Council on Energy, Environment and Water Integrated | International | Independent

Suggested citation: Saboo Ayushman, Kurinji Kemanth, Harsha Arya. 2025. How can Paddy Straw Storage Strengthen the Biomass Supply Chain? Infrastructure and Finance needs in Punjab. New Delhi: Council on Energy, Environment and Water.

India is projected to be the fastest-growing bioenergy market in the world between 2023 and 2030, accounting for 35 per cent of the global demand. With surplus biomass available, India can utilise this to mitigate crop residue burning, reduce fossil fuel dependence and improve farmer incomes. Punjab generates 20 million tonnes of paddy straw residue, a portion of which is often burnt contributing to poorer air quality in the region. Punjab targets to manage six million tonnes of paddy straw through ex-situ crop residue management in the upcoming year.

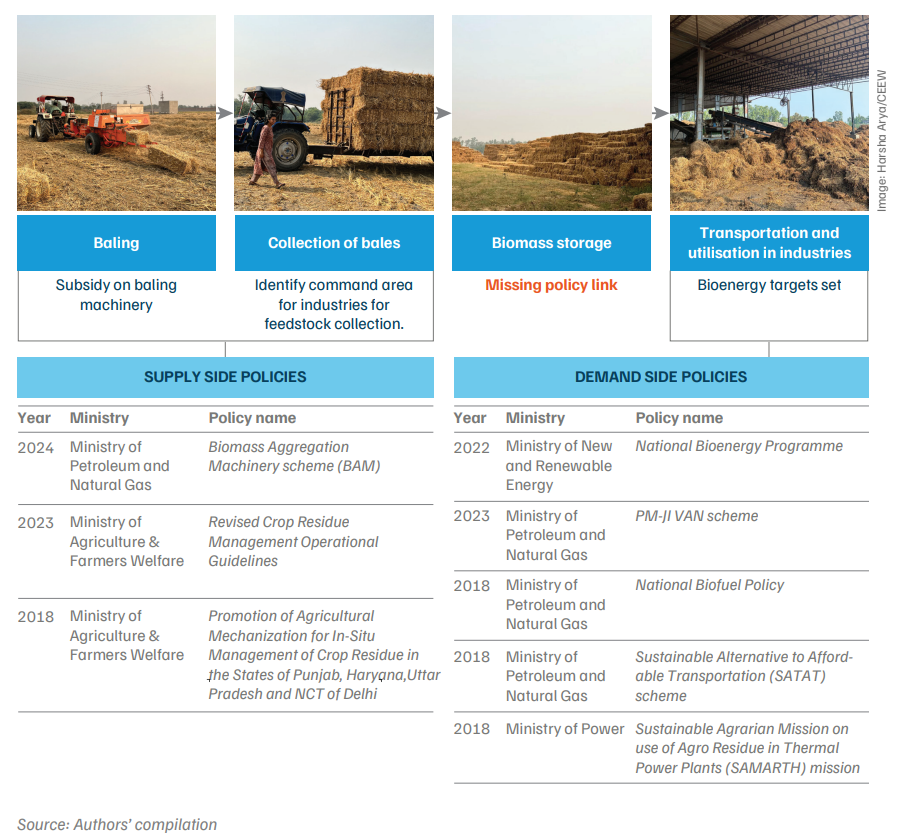

A robust supply chain network is needed from baling to collection to storage and transportation to the end-user to achieve this target, given the seasonal availability of crop residue. Global studies highlight that storage conditions for lignocellulosic biomass, such as paddy straw, are an important parameter to consider while designing bioenergy systems to ensure a continuous feedstock supply. While existing government schemes support baling, collection, and utilisation of crop residue, policy discourse around effective biomass storage is currently missing in India.

The study is conducted using a mixed-methods approach, combining review of global biomass storage policies and field insights from eight paddy straw utilising companies across various sectors in the state of Punjab on feedstock quality, collection, infrastructure and operations. The study provides an overview of factors impacting feedstock quality, examining infrastructure needs, and estimating land and financial requirements for setting up efficient paddy straw-based storage depots for Punjab. Through this study, we aim to inform government and industry stakeholders on the importance of storage and develop storage guidelines for valuable lignocellulosic biomass like paddy straw in India to meet policy targets.

India is projected to be the fastest-growing bioenergy market in the world between 2023 and 2030, accounting for 35 per cent of the global demand (Moorhouse and Báscones 2025). India has already set several blending targets—like 5 per cent compressed biogas blending requirement by 2028–29, 7 per cent of biomass cofiring in power plants by 2026, 20 per cent ethanol by 2025–26 and 5 per cent biodiesel by 2030 (Ministry of Petroleum & Natural Gas 2023). With such growing targets, the demand for sustainably sourced biomass is set to grow, requiring dedicated policy support, robust supply chains, and skilled workforces. Among the various types of biomass, channelling the surplus crop residue of 230 million tonnes generated annually for bioenergy production can deliver India several wins: reduced fossil fuel dependence and stubble burning, creation of rural jobs, and improved farmer incomes.

While existing government schemes support baling, collection, and utilisation of crop residue, policy discourse around effective biomass storage is currently missing in India. Punjab is the central key state taken in the study, as it has increased the utilisation of paddy straw for value added pathways to tackle crop residue burning improving air quality. Our study outlines factors impacting feedstock quality at biomass storage depots, examines minimum infrastructure needs, and estimates investments. We also estimate the budget and land required in setting up effective paddy straw biomass storage depots for managing over 30 per cent surplus paddy straw projected to be used in ex-situ crop residue management in Punjab.

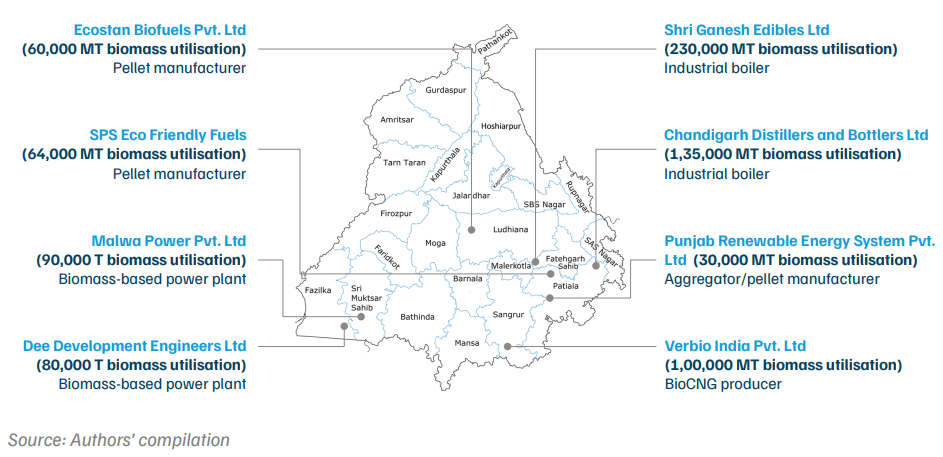

We used a mixed-methods approach for this exploratory study. We reviewed global biomass storage policies and practices, then designed a semi-structured questionnaire for Punjab’s storage depot managers on feedstock quality, collection, infrastructure and operations. From October to November 2024, we conducted field visits and interviewed storage managers of eight major paddy straw utilising companies with capacities between 30,000 and 2,30,000 MT, covering biomass power plants, compressed biogas (CBG) plants, pellet and briquette manufacturers, and industrial boilers. Findings were validated through government and industry stakeholder consultations.

Figure ES1. Storage facilities of eight different companies in Punjab

During our field visits, except for Verbio India Pvt Ltd, all surveyed companies reported paddy straw bale loss between 15 and 25 per cent per annum due to quality degradation at storage depots. They completely discard the bottom layer of the bale stack (3-5 per cent of the whole stack) as water seeps through during the rainy season. With no clear storage guidelines in place, such losses will make a dent in business profitability. In contrast, the importance of biomass storage is seen globally, with countries such as the United Kingdom and the United States providing guidelines outlining the dos and don’ts for bale storage (Wendt 2020; UNFCC 2014; HSE 2012; Thorsell et al. 2004). We find that India has limited literature on biomass storage, with only one paper dating back to 1991. While international studies are critical to identify the parameters for safe biomass storage, the western context has limited replicability for India due to differences in weather conditions.

India has established storage guidelines for valuable commodities like cotton and jute bales, cattle feed and fire safety codes for coal storage yards in the past (BIS 2019; Central Warehousing Corporation 2009; BIS 2002; Garg, Sherasia and Bhanderi 2013). India must derive inspiration from such directives for establishing guidelines for paddy straw and other biomass storage for biofuel production.

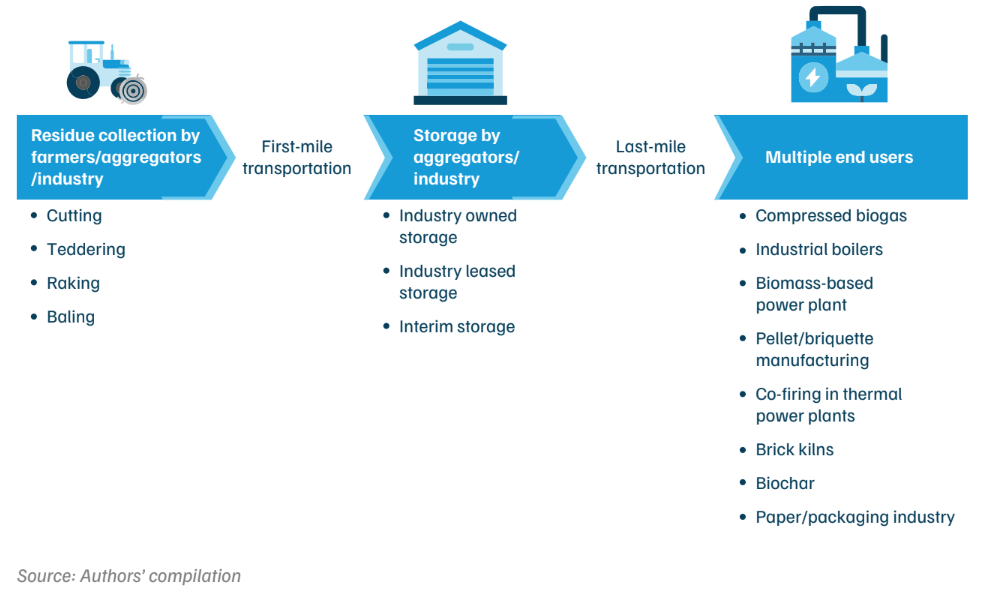

In Punjab, biomass-based companies begin collection by slashing the paddy straw, followed by drying to reduce the moisture content during the short harvest window of 15–20 days. The loose stubble is then arranged in rows by a rake and baled using a baler. Once baled, the biomass is loaded onto trolleys, transported to storage facilities, and unloaded into stacks for storage (Figure ES2).

Figure ES2. The ex-situ supply chain includes a wide variety of stakeholders

Figure ES3. Leased land has limited infrastructure development compared to company owned land

Table ES1. Key infrastructure deployed to reduce biomass losses, avoid waterlogging, and prevent fire risks

| Infrastructure measure | Purpose |

|---|---|

| Biomass cover | Biomass stacks are covered by sheds (higher cost, durable) within industrial land, or tarpaulins. |

| Drainage | Proper drainage is essential for maintaining feedstock quality and allowing water runoff at the stacks' base level. Depending on the land, drainage can be in the form of trenches, or with proper lining. |

| Flooring | Raised stack platform, averaging 1–1.5 feet above ground level, with a slope, protects the bottom layer of the biomass stack from deterioration by preventing moisture absorption from the ground. |

| Security infrastructure | Security infrastructure such as CCTV cameras, lightning arrestors, and lighting (solar) supports surveillance and timely response to hazard risks. |

| Fire safety equipment | Firefighting measures, including extinguishers, hydrant systems, water pumps and a fire tender, depending on storage location and size, prevent fire spread in case of ignition. |

| Weighbridge | A weighbridge is crucial to measure the feedstock quantity procured, and moisture content levels. |

| Storage perimeter | A boundary wall or fencing protects the storage facility from unknown sources of contact, and serves as a security measure. |

| Source: Authors' compilation | |

Under the State Policy for Biofuels, the Punjab government has set targets to meet 20 per cent of the state’s overall fuel demand through biofuels by 2035 (ChiniMandi 2025). Currently, the state has projected to use over six million tonnes (~30 per cent of total) of paddy straw for fuel, power, and manure production. From our surveyed sites, only 15–30 per cent of the feedstock is kept on industrial land, whereas the remaining 70–85 per cent is kept out on leased land. Our estimation indicates that over 4,200 (rectangular bales) to 5,580 (round bales) acres are sufficient for 6 MMT paddy straw, if stored optimally. To put this into context, this is 7–30 per cent lower compared to the assumed 6,000 acres, using the thumb rule of 10 acres for 10,000 tonnes of biomass.

The minimum infrastructure required in setting up safe storage for 6 MMT of paddy straw on leased land would require INR 150–240 crore (USD 17–23 million) as shown in figure ES4. This will translate to an initial storage cost of INR 250 per tonne for rectangular bales and INR 400 per tonne for round bales. This outlay can be shared between public and private institutions which can recoup the initial investment within three years, if facing more than a 15 per cent feedstock loss. This investment will support creating a robust biomass supply chain and generate 3,500–5,500 direct semi-skilled rural jobs in feedstock collection, transport and management.

Figure ES4. An initial cost of INR 250–400/tonne is required to store 10,000 tonnes of bales on leased land

Figure ES5. A model storage layout for storing 10,000 tonnes of paddy straw bales on leased land

We recommend the following measures to support key infrastructure establishment for effective biomass storage:

As the world’s fastest-growing economy and third-largest energy consumer, India is prioritising bioenergy as a key component of its energy transition, which is expected to grow up to 45 per cent by 2030 (IEA 2025; MoPNG 2023). India’s push has been reflected in launching the Global Biofuel Alliance under its G20 presidency, and in its mandated blending obligation targets (Figure 1) (MoPNG 2024). The scaling of bioenergy production aims to meet the dual objectives of reducing fossil fuel dependence and agricultural residue burning.

By channelling crop residue for biofuel production, India can leverage an estimated surplus of 228 million tonnes of biomass from an annual output of 750 million tonnes (MNRE 2024). Punjab, Uttar Pradesh, Maharashtra, Gujarat, and Madhya Pradesh generate more than 20 million tonnes of surplus crop residue annually (National Institute of Bio Energy n.d.). The locally produced biomass-derived fuels will also result in foreign exchange savings as they reduce fossil fuel import dependence and generate rural jobs (MoPNG 2024). The byproducts of bioenergy, such as fermented organic manure, also help rejuvenate soil health and increase crop productivity, providing environmental benefits.

Figure 1. India’s ambitious targets to be a bioenergy leader

20% ethanol blending in petrol by 2025-26

7% co-firing in solid biomass coal power plants by 2026

5% compressed biogas (CBG) blending in CNG/PNG by 2028-29

2% sustainable aviation fuel (SAF) blending target by 2028

5% blending of biodiesel in diesel by 2030

Source: Authors' compilation

Since 2018, the Indian government has promoted various in-situ (mulching residue back into the soil) and ex-situ (value-added utilisation) management methods under the Crop Residue Management (CRM) scheme (MoAFW 2018). The push for ex-situ management has been coupled with the push for national bioenergy targets, realising the potential of lignocellulosic biomass, especially paddy straw. It is known as a valuable feedstock, having high lignin and cellulosic content, high calorific value, and is found in abundance, accounting for 18 per cent of the total surplus residue in India (National Institute of Bio Energy n.d.). While ex-situ management has gained traction in recent years, to fully utilise the potential of paddy straw, the supply chain needs a strong foundation (Kurinji and Kumar 2021).

Punjab, an agrarian state, has been tackling crop residue burning as it generates 21 million tonnes of residue annually. Paddy straw has significant potential for utilisation as a feedstock due to its lignocellulosic properties and abundant supply (Belal 2013). Currently, almost half of Punjab farmers burn paddy straw completely or partially to save money, control pests and prepare land for the next crop (Kemanth, Singh and Ignatious 2024). Beyond particulate matter emission, burning of paddy straw releases 70 per cent of the carbon in the straw as carbon dioxide, 7 per cent as carbon monoxide, and 0.66 per cent as methane (Kadian et al 2024). Exposure to intense crop residue burning increases the risk of acute respiratory problems threefold (Chakrabarti et al. 2019).

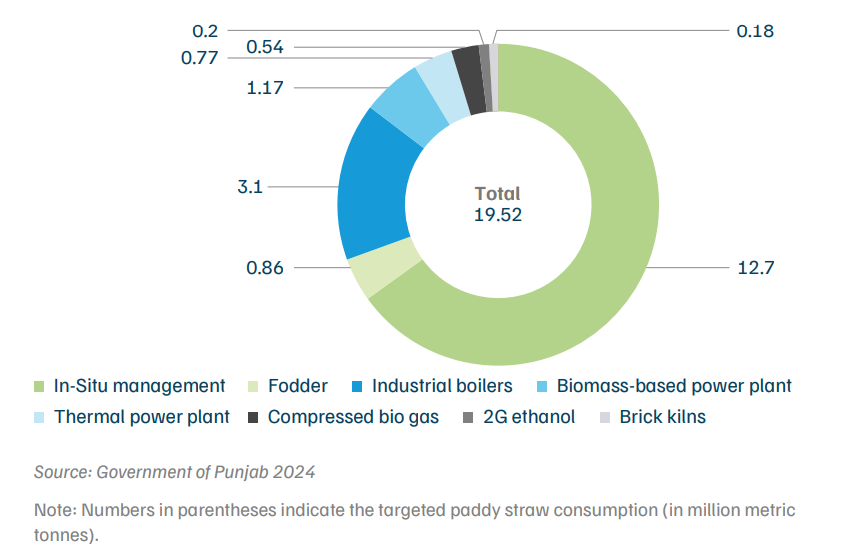

Responding to this, the Union and the Punjab governments have designed subsidies for farmers and incentives for the industrial use of paddy straw. Over six million tonnes of paddy stubble (out of 20 million tonnes generated annually) are targeted to be used in industrial boilers, compressed biogas, 2G ethanol, biomass power plants, and pelletisation plants (Figure 2) (Government of Punjab 2024). However, the sector is witnessing slow progress towards meeting targets due to supply chain bottlenecks, seasonality issues, and technology reliability.

Figure 2. About 6 million metric tonnes of paddy straw was targeted under ex-situ CRM in Punjab in 2025

The demand for paddy straw is increasing as more industries realise the profit potential of the various bioenergy production technologies, thereby reducing the amount of surplus residue burnt (ICAR 2021). For instance, in Punjab, only six CBG plants are currently functional out of the 78 that have been commissioned. The number of pelletisation plants operational has increased to 18 with a utilisation capacity of three lakh tonnes of stubble annually (Anju Agnihotri Chaba 2024). Besides, the Punjab government has set aside INR 60 crore in 2025 for industries to transition or set up new biomass-based boilers to generate further demand for crop residue (PTI 2025). However, a robust supply chain is critical to increase industry participation and meet the rising demand for stubble.

Global studies highlight that storage conditions for lignocellulosic biomass (Wendt 2020), such as paddy straw, are an important parameter to consider while designing a straw collection system for industrial applications to ensure a continuous feedstock supply (Kadam et al. 2000). Factors like poor feedstock quality (due to factors like moisture content, temperature etc) and seasonal availability (Blunk et al. 2003) lead to compositional changes, dry matter loss, and fire risks (Kadam 2010). The financial viability of capital intensive bioenergy industries requires a smooth operational process which, in turn, is reliant on the quality of the feedstock.

As India pushes to increase its bioenergy production, the demand for biomass is set to grow, necessitating the need for more extensive storage infrastructure requirements to ensure a reliable supply chain. Given the seasonal nature of biomass collection during the harvest season, industries must collect and store for year-round consumption, while maintaining the quality of the feedstock, to operate at maximum capacity. As depicted in Figure 3, the current set of schemes only assists in baling, collection, and utilisation of biomass. A critical gap that needs to be bridged between the biomass supply side and end-user requirements is biomass storage.

Figure 3. Storage requires policy attention in the biomass supply chain

Our initial interaction with companies reported an annual loss of 10–20 per cent of paddy straw due to improper storage, with bales commonly left uncovered and stacked in open fields. Due to inadequate storage sheds, tarpaulin covers, limited health and fire safety standards, and the absence of uniform stacking configurations, paddy straw is prone to degradation.

We aim to bridge the aforementioned gap by identifying factors affecting biomass storage in Punjab, and proposing recommendations to enhance the existing and forthcoming biomass storage infrastructure. The objectives of the study were to:

Through this study, we aim to inform stakeholders, including policymakers, industry players, and village-level entrepreneurs (VLEs) about actionable insights on how to develop biomass storage infrastructure.

We structure the report as follows: Section 2 describes the study’s approach. Section 3 discusses the literature review and the gaps in the Indian context. Sections 4, 5, 6, and 7 are the report’s main findings, which we categorise into four sections: feedstock collection and handling; feedstock quality; storage infrastructure; and operations and maintenance. Section 8 will outline a model storage depot, detailing infrastructure and financial requirements. Section 9 provides recommendations for industries and policymakers to establish guidelines for storage to strengthen the paddy straw supply chain.

We followed a mixed methods approach for this study. First, we conducted a systematic literature review to understand the existing policies and practices regarding biomass (particularly paddy straw) storage methods globally. This review helped identify factors affecting biomass storage, which were used to develop a semi-structured questionnaire. The questionnaire explored storage depot managers’ decisions regarding feedstock quality, collection, handling, infrastructure, and operation and maintenance. Additionally, some questions were themed around the investments made and challenges encountered during the biomass supply chain.

To ensure the questionnaire was grounded in practical insights, we conducted 15 telephonic pilot interviews with stakeholders, such as VLEs and industry representatives from six districts in Punjab and Haryana.

Following this, we visited and conducted in-depth interviews with the store managers and employees of eight major paddy straw utilising companies, with capacities between 30,000 and 2,30,000 MT in Punjab, between October and November 2024 (Figure 4). In our field visits, we covered all the primary biomass utilisation industries, including biomass power plants, compressed biogas (CBG) plants, pellet and briquette manufacturers, and biomassbased industrial boilers. We also correlated the data based on the responses calculated, and had multiple government and industry stakeholder consultations to validate findings.

Figure 4. We visited the storage facilities of eight different industries in Punjab

The accuracy of the study is limited by certain constraints in this study -

We reviewed the existing literature on lignocellulosic biomass storage found globally and in India. Our two objectives for the literature review were: a) To explore studies on the factors that impact feedstock quality and storage practices; and b) To find if there are studies on lignocellulosic biomass storage in the Indian context.

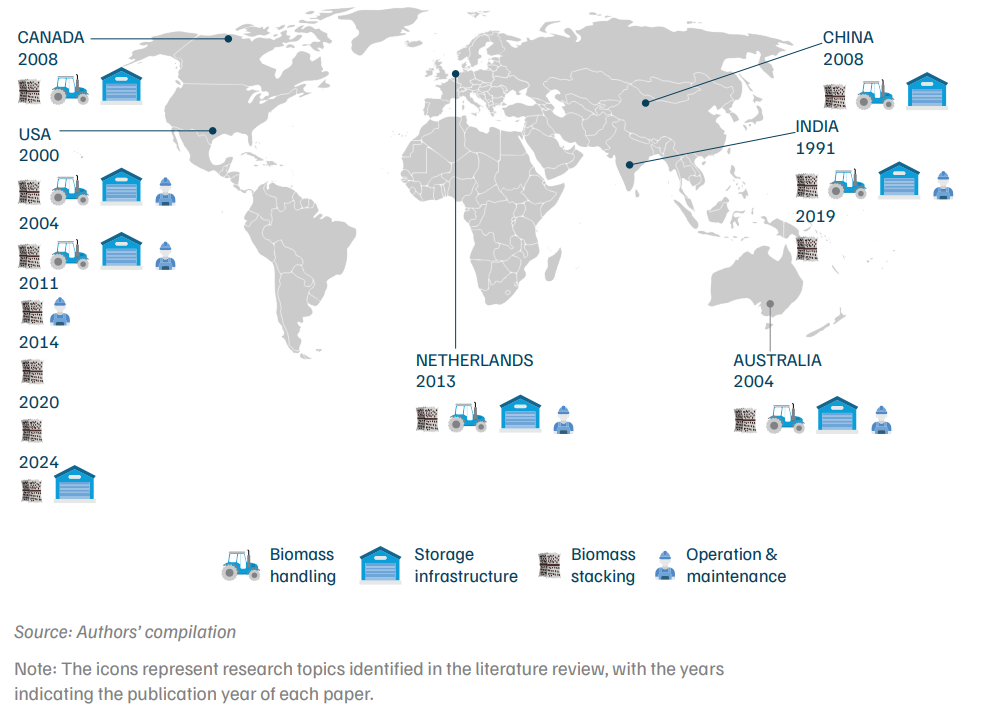

From our literature review, we found that most studies on lignocellulosic biomass storage are from the Western world, especially from the United States and Europe. Studies in the United States are based on corn stover, the primary lignocellulosic agricultural residue, which is also stored in the form of bales for long-term use (Graham et al. 2007).

Biomass supply chain design studies encompass the storage process as an operational and tactical decision while designing a straw collection system (Sharma et al. 2013). Feedstock storage and storage losses are accounted for while calculating the total cost to deliver feedstock for bioenergy production (Thorsell et al. 2004). Uncontrolled biomass loss occurs due to microbial degradation, due to higher moisture content found to be common in studies when storage conditions are not optimised (Wendt 2020). For instance, the US Department of Energy studied the collection, storage, and transportation of corn stover in 2003 (Atchison and Hettenhaus 2004). The study indicated that more than 25 per cent of total corn stover biomass weight loss occurs in one season when bales are kept without cover and affected by wet weather. A study in Mississippi, USA, found that moisture above 30 per cent can sustain high temperatures for up to 40 days in the bales. In addition, chemical degradation becomes dominant when the bale temperature exceeds 50°C (Lemus 2009).

Research on rice straw in California suggests that baled straw with a moisture content above 25 per cent results in fermentation and dry matter loss, with risks of spontaneous combustion in stacks (Kadam, Forrest and Jacobson 2000). The loss is caused by aerobic organisms consuming available carbohydrates in biomass in the presence of oxygen, which increases with more moisture (Darr and Shah 2012). A higher moisture content also increases methane emissions from lignocellulosic biomass storage as anaerobic digestion takes place (UNFCC 2014), although more accurate estimate studies are needed for the Indian context.

Bale properties like density, surface area, porosity, and homogeneity influence the degradation rate during storage (Ball et al. n.d.). Losses also occur due to the quality of storage infrastructure, with research discussing the various types of storage, permanent structure, tarped cover, and open storage and their loss impact (Davis 2016). Losses were low in bales stored indoors, under permanent cover, or tarped, and open stacks incur higher overall quality losses, requiring the disposal of straw (Blunk et al. 2003). The International Energy Agency (IEA) study in 2013 examined health and safety aspects of biomass storage, transport and feeding, highlighting safety measures, such as rodent control, alarm systems, and smoke and gas detectors (Koppejan et al. 2013). Countries such as the United Kingdom and the United States have provided guidelines outlining the dos and don’ts for bale storage (HSE 2012). While this study is important to identify the parameters for safe biomass storage, the Western context for losses incurred and the storage method have limited replicability for India due to the differences in weather conditions.

We observed limited research on biomass storage in the south Asian context (Figure 5). In India, a single paper on biomass storage research dates back to 1991. It stresses uniform bale stacking and key storage infrastructure requirements to minimise losses (Bansal and Singhal 1991). However, a research gap was identified as no further studies were done on biomass (feedstock) storage in India. In China, studies on the physio-chemical properties of paddy straw as a lignocellulosic feedstock for biofuel production gained attention in 2012 (Chiueh et al. 2012). However, these studies primarily focus on feedstock characteristics rather than safety and investment requirements for storage infrastructure. Thus, there remains a research gap in addressing lignocellulosic biomass storage, especially for paddy straw bales in the Indian context.

Figure 5. Research gap in addressing biomass storage in India versus the rest of the world

On a positive note, India’s policy framework has offered an ecosystem to support the setting up of biomass storage guidelines. The 2024 CRM operational guidelines aim to establish 333 collection centres in Punjab, aiming to collect 1.5 million tonnes of paddy straw (MoAFW 2023). Yet, there is a lack of information on how the collection centres will be designed and located.

Previous policy examples can support setting up guidelines for biomass storage. Central Warehousing Corporations have issued storage guidelines for high value commodity such as cotton bales (BIS 2019) and for cotton and jute bales (Central Warehousing Corporation 2009). Similarly, the Bureau of Indian Standards has laid down fire safety code of practices at coal storage yards (BIS 2002). The National Dairy Development Board has also outlined quality measures in 2013 for storing cattle feed (Garg, Sherasia and Bhanderi 2013). Furthermore, warehousing policies exist, such e-Handbook on Warehousing Standards, released in 2022 (Warehousing Association of India 2022). These policies can serve as precedents for establishing guidelines for paddy straw and other biomass storage planned for biofuel production.

The literature review offered insights into the key factors that affect biomass loss while building and maintaining a biomass storage depot. The factors were mapped into four categories to dive deeper into how each factor affects storage, leading to the development of the questionnaire. Figure 6 shows the key factors categorised for the study.

Figure 6. Factors identified from existing literature affecting biomass storage

Source: Authors’ compilation

The annexure provides detailed information on these factors and the corresponding research questions. The following sections detail the findings in order of the categorisations identified above from the eight companies we visited in Punjab.

In this section, we discuss how the collection process of paddy straw is carried out on the ground, and how it affects feedstock quality. Paddy straw collection is a resource-intensive process involving coordination among multiple stakeholders.

In Punjab, the Kharif harvest season is a short 15–20 day window in the months of October and November, as farmers clear land to sow for the next Rabi season. The collection begins with slashing the paddy straw, followed by drying, to reduce the moisture content. The stubble is then arranged in rows using a rake to facilitate baling. Once baled, the biomass is loaded onto trolleys, transported to storage facilities, and unloaded into stacks for storage (Figure 3 in Section 1).

The collection process involves various supply chain actors with roles and levels of involvement depending on the firm’s operational model. While there is no one-size-fits-all approach, most companies prefer collecting within 15–20 km, as transportation beyond this entails a high delivered cost, which may not be viable for companies engaged in the supply chain (Kurinji and Kumar 2021).

Figure 7 summarises the three observed biomass supply chains from our visits, and the procurement costs associated with each. Additional research is required to evaluate the optimal collection system.

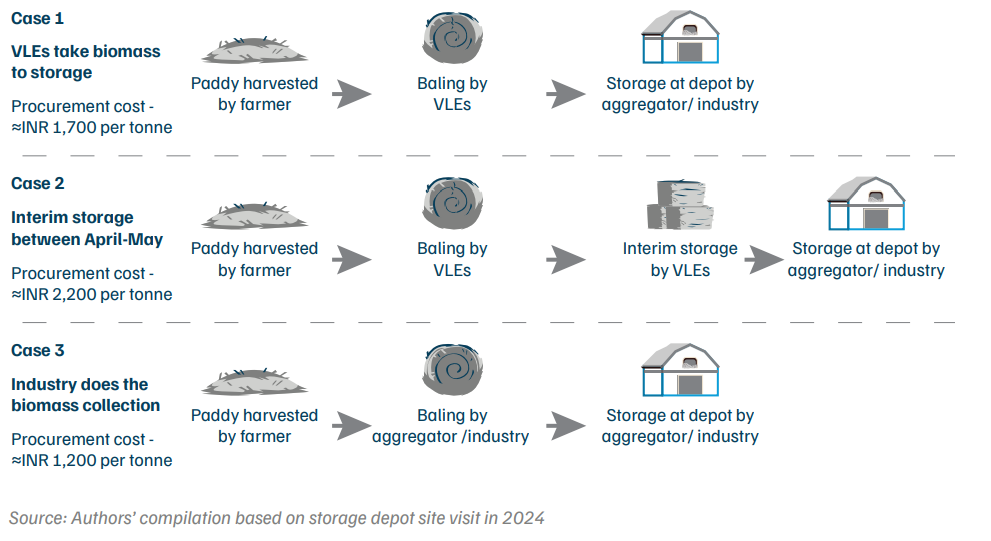

Figure 7. Three paddy straw collection and storage models followed in the ex-situ ecosystem

Case 1

In this scenario, farmers leave residue in the fields after harvesting, which is then collected by village-level entrepreneurs (VLEs)/aggregators using their own baling machines. Based on demand and experience, farmers/VLEs supply biomass directly to companies or aggregators. Companies may provide additional compensation for transportation costs, while VLEs handle transportation and loading/unloading.

Case 2

The VLEs, often farmers themselves, collect biomass and store it on their land until they sell it to aggregators or companies before the rainy season. This approach allows interim storage players to receive higher payments due to limited off-season paddy straw availability. However, interim storage poses higher risks due to a lack of safety infrastructure and potential feedstock losses.

Case 3

The paddy residue is collected directly by the company through contracted employees, and stored at company-managed storage depots. This approach centralises the company’s control of the collection and storage process, potentially reducing losses. The company manages all aspects of biomass handling, from collection to storage.

The feedstock collection method affects bale moisture per cent, impacting quality and industrial use. During our interviews, VLEs/biomass companies in Punjab reported that farmers are eager to clear fields quickly and become impatient with collection delays. Collection decisions, including the on-field drying period after cutting the straw and baling at a higher dew point during the day, affect moisture content and water retention in bales.

The current method of the baling process in Punjab by VLEs takes approximately three days, involving drying, raking, and baling. However, it was reported that weather conditions delay the drying of stubble during cloudy November days. Cloud cover reduces cut straw’s exposure to the sun, slowing the drying process. Dew formation, caused by colder nights, increases the stubble’s moisture content, even if it has undergone some drying during the day. This leads to baling machinery clogging and uneven bale density. Most of the surveyed companies recommended extending the drying period and baling process to a minimum of five days, giving the straw more time to dry, and reducing the moisture content once baled.

In Punjab, paddy straw is collected either in rectangular or round bales, with rectangular bales weighing between 15–30 kg and round bales ranging from 250–500 kg each. Six companies in our survey stored rectangular bales, while two stored round bales. Round and rectangular bales differ in machinery cost and the workforce required to load and unload. Based on the visits, the choice of bale shape is influenced by the collection method, costs, and storage land availability.

The cost of baling machinery for small rectangular bales (25–30kg) is lower than for large round bales (200–400 kg). For instance, small rectangular bale machinery ranges from INR 8.5 lakh to INR 18 lakh per machine. In contrast, round bale machinery costs from INR 21 lakh to INR 85 lakh per machine, depending on the capacity. Thus, small rectangular balers are more popular on the ground due to the lower capital required. Companies with a higher financial capacity are able to operate with round bale machinery. Companies say that large rectangular balers are not as common in India as round or small rectangular balers, due to a combination of factors including higher initial equipment costs, the need for expensive specialised handling equipment (like bale handlers and trucks), and the higher moisture sensitivity of large rectangular bales, particularly in humid climates like India.

Choice of bale shape (round or rectangular) also affects the number of personnel required during the storage process. Handling rectangular bales is slow and labour-intensive, as the loading and unloading is a manual process, whereas round bales use a mechanised system with loaders and telehandlers. Findings from the ground detailed that handling rectangular bales requires 5–8 workers (including the driver) to load and unload. Round bales only require 3–4 workers, as a telehandler operator and support staff are required.

Field observations in Punjab revealed feedstock costs are mainly influenced by supply and demand within viable transport distances, indicating logistical and economic factors, rather than bale shape characteristics like density and water retention. Additionally, rectangular bale collection is outsourced to VLEs at pre-determined rates, whereas round bales are collected by company employees for their own use, making cost comparison of round and rectangular bales challenging. There is currently no comprehensive study in India that explores how the shape of bales influences the biomass deterioration rate during storage.

Table 1. Comparison between rectangular (small) and round (large) bales

| Factors | Rectangular bale (small) | Round bale (large) |

|---|---|---|

| Machine Price (INR lakh) | 8.5–18 | 21–85 |

| Bale weight (kg) | 25–30 | 200–400 |

| Stacking method | Manual | Mechanised using a telehandler |

| Workforce required (number of staff per baler set*) | 5–8 | 3–4 |

| Land required (acres per 10,000 MT bales**) |

7 | 9.3 |

| Advantages |

|

|

| Disadvantages |

|

|

Source: Authors’ compilation from stakeholder consultation and secondary literature.

In this section, we discuss the feedstock quality required for utilisation, and quality characteristics measured on the ground. The required quality has an effect on both industry players (improving utilisation efficiency) and suppliers of the residue (receiving fair compensation)

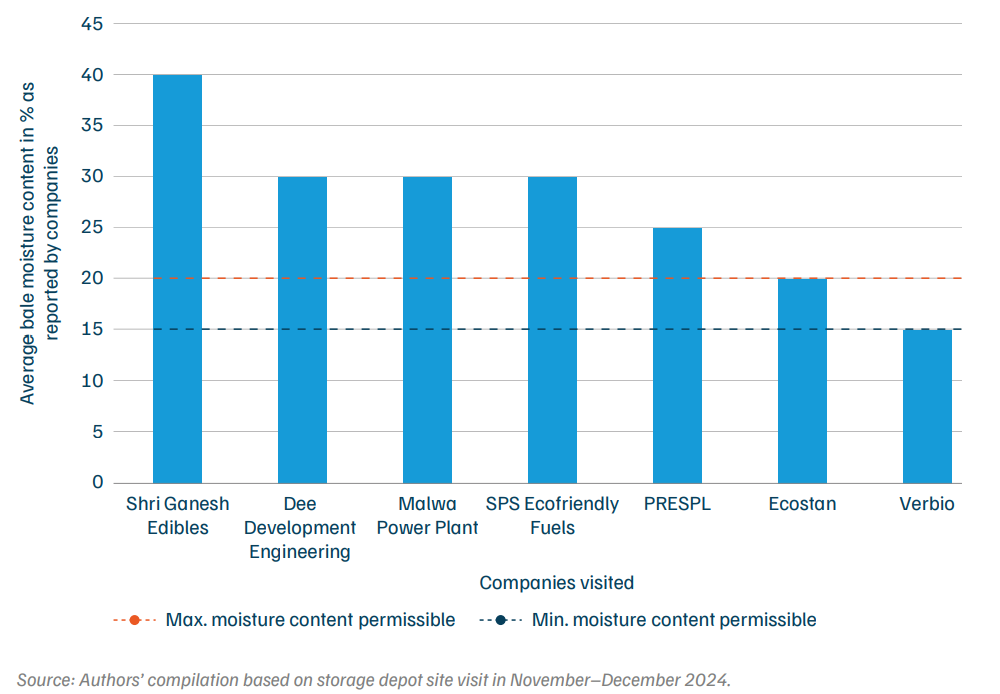

Our on-ground findings aligned with the literature, as companies cited higher moisture content as the primary driver for speeding bale degradation, keeping this quality parameter at utmost importance. Our conversations with companies and storage depot managers detailed that permissible moisture content for industrial processing is universally below 20 per cent, which is measured using a moisture meter. However, some firms reported receiving biomass with up to 40 per cent moisture above the threshold of 15–20 per cent due to unfavourable weather conditions and misaligned baling practices during feedstock collection (Figure 5). The two companies receiving bales with low moisture content reported collecting residue on their own and establishing clear protocols for VLEs to follow. During our discussions, it was constantly stressed that the moisture content at the beginning of the process, the baling stage, should be low (15–20 per cent) to reduce the quality degradation during storage.

In order to ensure receipt of quality feedstock, three of the eight sites reported making payment cuts if moisture content exceeded 25 per cent, applying a 1 per cent reduction in price for every percentage point above the threshold—for example, bales collected at 30 per cent incurred a 5 per cent payment cut. This was set to push balers to provide feedstock at the preferred moisture content. It can be noted that the moisture level, even with payment cuts, is higher than the industry requirement, and can lead to self-heating cases in newly stacked biomass.

Figure 8. Moisture content in collected bales often exceeds the industry’s permissible limits

Source: Authors’ compilation based on storage depot site visit in November–December 2024.

Note: Average bale moisture content values, measured using a moisture meter, were self-reported by companies during interviews.

Consequently, there were other factors described as affecting feedstock quality, besides moisture content, such as bale temperature due to high moisture content. The spoiled bales also affect the gross calorific value (GCV), which is an important factor for biomass power plants and industrial boilers, leading to lower combustion efficiency. The reported difference in GCV value by these players was 300–400 between low and high moisture bales. During our visits, the degradation was visible through bale discolouration and unpleasant odours. Additionally, broken twine from mishandling bales during transport and stacking leads to unbundling, which results in losses.

Infrastructure at storage depots is a precautionary measure for feedstock to be preserved for a longer duration. While there is no guarantee of it being safe appropriate infrastructure helps keep the feedstock intact and be prepared for any kind of fire or safety incident.

This section will discuss the types of storage depots observed, and the physical infrastructure found in our ground visits.

Storage methods employed by industry developers are predicated upon their own experiences or insights from peers. Field observations suggest a general guideline of 1,000– 1,200 tonnes of paddy straw stored per acre of land. Current practices follow two primary storage types: open and semi-open. Open storage involves bales kept outdoors, typically in interim storage or leased land areas, with limited infrastructure and safety provisions, thereby entailing a greater risk of loss. Conversely, semi-open storage is characterised by its longterm nature, owing to its strategic placement on land within or adjacent to industrial facilities. This method offers enhanced protection through the use of sheds to mitigate losses, and incorporates built-in infrastructure and safety measures.

Among the eight surveyed companies, all but one leased land for storage. The exception only stored bales on its own land. Industry developers prefer the leased land to be adjacent to the company, to ensure transport efficiency and reduce operational costs. Four out of the eight companies leased land for storage within a 10-km radius, in addition to the land leased adjacent to the factory site. The land selected is required to have easy road access for trolley transportation.

However, it is challenging to lease land due to land ownership and lease duration. Farm land is usually leased, with farmers having concerns over agricultural productivity post-lease tenure. Vehicle movement at storage depots leads to soil compaction, requiring time and resources to restore agricultural use. For example, Verbio India Pvt Ltd requires a minimum lease term of three years to justify the economic cost of setting up infrastructure and safety measures. Our survey indicates annual rental rates vary depending on location, from INR 60,000 to INR 1 lakh per acre, with most agreements having an annual rental increment of 5–10 per cent. As a result, industries limit infrastructure development due to land longevity.

Besides location and land ownership, the companies also highlighted other factors for selecting appropriate land for storage. New storage sites require levelling of land, in case of uneven land provided. The level surface allows for uniform stacking, reducing the risk of structural collapse. Subsequently, drainage lines and raised platforms are laid to minimise water retention at the base of the stack. Most companies cited doing minimal land preparation for leased land storage. Existing land preparation includes removing the degraded bales from the season, and cleaning the land if previously used for storage.

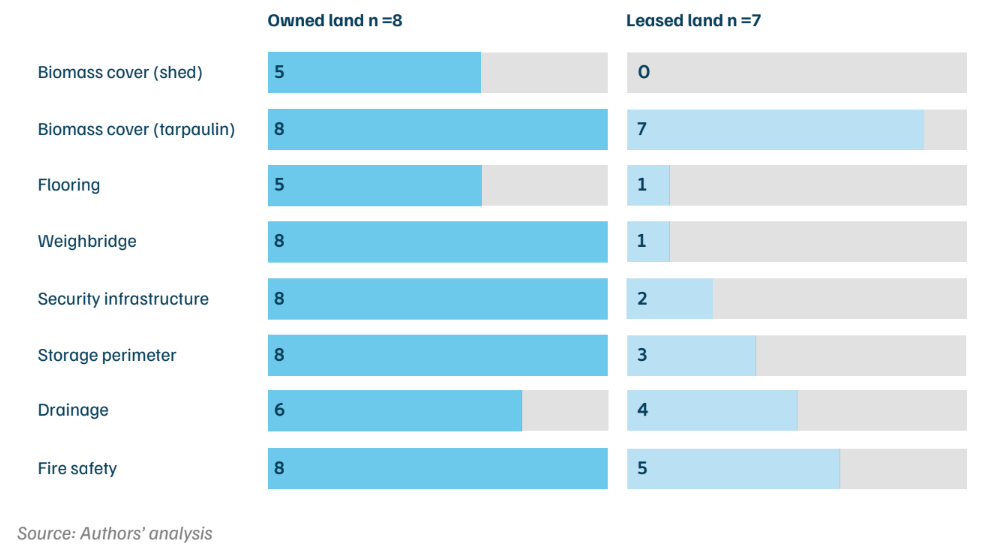

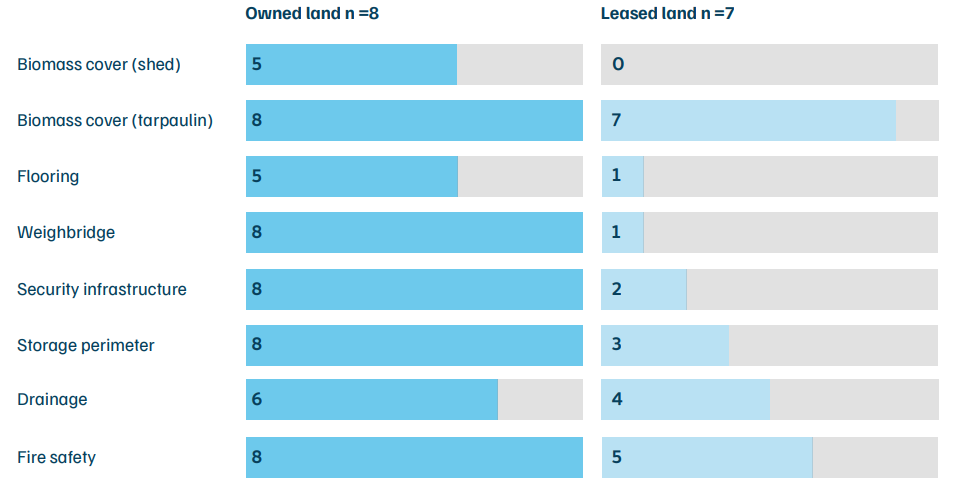

Research highlights the need for infrastructure at the depot to prevent or reduce biomass losses and hazard risk. These measures include tarpaulins and sheds to cover biomass, flooring and drainage systems to avoid waterlogging, and boundary walls to prevent unidentified fire risks. This section details the infrastructure observed in leased and company owned land, and its importance to industry players. Of the eight industries visited, seven had both company owned and leased land, whereas one only stored on own land. The infrastructure found on leased and owned land storage areas is summarised in Figure 9.

Figure 9. More physical infrastructure was established on industries’ own land

Source: Authors’ compilation.

Note: While seven surveyed companies stored paddy straw on both leased and owned land, one stored only in its own land. Typically, tarpaulin is used as biomass cover on leased land, while owned land had both shed and tarpaulin.

Biomass cover (shed and tarpaulin)

Biomass stacks need to be covered to prevent external factors from touching feedstock susceptible to microbial degradation and loss. Stacks were found to be covered either by a shed (only found on industrial land) or tarpaulin sheets. Five out of eight companies used sheds located on factory owned land. Although sheds have higher upfront costs, their durability and placement offer better protection than tarpaulins. Some companies observed pre-processing machines like conveyors and shredders housed under the same shed.

The covering of stacks with tarpaulin usually happens later, as freshly baled straw has high moisture content, which can trap heat, leading to self-heating and fire risk, requiring ventilation to dry. While all respondents confirmed using tarpaulin to cover stacks, the time and method for covering stacks differed due to workforce capacity, convenience, and unpredictable weather. Five out of eight companies reported starting to cover all the stacks by April or May, just before the rainy season, whereas the others only applied the measure when required, saving material and workforce costs. Tarping involves covering stacks with different GSM polyethylene sheets, and ropes over the stacks to keep the sheets secure. The job of tarping rectangular bale stacks was reported to be challenging and time consuming, as they are 15–20 feet high. All industries reported different tarping methods, with some covering it fully from the top of the stack to the ground, and some only covering the top rows.

Drainage

Proper drainage is essential for maintaining feedstock quality and allowing water runoff at the base level of the stacks. Half the respondents had a temporary form of drainage on leased land, whereas six of the 8 companies had proper drainage on owned land. On leased land, developers, after land-levelling, line drains around the perimeter to avoid waterlogging at storage depots. Natural slopes often assist in drainage, but the absence of paving results in localised waterlogging at the site, which was visible during our visit. Some developers deployed water pumps at the end of the season to drain accumulated water. In contrast, land owned by companies had proper drainage systems along the periphery of their depots, effectively managing runoff in the event of rain.

Flooring

Without a base platform, the bottom layer of the stack deteriorates due to moisture absorption from the ground. Industries agreed that flooring is important, and a sloping stacking platform is ideal. Factory sites which had sheds had a raised stack platform, averaging 1–1.5 feet above ground level, keeping the structure of the stack intact. However, only Verbio India Pvt Ltd reported having a raised concrete stacking platform for 1.5 ft on owned land outside the shed area. No stack platform was observed on leased land, with stacks either having a base platform of a tarpaulin sheet or degraded biomass. Waterlogging was sighted at the leased site, which caused the first row of stacks to be degraded, visible in the image below. Our calculations indicate biomass loss from the base layer is 3 per cent and 5 per cent of the total stack stored for rectangular and round bales, respectively, though losses may vary based on specific storage conditions.

Security infrastructure

Security infrastructure ensures timely responses to any kind of hazard risk. Security infrastructure entails having CCTV cameras, lightning arrestors, and safe lighting. Overall, storage on the companies’ own land had all security provisions due to the industrial process being there. However, limited security infrastructure was seen on leased land (two of the seven sites). On leased land, CCTV cameras for surveillance are absent due to the absence of poles or structures to install cameras. This leads to alternatives like reliance on patrolling by security guards. The practice for lighting is positioned along depot boundaries rather than inside storage areas, to avoid high-tension (HT) power lines that might generate sparks.

Proximity to HT lines was observed at two leased sites. While warehousing standards recommend maintaining a safe distance from HT lines, challenges in securing land for biomass storage overlook some factors (Punjab Government Gazette 2021). While the Union government has included lightning arrestor provisions in the Crop Residue Management Guidelines, we found that the on-ground lightning arrestor requirement is higher than the one lightning arrestor for 4,500 tonnes of paddy straw storage specified in the guidelines (MoAFW 2024).

Fire safety equipment

The hazard response at biomass depots focuses primarily on preventing fire spread in case of ignition, as storage personnel noted that containing stack fires can be extremely challenging. While firefighting provisions exist, the emphasis remains on surveillance to detect fire sources and fires early. Developers limit firefighting measures at leased depots (five of seven surveyed sites) to mainly fire buckets and extinguishers, due to reasons listed in section 6.1. In contrast, storage sites located within all surveyed industrial sites had firefighting provisions; for example, having a shared fire hydrant system between industry and depot along the facility’s perimeter, or having a dedicated fire tender in the company.

The National Building Code of India and state-specific regulations mandate a minimum clearance of 20 feet around buildings and storage stacks to ensure there is space for fire tenders without any obstruction (Government of Punjab 2021). As per fire safety guidelines, hydrants are to be strategically planned within a maximum spacing of 100 feet. Each hydrant must be connected to a reliable water supply, capable of delivering a minimum pressure of 3.5 kg/cm², as recommended by the National Building Council (NBC 2016).

Weighbridge

All eight storage facilities within the industrial land had a weighbridge present, which is a crucial part in monitoring and quantifying the feedstock procured. However, due to limitations on infrastructure development on leased land, only two of them had a weighbridge. Respondents highlighted that a weighbridge should be a standard at a storage facility, as it is the primary tool to check the weight and moisture-content levels. Industries had varying types of weighbridges, either over the top or under the road, with some having additional digital features.

Storage perimeter

Hazard prevention at storage sites hinges on reducing fire sources and surveillance infrastructure to mitigate fire risks. Research indicates that while self-ignition of bales is common, biomass is highly susceptible to fire hazards from external ignition sources like lightning, spark from vehicles, short circuit in electrical lines, etc. (Koppejan et al. 2013). Consequently, most company storage sites employ a boundary wall to minimise these risks. However, none of the leased storage depots we surveyed had fences, and in fact, five depot managers reported fire incidents in the past, with four citing unknown ignition sources.1

This section discusses the challenges encountered during the day to day operations of a storage site, the subsequent losses that occur and the strategies employed to maintain it.

The biomass stacking process varies depending on the shape of bales, and who carries out the activity (VLEs, aggregators, outsourced personnel). As discussed earlier, round bales require less workforce for stacking due to mechanical handling, whereas rectangular bales require a larger workforce. All of the surveyed companies had their own stacking practices based on operational experience with differentiating measurements; for example, stack length/width and distance between stacks. Our interviews and field visits find that stack lengths ranged from 50 to 120 feet, and widths from 50 to 80 feet, depending on land layout. The reported stack gap (distance between two stacks) was between 15 to 25 feet.

Companies storing rectangular bales emphasised the importance of uniform stacking. This practice reduces the risk of bales toppling over, and minimises water retention in the stacks, preserving the quality of the stored paddy straw. However, there were challenges reported, as stacking personnel often lack motivation and understanding of storage requirements. Moreover, only verbal instructions are provided for biomass stacking, loading, and unloading, not formal training. This gap arises from temporary employment during the narrow harvesting window. As a result, inconsistencies persist in stacking practices and understanding of storage protocols.

A part of the feedstock cannot be used at the end of every season, as the paddy straw is prone to degradation over time. All of the respondents faced feedstock losses ranging from 15 per cent all the way up to 25 per cent per annum—with one being an outlier, only recording 1–3 per cent loss. It was also stated that usually, the bottom layer of the stack is discarded as water seeps through during the rainy season, making it unsuitable. Our internal calculations also suggest that one layer of the stack accounts for 3–5 per cent of the whole stack.

Annually, fresh bales are procured, which are required to be kept after land cleaning and preparation steps, as discussed in Section 6.1. With no standardised method of discarding bales, industries take up the initiative by themselves. Our on-ground discussions found that the industries dump the spoiled bales in a designated area, mulch them back, compost or provide them back to the industries. The growing pile of waste bales is a safety concern and a logistical issue, as they occupy valuable space that could otherwise be used for fresh feedstock. This practice creates a risk-prone situation, as the new bale stacks are placed close to discarded ones, leaving them open to possible contamination and prolonged anaerobic digestion, leading to methane emissions. Additionally, the scattered bales fall over the open space designated for vehicular movement, affecting day-to-day operations and the quality of roads.

It is important to note that the losses are not measured or recorded, but they were communicated verbally during interviews.

During our site interactions, five facilities reported fire incidents within their operative years (all on leased land), highlighting a recurring issue. Fires in bale stacks, for instance, are intense and can burn for extended periods, spreading rapidly throughout the stack. While a gap of 15–20 feet is currently maintained between stacks to minimise the risk of fire spreading, this measure alone is insufficient to ensure comprehensive fire safety. A concern raised by respondents was the accessibility of firefighting infrastructure, particularly in remote industrial areas. Many industries reported that fire brigades take time to reach their facilities in case of a fire, further damaging the feedstock. To address this, respondents suggested that fire tenders or planned fire brigade depots should be strategically located near industrial clusters. This would reduce response time and improve the effectiveness of firefighting.

Bales, being a primary feedstock in specific industries, make it a valuable and necessary commodity required to be insured. However, industries often find it difficult to avail of insurance as provisions are not readily available or coupled. In the survey, six out of eight industries had insurance on the feedstock, but three of them faced challenges in renewing it when a fire incident had occurred. The survey revealed that obtaining insurance for paddy straw bales is particularly challenging, unless the storage site is located within the company’s premises. Insurers are reluctant to provide coverage for leased storage sites due to perceived higher risks of any future fire/hazard incident. Additionally, insurers have certain conditions, such as the presence of boundary wall fencing and specific fire safety measures, which necessitate higher capital expenditure for setting up leased land. However, there is a lack of clarity regarding the exact documentation and requirements set by insurers, leaving companies uncertain about how to meet these standards and build compliant storage facilities.

We also accessed information on insurance for paddy biomass by contacting two insurance companies. However, we found that the requirements were unclear, and were informed that they can change on a case-by-case basis.

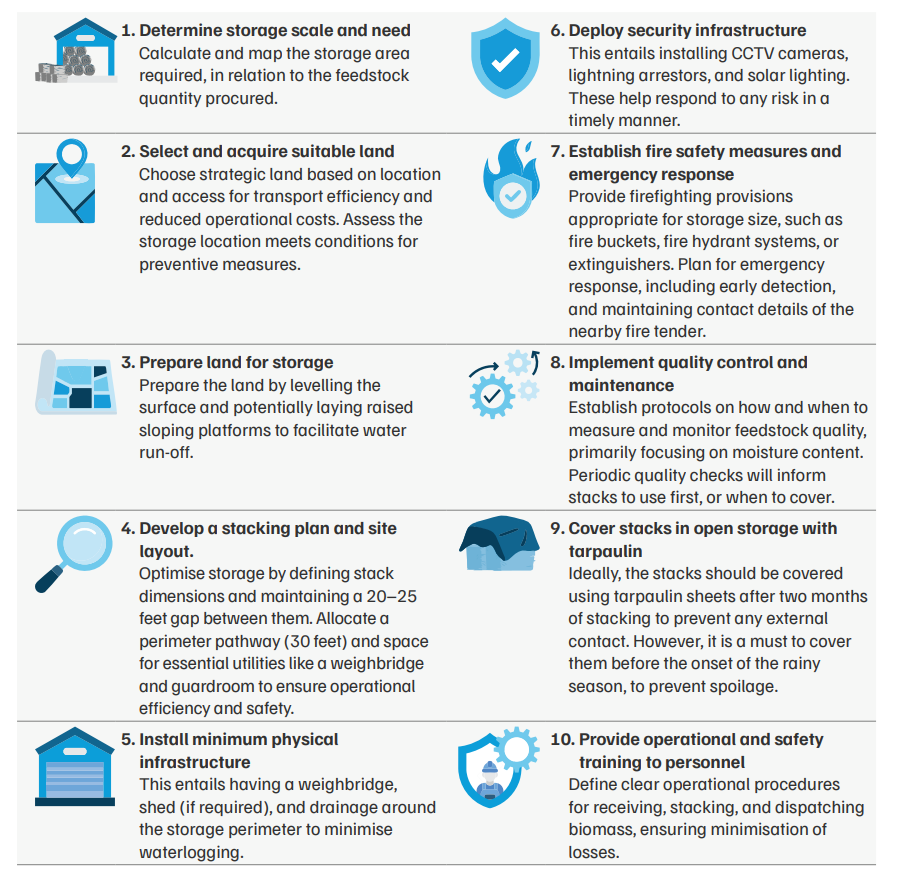

Figure 10. A 10-point checklist for industries planning to invest in paddy straw storage

Source: Authors’ analysis

We took on the exercise of outlining a model layout outside company owned land, as the majority of the annual feedstock required is kept outside. The model layout and calculations below are all for a capacity of 10,000 tonnes of paddy straw bale storage. From our surveyed sites, only 15–30 per cent of the feedstock is kept on industrial land, whereas the remaining 70–85 per cent is kept out on leased land. Due to land-related constraints and the perceived risks described earlier, we found that all storage facilities on leased land missed at least one of the seven key infrastructures identified to be deployed at a site. This section lays out a model storage facility, with insights from literature, ground findings, and satellite imagery analysis.

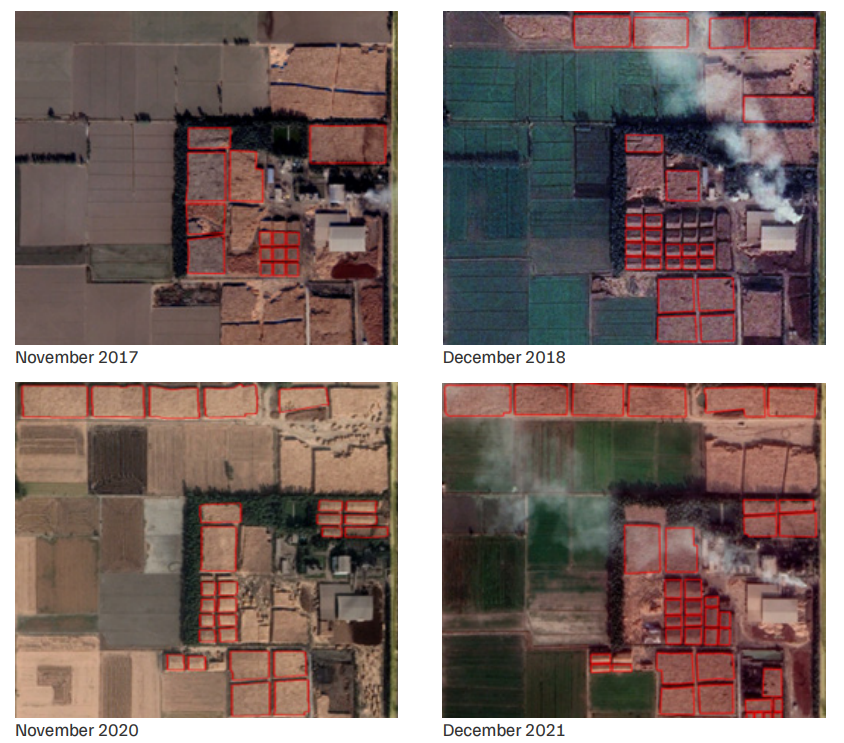

In discussions with depot managers and aggregators, it was suggested that the ground rule followed is 10–15 acres can accommodate up to 10,000–15,000 tonnes (one acre for 1,000 tonnes) of paddy residue. Satellite images taken from Google Earth Pro were analysed to identify the storage depot layout and observe the sizes of stacks and their distribution across different storage depots.

Figure 11. Different stacking practices employed over multiple years at a storage site

Source: Authors’ compilation

Note: Satellite images accessed via Google Earth Pro (January 2025). Red outlines mark paddy straw bales arranged in small, medium, and large stacks.

From the satellite observations, it was evident that stack sizes varied, for which we categorised stacks into three configurations—small, medium, and large—based on a timeseries analysis. The configurations for rectangular bales are: small stacks are 400 sq ft (50 x 80 ft), medium stacks are 1,600 sq ft (80 x 80 ft), and large stacks are 10,000 sq ft (125 x 80 ft). For round bales, the configurations are: small stacks are 3,600 sq ft (100 x 36 ft), medium stacks are 7,200 sq ft (200 x 36 ft), and large stacks are 10,800 sq ft (300 x 36 ft).

Following the satellite analysis, two Excel tools (one for each shape) were developed to calculate the storage area based on the area allocated for stacking and utilities (area for vehicular movement, a guard room, and a weighbridge are allocated). The tool also incorporates spacing between the stacks of 25 feet, and a perimeter pathway of 30 feet. The calculator for rectangular and round bales assumes each depot follows a single-bale storage type. While the calculator presents a stack matrix format, this layout is not a fixed rule, depending on site-specific conditions, land availability, and operational preferences. A spoilage factor is also included to realise the potential losses incurred in the future.

Table 2. An example of a calculator for estimating land required to store rectangular bales

| Targets | B. Bale parameters | ||

|---|---|---|---|

| Target biomass (MT) | 10,000 | Bale length (ft) | 2.25 |

| Target biomass in (kg) | 1,00,00,000 | Bale width (ft) | 1.5 |

| Target area (acres) | 10 | Bale height (ft) | 1.25 |

| Maximum stack height (ft) | 15 | Bale weight (kg) | 25 |

| Stack spacing (ft) | 25 | ||

| Perimeter space (ft) | 30 | ||

| Utilities area (acres) | 0.2 |

| Parameters | Small stack | Medium stack | Large stack |

|---|---|---|---|

| Length (ft) | 50 | 80 | 125 |

| Width (ft) | 80 | 80 | 80 |

| Stack area (sq ft) | 4,000 | 6,400 | 10,000 |

| Bales per Layer | 1,116 | 1,838 | 2,625 |

| Total bales per Stack | 13,388 | 22,050 | 31,500 |

| Stack weight (kg) | 3,34,697.50 | 5,51,250 | 7,87,500 |

| Stack weight (MT) | 334.69 | 551.25 | 788 |

| Stack type | Percentage | Stacks needed | Matrix layout | Total area (sq ft) | Storage (MT) | Area (acres) |

|---|---|---|---|---|---|---|

| Small stacks | 30 | 9 | 3 | 91,000 | 3,012.19 | 2.09 |

| Medium stacks | 50 | 9 | 3 | 1,22,500 | 4,961.25 | 2.81 |

| Large stacks | 20 | 3 | 2 | 82,075 | 2,362.5 | 1.88 |

| Totals | 100 | 21 | 2,95,575 | 10,335.94 | 6.79 |

| Total area required (acres) | 7.0 | Area within limit ? | Yes |

| Total storage capacity (MT) | 10,335.94 | Storage target met ? | Yes |

| Biomass loss (%) | 5% | Net usable tonnage (MT) | 9,819.14 |

Source: Authors’ analysis; cells highlighted in grey can be modified to optimise the storage site

For both round and rectangular bale storage model depots, we assumed there were 10,000 tonnes to store. As seen in the above calculator, seven acres of land is required to store 10,000 tonnes of rectangular bales based on the stack configurations provided, saving 33 per cent in land required. The cells highlighted in green can be changed according to the land availability and developer choice, against the thumb rule of 10 acres for 10,000 tonnes.

For the round bale storage model depot, the same assumptions of quantity stored, stack spacing and perimeter spacing are taken into account. Round bales are stacked using a telehandler which has a reach of nine metres, essentially capping the stack height at 30 feet. The area required to store 10,000 tonnes is 8.30 acres, saving 17 per cent land required.

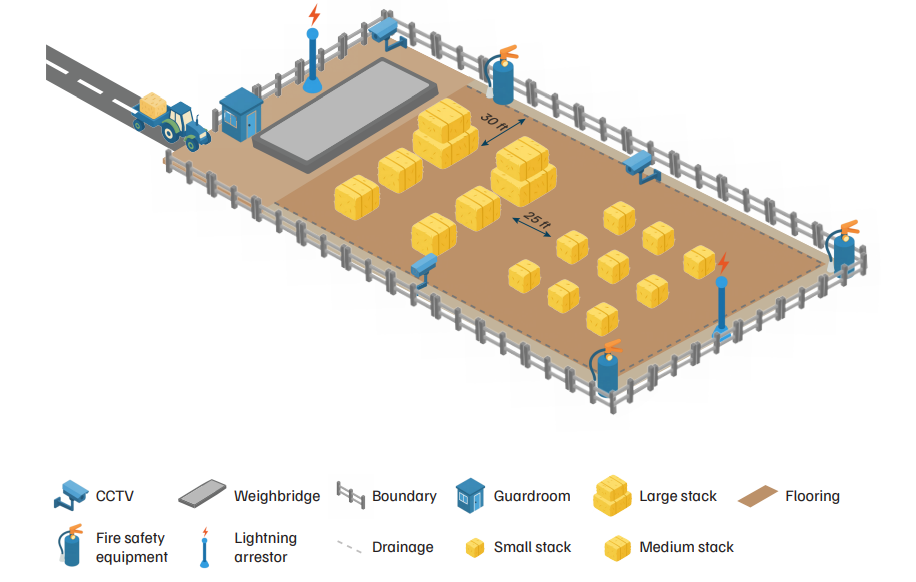

The model layout below showcases the minimum infrastructure required at a biomass storage facility. The layout is based on the assumption of storing 10,000 tonnes of paddy straw bales in a matrix format..

Figure 12. A model storage layout for storing 10,000 tonnes of paddy straw bales on leased land

Source: Authors’ analysis.

Note: The same layout with the required infrastructure can be used for round bales, with differences in stack shape (pyramid format) and larger land requirements.

To estimate the required investment, we have made the following assumptions based on the model storage layout in Figure 12:

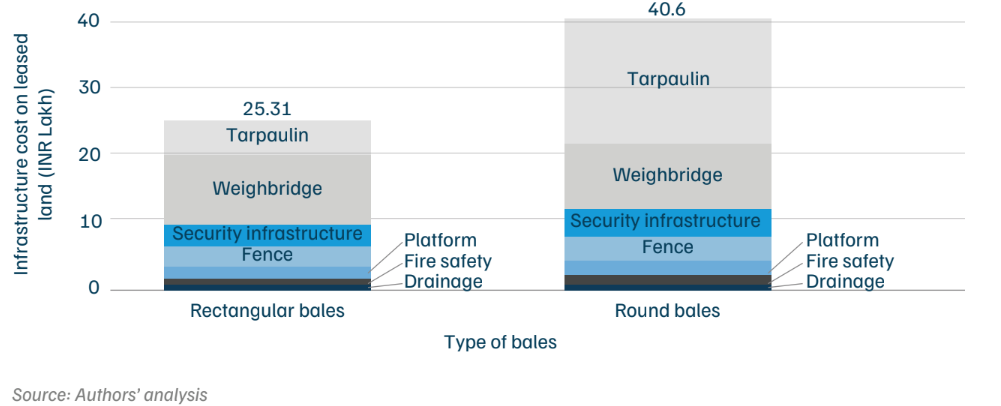

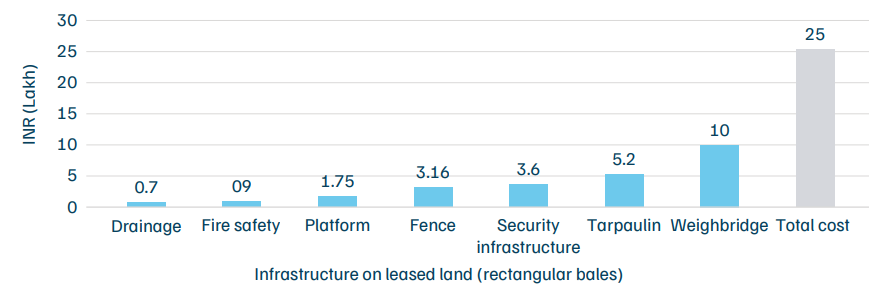

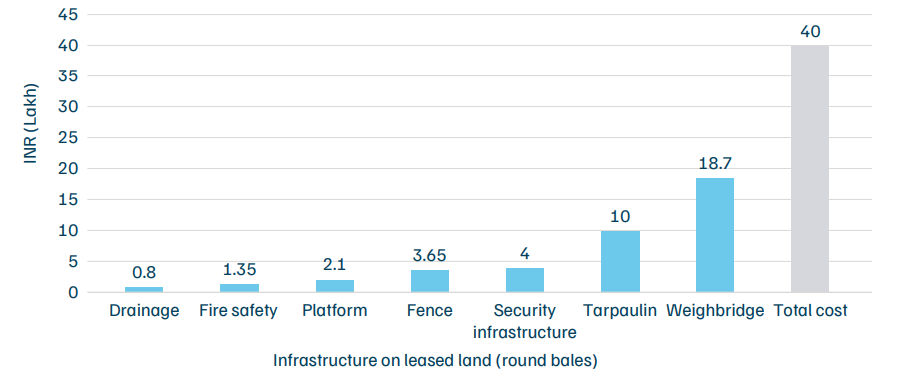

Figure 13. Initial storage cost of INR 250–400/tonne (rectangular–round) is required to store 10,000 tonnes of bales on leased land

Source: Authors’ analysis

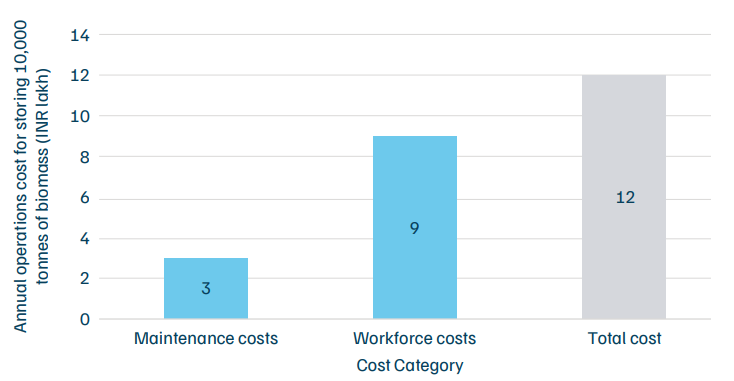

Our calculations suggest that the minimum infrastructure required to set up a storage facility will cost approximately between INR 250 per tonne for rectangular bales, and INR 400 per tonne for round bales. Round bales require additional land and tarpaulin costs as a higher surface area needs to be covered. This cost will vary as per the company’s life cycle, as the capital expenditure is staggered over an extended period. In addition, the capacity of the company to install infrastructure at the storage site will depend on the firm’s working capital and the ease of tenure ensuring the land. Hence, it is necessary to have a detailed financial understanding of the viability of the infrastructure provided.

To estimate the operational expenditure at the biomass storage depot, we have made the following assumptions in addition to the one listed for biomass storage at the depot:

Figure 14. Workforce costs constitute the maximum in operational expenses

Source: Authors’ analysis

The operational costs associated with managing paddy straw storage and processing are significant, with workforce expenses constituting the largest portion of the spending. Maintenance and monitoring are critical to ensuring the quality and safety of the bales, especially during the monsoon season, when additional measures like tarpaulin covering are necessary. Workforce is critical to keep track of feedstock quality and utilisation, with each storage site requiring five to eight employees, including a manager, site supervisor, machine/ vehicle operator, and security staff, depending on the size of the storage facility.

Payback period

With the initial setup cost and operating costs calculated, a payback period analysis is done to evaluate the investment viability and to assess how long it will take to recoup the investment made. In this scenario, a payback period is calculated, within which, the initial investment in storage facilities would be recovered through savings from avoided losses, taking into account different loss percentages at different procurement prices.

Table 3. Payback period (in years) for both rectangular and round bales

| Rectangular bales | Loss factor (%) | ||||

|---|---|---|---|---|---|

| Benchmark Price (INR/tonne) |

5 | 10 | 15 | 20 | |

| 1000 | Not viable | Not viable | 8.9 | 3.2 | |

| 1500 | Not viable | 8.9 | 2.4 | 1.4 | |

| 2000 | Not viable | 3.2 | 1.4 | 0.9 | |

| 2500 | 83.3 | 2.0 | 1.0 | 0.7 | |

| Rectangular bales | Loss factor (%) | ||||

|---|---|---|---|---|---|

| Benchmark Price (INR/tonne) |

5 | 10 | 15 | 20 | |

| 1000 | Not viable | Not viable | 14.3 | 5.1 | |

| 1500 | Not viable | 14.3 | 3.9 | 2.2 | |

| 2000 | Not viable | 5.1 | 2.2 | 1.4 | |

| 2500 | 133.3 | 3.1 | 1.6 | 1.1 | |

Source: Authors’ analysis

Note: Payback period is calculated by initial setup cost/annual net savings). Calculations can be seen in the Annexure.

Investing in storage is ideal when annual losses exceed the operating expenses. For rectangular bales, losses above 15 per cent above the rate of INR 1,500 per tonne is recommended as the payback period is within three years; whereas, for round bales, losses above 15 per cent at INR 2,000 per tonne and above 20 per cent at INR 1,500 per tonne is recommended. The avoided losses make it compelling to invest in storage within the one-tothree year timeframe.

As ex-situ crop residue management gains traction with six million tonnes of paddy stubble projected to be managed in Punjab, adequate storage space and infrastructure investment are required. Based on the model calculator, to store six million tonnes, approximately 4,200 acres (rectangular bales) to 5,580 acres (round bales) will be required. The infrastructure investment with rectangular bales (at INR 250 per tonne) will translate to INR 150 crore (USD 17 million), and with round bales (at INR 400 per tonne) will translate to INR 240 crore (USD 27 million). This investment will not only create a strong biomass supply chain, but will also ensure job-creation opportunities with a workforce required to collect, transport and manage the feedstock. This could create 3,500–5,500 direct semi-skilled jobs

This section provides an overview of our recommendations to policymakers in the biomass supply chain.

With increasing feedstock demand, companies have demonstrated storage practices based on experience. Biomass storage guidelines are needed to serve as a reference, to aid in designing efficient and safe storage facilities. The guidelines should include optimal paddy straw collection practices, quality measures, minimum infrastructure required, stacking methods, stack covering and protection measures, fire safety measures, training needs, and monitoring standards. Given the diverse biomass availability across states, a nationallevel framework will provide a cohesive structure while allowing states to tweak guidelines according to the specific biomass found.

Once sufficient data is available on biomass storage challenges and best practices, the guidelines must be developed in consultation with relevant ministries, as multiple departments are in the ex-situ management network. The Ministry of Petroleum and Natural Gas and the Ministry of Agriculture and Farmers’ Welfare administer schemes subsidising biomass collection machinery; their involvement is important towards formulating guidelines. The Warehousing Development and Regulatory Authority (WDRA) is the statutory body responsible for preparing warehousing guidelines in India. The Ministry of Rural Development and Panchayati Raj oversees land availability and allocation for storage sites. The Bureau of Indian Standards (BIS) should also be consulted in developing standards similar to those established for cotton bale storage. As more Indian states (Uttar Pradesh, Madhya Pradesh) are launching biofuel policies to spur growth in the sector, national guidelines will standardise biomass storage practices, and help minimise financial and feedstock losses. A strong guideline framework can translate into a biomass quality standard certification in the long run.

Currently, VLEs anticipate off-season demand and store paddy straw at interim depots until April or May. They sell stored paddy straw before the monsoon commences to avoid losses, as the feedstock is susceptible to degradation through moisture ingress and fire risk. Establishing dedicated interim biomass storage depots with infrastructure would mitigate these risks, while ensuring feedstock supply to industries post-kharif harvest. This is why a pilot project must be conducted in regions with high-demand feedstock requirements prior to statewide implementation. Pilot projects should undergo monitoring by the state energy development agency to understand acceptability among VLEs and ensure compliance with safety standards.

The Department of Rural Development and Panchayat, Government of Punjab, should also play a role in providing suitable land (location and road access) and demarcating land for storage, which is done similarly by the Punjab Energy Development Authority (PEDA) to define the catchment for present and upcoming compressed biogas plants. The Central Warehousing Corporation sets annual tariffs for storing notified commodities. However, no such structured mechanism exists for paddy straw storage. The PEDA should collaborate with the Warehousing Corporation to establish shared storage facilities to address this gap. These common depots would provide storage under a fee-based model to ensure financial returns. The state government should explore a public-private partnership (PPP) model to reduce the financial burden on the state and create local employment. These depots could also serve as a facility to store assets like CRM machinery, fertilisers, and biofertilisers from BioCNG plants.

With more and more companies encouraged to use paddy straw in Punjab, there will be a constantly increasing demand for feedstock of the highest quality. Rising demand and competition among paddy straw-based companies will result in feedstock price volatility, impacting the production costs and overall profitability of the firm. We recommend that PEDA undertake price discovery studies with premier institutions, in consultation with industries, to determine the optimal price range for paddy straw, for the economic viability and sustainability of these biofuel/bioenergy projects. The price discovery research should account for the availability, collection, transportation, and storage of paddy straw, as well as the impact of government policies. Companies say the cost of feedstock is just seen as the procurement price, although there is a storage cost attached as well, which is not currently taken into consideration. On the other hand, various government policy documents like CRM Operational Guidelines and Madhya Pradesh’s Biofuel Policy, mention that the price of agricultural residue will be decided with the consent of the farmers. However, the collection and supply of agricultural residue is largely unorganised, with farmers receiving limited or no payment (Kemanth, Singh and Ignatious 2024). A transparent, well-defined price discovery mechanism will help in determining the paddy straw pricing range that is feasible for the project developer, and also nudge farmers to provide feedstock surplus for a fair and remunerative price.

Surveyed companies reported 15–25 per cent loss of feedstock per annum due to bale quality degradation, caused due to moisture absorption during the rainy season and improper storage conditions. With no standardised method of discarding bales, companies dump the spoiled bales in a designated area, mulch them back, or compost. The growing pile of waste bales is a safety concern and a logistical issue, as they occupy valuable space that could otherwise be used for fresh feedstock. It also creates a risk-prone situation, as the new bale stacks are placed close to discarded ones, leaving them open to possible contamination and prolonged anaerobic digestion, leading to methane emissions. While the CPCB’s Environmental Guidelines for Compressed Biogas Plant (CBG)/BioCNG Plants, released in 2022, briefly mentions that rejected biodegradable input material (like spoiled bales) should be disposed of in accordance with the Solid Waste Management Rule, 2016, a detailed procedure is missing (Central Pollution Control Board 2022). Similar to the technical guidelines developed for handling and disposal of industrial wastes and byproducts, the CPCB, in consultation with SPCBs and companies, should develop protocols for safely discarding degraded bales.

The biomass supply chain has inherent risks with the handling of the feedstock. The storage of feedstock is handled by multiple large and small players, who have their own risk-taking ability. In the event of a risk-prone situation, for example, a fire incident, owners suffer substantial financial loss, as their incomes are dependent on selling feedstock to industries. The feedstock losses also extend the effect on industries dependent on a constant supply of quality feedstock, with project financing becoming tougher.

To fully utilise the potential of bioenergy production, there is a need to implement financial provisions to safeguard the feedstock. Insurance as a financial instrument has been implemented in other sectors, which is yet to be introduced to the biomass supply chain. This can be done through three steps. First, conduct a risk assessment in conjunction with industries, which will quantify the risk probability in the likelihood of biomass supply chain disruption (losses occurring at storage due to fire hazards or other accidents). Second, calculate risk pricing, which will translate the probability into cost impacts for project financing models, enabling insurers to price policies accurately. Lastly, develop tailored insurance products that protect the feedstock against any risk-prone situation, which will increase industry confidence and enable long-term financing/contracts. The addition of insurance to the biomass supply chain will help reduce the perceived risk, and stabilise longterm contracts.

We estimate that development of storage infrastructure to manage the government target of 6 MMT paddy straw will spur 3,500–5,500 direct semi-skilled jobs. Although the surveyed companies had their own stacking practices based on operational experience—for example, stack length/width and distance between stacks—they emphasised the importance of uniform stacking. This practice reduces the risk of bales toppling over, and minimises water retention in the stacks, preserving the quality of the stored paddy straw. However, since biomass collection/stacking is a temporary employment during the narrow harvest window, companies report only providing verbal instructions, with no formal training for biomass stacking, loading, and unloading. We recommend that biomass-based companies should define clear operational procedures for the workforce employed in receiving, stacking, and dispatching biomass, ensuring minimisation of losses at storage depots.

As India progresses to becoming a leader in bioenergy production, and curb agricultural residue burning, the biomass supply chain needs to be strengthened. The practice of storing biomass requires to be done properly to limit losses avoiding methane emissions and any fire risk. The seasonal availability of the biomass stresses the importance of storage required in order to ensure there is quality feedstock all year round. To streamline the processes, innovative solutions for the supply chain need to be tailored to India’s large, diverse biomass surplus.

This study brought the on-ground findings on current practices being followed in Punjab for paddy straw bales, and the need for guidelines voiced by the industry. The growing trend of ex-situ management has increased industry participation requiring additional storage areas to operate. These storage facilities currently based on experience or peer learning and often face productivity and often monetary losses. Proper guidelines and trainings are required to store keeping collection methods, quality measurements (moisture content primarily,) stacking methods, fire safety measurements and minimum infrastructure.

This study serves as a starting note to introduce how important storage is and the minimum infrastructure required to store paddy straw bales. Additional scientific studies—on the impact of bale characteristics like density, storage infrastructure, and handling methods on biomass storage—will be necessary to fully utilise the biomass. While this study focuses on paddy straw, India has a large and diverse biomass availability, which has the potential for bioenergy. Similarly, guidelines on how other crop residues are managed and stored efficiently will help achieve national targets.

Ex-situ crop residue management is the process of removing crop residue from the field and managing it through utilisation pathways such as compressed bio gas, biomass-based power plants, industrial boilers, pellet/briquette manufacturing, 2g ethanol, brick kilns, biochar and paper/packaging industry.

The ex-situ biomass supply chain is a sequential process concentrated within a short 15–20 day kharif harvest window in October and November. It begins with residue collection, involving slashing, drying (with a recommended minimum five-day period to limit moisture), raking, and baling the stubble. This is followed by first-mile transportation of bales from fields to storage, which can be interim or main (leased/owned, either open or semi-open with sheds). Finally, last-mile transportation delivers the stored biomass to end-user facilities, where it is utilised in various industries.

It ensures a continuous feedstock supply for year-round industrial operations despite seasonal availability. Proper storage is vital for maintaining feedstock quality, preventing degradation from high moisture (ideal to be 20 per cent or less) and microbial activity, which reduces calorific value and poses a fire risk. Storage minimises significant losses impacting profitability and prevents methane emissions from degraded bales.

Behaviour Change Approaches to Tackle Stubble Burning at Scale

Organic Waste Circular Economy for Viksit Bharat

How Can India Tackle Air Pollution with an Airshed-level Approach?

Roadmap of the methodology to assess the climate co-benefits of the SUP ban in Tamil Nadu

Roadmap of the methodology to assess the climate co-benefits of the SUP ban in Maharashtra