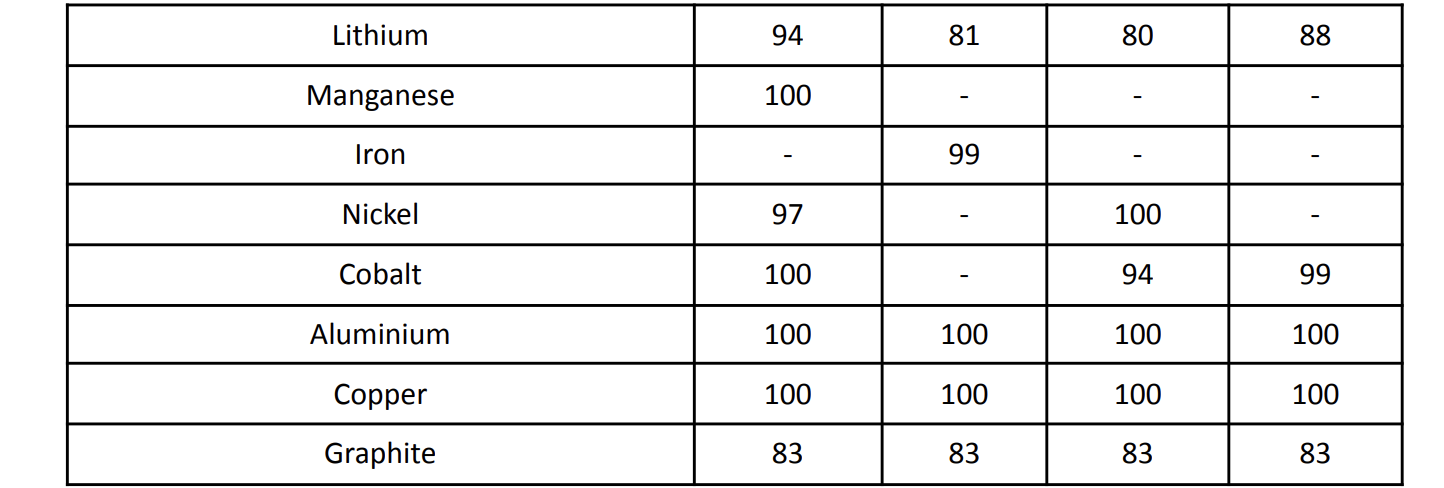

Thereafter, materials found in the LIB waste and to be recovered are multiplied by the recovery rates to estimate the quantity of recovered materials from LIB waste using hydrometallurgy recycling. Below are the recovery rates of minerals from hydrometallurgy recycling of LIB waste:

Table 3: Recovery rates of minerals from hydrometallurgy recycling of LIB waste

iii. Prices of recovered materials

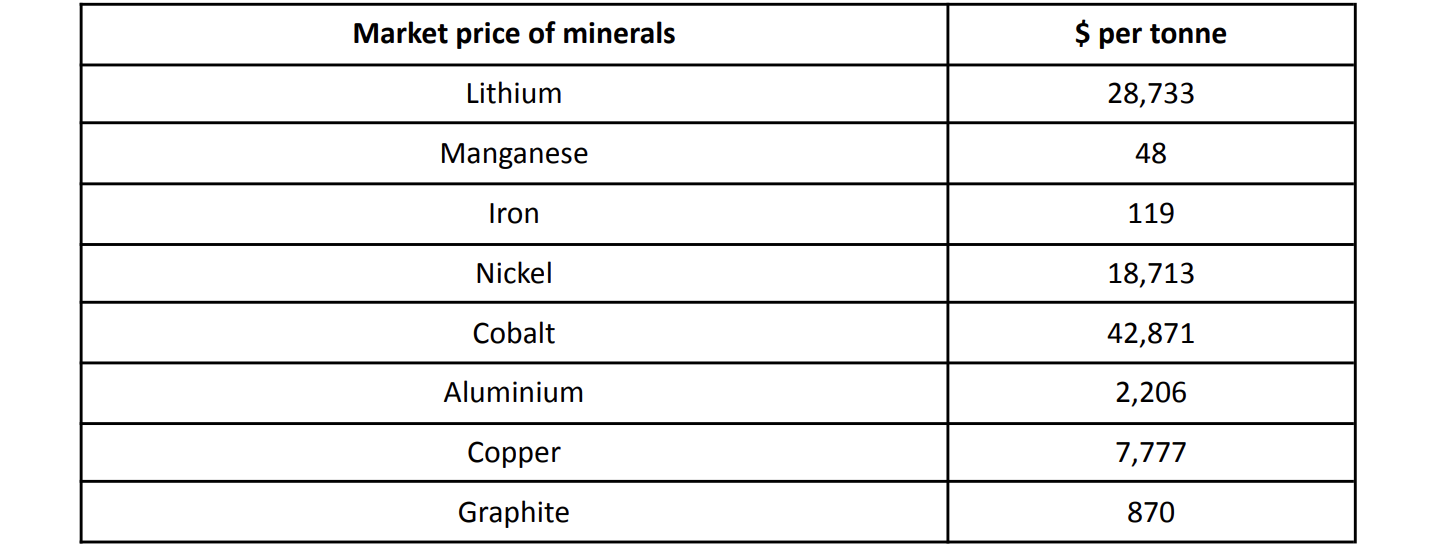

The quantum of recovered materials is then multiplied by the market prices to arrive at the market opportunity for this value chain. 17 There is a huge range in the prices of recycled materials depending on their purity. As a result, we have used the price of virgin counterparts as a proxy for recycled materials in this analysis. The prices of the recovered material from recycling LIB have been taken from secondary sources. The average prices for five years, 2019-2023, have been used for the assessment period (2024 to 2030). The prices are kept constant, and any change in the prices will directly impact the market opportunity.

Table 4: Average prices of materials

Source: Indian Bureau of Mines and Daily Metal Prices

Market opportunity for the three product categories across the two scenarios: policy and ambitious.

1. Market opportunity for electric vehicles (EVs)

Waste generation:

● 2w, 3w, cars, and bus sales in Odisha were taken from the Vaahan dashboard and projected until 2030 using a CAGR (compound annual growth rate). (Refer to Annexure II for detailed calculation).

● New EV sales in Odisha were obtained from the Vaahan dashboard from 2014 to 2023. The EV penetration percentage in each vehicle category was calculated using the formula below.

EV penetration in each category = (total EV sold in the year / total vehicle sold in that year)*100

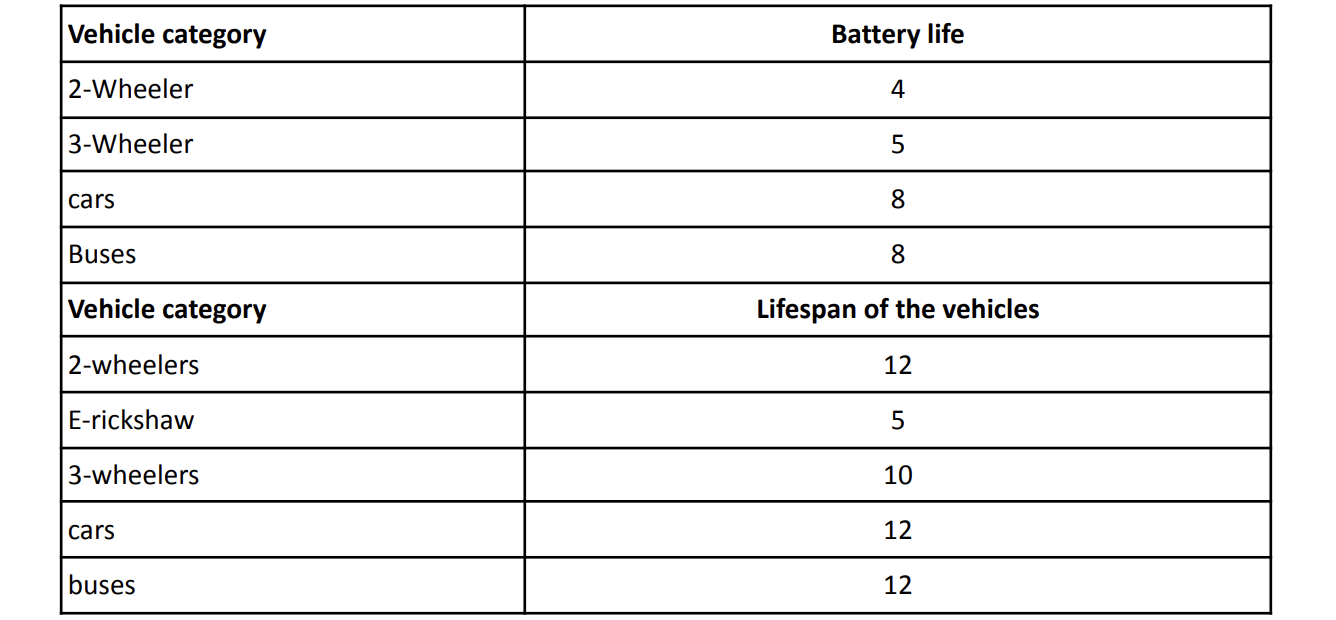

● Thereafter, the life of the batteries was derived from the extended producer responsibility (EPR) targets under the Battery Waste Management Rules, 2022 (BWM Rules). The life of 2w, 3w, cars, and buses is applied to EV sales to calculate the number of LIB waste from 2024 to 2030. The life of the vehicle has been taken from secondary sources.

Table 5: Life of battery and vehicles

Source: Battery Waste Management Rules, 2022 for battery life; For the lifespan of the vehicles: 2-wheelers - AMO Electric Bikes 2022, e-rickshaw - Shandilya et al. 2019, 3-wheelers - expert consultations, cars - Government of NCT of Delhi 2021, buses - Khanna et al. 2024

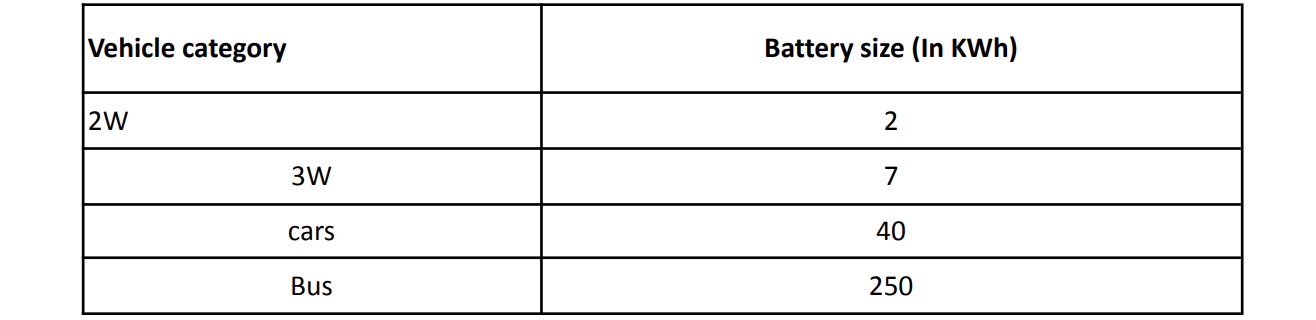

Table 6: Battery size of different vehicle categories:

Source: Niti Aayog 2022

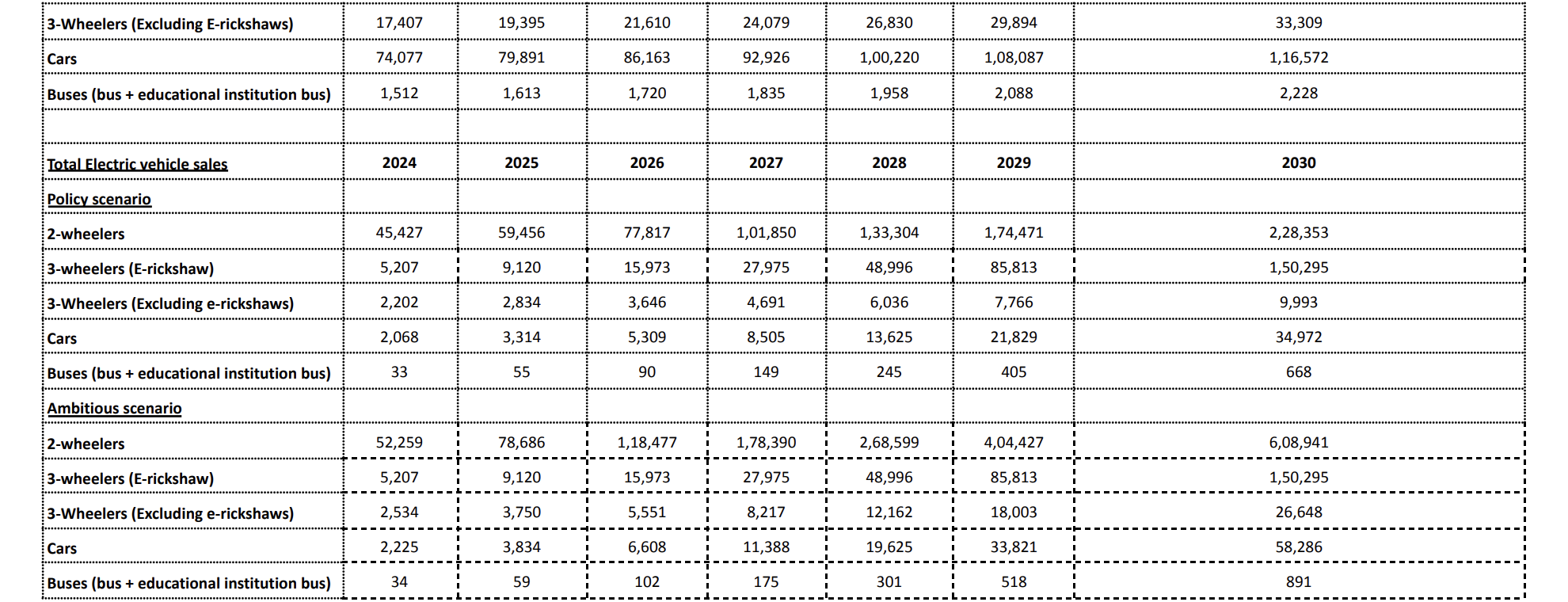

● Under the policy scenario, it is assumed that Odisha will also meet India's EV penetration target of EV30@30 (Niti Aayog 2023), i.e., 30 per cent of new EV sales by 2030. In this regard, the current EV penetration percentage, i.e., in 2023, is projected to reach 30 per cent across all the vehicle categories by 2030, and the EV sales are calculated year on year from 2024 to 2030 using this trend. In this context, the LIB waste generation from EVs for the period 2024-2030, under the policy scenario, was estimated:

Table 7: Estimated LIB waste generation from EV in Odisha under the Policy scenario for 2024-30

Source: Authors’ analysis

● Under the ambitious scenario, it is assumed that EV sales penetration will be 30 per cent of private cars and 70 per cent of commercial cars; therefore, an average of 50 per cent is taken for cars. Additionally, penetration will be 40 per cent for buses and 80 per cent for two and three-wheelers by 2030. This scenario is conditional on the success of FAME II and other measures India takes (NITI Aayog and Rocky Mountain Institute 2019). In this regard, the current EV penetration percentage, i.e., in 2023, is projected to reach these percentages across all the vehicle categories by 2030 and, the EV sales are calculated year on year from 2024 to 2030 using this trend. Similarly, the LIB waste generation from EVs for the period 2024-2030, under the ambitious scenario was estimated:

Table 8: Estimated LIB waste generation from EV in Odisha under the ambitious scenario for 2024-30

Source: Authors’ analysis

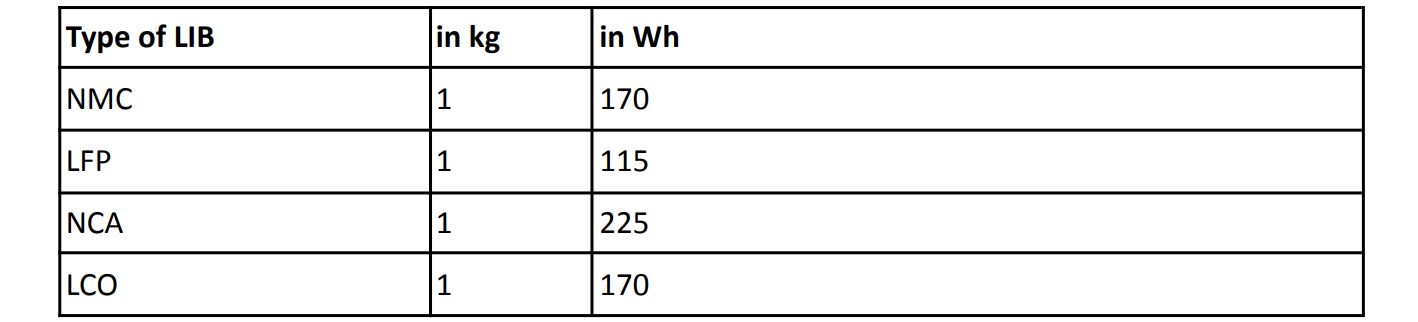

● The below conversion metrics were used to calculate the LIB from Wh to kgs:

Table 9: Size of different types of LIBs

Source: Niti Aayog 2022

Waste characterisation:

● The LIB technologies for different vehicle categories have been taken from CEEW analysis of the demand for transport technologies. These technologies are kept constant for the assessment period (2024 to 2030).

Table 10: Battery technology for LDVs

Table 11: Battery technology for HDVs

Source: Warrior, Tyagi, and Jain 2023

● It is important to note that recent reports have shown a declining trend for NMC batteries in LDVs and leaning more toward LFP, as shown in the table below. This trend is mainly driven by Chinese original equipment manufacturers (OEMs).

Table 12: Battery technology trends in LDVs

Source: Compiled from IEA 2023

On the contrary, only approximately 3 per cent of EV cars with LFP batteries were manufactured in the United States in 2022. Additionally, new technologies such as sodium-ion are emerging, which are cost-effective and do not rely on critical minerals (IEA 2023). However, there is limited granular data on battery chemistries and the distribution of various subtypes across vehicle categories. As a result, the earlier available data, which indicated the dominance of NMC chemistry in LDVs, is used in the analysis. This trend may change and will directly impact the market opportunity estimated herein.

Recycling and recovery rates

● Market opportunity for policy scenario: The recycling targets under EPR under the BWM Rules have been considered as the recycling rate for EVs from 2024 to 2030, i.e., 70 per cent. Therefore, the quantity of LIB waste to be recycled cumulatively from 2024 to 2030 for the policy scenario is 2.6 kilo tonnes. Applying the recovery rates and the prices set out above, the market potential comes to be 8.2 million USD.

● Market opportunity for ambitious scenario: Recycling targets are considered to reach 100 per cent, by 2030 given that considerable increase in recycling capacities are projected in India. Therefore, the quantity of LIB waste to be recycled cumulatively from 2024 to 2030 and for the ambitious scenario it is 4.3 kilo tonnes. Applying the recovery rates and the prices set out above, the market potential comes to be 13.5 million USD.

2. Market opportunity for LIB waste from stationary storage

Waste generation:

● For stationary storage, only LIBs for telecom towers in Odisha are considered. The contribution of other applications, such as power backup systems, is not considered as these systems largely use lead-acid batteries, and the current penetration of LIB is low. The absence of any Odisha-specific study projecting the future trajectory of LIB penetration in these applications further limits the waste generation modelling.

● As per the Department of Telecom, there are 25,115 telecom towers in Odisha (Business Standard 2023). Furthermore, as per India Energy Storage Alliance, LIB penetration is up to 20 per cent in the telecom sector (IESA 2022). Therefore, it is assumed that 20 per cent of the stationary storage battery waste from telecom towers will be LIB waste, i.e., 5,023 units.

● The calculation of the average battery energy capacity for telecom tower batteries involves utilising the average voltage (V) and ampere-hours (Ah) of the battery. The resulting battery capacity in watt-hours (Wh) is obtained by multiplying V with Ah. On average, the battery capacity for a telecom tower is 600 Ahr and 48 V, having a capacity of 28,800 Wh.

Waste characterisation:

● The primary technology for stationary storage batteries leans towards LFP, with a minor contribution from NMC (Warrior, Tyagi, and Jain 2023). The average weight of batteries, as mentioned in previous sections, is also used for LIB in stationary applications.

● Therefore, the end-of-life LIB waste is calculated using the below formula:

LIB waste (in tonnes) = i ∑ LIB waste in unite * LIB capacity per telecom tower* LIB technology percentage i /

Average energy densityy i *1000

Where:

i= 1,2 where 1 is LFP battery, and 2 is NMC battery

LIB waste: 5,023 units.

LIB capacity per telecom tower: 28,800 Wh

LIB technology percentage: 17 per cent for NMC and 80 per cent for LFP

Average energy density: 115 Wh per kg for LFP batteries and 170 Wh per kg for NMC batteries.

● As per the above calculation, the LIB waste from stationary storage will be 1,151 tonnes.

● The life of these batteries is assumed to be eight years, given that they are primarily LFP (Lithium iron phosphate). Since buses are also primarily LFP and have the EPR targets applicable after eight years of placing the battery in the market under the BWM Rules, the same target has been applied to stationary storage batteries.

● In this context, LIB waste from telecom tower stationary storage LIBs existing in 2023 will reach 1,151 tonnes in 2030 in Odisha. Please note that any discontinuity, replacement, etc., has not been considered for this calculation.

Recycling and recovery rates:

● Market opportunity in policy scenario: The recycling target for industrial battery under EPR under the BWM Rules has been considered as the recycling rate for stationary storage from 2024 to 2030, i.e., 70 per cent. Applying the recovery rates and the prices set out above, the market potential is 1.88 million USD from recycling 800 tonnes.

● Market opportunity in ambitious scenario: Recycling targets are considered to reach 100 per cent, by 2030, given that a considerable increase in recycling capacities is projected in India. Applying the recovery rates and the prices set out above, the market potential is 2.68 million USD from recycling 1,151 tonnes.

2. LIB waste from consumer electronics

Waste generation:

● Two categories of consumer electronics: mobiles and laptops/computers, were selected to estimate LIB waste from consumer electronics generated in Odisha.

Mobiles

● As per Odisha Economic Survey, 2023 (Planning and Convergence Department 2023), 80.7 per cent of households had mobile access in 2015-16 and 88.3 per cent in 2019-21. In this context, the penetration of mobiles in households is projected to reach 100 per cent by 2030.

● Using Odisha’s population projections till 2030 (Ministry of Health and Family Welfare 2020) and assuming that the average number of members in a household is 4.3, the number of households was estimated until 2030.

● Thereafter, penetration per cent of mobile access was used to calculate the number of households that had mobile access. It is assumed under this analysis that each household will have one mobile. The average life of mobiles is considered to be three years, even though, as per the E-waste (Management) Rules, 2022, the lifespan is given as five years. This is because of the reduced mobile lifespan (Statista 2023). Applying the life of mobiles to the number of mobiles and the average weight of mobile battery, LIB waste from mobiles was calculated. However, any change in the penetration of mobiles in households will directly impact the market opportunity.

Computers

● Odisha’s computer facility penetration was 4.3 per cent of households in 2019 (Indian Express 2019). It is assumed that each such household will have only one computer/laptop. Assuming this penetration constant till 2030 for the current analysis, the number of computers/laptops sold was calculated. Any change in the penetration of computers/laptops in households will directly impact the market opportunity.

● The average life of computers/laptops is considered to be 5 years as per the E-waste (Management) Rules, 2022. Applying this life to the number of computers/laptops along with the average weight of their battery, LIB waste from computers/laptops was calculated.

Waste characterisation

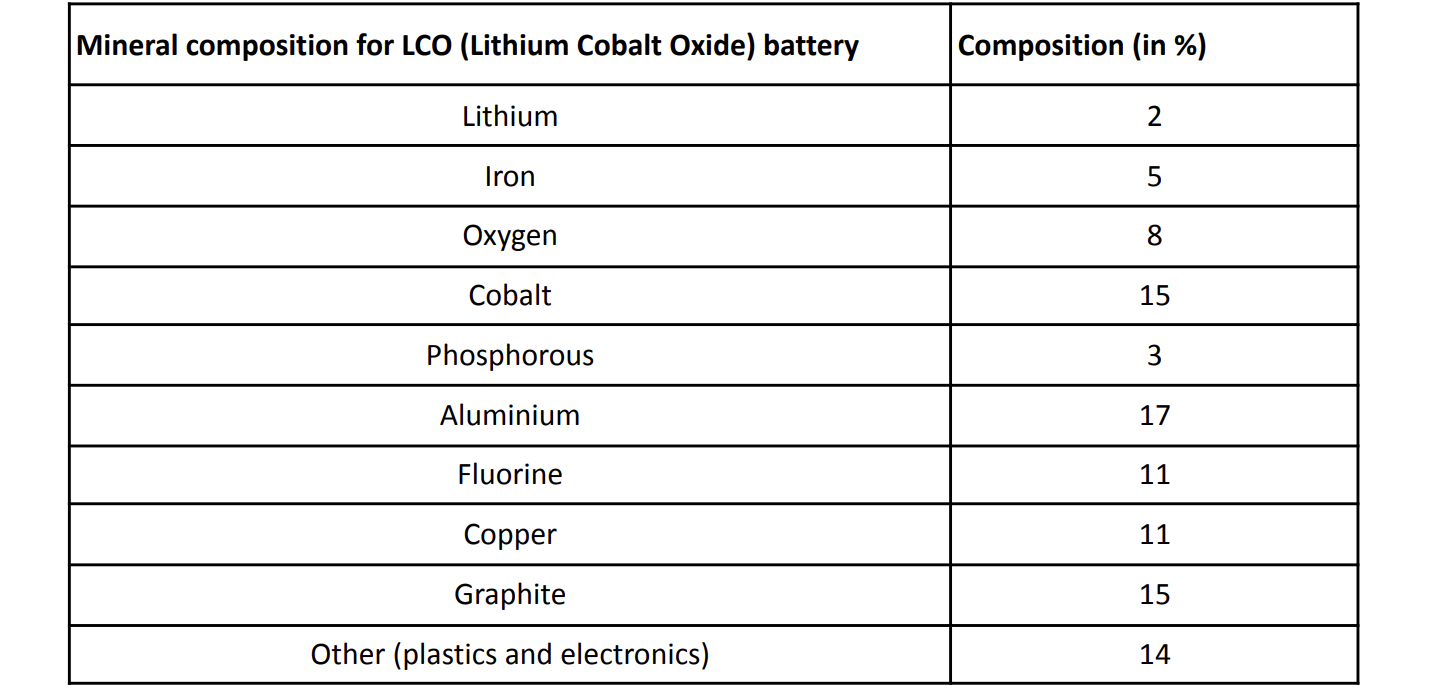

● The average battery weight for mobiles is considered to be 56 gms, and for laptops, it is 235 gms. This has been estimated from secondary sources of companies selling these products. However, this weight may vary depending on the battery size, mobile type, and price; therefore, any change in the weight of the battery will change the market opportunity. The average battery weight of Lithium Cobalt Oxide (LCO) is 170 Wh per kg. Consumer electronics will predominantly use LCO battery technology till 2030 (Niti Aayog 2022). Therefore, using the below formula, the quantum of LIB waste from consumer electronics in the period of 2024-2030 can be estimated.

LIB waste (in tonnes) = Number of LIB waste in the year * average battery weight (in tonnes)

● On the basis of the above methodology, the LIB waste generated from consumer electronics for the assessment period 2024-2030 in Odisha is 1.4 kilo tonnes or 1,440 tonnes.

Recycling and recovery rates

● Market opportunity in policy scenario: The recycling target for portable batteries used in consumer electronics that is chargeable under EPR under the BWM Rules has been considered as the recycling rate from 2024 to 2030, i.e., 70 per cent. Applying the recovery rates and the prices set out above, the market potential is 7.4 million USD by recycling 1 kilo tonnes.

● Market opportunity in an ambitious scenario: Recycling targets are considered to reach 100 per cent by the year 2030, given that considerable increase in recycling capacities is projected in India. Applying the recovery rates and the prices set out above, the market potential appears to be 8.9 million USD by recycling 1.2 kilo tonnes.

The total estimated market opportunity (across all product categories) under the policy scenario for recycling (including pilot stage refining) LIB waste generated (from all three categories) in Odisha from 2024-2030 is 17.4 million USD.

The total estimated market opportunity (across all product categories) under the ambitious scenario for recycling (including pilot stage refining) LIB waste generated (from all three categories) in Odisha for the period of 2024-2030 is 25 million USD.

The FTEs calculated for recycling and refining (at a pilot stage) are used on LIB waste generated. The results are as follows:

- Under the policy scenario, the total cumulative jobs for the assessment period 2024-2030 is 108 for recycling and refining (at a pilot stage), a cumulative LIB waste of 4.4 kilo tonnes. The LIB waste generation in the last year 2030 is approximately 2,000 tonnes.

- Under the ambitious scenario, the total cumulative jobs for the assessment period 2024-2030 is 181 for recycling and refining (at a pilot stage), a cumulative LIB waste of 6.6 kilo tonnes. The LIB waste generation in the last year 2030 is approximately 3,344 tonnes.

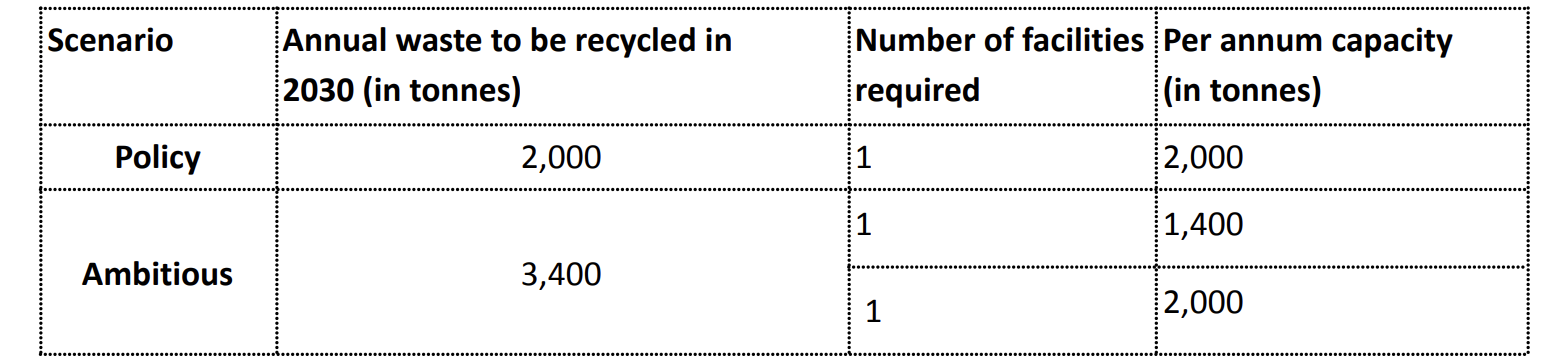

Investment opportunity is the capital expenditure (capex) to be incurred in setting up the LIB waste recycling facilities under different scenarios.

○ An average estimate of a secondary source (Moerenhout et al. 2022) and a primary consultation was used as the capital expenditure. Annexure III contains the details.

○ The recycling capacity was sized to the maximum LIB waste generated in Odisha, that is for the year 2030. The number of recycling plants and capacities are indicative to show the investment potential.

Table 13: Capex requirements

Source: Authors’ analysis

○ In this context, the investment opportunity under the policy scenario is 8 million USD, and under the ambitious scenario, it is 13.5 million USD.

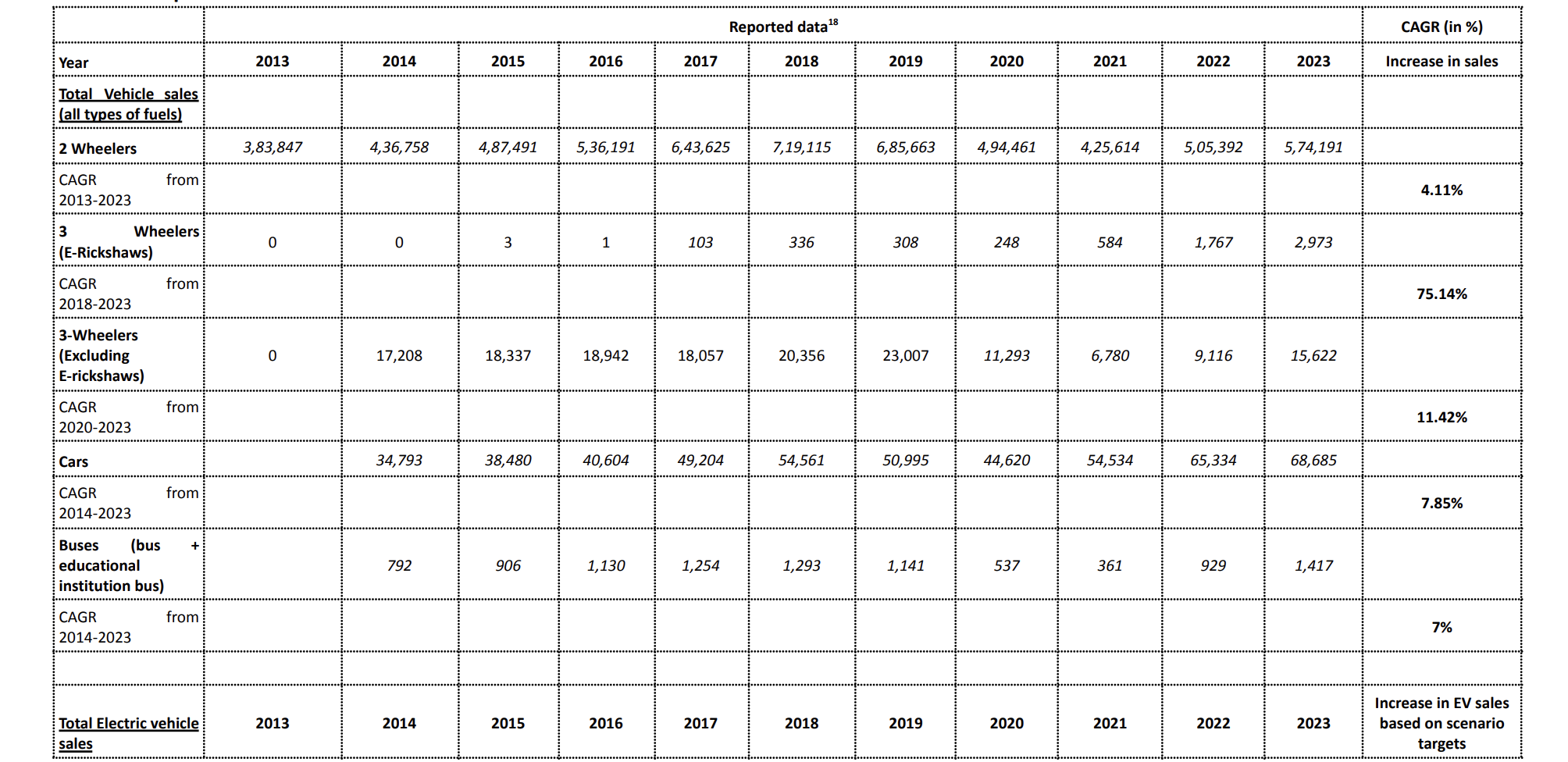

Table 14: Reported data on vehicle and EV sales

Source: Vahan Dashboard

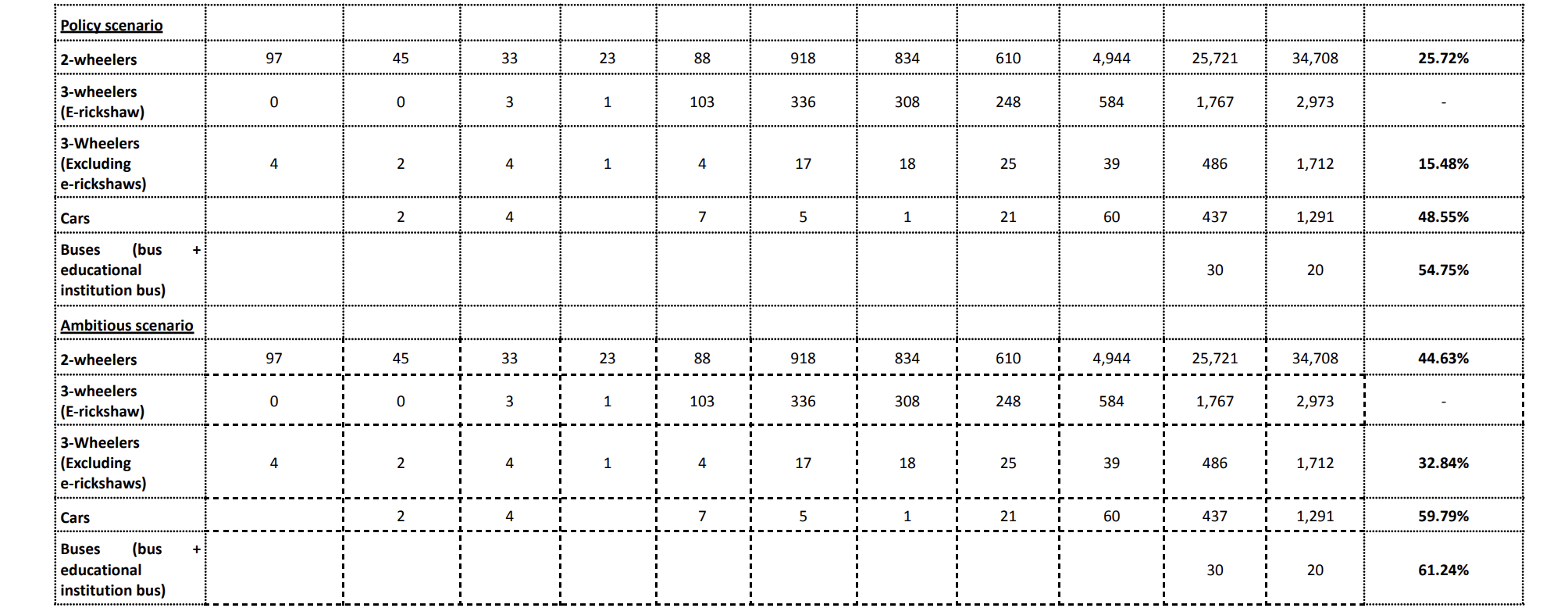

Table 15: Data projected for vehicle and EV sales based on CAGR

Source: Authors’ analysis

Table 16: LIB penetration among other batteries used in EVs

Source: Authors’ analysis based on key market players; e-rickshaws: Niti Aayog 2022

Table 17: Sales years considered to calculate the CAGR for projecting overall vehicle sales in different categories

Source: Authors’ analysis

Table 18: Estimated number of EV LIBs attaining end-of-life (EOL) under policy and ambitious scenarios

Source: Authors’ analysis

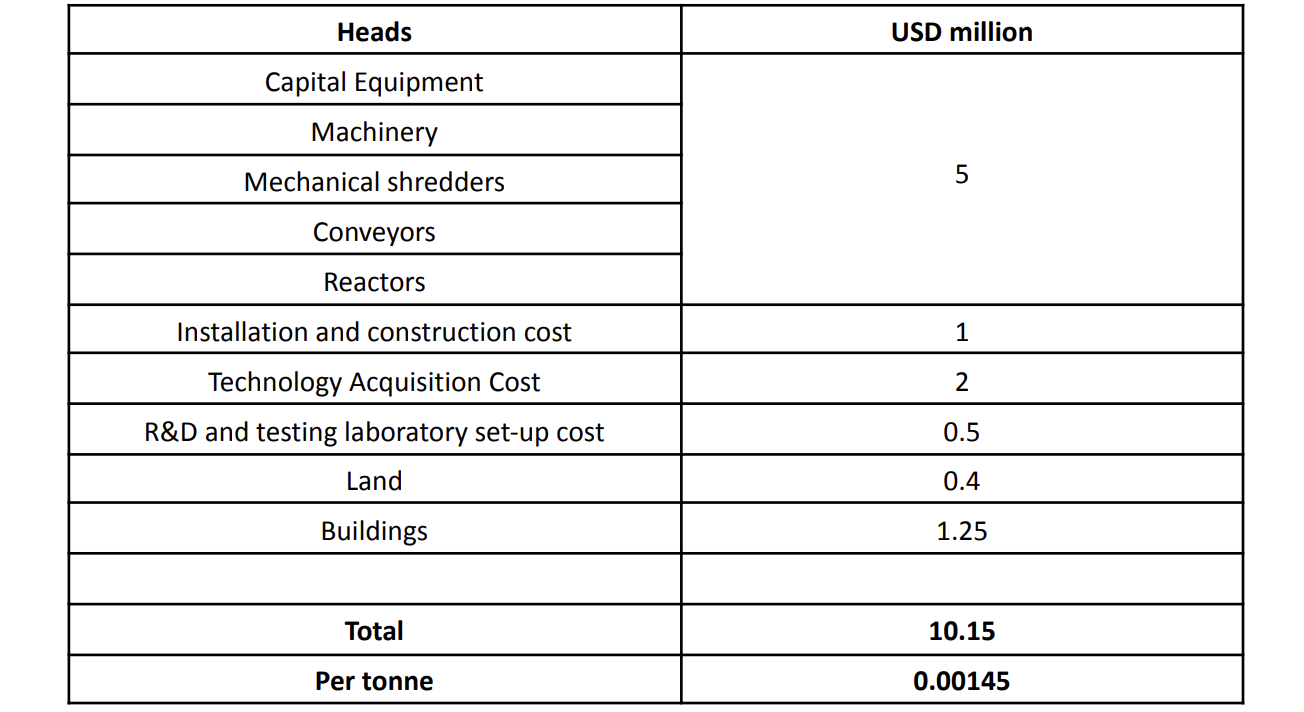

Table 19: Capital expenditure for a LIB recycling facility with a capacity of 5000 to 7000 tonnes per annum

Source: Moerenhout et al. 2022

The primary consultation suggested that for each tonne of LIB recycling facility, approximately 6,500 USD of capital expenditure is required.

Therefore, an average, 0.0040 million USD per tonne is considered to estimate investment opportunity.

AMO Electric Bikes. 2022. “What Is The Life Of Electric Bikes In India?” LinkedIn, June 20, 2022.

https://www.linkedin.com/pulse/what-life-electric-bikes-india-amoelectri...

Business Standard. 2023. "Urban areas in Odisha to get 5G, 1,814 villages to get 4G by December." February 09, 2023.

https://www.business-standard.com/article/current-affairs/urban-areas-in...

Castelvecchi, D. 2021. “Electric cars and batteries: How will the world produce enough?.” Nature 596 (7872): 336–39. https://www.nature.com/articles/d41586-021-02222-1

IEA. 2023. “Global EV Outlook.” Paris: IEA.

https://www.iea.org/reports/global-ev-outlook-2023/trends-in-batteries

IESA. 2022. "India Stationary BTM ES & Railway Battery Market 2021-2030."

https://indiaesa.info/resources/industry-reports/4079-2021-india-station...

Feng, Jin, Beilei Zhang, Pin Du, Yahong Yuan, Mengting Li, Xiang Chen, Yanyang Guo, Hongwei Xie, and Huayi Yin. 2023. "Recovery of LiCoO2 and graphite from spent lithium-ion batteries by molten-salt electrolysis." Iscience 26, no. 11 (2023).

https://www.cell.com/iscience/pdf/S2589-0042%2823%2902174-0.pdf

Government of NCT of Delhi. 2021. “Circular on Supreme Court order that more than 10 years old diesel vehicles and more than 15 years old petrol vehicles shall not ply in NCR.”

https://transport.delhi.gov.in/sites/default/files/transport_data/Circul...

Gupta, et al. 2019. "Recycling of Lithium-ion batteries in India - $1,000 million opportunity JMK Research & Analytics, 2019." New Delhi: JMK Research & Analytics.

https://jmkresearch.com/electric-vehicles-published-reports/recycling-of...

IEA. 2023. “Global EV Outlook 2023 - Trends in batteries” Paris: IEA.

https://www.iea.org/reports/global-ev-outlook-2023/trends-in-batteries

Jha, Manis Kumar, Anjan Kumari, Amrita Kumari Jha, Vinay Kumar, Jhumki Hait, and Banshi Dhar Pandey. 2013. "Recovery of lithium and cobalt from waste lithium ion batteries of mobile phone." Waste Management 33, no. 9 (2013): 1890-1897

https://linkinghub.elsevier.com/retrieve/pii/S0956053X13002171

Joulié, M., R. Laucournet, and E. Billy. "Hydrometallurgical process for the recovery of high value metals from spent lithium nickel cobalt aluminum oxide based lithium-ion batteries." 2014. Journal of Power Sources 247 (2014): 551-555.

https://linkinghub.elsevier.com/retrieve/pii/S037877531301478X

Khanna et. al. 2024. "The Road Ahead for Private Electric Buses in India: Case of Non Urban Routes." New Delhi: SGArchitects, Council on Energy, Environment and Water, and Institute for Transportation and Development Policy, India.

https://www.ceew.in/sites/default/files/the-road-ahead-for-private-elect...

Kumar, Parveen, Pawan Mulukutla and Madhav Pai. 2023. “Enabling EV Battery Reuse and Recycling in India.” New Delhi: World Resources Institute.

https://wri-india.org/sites/default/files/Conference%20Proceeding-Batter...

Lohum. n.d. “Lohum: Home page.” Accessed on January 01, 2024. https://lohum.com

MEiTY (Ministry of Electronics and Information Technology). n.d. “MEiTY: Centres of Excellence.” Accessed on December 10, 2023. https://www.meity.gov.in/centre-excellences

Mercom. 2023. “Himadri Chemical to Set up Li-ion Battery Components Plant in Odisha.” December 07, 2023. https://www.mercomindia.com/himadri-set-up-li-ion-battery-plant-odisha

Ministry of Health and Family Welfare. 2020. “Population Projection for India and states 2011- 2036.”

https://main.mohfw.gov.in/sites/default/files/Population%20Projection%20...

Moerenhout, T., Goldar, A., Ray, S., Shingal, A., Goel, S., Agarwal, P., Jain, S., Thakur, V., Tarun., Gaurav, K., Aneja, DA., Bansal, A. (2022). “Understanding Investment, Trade, and Battery Waste Management Linkages for a Globally Competitive EV Manufacturing Sector. Report.” New Delhi.

https://icrier.org/pdf/Understanding_Investment_Trade_BatteryWaste_Manag...

Muzayanha, Soraya Ulfa, Cornelius Satria Yudha, Adrian Nur, Hendri Widiyandari, Hery Haerudin, Hanida Nilasary, Ferry Fathoni, and Agus Purwanto. 2019. "A fast metals recovery method for the synthesis of lithium nickel cobalt aluminum oxide material from cathode waste." Metals 9, no. 5 (2019): 615. https://doi.org/10.3390/met9050615

https://pdfs.semanticscholar.org/b0fe/27682b0fbd46570dd78fd6beb584c1fc16...

National Productivity Council (NPC). 2019. “Toolkit for implementation of Hazardous Waste Management rules, 2016.”

https://www.npcindia.gov.in/NPC/Files/delhiOFC/EM/Hazardous-waste-manage...

Niti Aayog. 2022. “Advanced Chemistry Cell Battery Reuse and Recycling Market in India.”

https://www.niti.gov.in/sites/default/files/2022-07/ACC-battery-reuse-an...

Niti Aayog. 2023. “NITI Aayog convenes India’s Electric Mobility Enablers under G20 Presidency.”

https://www.pib.gov.in/PressReleasePage.aspx?PRID=1941114

NITI Aayog and Rocky Mountain Institute (RMI). 2019. “India’s Electric Mobility Transformation: Progress to date and future opportunities.”

https://rmi.org/wp-content/uploads/2019/04/rmi-niti-ev-report.pdf

Planning and Convergence Department, Directorate of Economics and Statistics. 2023. “Odisha Economic Survey 2022-23.” Bhubaneswar: Government of Odisha.

https://finance.odisha.gov.in/sites/default/files/2023-02/Odisha%20Econo...

Shandilya, Nandini et al. 2019. “E-rickshaw Deployment in Indian Cities-Handbook.” New Delhi: ICLEI South Asia.

https://shaktifoundation.in/wp-content/uploads/2019/07/Handbook-ERicksha...

Statista. 2023. “Frequency of smartphone change in India as of April 2023.”

https://www.statista.com/statistics/1179244/india-frequency-of-smartphon...

Tao, Ren, Peng Xing, Huiquan Li, Zhenhua Sun, and Yufeng Wu. 2022. "Recovery of spent LiCoO2 lithium-ion battery via environmentally friendly pyrolysis and hydrometallurgical leaching." Resources, Conservation and Recycling 176 (2022): 105921.

https://linkinghub.elsevier.com/retrieve/pii/S0921344921005309

The New Indian Express. 2019. “Odisha at bottom in computer and internet use.” November 30, 2019.

https://www.newindianexpress.com/states/odisha/2019/Nov/30/odisha-at-bot...

Tyagi, Akanksha, Charu Lata, Jessica Korsh, Ankit Nagarwal, Deepak Rai, Sameer Kwatra, Neeraj Kuldeep, and Praveen Saxena. 2022. “India’s Expanding Clean Energy Workforce.” Council on Energy, Environment and Water, Natural Resources Defense Council, and Skill Council for Green Jobs. https://www.ceew.in/sites/default/files/Green-Jobs-Report-Jan27.pdf

Warrior, Dhruv, Akanksha Tyagi, and Rishabh Jain. 2023. “How Can India Indigenise Lithium-ion Battery Manufacturing? Formulating Strategies across the Value Chain.” New Delhi: Council on Energy, Environment and Water

https://www.ceew.in/sites/default/files/how-can-india-scale-lithium-ion-...

Willing, Nicole. 2023. “NMC to LFP transition poses battery recycling challenge.” Argus Media, November 29, 2023.

https://www.argusmedia.com/en/news-and-insights/latest-market-news/25139...