Council on Energy, Environment and Water Integrated | International | Independent

Suggested citation: Agrawal, Shalu, Sunil Mani, Abhishek Jain, and Karthik Ganesan. 2020. State of Electricity Access in India: Insights from the India Residential Energy consumption Survey (IRES) 2020. New Delhi: Council on Energy, Environment and Water.

Over the last decade, the Government of India’s efforts in providing electricity access to the country’s population has been commendable. Using the nationally representative India Residential Energy Consumption Survey (IRES), this study undertakes an independent assessment of the quality and reliability of power supply and consumer satisfaction with electricity services. Further, it analyses how distribution companies (discoms) handle the metering, billing, and payment collection (MBC) process across households. The study also proposes strategies to fill the remaining gaps to realise the goal of universal, affordable, and reliable electricity access in India.

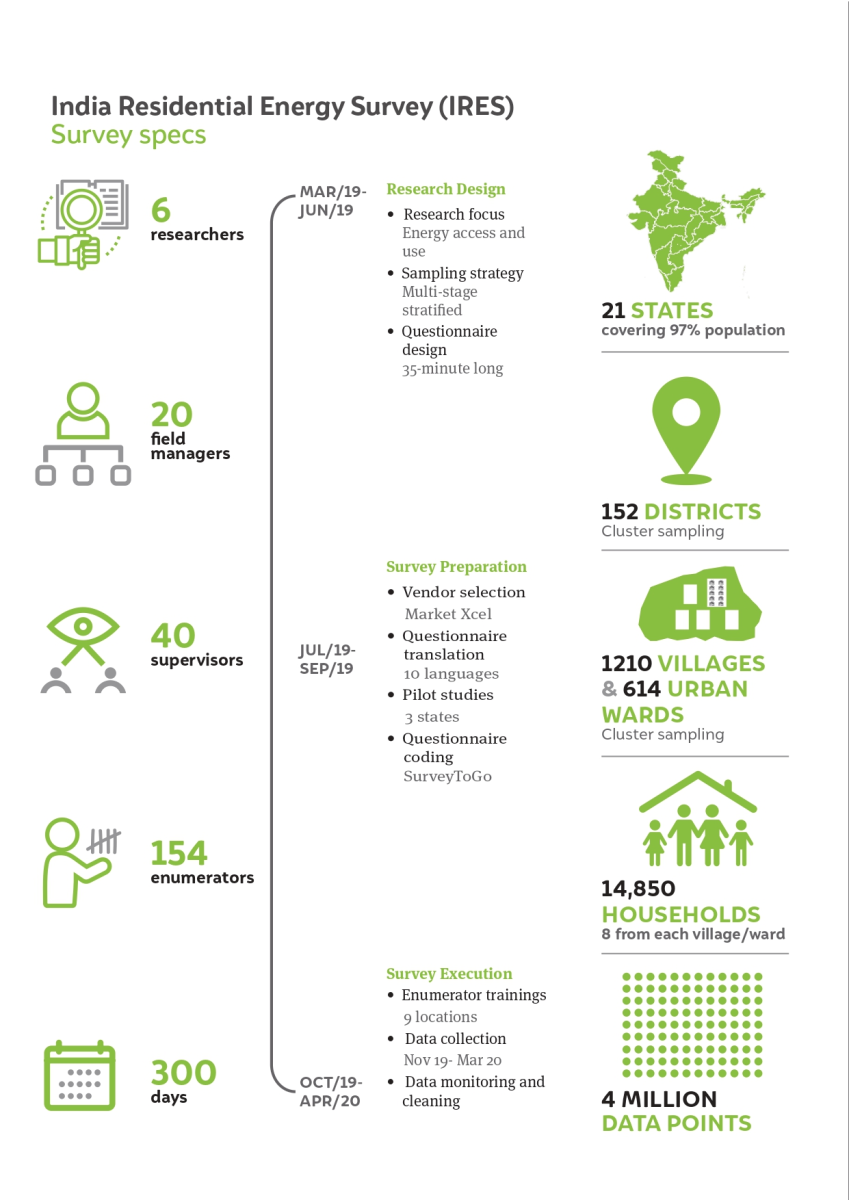

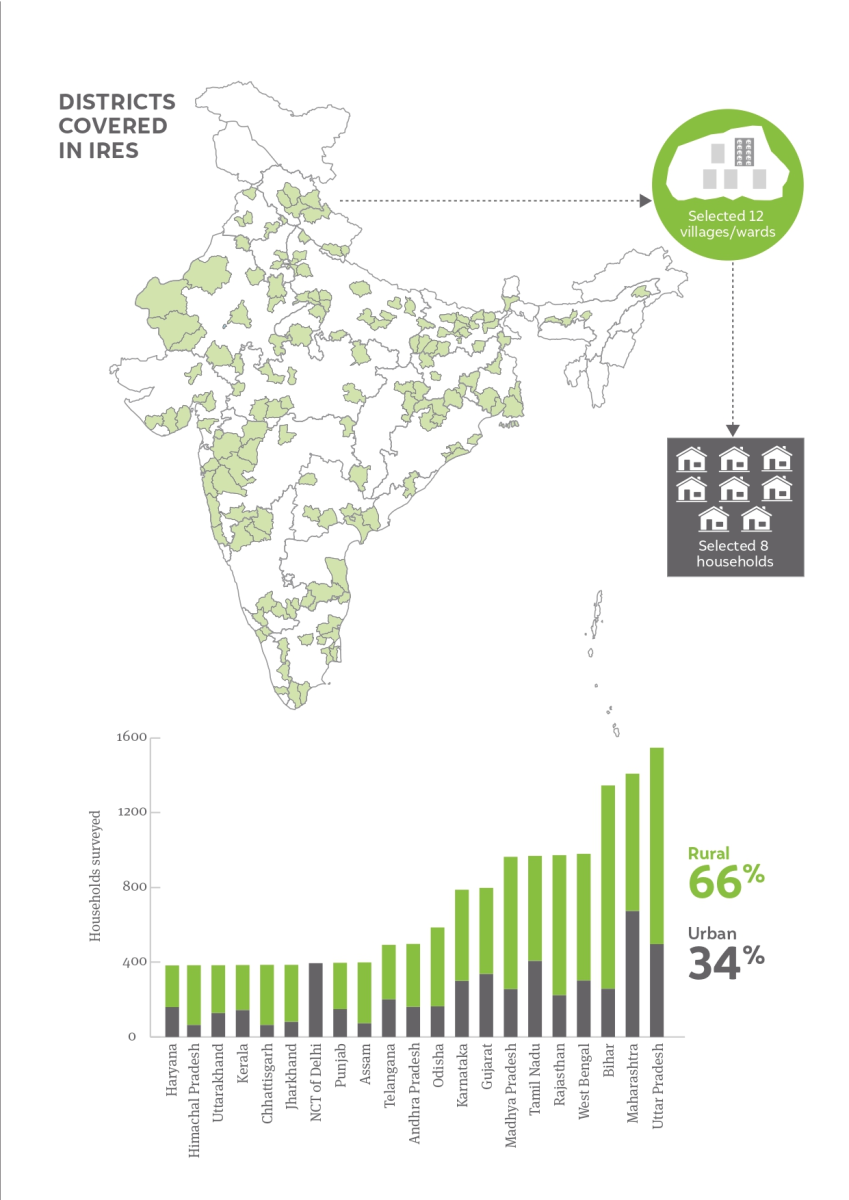

The India Residential Energy Consumption Survey (IRES) is the first-ever pan-India survey on the state of energy access, consumption, and energy efficiency in Indian homes. It covers nearly 15,000 households in 1210 villages and 614 wards in 152 districts across 21 states. Conducted in 2019 in collaboration with the Initiative for Sustainable Energy Policy (ISEP), the survey findings help make comparisons of the progress made since ACCESS2018 and ACCESS2015.

As one drives across different parts of rural India, it is heartening to see the electric wires lining the landscape as far as one can see. They carry not just power but hope to the millions who use electricity to meet their lighting, cooling, life and livelihood needs. With the aggressive implementation of Pradhan Mantri Sahaj Bijli Har Ghar Yojana (Saubhagya) since September 2017, 26.3 million households were given grid-electricity connections at subsidised rates or free of cost (Ministry of Power 2019). As per the Saubhagya dashboard, all ‘willing’ households in India are electrified, as of 31 March 2019.

In 2015 and 2018, the Council on Energy, Environment and Water (CEEW) conducted two rounds of energy access surveys (Access to Clean Cooking energy and Electricity— Survey of States [ACCESS]) in rural households across six of India’s energy-poor states— Bihar, Jharkhand, Madhya Pradesh, Odisha, Uttar Pradesh, and West Bengal. As rapid electrification sweeps over the country, it is desirable to have a survey across the nation to find answers to questions such as: (i) Once electrified, do all households also have seamless access to electricity supply? (ii) Has India delivered on the dream of ‘24x7 power for all’? and (iii) importantly, how do consumers respond to supply disruptions from the grid?

Providing reliable electricity services is linked to the ability of power distribution companies (discoms) to collect commensurate revenue from the consumers. However, most Indian discoms are under severe financial distress, in part due to gaps in metering, billing, and collection (MBC) (Ganesan, Bharadwaj, and Balani 2019). With many new households wired to the grid, it is essential to know how has the needle moved on the MBC front. India is at the cusp of a new decade of change and growth in the power sector. An independent assessment of the state of electricity access in the country and identifying gaps in that access therefore becomes necessary.

To understand the state of access to electricity, we undertook a nationally representative survey covering nearly 15,000 households spread across 21 states of India. The survey, which we call the India Residential Energy Survey (IRES), was conducted in collaboration with the Initiative for Sustainable Energy Policy (ISEP) and covers different dimensions of energy use in households. In this report, we answer the following questions:

We present the results of the IRES 2020 survey and based on our assessment, we propose strategies to fill the remaining gaps to realise the goal of universal, affordable, and reliable electricity access in India.

India Residential Energy Survey (IRES) Survey specs

Source: Authors’ analysis

DISTRICTS COVERED IN IRES

Source: Authors’ analysis

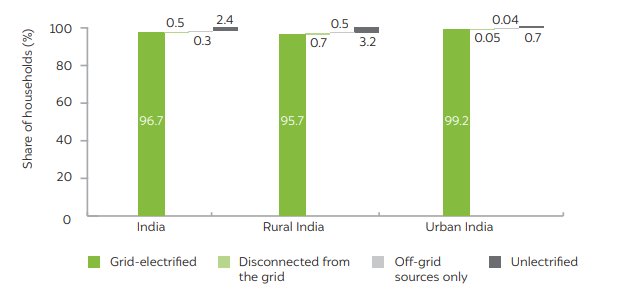

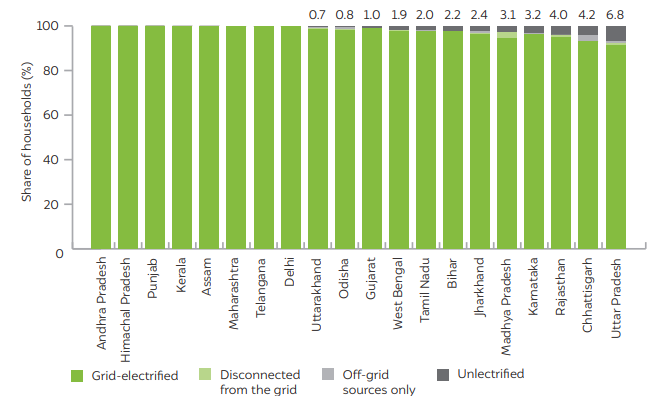

As per IRES 2020, nearly 97 per cent of Indian households are electrified. India has made a commendable effort on household electrification, as 96.7 per cent of Indian households are now connected to the grid, with another 0.33 per cent relying on off-grid electricity sources. However, 2.4 per cent of Indian households still remain unelectrified (Figure ES1). Most of the unelectrified households are concentrated in the rural areas of Uttar Pradesh, Madhya Pradesh, Rajasthan, Haryana, and Bihar (Figure ES2).

A majority of the unelectrified households cited their inability to afford grid-connection as the reason for not having a connection. Given the availability of free-connection under Saubhagya scheme, some of households were likely not aware of the scheme, not able to access it, or were deterred by the recurring monthly expenditure of paying electricity charges. Most of these households are multidimensionally poor, characterised by reliance on labour activities for sustenance, life in a kachha house, non-ownership of a motorised vehicle, and use of traditional biomass as the primary cooking fuel. Other reasons for households not having access to electricity are lack of grid supply in the neighbourhood, refusal of connection due to inadequate documents, and application under process.

Figure ES1 With only 2.4 per cent of households lacking access to electricity, India is close to achieving universal electrification

Source: Authors’ analysis

Figure ES2 A few north-central states have a majority of the unelectrified households

Source: Authors’ analysis

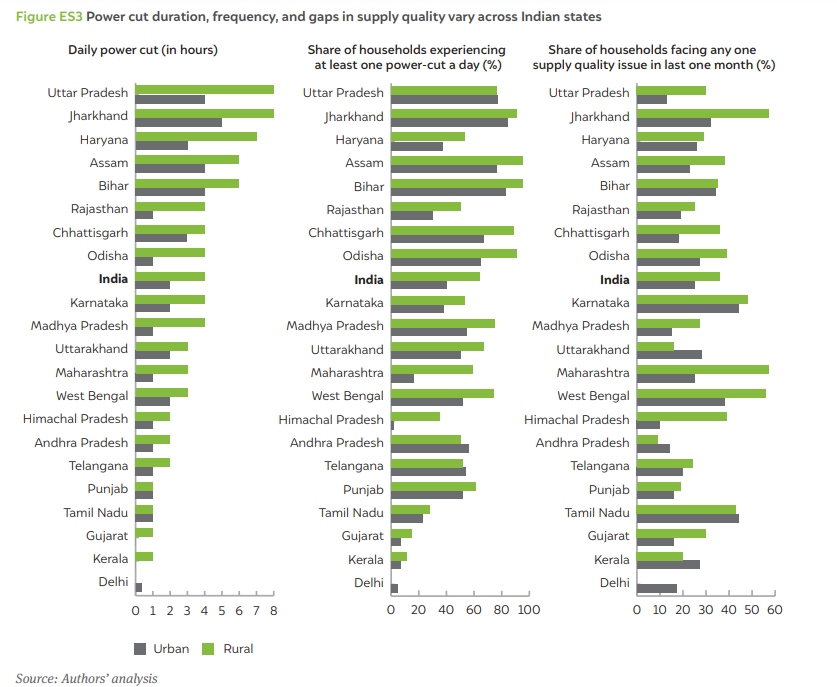

An average Indian household receives 20.6 hours of power supply from the grid. The average daily supply in urban areas (22 hours) is longer by a couple of hours than in rural areas (20 hours). Delhi, Kerala, and Gujarat are the top states, maintaining slightly over 23 hours of average supply in both urban and rural areas. In contrast, households in Uttar Pradesh, Jharkhand, Haryana, Assam, and Bihar face the longest power outages, with rural households in these states facing six or more hours of daily outages (Figure ES3).

However, the current supply situation has significantly improved in rural India, especially in the six ACCESS states (Bihar, Jharkhand, Madhya Pradesh, Odisha, Uttar Pradesh, and West Bengal), where daily power supply to rural households is around 18.5 hours in 2020 compared to 12.5 hours in 2015 and 15 hours in 2018.

Most households faced unanticipated supply interruptions (76 per cent). Two-thirds of rural and two-fifths of urban households face outages at least once a day. Power outage duration and frequency are higher in Uttar Pradesh, Jharkhand, Assam, Bihar, and Haryana (Figure ES3). A third of households also faced at least one of the three supply quality issues—long blackouts, low voltages, or appliance damage due to voltage fluctuations—during the month preceding the survey. Only six per cent households reportedly registered a compliant in the past six months, indicating high consumer inertia or low awareness about their rights as electricity consumers.

Figure ES3 Power cut duration, frequency, and gaps in supply quality vary across Indian states

Source: Authors’ analysis

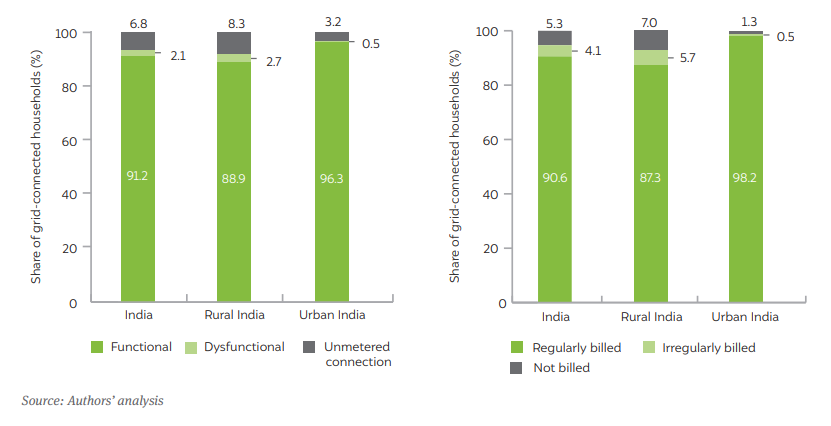

Of all grid-electrified households in India, 93 per cent have metered connections and 91 per cent are billed regularly. Metering and regular billing is critical for revenue collection and financial health of discoms. While most ACCESS states have improved metering rates over the past five years, with a six-fold improvement in Uttar Pradesh, the issue of unmetered connections and dysfunctional meters is more pronounced in rural areas (Figure ES4), particularly in Jharkhand and Madhya Pradesh. Further, metering gaps are higher in the case of households electrified over the past three years (20 per cent). A respondent from Kharagpur village of Palamu district of Jharkhand stated that, “the meter is kept in the house but has not been installed”.

While four per cent of grid users receive bills irregularly (few times in a year or once in a few years), another 5 percent of grid users have never seen a bill, though most of these households have been electrified for more than a year. Billing issues are pronounced in rural areas, mainly due to the high transaction cost and absence of an adequate billing mechanism. Jharkhand has the lowest share of grid users billed regularly (55 per cent), followed by Bihar (64 per cent). Billing irregularities are high in Assam, Uttar Pradesh, and Madhya Pradesh as well.

Discoms face losses in many states in India due to low collection efficiency. While we did not investigate payment compliance (due to problem of desirability bias), we assess payment modes used by households. Most households in India pay their bills in cash through discom payment counters and collection agents. Only 17 per cent of billed consumers pay their bills digitally (27 per cent in urban India and 12 per cent in rural India). This is despite the fact that 70 per cent of Indian households have a smartphone.

Figure ES4 More than 10 per cent of rural households do not have a functional electricity meter

Source: Authors’ analysis

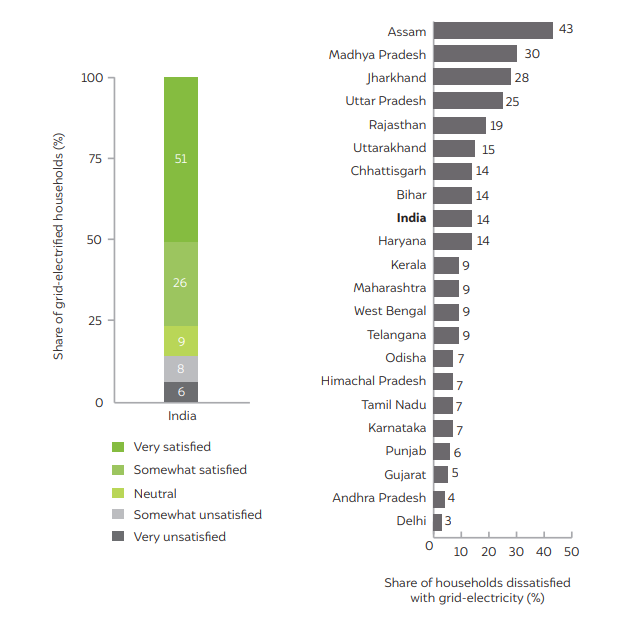

More than three-fourths of the grid users are satisfied with their electricity situation. In the six ACCESS states, the satisfaction levels among rural consumers increased from 23 per cent in 2015 to 55 per cent in 2018 to 73 per cent in 2020, which is in tandem with the consistent improvement in supply hours. This is a reason to celebrate. Yet, there remain several gaps in electricity service and these partly explain the existing gaps in consumer satisfaction (Figure ES6).

As many as 87–97 per cent of grid users in Delhi, Odisha, Andhra Pradesh, Himachal Pradesh, Maharashtra, Punjab, and Gujarat are very highly satisfied with electricity service, as typically power outages are less than two hours per day on average in these states, barring Odisha and Maharashtra. In contrast, more than 25 per cent of grid users are not satisfied with electricity services in Assam, Madhya Pradesh, Jharkhand, and Uttar Pradesh.

A major driver of household satisfaction is the duration of power supply, with reliability of supply and voltage stability also being significant factors. Regular billing is also associated with satisfaction among rural households. Our analysis underscores the importance of providing uninterrupted and reliable power supply to consumers along with regular billing.

Figure ES5 Majority of the dissatisfied households are in northern and eastern India

Source: Authors’ analysis

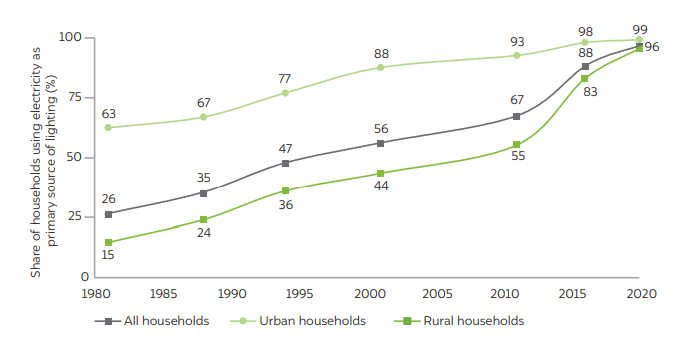

When our team was conceptualising the survey, in the summer of 2019, India had already achieved a milestone that was celebrated widely—electrifying nearly all households across the length and breadth of the country. Our study confirms the progress that India has made in terms of enabling access to electricity to its people. The share of households using electricity as the primary source of lighting has risen from 26 per cent in 1980 to 97 per cent in 2020. Over the past two decades alone, successive government schemes have brought nearly 800 million Indians out of darkness.

Figure ES6 India’s progress on household electricity access (1980-2020)

Source: Authors’ compilation based on Census, National Sample Survey Organisation (NSSO) survey, and IRES data

However, India is yet to achieve “access to affordable, reliable, sustainable and modern energy for all” (a subset of Sustainable Development Goal 7 of the United Nations to be achieved by 2030). We make the following recommendations to bridge the gap.

As most unelectrified households are concentrated within the rural areas of a few states, discoms must undertake targeted efforts to address the gap in (i) awareness about government schemes for electrification, (ii) documentation challenges, and (iii) adequate infrastructure to extend a connection.

We observed that poor households are reluctant to get an electricity connection due to unaffordable recurring costs and electrified households getting disconnected because of their inability to pay the electricity bill (at times due to irregular billing leading to a large outstanding amount). This situation calls for streamlining the billing operations. While all states in India have differentiated power tariffs, there is scope for inter-state learning. We call upon states with relatively higher tariff incidence on low-consumption category to consider implementing ultra-low tariffs and help the poorer households in sustaining their electricity access. More research is required on the principles and definition of a lifeline tariff.

Nearly 90 per cent of distribution transformers (DTs) in urban India and 64 per cent in rural India are already metered (Ministry of Power 2020). In the absence of direct communication with households, DTs remain the source of how electricity supply is experienced by households. Discoms can use this data to improve transparency on supply situation, identify areas with losses and plan other technological upgradations.

Discoms in India are mandated to follow SoPs related to supply quality, metering, and billing and are required to compensate consumers in case of violations. However, very few consumers register complaints as a result of low awareness about their rights and the complex process of claiming compensation for supply inadequacies. Besides promoting consumer education, electricity regulators must enforce compliance by imposing penalties on discoms for failure to meet the standards. Regulators could also consider a provision for ‘automatic compensation’ to consumers based on independent monitoring of supply quality.

Although discoms have achieved a phenomenal increase in metering and regular billing, some gaps remain. In addition to the upgradation of information technology (IT) infrastructure and billing systems, discoms should consider local and context-relevant solutions and create incentives for actors to help achieve the metering and billing targets. Another Achilles heel of discoms, collection efficiency, could be enhanced by offering digital modes of payment for consumers such as provisioning for online payment channels through IT kiosks, microentrepreneurs (local shops/youth), and existing public and private institutions to serve those unfamiliar with direct online payments. Less than one-fifth of consumers pay their electricity bills through online modes though 70 per cent of them have smartphones. Developing user-friendly mobile applications in vernacular languages, financial incentives, and consumer education are also needed to attract more consumers towards direct digital payment modes.

The high levels of consumer satisfaction stand testimony to the sustained efforts made over the last few decades by discoms. Supply duration, reliability, and quality along with bill regularity are important drivers of consumer satisfaction, which also keeps evolving. To sustain consumer trust and satisfaction, discoms need to adopt a proactive approach to resolving any outstanding issues in service delivery besides improving transparency in their overall operations.

When we were conceptualising the IRES survey, in the summer of 2019, the world was a different place. India had achieved what was considered an impossible milestone in record time—electrifying nearly all households across the length and breadth of the country and opening a world of opportunity for the hitherto unconnected to reap the benefits of household electrification—and that was celebrated widely. The latter half of 2019 was already showing signs of an economic slowdown, with declining power demand being an unmistakeable sign of times to come. The COVID-19 pandemic only helped that slide to deepen further. Newly electrified households or others are still very much connected to the grid, and they remain the only constant in these times of uncertainty. A new wave of the pandemic, further restrictions, or a protracted economic slump will likely impact consumption in other sectors quite intensely. The implications of the ongoing pandemic on various facets of the distribution system and particularly on households is only beginning to play out.

Our study finds that 2.43 per cent of the households are yet to be electrified, mainly in the rural hinterlands of northern and central India. We suggest that the discoms’ approach to electrifying these households should be based on scalable solutions that are fit for purpose and do not burden the utility with excessive capital investment or the consumer with a bill that they cannot afford. There is evidence of many who were connected to the grid but excluded later, presumably because of their inability to pay for the services of the grid. The proposed National Tariff Policy (2020) and the draft amendment to the Electricity Act (2003) call for a tariff that brings about more parity across consumer categories along with a parity in service provisions. This implies that the cross-subsidy presently enjoyed by residential consumers in many states is likely to diminish, leaving them to foot a higher bill. This will only hasten the exit of many more consumers from the grid or, even worse, drive them towards illegal access of grid services. While tariff rationalisation is much needed to provide fillip to industrial and commercial activity, in a slowing economy, support to deserving poor consumers must be sustained through budgetary support. For determining who needs support, we need to understand the needs of consumers at various economic rungs—wealth and income classes, and assess which groups need support and to what extent. This report and the underlying survey provide useful insights on this from, though more research is needed on this front.

We find that the aspirational 24x7 power for all has not been achieved in many parts of the country—neither urban nor rural. Supply hours have improved in leaps and bounds in rural areas in the key states such as Uttar Pradesh and Bihar. However, outages in the evening hours and during times of peak demand in the system still suggest that much more needs to be done. Such outages are happening despite the surfeit of power, and is, of course, tied to the financial troubles of distribution utilities, which need sustainable remediation. The top two priorities for the discoms on this front would be to maximise revenue (by streamlining the metering, billing, and collection mechanisms) to then be able to invest adequately in infrastructure as well as tune up performance management to reduce technical losses, thereby improving their overall operational performance.

We find that the reliability of supply and quality still need to catch up to achieve satisfactory levels. While these issues are concentrated in specific districts or regions, it is pertinent to point out that even in urban areas, unscheduled outages—lasting up to 12 hours—only show how the distribution utilities are flouting standards of performance (SoPs) and without consequences. We find that the average consumer, being unaware of consumer rights, does little to hold the utility accountable for unreliable supply. The onerous task of taking utilities to task is left to a few civil society organisations that represent the issues of the consumer, which is not a scalable and sustainable approach to ensure reliable electricity supply.

We propose that a technology-driven monitoring mechanism, with automated and periodic reporting on achievement of SoPs by utilities at all levels, must be put in place. We further call upon the regulators to mandate the installation of these systems in a time-bound manner and prioritise investments to enable discoms to achieve transparent reporting on supply quality and quantum. Compensation to the consumers, in cases of failure of discoms to meet the SoPs, must be time-bound and automated. The recent draft of Electricity (Rights of Consumers) Rules 2020 contain these provisions, which need to be implemented in coordination with the state government, regulators and discoms. This, of course, would require robust metering and transparency in reporting by utilities. Equally, efforts to educate consumers about their rights also need to be taken up through the right channels. Resources for consumer education provided for in the budgets of discoms are not entirely utilised effectively. Outages and unreliable supply are ultimately bad outcomes and the associated costs could be far higher than what discoms ‘save’ by not supplying the power. Studies that determine these costs must be carried out and communicated effectively to all stakeholders to help drive demand for a 24x7 reliable power supply.

We strongly believe that consumers have a role to play in making our discoms viable and improving the supply overall—they are the ones who ultimately pay the bills and help generate revenues that flow upstream to generators, fuel providers, and a host of allied sectors. We did a novel assessment of the metering, billing, and collection practices across the states. We find that in recent years there has been a phenomenal increase in metering in some large states and the universal metering metric is likely to be achieved soon. However, the main purpose of metering is to enable delivery of bills on time and ensure regular collection of consumption charges from consumers. Our survey shows that over five per cent of consumers have never received a bill and a few more of them receive bills that are not with a set periodicity. This is detrimental to the consumer–discom relationship, as timely billing and timely payment go hand in hand for continued good services. The discom though has to be the starting point for triggering an improvement in this regime. Streamlining of the MBC process as a whole in enabling delivery of bills based on metered readings is the need of the hour for discoms. There is also an urgent need to make the payment processes seamless and hassle-free for the consumer. The COVID-19 experience calls for innovation to enable some form of regular payments for services. With physical access to the few representative offices and payment centres of the discoms becoming more restricted, other modes of payments, primarily technology-enabled online payments through multiple channels that are available now, should be harnessed effectively. For this transition, consumer trust on every actor in the value chain is important and that trust begins with the electricity bill that is based on a metered reading and generated periodically.

Finally, research has shown that satisfied consumers gladly pay for the services rendered. What determines consumer satisfaction? In our assessment, duration of supply is the prime influencer. As service delivery evolves, quality of supply and even aspects like a reliable bill that informs consumers about their obligations are important in driving consumer satisfaction. We strongly believe that discoms must work towards meeting consumer expectations. This starts with building trust and improving transparency in their overall operations. Electricity in India is treated as a public good, but to operate the systems, financial viability and establishing value proposition are equally important. We expect reforms proposed in the Electricity Act Amendment Bill (2020) to create an upheaval of sorts in the discom model—more accountability but with a higher price tag.

In forthcoming studies, as part of a series of analyses of the IRES, we will deliberate on how energy efficiency is seen by residential consumers and the approach to improving penetration of efficient appliances to various categories of consumers. We will also deliberate on subsidy targeting and the fiscal room that discoms and states can create for themselves by assessing the consumer profile and determining deserving beneficiaries.

Maximising Rooftop Solar Performance by Enabling a Robust O&M Ecosystem

What Drives Rooftop Solar Installation Decisions in Indian Homes?

Building a People-centric Energy Future:

Roadmap of the methodology to assess the climate co-benefits of the SUP ban in Tamil Nadu