Council on Energy, Environment and Water Integrated | International | Independent

Suggested citation: Agarwal, Disha, Arushi Relan, Rudhi Pradhan, Sanyogita Satpute, Karthik Ganesan, Shalu Agrawal. 2025. How can India Meet its Rising Power Demand? Pathways to 2030. New Delhi: Council on Energy, Environment and Water.

India’s electricity demand is growing fast with rapid economic development, urbanisation and climate-induced heat stresses. Since FY21, India’s electricity consumption has risen at ~9% per annum, compared to an average of 5% annually in the preceding decade. This study assesses various pathways that India can take to reliably meet the electricity demand in 2030. For this, the study models India’s power system despatch for every 15 minutes in 2030 with existing and planned generation capacities, and interstate and interregional transmission constraints to answer two critical questions. One, can India meet its projected 2030 power demand with existing and planned capacities? Two, if the demand grows faster than projected, what will be the cost-effective pathway for India to meet the demand reliably? Based on an assessment of current grid and on-ground challenges, it then provides a seven-point agenda for the Ministry of Power (MoP), Ministry of New and Renewable Energy (MNRE), and other central and state agencies to realise the benefits of the most desirable pathway.

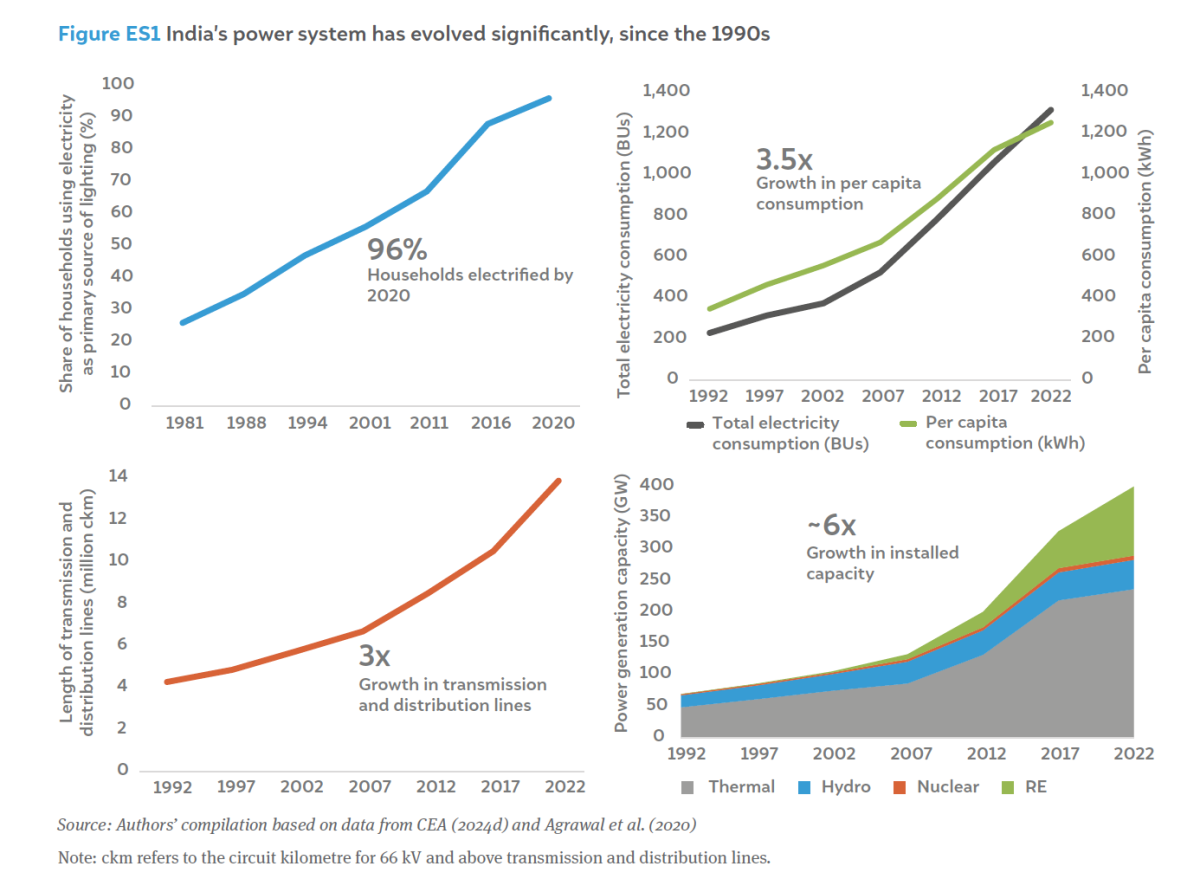

Since 2014, India has simultaneously improved access to electricity, addressed energy security concerns, and laid the foundation for a clean energy transition. India’s power system has evolved significantly since the 1990s (Figure ES1). India became the world’s third- largest producer of electricity in 2019 (IEA 2021). By 2020, 96 per cent of the households were electrified (Agrawal et al. 2020). The country saw a fivefold increase in solar and wind power capacities between 2013 and 2022, making it amongst the top four renewable energy (RE) installers globally (PIB 2024a). Notwithstanding these achievements, India faces the unique and complex challenge of decarbonising its expanding power system while providing reliable and affordable electricity to meet rising demand.

The Central Electricity Authority (CEA), in its 20th Electric Power Survey (EPS), projects that India’s FY30 electricity requirement and peak demand will both grow by 6.4 per cent per annum, from FY22 (CEA 2022a). However, recent trends show ~9 per cent annual growth in the electricity requirement since FY21, compared to an average of 5 per cent per annum in the decade before (CEA, n.d.-d). The EPS demand estimates for 2030 consider baseline projections for green hydrogen production, rooftop solar penetration, electric vehicles, and other sectors based on extant policies. One-third of this electricity demand is likely to be consumed by the industrial sector. Considering the push to decarbonise the industrial sector through electrification, the industrial electricity demand is expected to grow faster than anticipated. This would result in a higher electricity demand than that projected by the EPS. For instance, the impact of producing 5 million tonnes (MT) of green hydrogen in the context of an interconnected grid system could result in a 13 per cent higher electricity requirement than that projected in the EPS for 2030 (Pradhan et al. 2024). Additionally, economic growth, urbanisation, and climate–induced extreme weather events are likely to influence demand growth and make it more uncertain.

While the supply side has responded to the growing demand, capacity addition has been slow in recent years due to a combination of domestic and extraneous factors. For instance, as of August 2024, over 30 GW of coal capacity is under-construction, 19 GW of which was awarded before 2019 (CEA 2024c). Simultaneously, India has deployed only 3 GW of hydro and nuclear capacities and about 90 GW of RE capacities between 2019 and 2024, resulting in around 218 GW of total non-fossil based capacity (CEA, n.d.-b).1 The country still needs to deploy around 56 GW of non-fossil based capacity every year between 2025 and 2030 to meet its 500 GW of non-fossil capacity target by 2030 (CEA, n.d.-b, PIB 2023d).

These trends raise a critical question: how should India plan for adequate resources to meet its energy and peak power requirements by 2030? Answering this question requires an assessment of alternative scenarios the country may face and be prepared for such possibilities. For instance, would India be able to reliably meet its 2030 power demand with its existing and planned generation and transmission capacities? If the country faces higher demand than that projected by the EPS, what might be some cost-effective strategies to enhance the capacities? Further, if India does not meet its 2030 non–fossil capacity target of 500 GW, how much new thermal capacity would be required? In choosing a desirable pathway to ensure energy security, how can India maximise the social and environmental outcomes while limiting the financial burden on its already strained electricity sector? Finally, what kinds of policy signals and market mechanisms are needed to achieve the energy trilemma of securing clean, affordable, and reliable electricity access by 2030?

To answer these questions, we modelled India’s power system and performed national-level despatch simulations. We conducted the exercise using Plan OS’ production cost, a security- constrained linear optimisation model, in collaboration with GE Vernova’s Consulting Services.

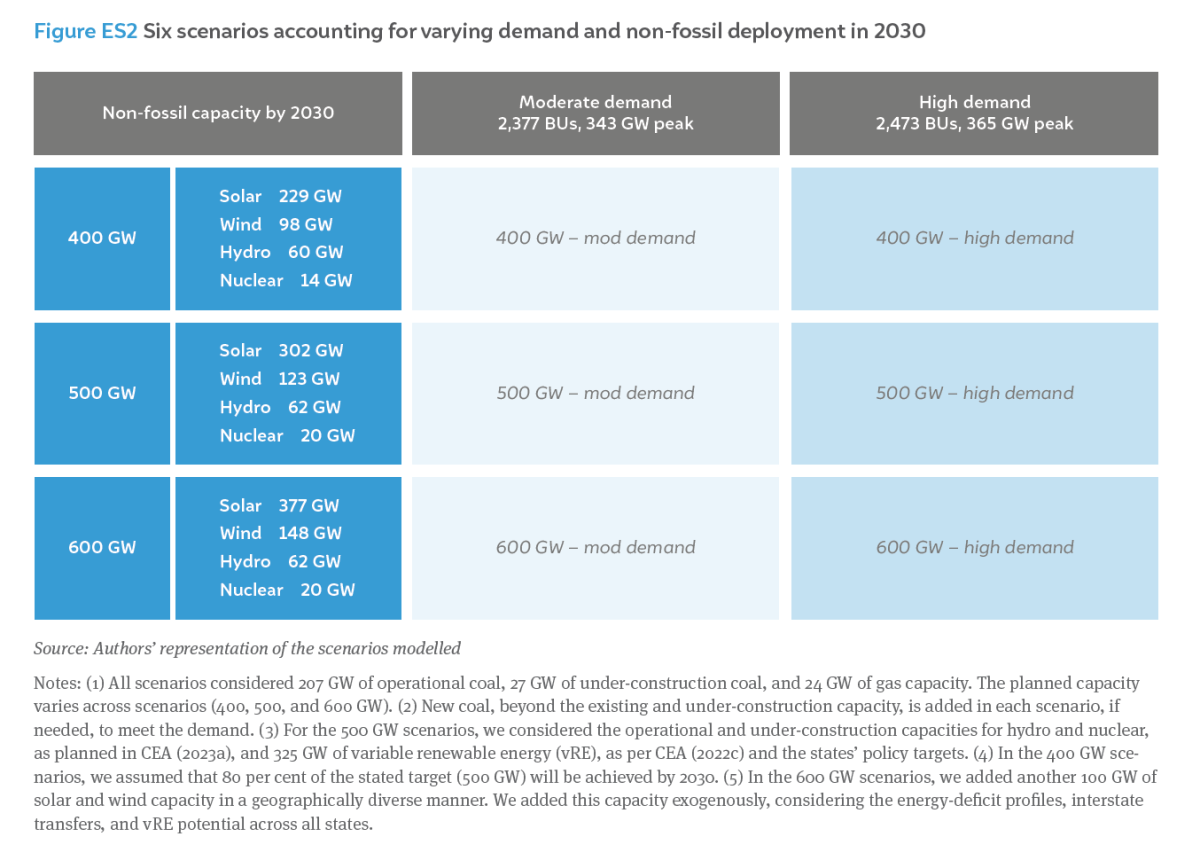

We simulated six scenarios for 2030, considering two major factors: i) uncertainty in growth and, therefore, total demand, and ii) uncertainty in the rate of non-fossil capacity deployment. For the first factor, we modelled moderate demand scenarios (5.8 per cent and 5.1 per cent growth in the energy requirement and peak demand respectively, between 2023 to 2030) and high demand scenarios (6.4 per cent and 6.0 per cent growth in the energy requirement and peak demand respectively, between 2023 and 2030); the latter assumes that the energy requirement and peak demand projections from EPS for FY32 will manifest early in 2030. For the second factor, we modelled varying non-fossil capacities – stated (500 GW), high (600 GW), and low (400 GW) – along with operating and under-construction thermal capacity,3 assuming that the residual demand will be met with additional coal capacities and transmission enhancements. These simulations resulted in a combination of six scenarios, described in Figure ES2.

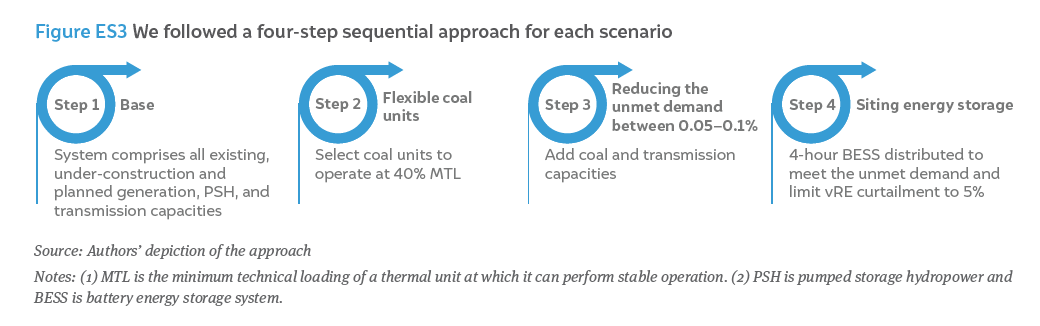

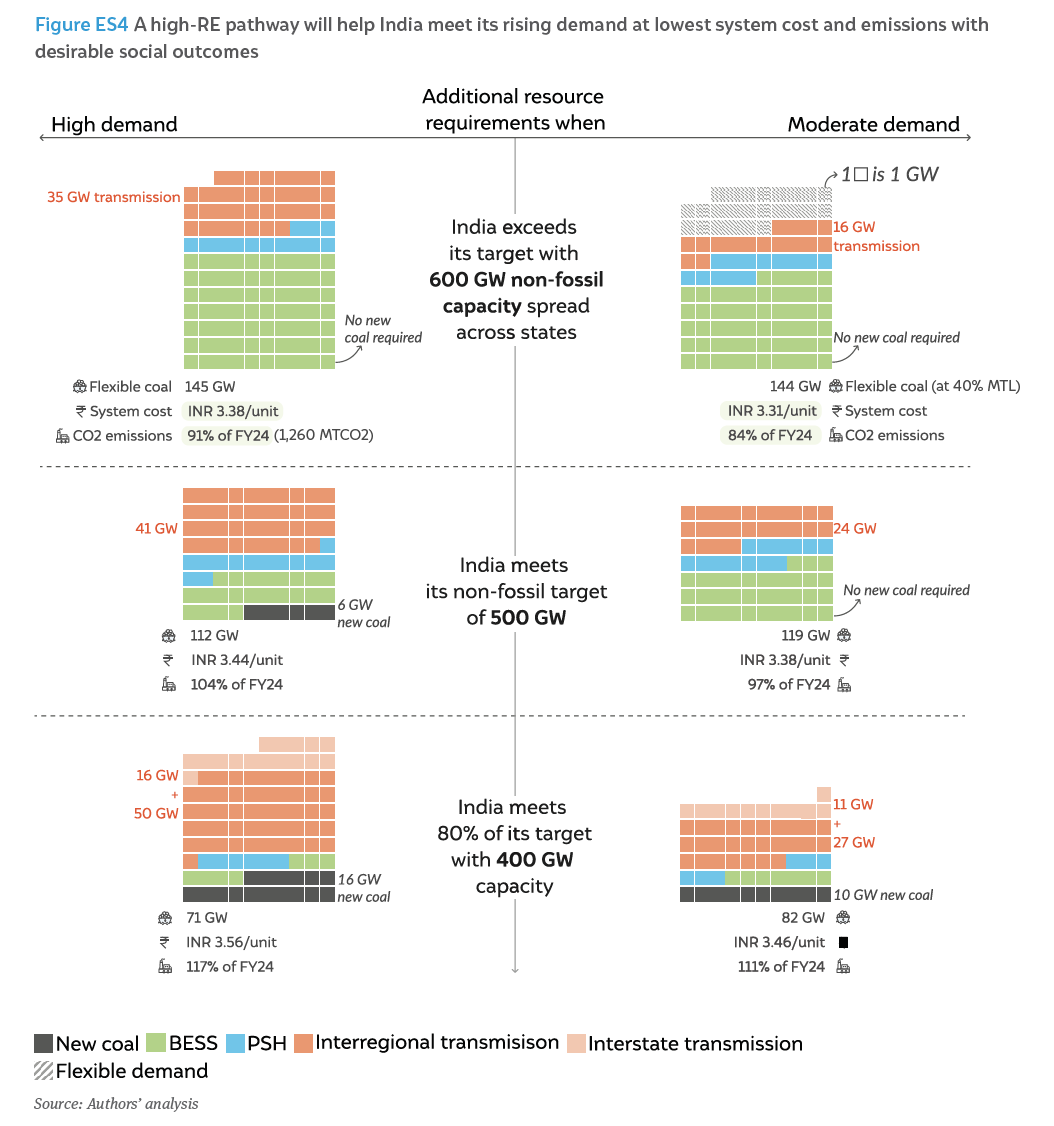

To facilitate comparison across scenarios, we constrained the model to meet the reliability criteria: (i) normalised energy not served (NENS) between 0.05–0.1 per cent, and (ii) vRE curtailment less than 5 per cent in 2030 (CEA 2023c). We used a four-step approach to meet these reliability criteria across all scenarios, as illustrated in Figure ES3. We also assumed the system would follow a Market-based Economic Despatch (MBED) scheduling framework in 2030. Once the reliability criteria were met, we evaluated the system costs. We considered the annualised capital costs for new coal units and enhanced transmission networks, the levelised costs of storage, and the production cost of electricity from all generating sources.4 Figure ES4 summarises the model results for all six scenarios.

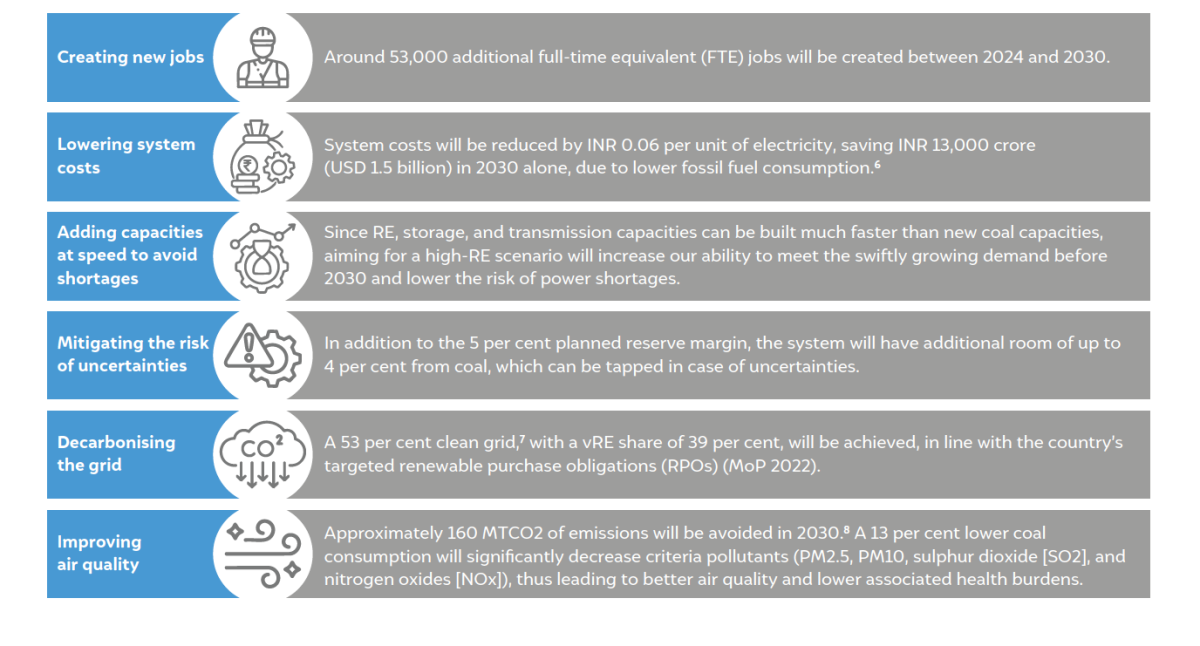

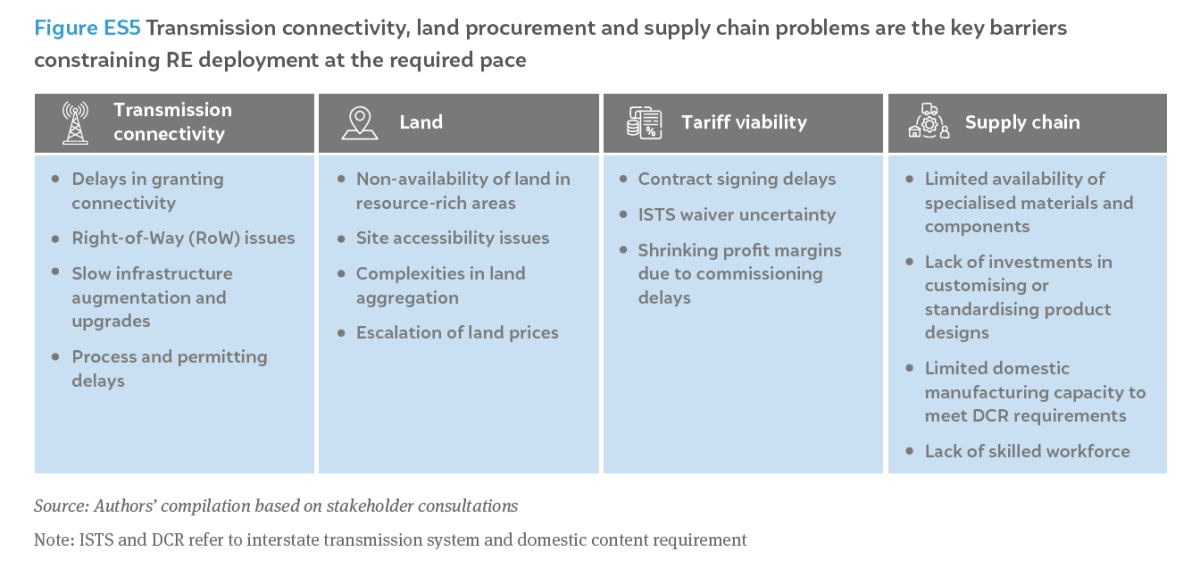

Meeting the rising demand with a high-RE pathway is a reliable, affordable, and clean option. However, our analysis and stakeholder consultations reveal several challenges that can restrict the pace of RE deployment, integration, and offtake. These include the slow pace of transmission capacity addition, connectivity delays,15 complexities in land procurement, and supply-chain constraints (Figure ES5). However, it is possible to overcome these challenges through continuous policy innovation and strategic interventions.

Drawing from the results of the model simulations and extensive discussions with key stakeholders in India’s power sector, we recommend a seven-point action agenda. This plan will facilitate realising the socio-economic benefits and the desired power system outcomes of cost-effectively integrating renewables at scale.

“India’s electricity demand is rising faster at around 9% per annum since FY21, compared to an average of 5% in the previous decade. The Central Electricity Authority projects electricity demand to grow at 6% CAGR between 2022 and 2030. However, recent trends suggest that actual demand could surpass these estimates. Economic growth, urbanisation, industrial electrification, upcoming demand avenues (green hydrogen, electric vehicles, etc.), and rising temperatures are likely to influence the demand growth and make it more uncertain.”

“Our analysis suggests that India can meet the electricity demand as projected by the Central Electricity Authority’s 20th Electric Power Survey, with existing and planned generation resources (i.e., with 500 GW non-fossil capacity) without any further coal addition in 2030. But if demand were to increase beyond these estimates, India will have multiple pathways, each with its own set of challenges to meet the demand reliably.”

“Our analysis suggests a high-RE pathway, i.e., 600 GW non-fossil capacity without any further addition of coal to be the most cost-effective pathway for 2030 to meet the rising demand reliably (without any power shortages). ”

“Temporal mismatch between the demand and supply from the intermittent renewable generation (variable RE) sources like solar and wind is the main challenge. Integration of flexible resources such as battery energy storage systems, pumped hydro, flexible coal and hydroelectricity, and transmission enhancements, and demand side flexibility will help manage the demand-supply variations in a high-RE grid.”

“There are four key barriers restricting the RE deployment at pace: (a) Transmission connectivity due to delays in granting connectivity, slow infrastructure augmentation and upgrades, process and permitting delays, and Right-of-Way issues; (b) Land, which includes non-availability of land in resource-rich areas, site accessibility issues, complexities in land aggregation, and escalation of land prices; (c) Tariff viability concerns, because of contract signing delays, ISTS waiver uncertainty, shrinking profit margins due to commissioning delays; and (d) Supply chain, including limited availability of specialised materials and components, lack of investments in standardising product designs, limited domestic manufacturing capacity to meet DCR requirements, and lack of skilled workforce”

How can India Create a Demand Flexibility Market?

Contracts for Difference for Flexible and Affordable Clean Power

Enabling Corporate India's Clean Energy Transition

Scaling Solar Power for Irrigation in India: